Analysis based on precise, granular data is key to fair, accurate insurance pricing – and is more important than ever before in an era of increased climate-related risks. In a recent Executive Exchange discussion with Triple-I CEO Sean Kevelighan, a co-founder of Norway-based 7Analytics discussed how his company’s methodology – honed by use in the oil and gas industry – can help insurers identify opportunities to profitably write flood coverage in what might seem to be “untouchable” areas.

7Analytics uses hydrology, geology, and data science to develop high-precision flood risk data tools.

“We are four oil and gas geologists behind 7Analytics,” said Jonas Torland, who also is the company’s chief commercial officer, “and between us we’ve spent 100 years chasing fluids in the very complicated subsurface.”

Torland believes his firm can bring a new level of refined expertise to U.S. insurers seeking to pinpoint pockets of insurability against flood.

“Instead of analyzing faults and carrier beds, we’re now analyzing streams and culverts and changing land-use features,” Torland told Kevelighan. “I think the approach we bring is brilliant for problems related to climate and population migration and urban pluvial flooding in particular.”

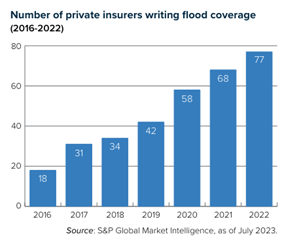

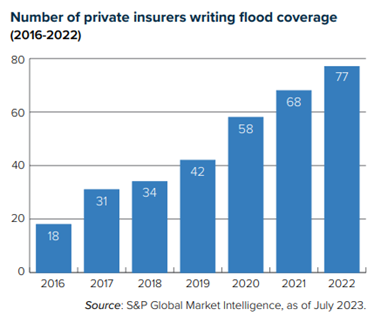

Torland said he hopes his company can help close the U.S. flood protection gap by giving private insurers the comfort levels and incentives they need to write the coverage. While more insurers have been covering flood risk in recent years, the National Flood Insurance Program (NFIP) still underwrites the lion’s share of flood risk.

NFIP’s recently reformed pricing methodology, Risk Rating 2.0 – which aims to make the government agency’s premium rates more actuarially sound and equitable by better aligning them with individual properties’ risk – has created concerns among policyholders whose premiums are rising as rates become more aligned with principles of risk-based pricing.

As the cost of participating in NFIP rises for some, it is reasonable to expect that private insurers will recognize the market opportunity and respond by applying cutting-edge data and analytics capabilities and more refined pricing techniques to seize those opportunities. This is where Torland believes 7Analytics can help, and he noted that the company had already had some positive test results in flood-prone Florida.

Kevelighan agreed that solutions like those provided by 7Analytics are what is needed to help private insurers close the flood insurance gap. Insurers are telling Triple-I as much.

“I think we can all agree that the current way we review flood risk is antiquated,” Kevelighan said. “So we’ve got to bring that new technology, that new innovation to begin changing behaviors and changing how and where we develop and how we live.”

Learn More:

Triple-I “State of the Risk” Issues Brief: Flood

Accurately Writing Flood Coverage Hinges on Diverse Data Sources

Lee County, Fla., Towns Could Lose NFIP Flood Insurance Discounts

Miami-Dade, Fla., Sees Flood-Insurance Rate Cuts, Thanks to Resilience Investment

Milwaukee District Eyes Expanding Nature-Based Flood-Mitigation Plan

Attacking the Risk Crisis: Roadmap to Investment in Flood Resilience