For insurers, “customer” is one word that encompasses individual policyholders, business owners, risk managers, agents and brokers, and others, all with different (often divergent) priorities. For reinsurers – whose primary customers are insurers themselves – “understanding the customer” is particularly challenging.

This was part of the motivation behind RiskScan 2024 – a collaborative survey carried out by Munich Re US and Triple-I. The survey provides a cross-market overview of top risk concerns among individuals across five key market segments: P&C insurance carriers, P&C agents and brokers, middle-market business decision makers, small business owners, and consumers. It explores not only P&C risks, but also how economic, political, and legal pressures shape risk perceptions.

“I get very excited when we have a chance to be in our customers’ shoes,” said Kerri Hamm, EVP and head of cyber underwriting, client solutions, and business development at Munich Re US, in a recent Executive Exhange interview with Triple-I CEO Sean Kevelighan. “To really understand how they feel about a broad range of issues from what are their most important risks to how they feel about the cost of insurance and the economic environment.”

Hamm discussed how more than one-third of respondents ranked economic inflation, cyber risk, and climate change as top concerns, identifying them as “increasing or resulting in rises of the cost of insurance.”

“When we really understand what our customers want, we can design a better product and think about whether the coverages we’re providing are meaningful to them,” Hamm said. “That can help us match pricing better to their expectations.”

One result that Hamm found “surprising” was that “legal system abuse” didn’t appear to be as widely accepted by respondents – apart from the insurance professionals – as driving up insurance costs. Kevelighan cited other research – including by Triple-I’s sister organization, the Insurance Research Council – that has found consumers to be aware of the growing influence of “billboard attorneys”.

Unfortunately, he said, “They don’t seem to be making the connection with how that’s affecting them. What we’re trying to do at Triple-I is to help them make that connection.”

Kevelighan talked about Triple-I’s education campaign around “the billboard effect” in Georgia. That campaign includes an actual billboard (“Trying to fight fire with fire,” he said), as well as a microsite called Stop Legal System Abuse. The campaign focuses on Georgia because the state tops the most recent list of places that the American Tort Reform Foundation calls“judicial hellholes”.

“We’re trying to help citizens in Georgia see that this is costing you,” Kevelighan said, adding that Triple-I has seen high engagement through the program with people in the state.

Identifying opportunities to mitigate climate risk was on the minds of “Risk Take” presenters at Triple-I’s 2024 Joint Industry Forum (JIF). Risk Takes – a new addition at JIF – are 10-minute problem/solution-oriented presentations by high-impact experts who are deeply engaged in addressing specific perils.

Inserted between panel discussions of broader issues and trends, these compact talks were tightly focused on how current challenges are being met.

Munich Re US, for example, is diving deep into understanding how consumers and insurers perceive climate-related risks. According to RiskScan 2024, a recently published survey by Munich Re US and Triple-I, more than one-third of respondents ranked climate change as a top concern, identifying it as “a key driver of insurance costs,” said Kerri Hamm, EVP and head of cyber underwriting, client solutions, and business development at Munich Re US.

However, when it comes to flood risk, the survey highlighted a substantial disconnect between concern about the peril and understanding of related insurance coverage. Despite understanding the rising severity of climate risks and their direct influence on insurance costs, many consumers erroneously believe their homeowners policy includes flood coverage or that they do not reside in an area at risk of flooding, contributing to a significant flood protection gap.

High-risk areas are only expanding, Hamm pointed out, as upsurges in flash flooding implicate more and more noncoastal properties. Increased private-sector interest in flood risk has led to new forms of flood coverage, such as a private Inland Flood Endorsement offered at Munich Re, to support these properties. Take-up rates for these insurance products remain low – underscoring the importance of consumer education and improved training for agents and brokers to encourage flood insurance sales.

“We can do better as an industry to make options available, attractive, and better known to vulnerable homeowners,” Hamm said. Education is vital, as is “developing innovative solutions that benefit our society by closing the insurance gap.”

Combining geoscience with data science is one solution, said Helge Jørgensen, CEO and co-founder of the Norway-based 7Analytics. Jørgensen discussed how, by leveraging geological and hydrological information with machine learning technology, his company develops granular data that can map out property flood risk “neighbor by neighbor,” enabling highly representative flood policies.

Beyond incentivizing private insurers to write flood coverage, this data is further “crucial for communities,” Jørgensen stressed, “because, if you have a lot of information on which areas and buildings are more exposed to flooding, then you can build resilience.”

