The 2024 U.S. wildfire season is expected to be more damaging than 2023 but below the historical average in terms of the number of fires and acres burned, according to AccuWeather.

AccuWeather’s wildfire team predicts fires across the country will burn between 4 and 6 million acres of land in 2024, below the historical average of around 7 million acres. Last year, U.S. wildfires in the United States burned 2,693,910 acres – the fewest acres burned since 1998, when around 1.3 million acres were scorched, according to the National Interagency Fire Center.

“Stormy weather lingering over the Northwest into the latter part of spring will put a lid on both wildfires and the measures humans take to suppress the fire danger,” AccuWeather reported. “Prescribed burns may be put on hold in the Northwest during May and early June due to above-average precipitation.”

California has been home to some of the worst fires in the United States over the past decade, but – thanks to a wet and stormy winter – AccuWeather says wildfires will likely be limited until later in the summer.

At the same time, AccuWeather meteorologists said the Texas Panhandle and other nearby areas of the southern Plains face a high to extreme risk of significant fires in 2024.

The annual monsoon is a key factor affecting wildfires across the southwestern United States.

“Monsoon-induced thunderstorms can be a double-edged sword,” AccuWeather says. “Downpours and an uptick in humidity can help crews battle and contain wildfires, while lightning strikes can trigger new infernos.”

AccuWeather says the start of the monsoon season in 2024 is likely to be slow at first before picking up in July and August.

Nearly 16 percent (15.7) of U.S. drivers in 2022 had auto liability insurance limits that were too low to pay for damages or injuries they caused, according to new research from the Insurance Research Council (IRC), a division of The Institutes.

The IRC report found that the underinsured motorist (UIM) rate increased from 12.6 percent in 2017, to a peak in 2020 at 16 percent, and remained elevated in 2021 and 2022. The 2022 rates, however, varied widely across the country, from 5.6 percent in the District of Columbia to 40.9 percent in Colorado. Other states with high UIM rates in 2022 included Nevada (39.4 percent), Georgia (37.3 percent), Louisiana (35.6 percent), and Kentucky (32.0 percent).

The IRC estimates are based on UIM and bodily injury (BI) liability exposure and claim count data collected from 10 major insurers representing approximately half of the U.S. private passenger auto insurance market. The ratio of UIM-to-BI claim frequencies yields a reasonable estimate of the proportion of injury-producing accidents in which the accident victim’s expenses exceeded the at-fault driver’s liability limits.

Auto insurers offer two types of coverage to protect policyholders: uninsured motorists (UM) coverage, which compensates accident victims for injuries or damage caused by a driver without liability insurance or from a hit-and-run driver; and underinsured motorists (UIM), which compensates the injured party for costs associated with injuries or property damage that exceed the at-fault driver’s liability coverage.

Once it is determined that the at-fault driver’s insurance will not fully cover damages, the accident victim files a claim with their own insurance company under their UM/UIM coverage.

“At the start of the pandemic, UIM frequency dropped as the shutdowns dramatically curtailed driving,” said Dale Porfilio, FCAS, MAAA, president of the IRC. “However, UIM frequency dropped less than BI. But by 2022, UIM claim frequency had returned to its 2019 level while BI claim frequency was still below pre-pandemic levels.”

Porfilio, who is also chief insurance officer for Triple-I, noted that, in today’s litigious society, having state minimum levels on uninsured motorist and underinsured motorist insurance does not provide adequate financial protection.

“Riskier behaviors like speeding and distracted driving, in combination with legal system abuse and economic inflation, all contribute to elevated UIM rates,” Porfilio added.

Industry stakeholders looking to keep pace with market challenges may find diversity in research the key to long-term success and resilience. A multitude of different perspectives, ideas, and solutions can enhance innovation and strategic outcomes. Join The Institutes for a webinar panel discussion of strategies for creating inclusive research spaces, addressing biases, and fostering a diverse and equitable research community, specifically in insurance.

The panel includes:

Julia Brinson, Vice President, Insurance Research, Conning

Dale Porfilio, Chief Insurance Officer for the Insurance Information Institute (Triple-I) and President of the Insurance Research Council (IRC).

Roosevelt Mosley, Jr. Principal & Consulting Actuary, Pinnacle Actuarial Resources, Inc.

Amy Cole-Smith, currently the Director for Diversity at The Institutes, moderated the discussion for this on-demand event.

