Even as California moves to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing, the state’s risk profile continues to evolve in ways that underscore the importance of risk-based insurance pricing and investment in mitigation and resilience.

Triple-I’s latest “State of the Risk” Issues Brief discusses this changing risk environment and the impact of Proposition 103 – a three-decades-old measure that has made it hard for insurers to profitably write coverage in the state. In a dynamically evolving risk environment that includes earthquakes, drought, wildfire, landslides, and — in recent years, due to “atmospheric rivers” — damaging floods, Proposition 103 has prevented insurers from using the most current data and advanced modeling technologies. Instead, it has required them to price coverage based on historical data alone.

It also has restricted accurate underwriting and pricing by not allowing insurers to incorporate the cost of reinsurance into their pricing. Insurers use reinsurance to maximize their capacity to write coverage, and reinsurance rates have been rising for many of the same reasons as primary insurance rates. If insurers can’t reflect reinsurance costs in their pricing – particularly in catastrophe-prone areas – they must pay for these costs from policyholder surplus, reduce their market share in the state, or do both.

Proposition 103 also has impeded premium rate changes by allowing consumer advocacy groups to intervene in the rate-approval process. This makes it hard to respond quickly to changing market conditions, resulting in approval delays and rates that don’t accurately reflect current (let alone future) risk. It also drives up legal and administrative costs.

This has led, in some cases, to insurers deciding to limit or reduce their business in the state. With fewer private insurance options available, more Californians are resorting to the state’s FAIR Plan, which offers less coverage for a higher premium.

This isn’t a tenable situation.

In September 2023, California Insurance Commissioner Ricardo Lara announced a Sustainable Insurance Strategy for the state that includes allowing insurers to use forward-looking risk models that prioritize wildfire safety and mitigation and include reinsurance costs into their premium pricing. In exchange, insurers must cover homeowners in wildfire-prone parts of the state at 85 percent of their statewide coverage.

Issues around property insurance affordability are not confined to California. They’ve been a long time in the making, and they won’t be resolved overnight.

“Any sustainable solutions will have to rest on actuarially sound underwriting and pricing principles,” the Triple-I brief says. “Unfortunately, too often, the public discourse frames the risk crisis as an `insurance crisis’ – conflating cause with effect. Legislators, spurred by calls from their constituents for lower insurance premiums, often propose measures that would tend to worsen the problem because these proposals generally fail to reflect the importance of accurately valuing risk when pricing coverage.”

California’s Proposition 103 and the federal flood insurance program prior to its Risk Rating 2.0 reforms are just two examples, according to Triple-I.

2023 was another year with high-risk climate and weather-related challenges, with 2024 positioned to pose its own challenges.

Indeed, 2023 was the warmest year for the globe since 1850 — when these records were first made. The temperature in 2023 was over two degrees Celsius above the 20th Century average, with the 10 warmest years in recorded history occurring from 2014-2023. Record-setting temperatures hit areas across Canada, the southern United States, Central America, South America, Africa, Europe, Asia, as well as parts of the Atlantic Ocean, the Indian Ocean, and South Pacific Ocean.

These shifts in global weather – combined with changing population and other dynamics – have played a powerful role in the risk of disasters.

Costs are high

In the United States, Allianz estimates, extreme weather events now cost the country $150 billion a year, making these perils “key threats” for organizations. However, larger companies are leading a response to these risks by transforming their business models to low carbon, while also creating new and improved plans to respond to climate events. Allianz notes that supply-chain resilience is a crucial area of focus for the coming year.

“Although this year’s Allianz Risk Barometer results on climate change show that reputational, reporting, and legal risks are regarded as lesser threats by businesses,” said Denise De Bilio, ESG Director, Risk Consulting, Allianz Commercial, “many of these challenges are interlinked.”

According to Allianz, exposure remains highest for utility, energy, and industrial sectors. Last year’s wildfires in Canada limited oil and gas output to 3.7 percent of national production. Water scarcity is now also considered to be a threat.