Urban growth, particularly rising populations in higher-risk areas, render community-level resilience initiatives even more important, he noted.

Guidewire’s Christina Hupy reinforced Jørgensen’s emphasis on utilizing granular data while discussing HazardHub, a property risk data platform owned by Guidewire.

“Historically, risk data was provided only at the Census block or even ZIP code level,” Hupy said, whereas HazardHub provides comprehensive and updated geospatial data across various perils to pinpoint individual property risk levels.

In collaboration with Triple-I, HazardHub will release a report in early 2025 focusing on wildfire risk within three high-risk California counties, aiming to demonstrate how using detailed geographic data can help sustain or improve underwriting profitability within such areas.

“We’re going to need to look at mitigation in these high-risk areas as the next frontier,” Hupy said, “to spark that interest from California government and carriers” and enhance resilience “both from a customer and a business perspective” in the state.

California’s Department of Insurance helped launch this frontier last month by announcing new regulations allowing insurers to use catastrophe risk modeling to set rates, rather than limiting insurers to only historic risk data, as was the rule for decades. Insurers must also expand their coverage in riskier areas and account for resilience efforts when setting rates, which was also not previously possible.

Alongside emerging forms of insurance coverage and innovative granular data tools, such regulations empower the insurance industry to incentivize climate risk mitigation and achieve considerable progress towards eliminating the protection gap.

The efficacy of collaboration and investment by “co-beneficiaries” in resilience initiatives was a dominant theme throughout Triple-I’s 2024 Joint Industry Forum – particularly in the final panel, which celebrated leaders behind recent real-world impacts of such investments.

Moderated by Dan Kaniewski, Marsh McLennan (MMC) managing director for public sector, the panelists discussed how their multi-industry backgrounds inform their innovative mindsets, as well as their knowledge on the profound ripple effects of targeted resilience planning.

The panel included:

Jonathan Gonzalez, co-founder and CEO of Raincoat;

Bob Marshall, co-founder and CEO of Whisker Labs;

Dawn Miller, chief commercial officer of Lloyd’s and CEO of Lloyd’s Americas; and

Lars Powell, director of the Alabama Center for Insurance Information and Research (ACIIR) at the University of Alabama and a Triple-I Non-Resident Scholar.

Productive partnership

Kaniewski – who spent most of his career in emergency management, previously serving as the second-ranking official at the Federal Emergency Management Agency (FEMA) and the agency’s first deputy administrator for resilience – kicked off the panel by raising the question “how do we define success?”

He characterized success as “putting theory into practice” and “having elected officials taking steps to reduce risk and transfer some of this risk from federal, state, or local taxpayers.”

But, as participants in earlier panels and this one made clear, government efforts can only go so far without private-sector collaboration.

“It doesn’t matter who makes that investment, whether it’s the homeowner, the business owner, or the government,” Kaniewski explained. “The reality is we all benefit from that one investment. If we can acknowledge that we benefit from those investments, we should do our best to incentivize them.”

Kaniewski and Raincoat’s Gonzalez were both integral in the development of community-based catastrophe insurance (CBCI), developed in the wake of Superstorm Sandy in 2012.

“A lot of the neighborhoods that experienced flooding due to Sandy didn’t have access to insurance prior to the flooding – and then, post flooding, the government really had to step up to figure out how to keep those families in those houses,” Gonzalez said.

In collaboration with the city, a nonprofit called the Center for NYC Neighborhoods developed the concept of buying parametric insurance on behalf of these communities, with any payouts going toward helping families stay in their homes after disasters. Unlike traditional indemnity insurance, a parametric policy pays out if certain agreed-upon conditions are met – for example, a specific wind speed or earthquake magnitude in a particular area – regardless of damage. Parametric insurance eliminates the need for time-consuming claim adjustment. Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders.

In this case, Kaniewski said, success was reflected in the fact that the pilot program received sufficient funding not only for renewal but expansion, bringing needed protection to even more vulnerable communities.

Powell reinforced this sentiment in explaining ACIIR’s research on the FORTIFIED method, a set of voluntary construction standards created by the Insurance Institute for Business and Home Safety (IBHS) for durability against severe weather. The insurance industry-funded Strengthen Alabama Homes program issues grants and substantial insurance premium discounts to homeowners to retrofit their houses along these guidelines, prompting multiple states to replicate the program.