Intersectionality hinges on two core fundamentals: all oppression is linked, and people can be impacted by multiple sources of interlocking oppression that converge to create a new and multi-layered struggle.

For example, intersectionality recognizes that a Black woman experiences racial and gender discrimination in ways that might be entirely different from the ways Black men face racism or White women face sexism. These differences stem from the principle that for Black women, the identities of “woman” and “Black” do not exist independently.

Intersectional research explores how gender, race, ethnicity, and other identity markers impact the data and analysis to drive valuable insights. But success requires discovering effective ways to generate those insights for the benefit of all in the customer base, not just some. Without the inclusion of intersectionality in research, disparities may continue, and market needs–along with accompanying opportunities–can go unmet.

According to Julia Brinson, applying intersectional research begins with better recruiting diverse talent. Building on her response, Roosevelt Mosley, Jr added, “Once that talent gets into our industry, we need to focus on developing and growing that talent into all areas of an organization.”

In a demonstration of how inclusion can play out around the research table, the panelists shared how their experiences influence how they approach research. Brinson, who holds a Master of Law in Insurance Law (among many other credentials), spoke about how she views insurance research problems with an eye for diversity using a “legal lens to understand the claims aspect” and how premiums may be affected.

The panelists also recommended how other researchers can effectively incorporate intersectionality into their work.

Dale Porfilio commented on how “diversity in thought and experience” can help address the industry’s challenges in this area, including “making sure products are affordable…and available to cover a broad range of risk…and integrating that with the social construct of fairness.”

However, Moseley warned that a one-size-fits-all approach to any particular category, such as race, gender, etc., won’t be sufficient to meet the requirements of intersectionality in research.

“There is a collective experience of groups, but within that collective experience, there is also significant diversity,” he said.

The common sentiment revolved around the need for “courageous conversations” and there was plenty of advice on how institutions foster an environment that promotes communication and collaboration among researchers of diverse backgrounds.

Insurers paid $1.12 billion in dog-related injury claims in 2023, according to research by Triple-I and State Farm.

The total number of dog-bite and related claims was 19,062 in 2023 – an increase of more than 8 percent from 2022 and a rise of 110 percent over the past 10 years.

However, the average cost per claim decreased from $64,555 in 2022 to $58,545 in 2023. California, Florida, and Texas had the most claims.

“Education and training for owners and pets is key to keeping everyone safe and healthy,” said Janet Ruiz, director of strategic communications at Triple-I.

“As the largest property insurer in the country, State Farm is committed to educating people about pet-owner responsibility and how to safely interact with dogs,” added Heather Paul, media relations specialist at State Farm. “It is important to recognize that any dog, including ones that are in the home, can bite or cause injury.”

During Dog Bite Prevention Week (April 7 – 13), a coalition of veterinarians, animal behavior experts, and insurance representatives urge people to understand the risks dog bites pose to people and other pets and the steps required to prevent bites from happening.

“Dogs are not just pets; they are beloved members of our households, providing joy, companionship, and comfort in our lives,” said Dr. Rena Carlson, president of the American Veterinary Medical Association (AVMA). “Together, we can nurture the bonds we share with our dogs and ensure the safety of our families and communities.”

Tips to prevent dog bites

All dogs – even well-trained, gentle dogs – can bite when provoked, especially when eating, sleeping, or caring for puppies. Therefore, it is essential to keep both children and dogs safe by preventing bites wherever possible. The National Dog Bite Prevention Week Coalition provides the following tips:

Make sure your pet is healthy. Not all illnesses and injuries are obvious, and dogs are more likely to bite if they are sick or in pain. If you haven’t seen a veterinarian in a while, schedule an appointment for a checkup to discuss your dog’s physical and behavioral health.

Prioritize proper socialization: Socialization involves gently introducing your dog to a range of settings, people, and other animals, and ensuring these experiences are positive. Whether it’s quietly observing the bustle of a park, meeting new people in a controlled manner, or getting used to the sights and sounds of your neighborhood, each positive experience builds confidence. Remember, socialization is a lifelong journey, not just a puppy phase.

Take it slow. If your dog has been mainly interacting with your family since you brought them home, don’t rush out into crowded areas or dog parks. Try to expose your dogs to new situations slowly and for short periods of time, arrange for low-stress interactions, and look for behaviors that indicate your dog is comfortable and happy to remain in the situation.