Promising developments

As Triple-I reported in late 2023, despite all the concern regarding climate risk, certain weather-related disasters actually declined in the past year. This includes U.S. wildfire, which saw its lowest frequency and severity in the past two decades, despite catastrophic losses in Washington State, Hawaii, Louisiana, and elsewhere, according to a Triple-I Issues Brief. California – a state often considered synonymous with wildfire – last year experienced its third mild fire season in a row.

Homeowners insurance rates in California, as elsewhere in the United States, have been rising. Some of this trend is due to wildfires and construction in the wildland-urban interface, which put increased amounts of expensive property at risk. According to Cal Fire, five of the largest wildfires in the state’s history have occurred since 2017.

Much of California’s problem, however, is related to a 1988 measure – Proposition 103 – that severely constrains insurers’ ability to profitably insure property in the state. Late in 2023, California Insurance Commissioner Ricardo Lara announced a package of executive actions aimed at addressing some of the challenges included in Proposition 103.

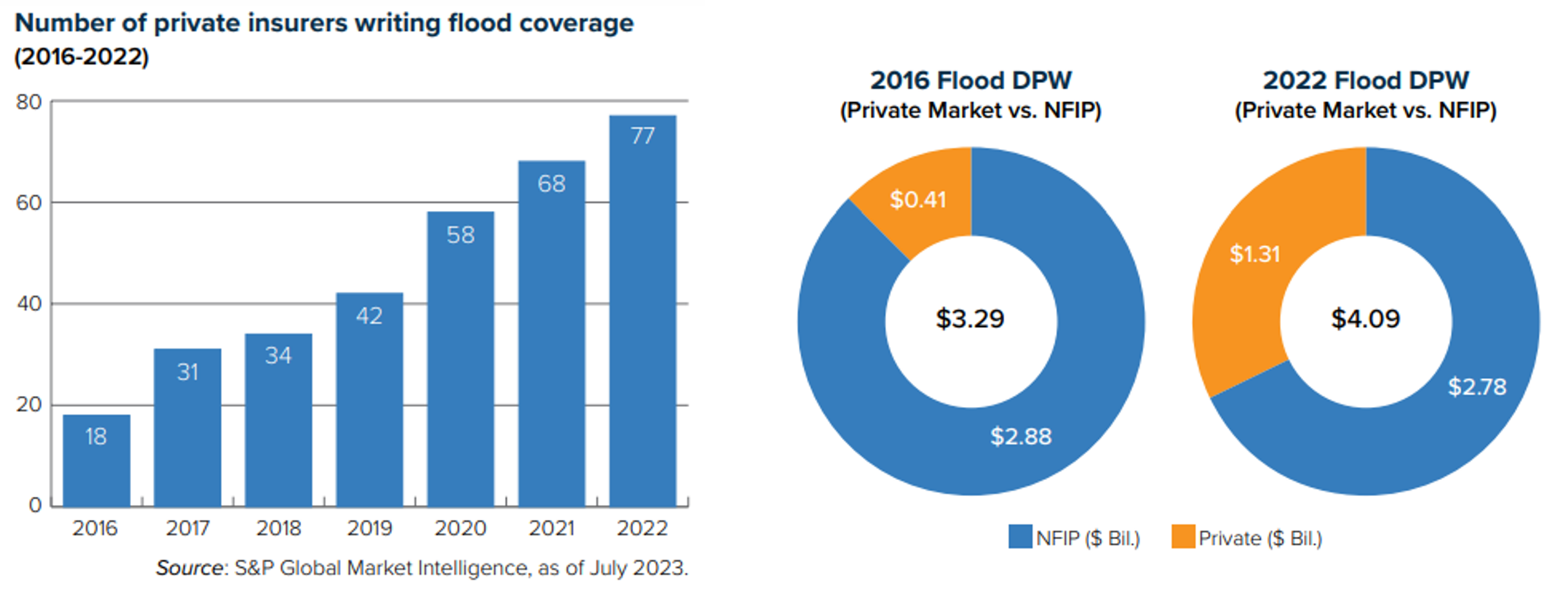

Flood remains a severe and increasing peril in the United States. While the federal government remains the main source of insurance coverage through FEMA’s National Flood Insurance Program (NFIP), the private insurance market is increasingly stepping up to assume more of the risk. As Triple-I has reported, between 2016 and 2022, the total flood market grew 24 percent – from $3.29 billion in direct premiums written to $4.09 billion – with 77 private companies writing 32.1 percent of the business. As the charts below make clear, private insurers are accounting for a bigger piece of a growing pie.