Such homes in Alabama sustained 54 to 76 percent reduced loss frequency from Hurricane Sally compared to standard homes, Powell reported, and an estimated 65 to 73 percent could have been saved in claims if standard homes were FORTIFIED.

Incentivizing contractors to learn FORTIFIED standards was especially critical, Powell explained, because they further advertised these skills and expanded the presence of FORTIFIED homes beyond the grant program.

“A lot of companies have said for several years, ‘we don’t know if we’re comfortable writing these…we haven’t seen it on the ground,’” Powell said. “Well, now we’ve seen it on the ground. We need to have houses that don’t burn down or blow over. We know how to do it, it’s not that expensive.”

Addressing concerns to drive adoption

Miller described how Lloyd’s Lab works to ease that discomfort by creating a space for businesses to nurture and integrate novel insights and products without fear. With mentor support, companies are encouraged to test new ideas while free from the usual degree of financial and/or intellectual property risks attached to innovation investments.

“It’s about having an avenue out to try,” Miller said. “Having that courage, as we continue to work together, to try to understand what’s working, what’s not, and being brave to say, ‘this isn’t working, but we can course correct.’”

Whisker Labs’ Marshall noted that numerous insurance carriers have taken a chance on his company’s front-line disaster mitigation devices, Ting, by paying for and distributing them to their customers.

Ting plug-in sensors detect conditions that could lead to electrical fires through continuous monitoring of a home’s electrical system. Statistically preventing more than 80 percent of electrical fires, communities benefit – not only by preventing individual home fires but also by providing data about the electrical grid and potentially heading off grid-initiated wildfires.

“There are so many applications for the data,” Marshall said, but “to have a true impact on society…we have to prove that we’re preventing more losses than the cost, and we have to do that in partnership with insurance carriers.”

Everyone wins if everyone plays

Cultivating innovative solutions is pivotal to enhancing resilience, the panelists agreed – but driving them forward requires more than just the insurance industry’s support.

He pointed to a project last year – funded by Fannie Mae and developed by the National Institute of Building Science (NIBS) – that culminated in a roadmap for resilience investment incentives, focusing on urban flooding.

The co-authors of the project, including Triple-I subject-matter experts, represented a cross-section of “co-beneficiary” groups, such as the insurance, finance, and real estate industries and all levels of government, Kaniewski said.

Implementation of the roadmap requires participation from communities and multiple co-beneficiaries. Triple-I and NIBS are exploring such collaborations with potential co-beneficiaries in several areas of the United States.

Triple-I recently kicked off a new webinar series featuring its Non-Resident Scholars. The first episode focused on the rising severity of natural catastrophes and innovative data initiatives these scholars are engaged in to help mitigate the impact of these perils.

Moderated by Triple-I’s Chief Economist and Data Scientist Michel Léonard, the panel included:

Phil Klotzbach, Senior Research Scientist in the Department of Atmospheric Science at Colorado State University;

Victor Gensini, meteorology professor at Northern Illinois University and leading expert in convective storm research;

Seth Rachlin, social scientist, business leader, and entrepreneur currently active as a researcher and teaching professor; and

Colby Fisher, Managing Partner and Director of Research and Development at Hydronos Labs.

“Wild and crazy”

Klotzbach discussed “the wild and crazy 2024 Atlantic hurricane season,” which he called “the strangest above-normal season on record.”

Abnormally fluctuating periods of activity this year created “a story of three hurricane seasons,” reflecting a broader trend of decreasing storm frequency and increasing storm severity, Klotzbach said.

While Klotzbach and his forecasting team’s “very aggressive prediction for a very busy season” was validated by Hurricane Beryl’s landfall as the earliest Category-5 hurricane on record — followed by Debbie and Ernesto — “we went through this period from August 20 to September 23 where we had almost nothing. It was extremely quiet.”

After extensive media coverage claiming the forecasts were a “massive bust,” along came Hurricane Helene, which developed into the “strongest hurricane to make landfall in the Big Bend of Florida since 1851.” Helene drove powerful, destructive flooding inland – most notably in Asheville, NC, and surrounding communities. Then came Hurricane Milton which was noteworthy for spawning numerous fatal tornadoes.

“Most tornadoes that happen with hurricanes are relatively weak – EF0, EF1, perhaps EF2,” Gensini – the panel’s expert on severe convective storms (SCS) – added. “Milton had perhaps a dozen EF3 tornadoes.”