Understand your dog’s needs and educate yourself in positive training techniques. Recognize your dog’s body language and advocate for them in all situations. This will give your dog much needed skills and help you navigate any challenges you might encounter.

Be responsible about approaching other people’s pets. Ask permission from the owner before approaching a dog and look for signs that the dog wants to interact with you. Sometimes dogs want to be left alone, and we need to recognize and respect that.

Make sure that you are walking your dog on a leash and recognize changes in your dog’s body language indicating they may not be comfortable.

Always monitor your dog’s activity, even when they are in the backyard at your own house, because they can be startled by something, get out of the yard and possibly injure someone or be injured themselves.

Join the discussion on Facebook Live April 11

To assist in these efforts, members of the National Dog Bite Prevention Week Coalition—which includes the AVMA, State Farm®, Triple I, and Victoria Stilwell Positively—will be hosting a Facebook Live event on Thursday, April 11, at 1 p.m. Eastern Time.

The event, moderated by certified animal behavior consultant and broadcaster Steve Dale, will discuss training tips to help prevent bites, how to safely socialize your dog after a period of isolation, and how to recognize the warning signs that a dog may bite. In addition, the coalition will be releasing the latest dog-related injury claims data. The panelists will also be answering questions submitted by the public during the event.

Residents and police gather outside of homes in Newark, N.J., that were damaged by a 4.8 magnitude earthquake on April 5. (Photo by Spencer Platt/Getty Images)

Last week’s earthquake in Lebanon, N.J. – the strongest to hit the state in more than 200 years and which halted activity in New York-area airports and was felt from Washington, D.C., to Maine – highlighted the importance of earthquake preparedness, mitigation, and insurance in areas traditionally not associated with damaging seismic activity.

Earthquake insurance is not covered under a standard homeowners policy. According to A.M. Best, $250 million in direct premiums written for earthquake coverage was in force in Connecticut, New Jersey, and New York in 2023, accounting for less than 5 percent of U.S. earthquake coverage premiums.

Claims from last week’s event are not expected to be excessive.

“Insurers may be anticipating small claims from owners of businesses,” said Janet Ruiz, Triple-I director of strategic communication. “For example, grocery stores, where glass bottles may have fallen from shelves. But the insurance impact is likely to be limited.”

The most significant impact occurred in Newark, N.J., where three multifamily row homes were declared uninhabitable because of potential structural damage, displacing dozens of residents. However, on Saturday morning, the properties were declared structurally safe and residents were allowed to return.

Earthquakes large enough to be felt by a lot of people are relatively uncommon on the East Coast. Since 1950 there have been about 20 quakes with a magnitude above 4.5, according to the United States Geological Survey. That’s compared with over 1,000 on the West Coast.

In 2011, a 5.8 magnitude quake near Mineral, Va., shook East Coast residents over a wide swath from Georgia to Maine and even southeastern Canada. The USGS called it one of the most widely felt quakes in North American history. The quake cost $200 to $300 million in property damages, including to the Washington Monument in D.C., much of it uninsured.

Just as floods can inflict damage in areas not designated by FEMA as “flood zones,” any property where a quake can happen can undergo significant damage. Unlike in earthquake-prone states like California, however, structures typically are not designed or built with seismic events in mind. Homeowners would be well advised to discuss with their insurance professionals whether earthquake coverage is right for them.

Last week’s temblor also should drive awareness of the need for Congress to reauthorize the National Earthquake Hazards Reduction Program (NEHRP) – a federal program that helps mitigate earthquake damage to buildings and communities. The NEHRP expired in September 2023. Bipartisan legislation to reauthorize the program was introduced in January 2024.

“I’ve seen what happens when communities aren’t prepared and haven’t mitigated,” said Dr. Lucy Arendt, a professor with St. Norbert College and Chair of the NEHRP Advisory Committee on Earthquake Hazards Reduction, in a March 7 congressional briefing hosted by the National Institute of Building Sciences (NIBS). “People are displaced from their homes. Schools are closed. Businesses shutter. There’s a lot of trauma.”

Arendt said investment in knowledge, time, and money prior to a severe disaster is significantly less than the cost to help communities recover from a major threat.

“There is a resilience gap between where we are today and where we should be as a resilient nation,” said Daniel Kaniewski, a former FEMA deputy administrator and member of the NIBS Multi-Hazard Mitigation Council. “I saw firsthand the collapse of infrastructure. These are things you might not see because it’s buried underground. But without water and power, that community cannot recover. Lifeline infrastructure needs to be restored quickly and efficiently.”

