By William Nibbelin, Senior Research Actuary, Triple-I

The U.S. Property & Casualty insurance market is expected to continue its trajectory of improving underwriting results in 2024 into 2025 and 2026, according to the latest projections by actuaries at Triple-I and Milliman. The latest report – Insurance Economics and Underwriting Projections: A Forward View – was released during Triple-I’s January 16 members-only webinar.

Year-over-year gains in net written premium increases and quarter-over-quarter loss ratios are primarily due to better-than-expected Q3 performance in personal auto.

The 2024 underlying economic growth for P&C ended slightly below U.S. GDP growth at 2.3 percent versus 2.5 percent year over year. A further economic milestone occurred in 2024, with the number of people employed in the U.S. insurance industry surpassing three million.

Michel Léonard, Ph.D., CBE, chief economist and data scientist at Triple-I, noted P&C underlying economic growth is expected to remain above overall GDP growth in 2025 (2.3 percent versus 2.1 percent) and 2026 (2.6 percent versus 2.0 percent) as lower interest rates continue to revive real estate and contribute to higher volume for homeowners’ insurance and commercial property.

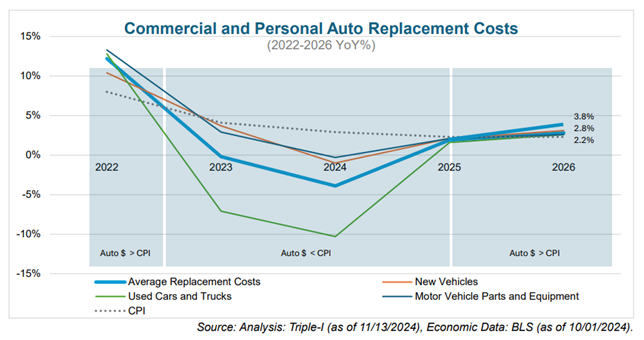

“This is an improvement on our 2025 P&C underlying growth expectations from second half of 2024,” Léonard said. “The pace of increase in P&C replacement costs is expected to overtake overall inflation in 2025 (3.3 percent versus 2.5 percent). This aligns with our earlier expectations from the second half of last year.”

Personal vs. commercial lines performance

The 2024 net combined ratio for the P&C industry is projected to be 99.5, a year-over-year improvement of 2.2 points, with a net written premium (NWP) growth rate of 9.5 percent. Combined ratio is a standard measure of underwriting profitability, in which a result below 100 represents a profit and one above 100 represents a loss. Personal lines 2024 net combined ratio estimates improved by nearly 1 point, while the commercial lines 2024 estimates worsened by 1.2 points.

Dale Porfilio, FCAS, MAAA, Triple-I’s chief insurance officer, expanded upon the dichotomy of commercial and personal lines results.

“Commercial lines continue to have better underwriting results than personal lines, but the gap is closing,” Porfilio said. “The impact from natural catastrophes such as Hurricane Helene in Q3 2024 and Hurricane Milton in Q4 2024 significantly impacted commercial property. The substantial rate increases necessary to offset inflationary pressures on losses have driven the improved results in personal auto and homeowners.”

Personal auto and homeowners are each projected to have improved 6.1 points over 2023, with a 2024 net combined ratio of 98.8 and 104.8, respectively. NWP growth rate for personal lines is expected to surpass commercial lines by 9 points in 2024, with personal auto leading at 14.0 percent, the second highest in over 15 years.

Jason B. Kurtz, FCAS, MAAA, a principal and consulting actuary at Milliman – a premier global consulting and actuarial firm – elaborated on profitability concerns within commercial lines.

“Commercial auto continues to remain unprofitable,” he said. “The 2024 direct incurred loss ratio through Q3 is only marginally improved relative to 2023 and is the second highest in over 15 years.”

Hurricane Milton is projected to be the worst catastrophic event for commercial property since Hurricane Ian in 2022 Q3, driving higher-than-expected losses and subsequently increasing the commercial property projected 2024 net combined ratio up 3.3 points to 91.2, which is also 3.3 points worse than 2023. During the webinar, commercial property forecasts were also shared for the fire and allied and inland marine sub-lines.

Continued worsening in general liability

General liability’s projected 2024 net combined ratio of 103.7 is 3.6 points worse than actual 2023 experience. Kurtz said the line has seen significantly worsening, with each quarterly loss ratio in 2024 worse than 2023 year over year.

“The 2024 direct incurred loss ratio through Q3 is the highest in over 15 years,” Kurtz said. “As a result, we have increased our expectations for 2025 and 2026 net written premium growth, as the industry responds to the worsening 2024 performance.”

Continuing the discussion on general liability, Emma Stewart, FIA, chief actuary at Lloyds added that U.S. general liability has experienced material deterioration in loss ratios and a slowing down of claims development.

“A large driver of this has been the post-underwriting emergence of heightened social inflation, or more specifically, legal system abuse and nuclear verdicts,” Stewart said. “If these trends continue to increase, reserves on this class can be expected to deteriorate further.”

Workers comp loss-cost preview

Ending with workers compensation, Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance, provided a preview of this year’s average loss-cost changes and discussed the long-term financial health of the workers compensation system.

“The 2025 average loss cost decrease of 6 percent is moderate, which will inevitably have implications on the overall net written premium change,” Glenn said. She added that the –6 percent average loss cost level change in 2025 is notably different than the -9 percent average seen in 2024, the largest average decrease since before the pandemic.

“Payroll for 2025 will develop throughout the year resulting from both wage and employment levels. Therefore, overall premium will become clearer as the year progresses,” she said.