Costly and underpublicized

Severe convective storms – which include tornadoes, hail, thunderstorms with lightning, and straight-line winds – accounted for 70 percent of insured losses globally the first half of 2024. And in 2023, U.S. insured SCS-caused losses exceeded $50 billion for the first time on record for a single year.

Hailstorms are especially destructive, behind as much as 80 percent of SCS claims in any one year. Yet their relative brevity and limited scope compared to large-scale disasters earns them far less public and industry attention.

“We haven’t had a field campaign dedicated to studying hail in the United States since the 1970s,” Gensini explained, “so it’s been a long time since we’ve had our models updated and validated.”

Data-driven solutions

To rectify this knowledge gap, the In-situ Collaborative Experiment for the Collection of Hail in the Plains (or ICECHIP) will send Gensini and some 100 other scientists into the Great Plains to chase and collect granular data from hailstorms next year. Beyond developing hail science, their goal is to improve hail forecasting, thereby reducing hail damage.

Gensini pointed to another project, the Center for Interdisciplinary Research on Convective Storms (or CIRCS), which is a prospective academic industry consortium to develop multidisciplinary research on SCS. Informed by diverse partnerships, such research could foster resilience and recovery strategies that “move forward the entire insurance and reinsurance industry,” he said.

Rachlin and Fisher echoed this emphasis on enhancing the insurance industry’s facilitation of risk mitigation in their presentation on Hydronos Labs, an environmental software development and consulting firm that utilizes open-source intelligence (OSINT).

The costs and variability of climate and weather information have created “a data arms race” among insurance carriers, and aggregating and analyzing publicly available information is an untapped solution to that imbalance, they explained.

The company’s end goal, Rachlin added, is to promote an insurance landscape centered around “spending less money on [collecting] data and more money using data.”

All panelists stressed the ongoing need for more reliable, comprehensive data to steer industry strategies for effective mitigation. Investments in this data now are less than the costs of post-disaster recovery that will continue to plague more and more communities in our rapidly evolving climate.

Register here to listen to the entire webinar on demand.

The need for collective action to address the property/casualty risk crisis was a recurring theme throughout Triple-I’s Joint Industry Forum in Miami – particularly during the panel on climate risk and resilience. The discussion focused heavily on what’s currently being done to address this evolving area of peril.

The panel, moderated by Veronika Torarp – a partner in PwC Strategy’s insurance practice – consisted of subject-matter experts representing a cross section of natural perils, from hurricanes and floods to wildfires and severe convective storms. They were:

Dr. Philip Klotzbach, research scientist in the Department of Atmospheric Science at Colorado State University;

Matthew McHatten, president and CEO at MMG Insurance and chairman of Triple-I’s Executive Leadership Committee;

Emily Swift, sustainable business framework senior manager at American Family Insurance; and

Heather Kanzlemar, consulting actuary at Milliman.

Part of the reason for this need to build coalitions is the diverse and overlapping causes of climate-related events and the related losses. Torarp cited a PwC study that projects the global protection gap in 2025 at $1.9 trillion, though she acknowledged that number may turn out to be “an understatement”.

Warmer, wetter, riskier

Running through the discussions of the various perils was the dynamic nature of evolving threats and the protection gap. Examples included increased inland flooding, such as the devastation caused in the rural southeast by Hurricane Helene, and damage inflicted by surprisingly intense tornadoes spun off by Hurricane Milton.

Dr. Klotzbach discussed the “very busy” 2024 Atlantic Hurricane season with its surprising impact on Asheville, N.C., and surrounding communities from Helene.

“It’s important to understand that the inland flooding threat is extremely problematic,” he said.

MMG’s McHatten emphasized the complexity of addressing flood risk, given the environmental forces driving it.

“Warmer planet, warmer ocean, more precipitation, more wind,” he said, “as well as this dynamic of atmospheric rivers and what happens to them as they start to hit higher elevations.” He pointed out how such conditions – which led to cataclysmic rains in Ashville as well as in MMG’s home state of Maine and the mountains of Vermont – are exacerbated by population trends.

“People live near water because that’s where economy and commerce was,” he said. “The ability to adapt to dynamic conditions that are changing rapidly is super-difficult. We can’t just say, ‘Raise every house six feet’ that’s near a body of water.”

Hope amid the perils

American Family’s Emily Swift discussed the state of severe convective storm risk, which she said is tending to migrate from its historic domain of the U.S. Midwest toward the Southeast.