This is an important development, as the growing private-sector involvement in flood can reasonably be expected to result, over time, in greater availability and affordability of flood insurance as the peril increases and NFIP – through increased reliance on risk-based pricing – spreads the cost of coverage more fairly among property owners. Historically, the system often subsidized coverage for higher-risk homes, to the detriment of lower-risk property owners. With NFIP premium rates rising to more accurately reflect the risk assumed, private insurers – armed with increasingly sophisticated data and analytical tools – are better equipped than ever to identify opportunities to write more business.

Much yet to be done

Growing awareness and action to address climate-related risk is promising, but the crisis is far from over. In several U.S. states, insurance affordability and even availability are being affected, and much of the conversation around this topic confuses cause with effect. Rising insurance rates and constrained underwriting capacity is a result of the risk environment – not a cause of it.

Investment in mitigation and resilience is necessary, and this will require collective responsibility from the individual and community levels up through all levels of government. It will require public-private partnerships and appropriate alignment of investment incentives for all co-beneficiaries.

Communities, businesses, and government at all levels to invest in mitigating flood risk and in improving resilience.

It’s important to amplify this message, especially in light of a recent proposal by Rep. Adam Schiff that would, among other things, disband NFIP and require property/casualty insurers to provide “all-risk policies” based on coverage thresholds and rating factors dictated by a board in which the insurance industry is only nominally represented. Last year’s budget uncertainty – in which a potential government shutdown was threatened – left open the very real possibility of funding for NFIP expiring if Congress failed to reach a deal.

“Federal policies and programs, including NFIP, are essential,” said Daniel Kaniewski, managing director, public sector, for Marsh McLennan in his testimony. “But all disasters are local, and so too are resilience investment decisions.”

Before joining Marsh McLennan, Kaniewski was the second-ranking official at FEMA, where he was the agency’s first deputy administrator for resilience.

“To increase the resilience of communities against the pervasive risk of flooding,” Kaniewski testified, “we believe that risk transfer— including from the NFIP, private flood insurance, reinsurance, and parametric insurance — should be paired with risk reduction.”

In this regard, Kaniewski emphasized NFIP’s Community Rating System (CRS), which encourages and rewards community floodplain management practices that exceed the NFIP’s minimum requirements. He cited Tulsa, Okla., as one of two U.S. communities to have achieved the highest CRS rating (the other is Roseville, Calif.), making residents eligible for the program’s greatest flood insurance discount of 45 percent.

Even without achieving the maximum rating, citizens save on flood insurance when their communities invest in resilience. For example, Miami-Dade County, Fla., recently became the latest jurisdiction in the hurricane- and flood-prone state to benefit from CRS program. The county’s new Class 3 rating will result in an estimated $12 million savings annually by giving qualifying residents and business owners in unincorporated parts of the county a 35 percent discount on flood insurance premiums.

Last year, 17 other Florida jurisdictions achieved Class 3 ratings. In Cutler Bay – a town on Miami’s southern flank with about 45,000 residents – the average premium dropped by $338. Citywide, that represented a savings of $2.3 million.

Unfortunately, only 1,500 communities nationwide participate in CRS, underscoring the importance of awareness-building, education, and collaboration.

Kaniewski also highlighted the opportunity presented by community-based catastrophe insurance (CBCI), which uses parametric insurance to provide coverage to local government entities that wish to cover a group of properties. Such programs enhance financial resilience by simultaneously providing affordable coverage and creating incentives for risk reduction.

“Our recent CBCI pilot in New York City was developed in partnership with the City of New York and several nonprofit and insurance industry partners and funded by the National Science Foundation,” Kaniewski said. “It provides a level of financial protection for low-to-moderate-income households that previously lacked flood insurance.”

