By Lewis Nibbelin, Research Writer, Triple-I

Organizations across the insurance value chain are navigating an increasingly complex risk landscape, demanding more integrated approaches to resilience shared among all segments of the property/casualty (P/C) market, according to RiskScan 2026, a new research study from Munich Re US and Triple-I.

Based on survey data from more than 1,700 participants in the United States and United Kingdom, RiskScan 2026 explores risk perceptions and exposures across five key market segments:

- P/C insurance carriers,

- P/C agents and brokers,

- Middle-market decision makers,

- Small-business owners, and

- consumers.

Comprising two in-depth reports, the study builds on the previous RiskScan 2024 and features a new report highlighting global specialty market perspectives and insights.

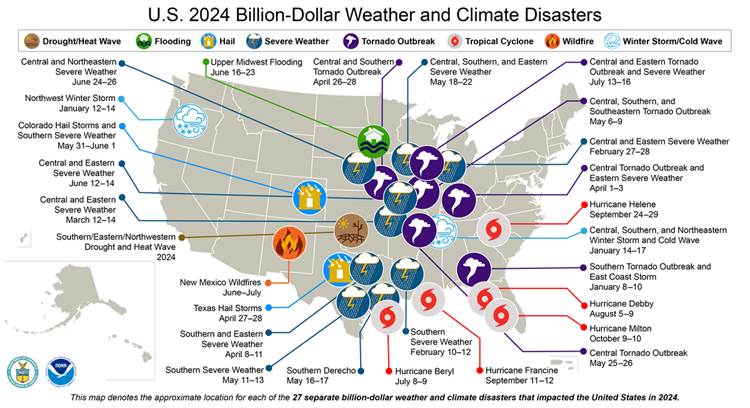

Across all audiences, cyber incidents, economic pressures, and AI emerged as chief concerns, indicating insurers and their customers are largely aligned on risks reshaping the market. Increasing frequency and severity of natural catastrophes also ranked high, particularly for perils traditionally associated with less catastrophic loss, such as wildfires, flooding, and severe convective storms.

“The real challenge – and opportunity – is in understanding how these forces intersect,” said Sabrina Hart, president and CEO of Munich Re Specialty North America. “A cyber event can trigger operational disruption, a climate event can cascade through supply chains, and legal inflation can magnify losses well beyond the initial event.”

Growing consumer awareness

While knowledge gaps remain, policyholders are becoming more aware of these connections. Consumers and businesses who participated in the 2024 survey, for instance, primarily did not identify legal system abuse as an insurance cost driver – a trend middle-market decision makers and small business owners reversed in the updated study.

Such responses suggest industry stakeholders increasingly recognize the long-term impacts of risks, rather than focus on the short-term disruptions of individual events. Economic conditions play a leading role in this shift as “a multiplier of insurance risk, affecting affordability, claims severity, capital allocation, and long-term market stability across the insurance value chain,” explained Michel Léonard, Triple-I’s chief economist and data scientist.

Flood and cyber take-up still low

Despite growing awareness, consumers continued to express less concern about flood than insurance professionals and businesses, in part reflecting misconceptions about flood risk and policy exclusions and limitations. Many consumers as well as small business owners are unaware that homeowners’ and commercial property insurance do not typically cover flood damage. Consumers may also believe flood coverage is unnecessary unless their mortgage lenders require it or drop their flood insurance coverage once their mortgage is paid off to save money.

Similarly, though all market segments considered cyber incidents a significant concern, the report notes that cyber take-up rates in the small commercial and personal line spaces remain low. Misunderstandings surrounding cyber risk coverage options and benefits help fuel this discrepancy, revealing a gap between insurer perceptions of product value and that of their customers.

“The protection gaps highlighted in this research underscore the urgent need to better educate consumers and businesses,” said Triple-I CEO Sean Kevelighan. “As flood, cyber, and other interconnected exposures continue to evolve, the industry has an important opportunity to strengthen public understanding, close protection gaps, and work collaboratively with consumers, policymakers, businesses, and communities to better predict, prepare, and prevent ever increasing risks.”

Learn More:

Bridging the Cyber Risk Resilience Gap Among Insurance Carriers

Cyber Claim Severity Surges as AI, Litigation Accelerate Risk

Legal System Abuse Awareness Campaign Spreads Across U.S.

Take Care in Addressing Homeowners’ Premiums, Bloomberg Cautions Policymakers

Inflation, Replacement Costs, Climate Losses Shape Homeowners’ Insurance Options