“As we’re seeing the impact of hurricanes move further west and severe convective storms move further east, that means a lot more risk exposure to our customers who are living in those regions,” she said. “However, I think there’s a lot of hope.”

Swift talked about emerging partnerships between the insurance industry and academia — particularly work being done through Industry-University Cooperative Research Centers (IUCRC) funded by the National Science Foundation (NSF) to better understand severe convective storms and develop innovative ways of addressing the risks they pose.

“I’m optimistic that, although we don’t know quite the direction where severe convective storms are heading, we at least have diversified our risks to better manage them” – thanks, in part, to the learnings derived from these partnerships, Swift said.

Kanzlemar reinforced Swift’s optimistic tone in discussing Milliman’s work around wildfire risk. In the midst of a growing insurance availability and affordability crisis in fire-prone states – particularly California – Milliman is partnering with the Insurance Institute for Building and Home Safety (IBHS) and and stakeholders in its Wildfire Prepared Home program to gather data to help inform insurance underwriting, as well as mitigation and prevention at the community level.

“Most insurers have data on type of structure, what the roof material is, the number of stories,” Kanzlemar said, “but a lot of the granular data around eave enclosures, ember-resistant vents, that data is typically not available, and almost no insurers had that data at a community level to account for adjacent risk.”

That’s the bad news, she said, but “the good news is in the kinds of solutions we’re working toward. Most insurers were willing to consider a contributory data model like a comprehensive loss-underwriting exchange for [wildland-urban interface (WUI)] data as long as there’s sufficient participation and reciprocity. That’s an effort that we’re calling the ‘WUI Data Commons’. ”

All the panelists agreed that such collaborative, data-driven approaches that respect consumer needs and interests at the community level were going to be key to solving natural catastrophe risk in our rapidly changing future.

Cyber incidents, changes in climate, and business interruption are the chief risk concerns among key marketplace segments in the insurance industry, according to RiskScan 2024, a new survey from Munich Reinsurance America Inc. (“Munich Re US”) and the Insurance Information Institute (Triple-I) reveals.

RiskScan 2024 provides a cross-market overview of top risk concerns among individuals across five key market segments: P&C insurance carriers, P&C agents and brokers, middle-market business decision makers, small business owners, and consumers. The survey explores not only P&C risks, but also how economic, political, and legal pressures shape risk perceptions.

Methodology

To produce a compelling snapshot of cross-market views, Munich Re US and Triple-I engaged independent market researcher RTi Research in the summer of 2024 to survey 1,300 US-based individuals.

Market surveys typically focus on a single audience, but RiskScan 2024 is a multi-segment survey offering a comprehensive view of risk perceptions and yielding comparative results between audiences. The key insights present a variety of commonalities and disparities across the five distinct target segments, covering the full range of insurance buyers and sellers across the United States.

This online survey was conducted across gender, age, geographic region, household income, business revenue, and company size.

Two primary cohorts make up five segments of participants in the RiskScan research:

consumers and small business owners (n=700) and

Insurance industry participants, which included carriers, agents, and brokers as well as middle market businesses (n=600).

Research participants were presented with various risks across five segments and then asked to select their top three risk concerns.

Key Insights

More than one-third of respondents chose economic inflation, cyber incidents, and climate change as their top three concerns based on insurance risks and market dynamics. All three of these reflect post-pandemic news topics. Economic inflation has increased over the last several years. Consumers and small business owners have experienced direct impacts with increased costs and industry participants have seen these impacts on increased replacement costs and P&C insurance premiums.

There are significant disparities in the ranking results between the two primary cohorts within the research. Insurance professionals tend to identify a variety of risks and have significant awareness of all risk categories, including emerging technologies. As expected, these audiences exhibit broader knowledge and awareness of risk transfer and mitigation of new and emerging risks. Consumers identified a smaller number of risks associated with more immediate and direct impacts on themselves.

The structure of RiskScan 2024 research yields a more complete understanding of the “white space” that exists between risk perception and action. The gaps were identified along three key risk areas:

Flood risk

cyber risks, and

legal system abuse

Flood risk was also indicated as one of the chief concerns for each audience. However, consumers lack awareness that flood events are typically excluded from homeowner’s policies. Industry professionals are more aware of flood coverage exclusions, the importance of purchasing flood coverage before a flood event, and the likelihood of these events occurring.