Kaniewski called on other industries – such as finance and real estate – to encourage flood resilience investments, along with the insurance industry and all levels of government. He cited the recent roadmap for resilience incentives issued by the National Institute of Building Sciences (NIBS) – funded by Fannie Mae and co-authored by representatives of a cross-section of “co-beneficiary industries” – that focused on residential structures prone to flooding. Triple-I subject-matter experts were co-authors on the NIBS project.

Sen. Tim Scott of South Carolina, committee co-chair – along with Sen. Sherrod Brown of Ohio – spoke from the perspective of a former insurance professional who has sold flood insurance about his state’s recent investment in mitigation.

“In 2023, the state’s budget included significant funding for mitigation efforts that would reduce flood damage from future storms,” Scott said.“Backing up that investment, the South Carolina Office of Resilience released a nationally praised Statewide Risk Reduction Plan, identifying the communities most vulnerable to floods and targeting mitigation resources to protect those residents. These are local solutions to local challenges – and they will make a huge difference in the lives of South Carolinians.”

While solutions that work in South Carolina might not work in other states, Scott said, “I’m confident that similar, locally based solutions and approaches could make a huge difference.”

Sen. Katie Britt of Alabama invited Kaniewski to elaborate on her state’s Strengthen Alabama Homes program, which provides grants and insurance discounts to homeowners who make qualifying retrofits to their houses. Britt cited research that found the program had “directly resulted in lower insurance premiums and higher home resale values.”

Kaniewski spoke in detail about Alabama’s efforts, including Strengthen Alabama Homes – which, he pointed out, is now being emulated by other states, including hurricane- and flood-prone Louisiana. He also cited by name the author of the research Britt referenced – Dr. Lars Powell, executive director of the Alabama Center for Insurance Information and Research at the University of Alabama and a Triple-I Non-resident Scholar – for producing “the first study that I’ve seen that gives empirical data — real evidence that mitigation pays.”

Steve Patterson, mayor of Athens, Ohio, described a range of nature-based solutions his city has taken – from rerouting the Hocking River, which runs through the middle of the city, to removing invasive plants and restoring native trees along the bank.

“That’s been very effective in reducing flooding in different neighborhoods throughout the city,” Patterson said. “There are a lot of things cities and villages can do.”

The work done by Athens – like green infrastructure work by the Milwaukee Metropolitan Sewerage District in Wisconsin and municipal entities – offers opportunities to reduce flood risk while improving quality of life for citizens. But, as Patterson points out, not all municipalities have the financial capacity to engage in such projects.

That is where the engagement of co-beneficiaries of resilience investment as partners becomes so crucial.

Homes with more modern roofs were able to avoid significant damage from Hurricane Ian, compared with those with older roofs, according to a recent study by the Federal Emergency Management Agency (FEMA).

Of the 200 homes surveyed, 90 percent with roofs installed before 2015 had roof damage, as opposed to 28 percent for those installed after 2015, when Florida imposed new ordinances regarding how roofs are attached to houses and how waterproof they need to be. Indeed, when Hurricane Ian made landfall at Cayo Costa, a barrier island in Lee County, Fla., on Sept. 28, 2022, it damaged 52,514 homes and other structures in the area, causing an estimated $55 billion in insured losses in 2024 dollars.

Some of this damage, according to the data, could have been mitigated by updated roofs.

History tells the same story

After the devastation of Hurricane Andrew in 1992, Florida took the initiative to develop innovative plans to prevent hurricane damage. These changes further came into effect in 2002, with a new focus on roofing. However, there were inconsistencies in the quality of the roofing.

“The 1970s-era homes performed better than some of the post-2002 new building code homes because of the sealed roof deck,” Leslie Chapman-Henderson, president of the Federal Alliance for Safe Homes, told The Miami Herald. “It was a nominal cost (to reinforce the roof) and a simple thing to do, but it made a huge difference.”

Now, with a renewed focus on metal sheet roofs—which bear the brunt of storms more resiliently than asphalt shingle roofs—FEMA’s data could drastically change the way in which homes are built, and how insurers are responding to fraudulent claims.

Insurance scams set progress back

Insurers are forced to raise the price of coverage in hurricane-prone areas in Florida because of a rash of schemes to deliberately damage roofs to qualify them for insurance claims, a persisting trend.