Most of the built environment is not designed to withstand earthquakes. Communities with weak building codes, older housing stock, unreinforced masonry buildings, and unmitigated hazards will fare worse than others, Kaniewski said.

“This, combined with the potential severe human toll, means that any U.S. earthquake could have catastrophic consequences that would reverberate well beyond the impact zone,” he added. “Damage to manufacturing facilities, transportation nodes, and communications networks and disrupted supply chains would be among the long list of cascading failures. Massive government spending would be necessary” to repair in the aftermath of such an event.

Colorado State University hurricane researchers predict an “extremely active” Atlantic hurricane season in their initial 2024 forecast. The team cites record-warm tropical and eastern subtropical Atlantic sea surface temperatures as a primary factor for their prediction of 11 hurricanes this year.

Led by senior research scientist and Triple-I non-resident scholar Phil Klotzbach, Ph.D, the CSU Tropical Meteorology Project forecasts 23 named storms, 11 hurricanes, and five major hurricanes during the 2024 season, which starts on June 1 and continues through Nov. 30. A typical Atlantic season has 14 named storms, seven hurricanes, and three major hurricanes.

The 2023 season produced 20 named storms and seven hurricanes. Three reached “major hurricane” intensity. Major hurricanes are defined as those with wind speeds reaching Category 3, 4 or 5 on the Saffir-Simpson Hurricane Wind Scale.

“We anticipate a well above-average probability for major hurricanes making landfall along the continental United States coastline and in the Caribbean this season,” Klotzbach said. “Current El Niño conditions are likely to transition to La Niña conditions this summer/fall, leading to hurricane-favorable wind-shear conditions. Sea surface temperatures in the eastern and central Atlantic are currently at record-warm levels and are anticipated to remain well above average for the upcoming hurricane season. A warmer-than-normal tropical Atlantic provides a more conducive dynamic and thermodynamic environment for hurricane formation and intensification.”

One hurricane and two tropical storms made continental U.S. landfalls last year. Category 3 Hurricane Idalia struck Florida’s Big Bend region near Keaton Beach on Aug. 30 with wind speeds of 115 mph. It was the third hurricane, and second major hurricane, to make a Florida landfall over the past two seasons. Idalia caused storm surge inundation of 7 to 12 feet and widespread flooding in Florida and throughout the Southeast.

“The widespread damage incurred from Idalia last year highlighted the importance of being financially protected from catastrophic losses – and that includes having adequate levels of property insurance and flood coverage,” said Triple-I CEO Sean Kevelighan. “Beyond Florida, we saw significant impacts from Idalia in southern Georgia and the Carolinas. All it takes is one storm to make it an active season for you and your family, so it is time to prepare as the 2024 Atlantic hurricane season’s start nears.”

With this forecast in mind, now is ideal time for homeowners and business owners to review their policies with an insurance professional to ensure they have the right amount and types of coverage. That includes exploring whether they need flood coverage, which is not part of a standard homeowners, condo, renters or business insurance policy.

Homeowners also can make their residences more resilient to windstorms and torrential rain by installing roof tie-downs and a good drainage system. Installation of a wind-rated garage door and storm shutters also boost a home’s resilience to a hurricane’s damaging winds and may generate savings on a homeowner’s insurance premium.

Private-passenger vehicles damaged or destroyed by either wind or flooding are covered under the optional comprehensive portion of an auto insurance policy.

Inflation remains the greatest challenge for middle-market companies, according to recent research from Chubb. While the companies Chubb surveyed performed well last year, they are looking at 2024 with trepidation, with rising wages expected to continue fueling inflation. Inflation has also been affected by the Middle East conflicts, which have altered trade routes.

As a result, nearly three-quarters of companies said they would consider increasing their insurance coverage in response to rising replacement costs of their assets due to inflation.

“For companies that experienced operational disruptions, nearly a third acknowledged that they could have been covered if they had purchased available insurance,” the report says. “In addition to potentially being underinsured for inflated property and equipment values, companies often underestimate the time it will take to get back up and running after an insured loss, which points to the need for adequate business interruption coverage and more thorough and realistic business continuity plans.”

Middle-market companies have struggled with inflation since the coronavirus pandemic, partially due to changing employee dynamics. Recession and talent shortage/employee retention were also considered major risks, with 10 percent of those surveyed ranking one of these as the top concern for their companies in the coming year.