Cyber incidents are a primary concern in all five market segments. Most audiences in the research, both consumer and commercial, feel unprepared as this threat vector is constantly emerging, expanding, and changing. Many people are knowledgeable about cyber risks and are concerned about how to mitigate new cyber threats. Troubling stories have come to light as the frequency and severity of cyber threats grow.

“The knowledge gap about insurance risks demonstrates the continued need for education of consumers and businesses, especially about flood, cyber, and legal system abuse,” says Triple-I CEO Sean Kevelighan. “Increasing knowledge will be instrumental for the collective work needed to better manage and mitigate future risks.”

The report includes additional results for each of the five primary audiences: consumers (n=500), small business owners (n=200), insurance carriers (n=200), insurance agents and brokers (n=200), and middle market businesses (n=200).

Download the full RiskScan 2024report to review the details. Triple-I aims to empower stakeholders by driving research and education on this and other key insurance topics. Follow our blog to keep abreast of these essential conversations.

The devastation wrought by Hurricane Helene in September 2024 across a 500-mile swath of the U.S. Southeast highlighted the growing vulnerability of inland areas to flooding from both tropical storms and severe convective storms, according to the latest Triple-I “State of the Risk” Issues Brief.

These events also highlight the scale of the flood-protection gap in non-coastal areas. Private insurers are stepping up to help close that gap, but increased homeowner awareness and investment in flood resilience across all co-beneficiary groups will be needed as more and more people move into harm’s way.

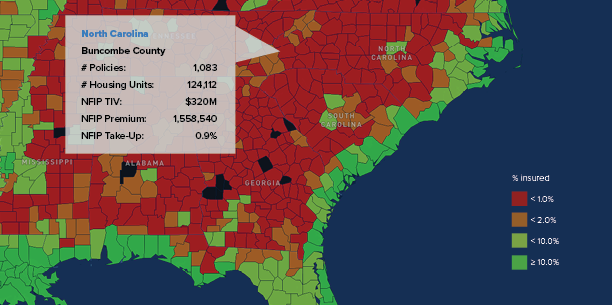

Helene dumped 40 trillion gallons of water across Florida, Georgia, the Carolinas, Virginia, and Tennessee, causing hundreds of deaths and billions in insured losses. Much of the loss was concentrated in western North Carolina, with parts of Buncombe County – home to Asheville and its historic arts district – left virtually unrecognizable. Less than 1 percent of residents in Buncombe County had federal flood insurance when Helene struck.

The experience of these states far inland echoed those of New York, New Jersey, and Pennsylvania in August 2021, when remnants of Hurricane Ida brought rains that flooded subways and basement apartments, with more than 40 people killed in those states.

“The whole swath going up the East Coast” that Hurricane Ida struck in the days after it made landfall “had less than 5 percent flood insurance coverage,” said Triple-I CEO Sean Kevelighan at the time.

Then, in July 2023, a series of intense thunderstorms resulted in heavy rainfall, deadly flash floods, and severe river flooding in eastern Kentucky and central Appalachia. Flooding led to 39 fatalities and federal disaster-area declarations for 13 eastern Kentucky counties. According to the Federal Emergency Management Agency (FEMA), only a few dozen federal flood insurance policies were in effect in the affected areas before the storm.

Low inland take-up rates largely reflect consumer misunderstandings about flood insurance. Though approximately 90 percent of all U.S. natural disasters involve flooding, many homeowners are unaware that a standard homeowners policy doesn’t cover flood damage. Similarly, many believe flood coverage is unnecessary unless their mortgage lenders require it. It also is not uncommon for homeowners to drop flood insurance coverage once their mortgage is paid off to save money.

Private insurers stepping up

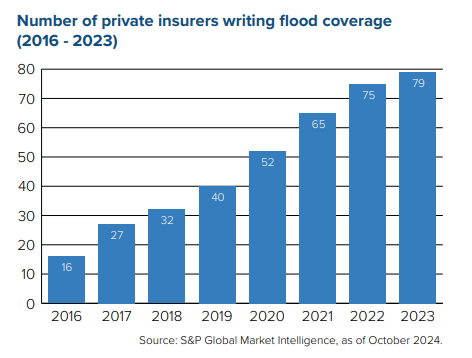

More than half of all homeowners with flood insurance are covered by NFIP, which is part of FEMA and was created in 1968 – a time when few private insurers were willing to write flood coverage. In recent years, however, insurers have grown more comfortable taking on flood risk, thanks in large part to improved data and analytics capabilities.