“Fraud drives insurance rates up and harms all Florida policyholders,” Citizens Property Insurance CEO Tim Cerio said. Still, implementing the changes suggested by the FEMA study may help alleviate some of the concerns posed by insurers—and help homeowners.

“When you’re looking at a home and evaluating its ability to survive a hurricane, the health of the roof is the first question to ask,” said Chapman-Henderson. “It not only increases your performance in the hurricane itself, but in the current environment it can help save you money on your insurance.”

Legislation proposed by U.S. Rep. Adam Schiff (D-Calif.) to create a federal “catastrophe reinsurance program” raises several concerns that warrant scrutiny and discussion – starting with the question: Does what’s being proposed even qualify as insurance?

If enacted into law, the bill would establish a “catastrophic property loss reinsurance program…to provide reinsurance for qualifying primary insurance companies.” To qualify, insurers would have to offer:

An all-perils property insurance policy for residential and commercial property, and

A loss-prevention partnership with the policyholder to encourage investments and activities that reduce insured and economic losses from a catastrophe peril.

The proposed program would phase in coverage requirements peril by peril over several years and discontinue FEMA’s National Flood Insurance Program (NFIP). It would set coverage thresholds and dictate rating factors based on input from a board in which the insurance industry is only nominally represented.

And nowhere in the 22-page proposal do any of the following words or phrases appear:

“Actuarial soundness”;

“Risk-based pricing”;

“Reserves”; or

“Policyholder surplus”.

Actuarially sound risk-based pricing and the need to maintain adequate reserves and policyholder surplus to ensure financial strength and claims-paying ability are the bedrock of any insurance program worthy of the name – not technical fine print to be worked out down the road while existing mechanisms are being dismantled and market forces distorted through government involvement.

Insurance is a complicated discipline, and prior federal attempts at providing coverage have struggled to balance their goal of increasing availability and reducing premiums against the need to base underwriting and pricing on actuarially sound principles to ensure sufficient reserves for paying claims.

Actuarially sound risk-based pricing and the need to maintain adequate reserves and policyholder surplus…are the bedrock of any insurance program worthy of the name – not technical fine print to be worked out down the road…

Sean Kevelighan, CEO, Triple-I

Learn from history

NFIP is a strong case in point. Created in 1968 to protect property owners for a peril that most private insurers were reluctant to cover, NFIP’s “one-size-fits-all” approach to underwriting and pricing has led to the program now owing more than $20 billion to the U.S. Treasury because it lacked the reserves to fully pay claims after major events like Hurricane Katrina and Superstorm Sandy. It also often led to lower-risk property owners unfairly subsidizing coverage for higher-risk properties.

Having thus learned the importance of risk-based pricing, NFIP has changed its underwriting and pricing methodology. The new approach – Risk Rating 2.0, announced in 2019 and fully implemented as of April 1, 2023 – more equitably distributes premiums based on home value and individual properties’ flood risk. As a result, premiums of previously subsidized policyholders – particularly in coastal areas with higher values – have risen, leading to outcries from many higher-risk owners who have seen their subsidies reduced.

In addition to leading to fairer pricing, Risk Rating 2.0 – by reducing market distortions – increases incentives for private insurers to get involved. For a long time, private insurers considered flood an untouchable peril, but improved data modeling and analytical tools have increased their comfort writing this business. As the charts below show, private insurers have been playing a steadily increasing role in recent years, covering a larger percentage of a growing risk pool.

Over time, this trend should lead to greater availability and affordability of flood insurance coverage.

Rather than incorporating the lessons generated by NFIP’s experience with a single peril, Rep. Schiff’s proposal would discontinue the reformed flood insurance program while adding a new layer of complexity to coverage across all perils and casting into question the future of various state insurance programs and residual market mechanisms currently in place.

Time-tested principles

Any attempt by the federal government to address insurance availability and affordability concerns must be made with an understanding of how insurance works – from pricing and underwriting to reserving and claim settlement. For example, the Schiff bill proposes piloting an all-perils policy with a term of five years. There are good reasons for property/casualty policies to be written with a one-year term. Specifically, the conditions that affect claims costs can change quickly, and insurers – as referenced above – must set aside sufficient reserves to be able to pay all legitimate claims. If they cannot revisit pricing annually, the financial results could be disastrous.