The study notes that:

More than two-thirds of companies have raised worker pay in the past year, with an average increase of 5.5 percent.

To retain talented employees, nearly half of companies have offered incentive compensation or retention bonuses and plan to continue that in the future.

Fewer than half the respondents felt they have enough cyber insurance coverage.

Nearly 40 percent of companies surveyed by Chubb expect to raise the prices of their products and services because of these factors.

Other significant findings include respondents stating that small companies are less prepared for business disruptions than mid-size and large ones. This, the study says, opens an opportunity for risk-management strategies that could reduce the need for increased coverage.

Cyber incidents reported to the FBI’s Internet Crime Complaint Center (IC3) in 2023 totaled 880,418. These attacks caused a five-year high of $12.5 billion in losses, with investment scams making up $4.57 billion, the most for any cybercrime tracked. Phishing, with 298,878 incidents tracked (down from its five-year high in 2021 of 323,972), continues to reign as the top reported method of cybercrime.

The 2023 Data Breach Report from Identity Theft Resource Center (ITRC) reveals that last year delivered a bumper crop of cybersecurity failures – 3,205 publicly reported data compromises, impacting an estimated 353,027,892 individuals. Meanwhile, supply-chain attacks increased, and weak notification frameworks further increased cyber risk for all stakeholders.

Email compromise, cryptocurrency fraud, and ransomware increase

In addition to record-high financial losses from cybercrimes overall in 2023, the report revealed trends across crime methodology and targets. Investment fraud was the costliest of all incidents tracked. Within this category, cryptocurrency involvement rose 53 percent, from $2.57 billion in 2022 to $3.94 billion. Victims 30 to 49 years old were the most likely group to report losses.

Ransomware rose 18%, and about 42 percent of 2,825 reported ransomware attacks targeted 14 of 16 critical infrastructure sectors. The top five targeted sectors made up nearly three-quarters of the critical infrastructure complaints: healthcare and public health (249), critical manufacturing (218), government facilities (156), information technology (137), and financial services (122).

Adjusted losses for 21,489 business email compromise (BEC) incidents climbed to over 2.9 billion. The IC3 noted a shift from dominant methods in the past (i.e., fraudulent requests for W-2 information, large gift cards, etc.). Now scammers are “increasingly using custodial accounts held at financial institutions for cryptocurrency exchanges or third-party payment processors, or having targeted individuals send funds directly to these platforms where funds are quickly dispersed.”

The report disclosed a $50,000,000 loss from a BEC incident In March of 2023, targeting “a critical infrastructure construction project entity located in the New York, New York area.”

The IC3 says it receives about 2,412 complaints daily, but many more cybercrimes likely go unreported for various reasons. Complaints tracked over the past five years have impacted at least 8 million people. The FBI’s recommendations for solutions to minimize risk and impact include:

Ramping up cybersecurity protocols such as two-factor authentication.

More robust payment verification practices.

Avoiding engagement with unsolicited texts and emails.

The scale of 2023 data compromises is “overwhelming.”

According to the ITRC, the surge in breaches during 2023 is 72 percent over the previous record set in 2021 and 78 percent over 2022. To add more perspective, the ITRC notes that “the increase from the past record high to 2023’s number is larger than the annual number of events from 2005 until 2020, except for 2017.”

Meanwhile, as the report highlights, two other outsized trends converged: increasing complexity and risk. The number of organizations and victims impacted by supply-chain attacks skyrocketed. The notification framework conspicuously weakened, too. Since some laws assign liability for notification to organizations owning the leaked data, the notification chain would stop there, leaving downstream stakeholders unaware. For example, a software company servicing nonprofits might duly notify its direct B2B customers but not the individuals served by the nonprofit organization.

The ITRC has been reviewing publicly reported data breaches since 2005, and it now has a database of more than “18.8K tracked data compromises, impacting over 12B victims and exposing 19.8B records.” This ninth report forecasts a bleak outlook for the coming year. Specifically, “an unprecedented number of data breaches in 2023 by financially motivated and Nation/State threat actors will drive new levels of identity crimes in 2024, especially impersonation and synthetic identity fraud.”