The private flood market has changed since 2016, when only 12.6 percent of coverage was written by 16 insurers. In 2019, federal regulators allowed mortgage lenders to accept private flood insurance if the policies abided by regulatory definitions. The already-growing private appetite for flood risk gained steam after that. Private insurers are gradually accounting for a bigger piece of a growing flood risk pie.

Insurance necessary – but not sufficient

Insurance can play a major role in closing the protection gap, but, with increasing numbers of people moving into harm’s way and storms behaving more unpredictably, the current state of affairs is not sustainable. Greater investment in mitigation and resilience is essential to reducing the personal and financial losses associated with flooding.

Such investment has paid off in Florida, where the communities of Babcock Ranch and Hunters Point survived Hurricanes Helene and Milton relatively unscathed. Babcock Rance made headlines for sheltering thousands of evacuees from neighboring communities and never losing power during Milton, which devastated numerous neighboring cities and left more than three million people without power.

Both of these communities were designed and built in recent years with sustainability and resilience in mind.

Incentives and public-private partnership will be critical to reducing perils and improving insurability in vulnerable locations. Recent research on the impact of removing development incentives from coastal areas can improve flood loss experience in the areas directly affected by the removal of such incentives, as well as neighboring areas where development subsidies remain in place.

Babcock Ranch – a small community in southwestern Florida dubbed “The Hometown of Tomorrow” – made headlines for sheltering thousands of evacuees and never losing power during Hurricane Milton, which devastated numerous neighboring cities and left more than three million people without power.

Hunters Point, a subdivision on Florida’s Gulf Coast, remained similarly unscathed during both Hurricanes Helene and Milton. Though the development is only two years old, it’s already been through four major hurricanes. Its homes were designed with an elevation high enough to avoid severe flooding and materials that make them as sturdy as possible in high winds. When the power goes out, each home turns to its own solar panels and battery system.

For residents of both communities, this news comes as no surprise; their flood-resistant infrastructure and solar panel power systems have helped them survive several storms and hurricanes with only minor damages, demonstrating the utility of disaster resilience planning.

Such planning is expensive to implement. Homes in either community can run for over a million dollars. But, as the combined costs of Hurricanes Helene and Milton rise to the tens of billions, it’s hard to overstate the long-term benefits. Every dollar invested in disaster resilience could save 13 in property damage, remediation, and economic impact costs, suggesting risk mitigation and recovery strategies will become even more essential as natural catastrophe severity increases.

Incentivizing investment

The National Flood Insurance Program (NFIP) Community Rating System (CRS) – a voluntary program that rewards homeowners with reduced premiums when their communities invest in floodplain management practices that exceed NFIP minimum standards – aims to encourage resilience. Class 1 is the program’s highest rating, qualifying residents for a 45 percent reduction in their premiums. Of the nearly 23,000 participating NFIP communities, only 1,500 participate in the CRS. Of those 1,500, only two – Tulsa, Okla., and Roseville, Calif. – have achieved the highest rating.

High ratings are difficult to secure and maintain. Homeowners in Lee County, which borders Babcock Ranch, nearly lost their discounts earlier this year due to improper post-Hurricane Ian monitoring and documentation within flood hazard areas.

Discounts in lower-rated jurisdictions, however, still equate to large premium reductions. Miami-Dade County, Fla., for instance, earned a Class 3 rating after extensive stormwater infrastructure upgrades, saving the community an estimated $12 million annually. Residents sustained minimized flooding from Hurricane Milton under these improvements, further justifying their cost.

Local mitigation efforts offer targeted resilience solutions and resources to alleviate community risks. The insurance industry-funded Strengthen Alabama Homes provides homeowners grants to retrofit their houses along voluntary standards for constructing buildings resistant to severe weather. Completed retrofits reduce post-disaster claims and qualify grantees for substantial insurance premium discounts, prompting flood-prone Louisiana to replicate the program.

Other nature-based planning exploits local flora as a source of natural hazard protection. Previous studies support conserving natural wetlands and mangroves to impede the rate and flow of flooding, leading many communities – including Babcock Ranch, which is 90 percent wetlands – to invest in green infrastructure. Reforestation and wetland restoration projects undertaken by the Milwaukee Metropolitan Sewerage District (MMSD) also promise to store or capture millions of gallons of storm and flood water, enabling risk management alongside improved quality of life for citizens.