“Who would have thought in 2019 that replacement costs would increase 55 percent within three years?” asked Dale Porfilio, Triple-I’s chief insurance officer. Supply-chain disruptions related to the COVID-19 pandemic and Russia’s invasion of Ukraine contributed to just such a replacement-cost spike. “Requiring five-year terms for policies would have led to a massive drain on policyholder surplus.”

Policyholder surplus is the financial cushion representing the difference between an insurer’s assets and its liabilities.

In announcing his proposed legislation, Rep. Schiff said it is intended to “insulate consumers from unrestrained cost increases by offering insurers a transparent, fairly priced public reinsurance alternative for the worst climate-driven catastrophes.”

This language ignores the fact that, under state-by-state regulation, premium rate increases are anything but “unrestrained” and ratemaking is based on actuarially sound principles that are transparent and fair. Property/casualty insurance already is one of the most heavily regulated industries in the United States.

Consumers deserve real solutions

Policyholders have legitimate concerns about affordability and, in some cases, availability of insurance. These concerns can create pressure for political leaders at both the state and federal levels to advance measures that are perceived as promising to help. Unfortunately, many recent proposals begin by mischaracterizing current trends as an “insurance crisis,” as opposed to what they really represent: A risk crisis.

Insurance premium rates tend to move in line with the frequency and severity of the perils they cover. They also are affected by factors like fraud and litigation abuse; climate, population, and development trends; and global economics and geopolitics. That is why insurers hire actuaries and data scientists and employ cutting-edge modeling technology to ensure that insurance pricing is actuarially sound, fair, and compliant with regulatory requirements in all states in which they do business.

That is how insurers keep lower-risk policyholders from unfairly subsidizing higher-risk ones.

But history has shown that direct government involvement in the underwriting and pricing of insurance products tends not to end well. Any plan that would attempt to micromanage insurers’ coverage of all perils through a lens that ignores time-tested, actuarially sound risk-based pricing principles raises a host of red flags that must be discussed and addressed before such a plan is allowed to become law.

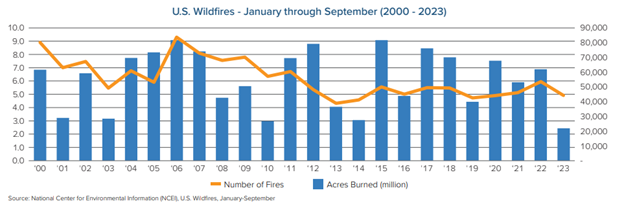

With record-breaking wildfires making headlines in recent years, it may be surprising to learn that U.S. wildfire frequency and severity for in 2023 are on track to be the lowest in the past two decades. In fact, the trend has been generally downward since 2000, according to a recently published Triple-I Issues Brief.

Despite catastrophic losses in Washington State, Hawaii, Louisiana, and elsewhere, California – a state often considered synonymous with wildfire – is in the midst of its second mild fire season in a row. This may be due to drought-breaking rains and snows, but Texas is experiencing fewer wildfires than in 2022, despite worsening drought conditions. About 37 percent of the continental U.S. remains under some form of drought, according to the U.S. Drought Monitor.

At the same time, Swiss Re reports that wildfire’s share of insured natural catastrophe losses has doubled over the past 30 years. How can those trends be reconciled? At least part of the answer resides in population trends – specifically, growing numbers of people choosing to live in the wildland-urban interface (WUI), the zone between unoccupied and developed land, where structures and human activity intermingle with vegetative fuels.

Mitigation is necessary – but not sufficient

The improvements in frequency and severity are likely due to investments in mitigation. State and local authorities have invested heavily to mitigate the human causes of wildfire. In addition, the federal Infrastructure and Jobs Act of 2021 included billions to support wildfire-risk reduction, homeowner investment in mitigation, and improved responsiveness to fires. More recently, the Biden Administration announced $185 million for wildfire mitigation and resilience as part of the Investing in America Agenda, which should help continue the declines in frequency and severity.