The faster a breach is identified and reported, the faster all potentially affected parties can take measures to minimize impact. However, reporting regulations can vary across jurisdictions and businesses, and their supply chain partners may hesitate to disclose breaches for fear of impacting revenue and brand reputation. ITRC outlines its forthcoming uniform breach notification service designed to enable due diligence, emphasizing swift action and coordination with business and regulatory authorities. The service will be offered for a fee to companies looking to better handle cyber risk in their supply chains and regulatory requirements. Other recommendations include the increased use of digital credentials, facial identification/comparison technology, and enhancing vendor due diligence.

The increased risk and rising financial losses from cyber risk likely drive growth for the cyber insurance market, which tripled in volume in the last five years. Gross direct written premiums climbed to USD 13 billion in 2022. For a quick rundown of how cyber insurance coverage supports risk management for organizations of all sizes, take a look at our cyber risk knowledge hub. To learn more about the fastest-growing segment of property/casualty, look at our recent Issues Brief.

Property owners in Lee County, Fla., could lose their flood insurance premium discounts under the National Flood Insurance Program (NFIP) Community Rating System (CRS), according to a recent announcement by FEMA.

CRS is a voluntary program that recognizes and encourages community floodplain management practices that exceed NFIP minimum requirements. Over 1,500 communities participate nationwide.

FEMA informed leaders in the affected communities – which include Cape Coral, Bonita Springs, Estero, Fort Myers Beach, and unincorporated Lee County – that they would begin losing their discounts starting October 1. Under CRS, these communities currently receive discounts of up to 25 percent. Unincorporated Lee County and the City of Cape Coral get the biggest benefit due to their Class 5 ratings. Rates will increase by approximately $300 annually for the 115,000 homeowners impacted by FEMA’s decision.

“This retrograde is due to the large amount of unpermitted work, lack of documentation, and failure to properly monitor activity in special flood hazard areas, including substantial damage compliance,” FEMA said in a statement.

FEMA officials told the Miami Herald that the problems began shortly after Hurricane Ian in 2022, when federal teams visited the communities hit the hardest and looked at the properties they thought were most likely to be substantially damaged, including older homes built in flood zones, some with previous flood damage.

“What the team found, unfortunately, is there was a lot of unpermitted work, lack of documentation,” said Robert Samaan, the regional administrator for FEMA’s Region 4, including Florida. “It was just a failure to properly monitor the activity in the special flood hazard area.”

FEMA shared with the Herald three letters it sent Lee County in 2023 — one in February, one in June and one in December — asking for information on the number of damaged homes and warning that not providing the information could result in the county losing its flood insurance discounts.

In recent months, a number of Florida communities, including Miami-Dade County, have benefited from lower flood insurance premiums as a result of improved CRS scores that reflect resilience-related investment. CRS has become particularly beneficial as NFIP pricing reforms – known as Risk Rating 2.0 –that more closely align premium rates with property-specific risks – have contributed to rising premiums for some property owners. Before these reforms, it was not uncommon for lower-risk owners to be subsidizing higher-risk ones through their premium rates.

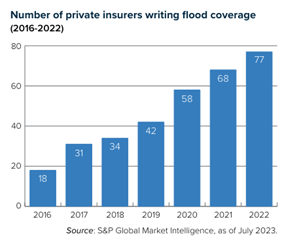

Rising NFIP rates have been accompanied by another trend: increased involvement by private insurers in the flood insurance market.

“Florida has the most robust private flood insurance market in the United States, which provides consumers with numerous options for coverage,” said Mark Friedlander, director of corporate communications for Triple-I. “Nearly a third of Florida flood policies are written by private carriers, and many private flood insurers offer better pricing and more robust policies than NFIP. It’s worth taking the time to shop for coverage and obtain multiple quotes.”

As recently as 2018, private insurers provided only 3 percent of flood coverage in Florida.

This growth mirrors a national trend. Between 2016 and 2022 the total flood market grew 24 percent – from $3.29 billion in direct premiums written to $4.09 billion – with 77 private companies writing 32.1 percent of the business, up from 18 companies writing 12.5 percent. Private insurers are accounting for a bigger piece of a growing pie.

Florida’s Office of Insurance Regulation has heavily promoted the availability of private flood insurance in the state over the past several years, and many private flood insurers are domiciled in the state, Friedlander said.

“We are committed to helping these communities take appropriate remediation actions to participate in the Community Rating System again and work towards future policy discounts,” FEMA said in its statement.

Earlier this year, Sea Isle City, N.J., had its Class 3 rating restored after a brief demotion in 2023. Sea Isle City and Avalon are the only towns in the state to have Class 3 ratings.