Most resilience projects are impossible to fund or operate without stakeholder partnerships and advanced data and analytics. Insurers, who have long assessed and measured catastrophe risk utilizing cutting-edge data tools, are uniquely positioned to confront these evolving risks and present a framework for successful preemptive mitigation.

Despite warnings from two leading insurance rating agencies that Hurricane Milton weakened or threatened Florida’s recovering home insurance market, the market “can manage losses” from the Category 4 storm “and are ready to cover yet another hurricane,” if one should come this season, according to industry experts who spoke with the South Florida Sun Sentinel.

AM Best and Fitch Ratings each issued reports last week warning that Milton could stretch liquidity of Florida-based residential insurers that are primarily focused on protecting in-state homeowners. But experts closer to Florida’s insurance industry cast doubt on those assertions. One reason is the two companies don’t rate most of the domestic Florida insurers whose financial strength they question, the Sun Sentinel reported.

While cautioning that loss estimates haven’t been released yet from catastrophe modelers, Florida market experts said the state’s insurers have sufficient reinsurance capital to weather not only hurricanes Debby, Helene, and Milton but another Milton-sized storm if one emerges during the latter portion of the 2024 Atlantic season.

Karen Clark, president of catastrophe modeler Karen Clark & Co., told the Sun Sentinel, “Florida insurers and the reinsurers that protect them use sophisticated tools to understand the probabilities of hurricane losses of different sizes.”

Joe Petrelli, president of Demotech – the only rating firm that reviews the financial health of most Florida-based property insurers – said insurers can purchase additional reinsurance capacity if they use up what they purchased to get them through the year.

“Carriers will have catastrophe reinsurance in place for another event, so it should not be an issue,” Petrelli told the Sun Sentinel.

“While we expect Milton to be a larger wind loss event compared to hurricanes Debby and Helene, we do not anticipate it to be near the level of insured losses caused by Hurricane Ian,” Mark Friedlander, Triple-I’s director of corporate communications said.

Ian was a Category 4 major hurricane that made landfall in Southwest Florida in September 2022 and caused an estimated $50 billion to $60 billion in private insured losses. The estimate accounted for up to $10 billion in litigated claims due to one-way attorney fees that were in effect at the time of the storm.

“The market is in its best financial condition in many years due to state legislative reforms in 2022 and 2023 that addressed the man-made factors which caused the Florida risk crisis – legal system abuse and claim fraud,” Friedlander said. “Florida residential insurers also have adequate levels of reinsurance to cover catastrophic loss events like Milton.”

As work continues to address the harm inflicted by Hurricane Helene, researchers at Colorado State University (CSU) warn that the next two weeks “will be characterized by [tropical storm] activity at above normal levels.”

The CSU researchers define “above normal” by accumulated cyclone energy (ACE) of more than 10. This level of hurricane intensity has been reached in less than one-third of two-week periods in early October since records have been kept.

Hurricane Kirk, they wrote, is “extremely likely” to generate more than 10 ACE during its lifetime in the eastern/central Atlantic. Tropical Depression 13 has just formed and is likely to generate considerable ACE in its lifetime across the Atlantic. The National Hurricane Center is monitoring an additional area for formation in the Gulf of Mexico that should be monitored for potential U.S. impacts.

“Hurricane Kirk is forecast to track northwestward across the open Atlantic over the next few days, likely becoming a powerful major hurricane in the process,” said CSU research scientist and Triple-I Non-resident Scholar Phil Klotzbach. “The system looks to generate approximately an additional 20 ACE before dissipation, effectively guaranteeing the above-normal category for the two-week period.”

With more than 160 people confirmed dead in Florida, Georgia, South Carolina, North Carolina, Virginia, and Tennessee, Helene is now the second-deadliest hurricane to strike the mainland United States in the past 55 years, topped only by Hurricane Katrina in 2005.

Reinsurance broker Gallagher Re predicts that private insurance market losses from Helene will rise to the mid-to-high single-digit billion dollar level, higher than its pre-landfall forecast of $3 billion to $6 billion, according to Chief Science Officer and Meteorologist Steve Bowen.

As always – and with particular urgency in the wake of Helene’s devastation – Triple-I urges everyone in hurricane-prone areas to stay informed, be prepared, and follow the instructions of local authorities. We also ask that people be mindful of the potential for flood danger far inland, as reflected in the experiences of many non-coastal communities during Hurricane Ida and Helene.