But with more people living in the WUI – nearly 99 million, or one third of the U.S. population, according to the U.S. Fire Administration – more than 46 million homes with an estimated value of $1.3 trillion are at risk.

According to the 2022 Annual Report of Wildfires produced by the National Interagency Fire Center (NIFC), 68,988 wildfires were reported and 7.5 million acres burned in 2022. Of these fires, 89 percent were caused by human activity and burned 55 acres per fire. By contrast, the 11 percent of fires caused by lightning resulted in an average of 563 acres burned, 10 times more than human-caused fires.

This difference may shed light on why the number of fires has been decreasing more dramatically than acres burned. Further, population shifts into the WUI are increasing the proximity of property to places prone to fire, helping to explain the rise in wildfire’s increased percentage of insured losses.

CSAA Insurance Group – a AAA insurer – is spurring innovation in the insurance industry through several initiatives tackling the dangers of climate risk.

“We’ve been on a journey to reduce our environmental footprint for a long time,” said Debbie Brackeen, Chief Strategy & Innovation Officer with CSAA, in a recent executive exchange with Triple-I CEO Sean Kevelighan. “We are seeking to reduce our carbon footprint by 50 percent by 2025. We view this work as aligned with our mission: to help our members prepare for and recover from climate risk.”

CSAA has taken several steps to help achieve its goals, including:

Leading the first-ever Innovation Challenge on climate resilience with IDEO and Aon, along with several other sponsors;

Working on the California Innovation Fund in partnership with Blue Forest, a $50 million fund that CSAA contributed half that capital, focused on forest restoration and reducing fuel in a smart and sustainable way; and

Supporting the Wildfire Interdisciplinary Research Center at San Jose State University, which conducts work around predictive modeling, among other endeavors.

While this may seem like a new development, Kevelighan noted that insurers have long worked toward these goals.

“We’ve seen the ESG movement take a hold in the past few years, but it’s been in the DNA of the Triple-I and the insurance industry generally for a long time,” Kevelighan said. “More than half the battle is recognizing that the risk is increasing, while identifying solutions.”

Still, with the increasing consequences associated with climate risk, more work needs to be done.

“There were billion-dollar wildfire losses at CSAA in my first two years in the industry,” Brackeen said. “I wondered if this was normal. It ignited in me that, whatever we do in innovation, it will have to do with wildfire risk. However, what concerns me the most is that risks are becoming uninsurable. This is from the cumulative effects of several different types of losses, including convective storms.”

“We have to seek different types of innovative partnerships to address these issues,” Brackeen concluded. “In this fight for our industry, there are no competitors. We have to be on the same side of the table.”

By Jeff Dunsavage, Senior Research Analyst, Triple-I

I’m pleased and proud to have been part of Triple-I’s Town Hall — “Attacking the Risk Crisis” — in Washington, D.C. In an intimate setting at the Mayflower Hotel on November 30, 120-plus attendees got to hear from experts representing insurance, government, academia, nonprofits, and other stakeholder groups on climate risk, what’s being done to address it, and what remains to be done.

Triple-I’s first-ever Town Hall was designed as a logical step in its multi-disciplinary, action-oriented effort to change behavior to drive resilience. Capping a year in which headlines about “insurance crises” in several states garnered major media attention, Triple-I and its members and partners recognized the need for clarification.

“What we’re seeing is not an ‘insurance crisis’,” Triple-I CEO Sean Kevelighan told the standing-room-only audience. “We’re in the midst of a risk crisis. Rising insurance premium rates and availability difficulties are not the cause but a symptom of this crisis.”

Whisker Labs CEO Bob Marshall discusses innovation with moderator Jennifer Kyung, Vice President and Chief Underwriter at USAA.

While the insurance industry has a critical role to play and is uniquely well equipped to lead the attack, simply transferring risk is not enough. A recurring theme at the Town Hall was the need to shift from a focus on assessing and repairing damage to one of predicting and preventing losses.

Three moderated discussions – examining the nature of climate risk and its costs; highlighting the need of strategic innovation in mitigating those risks and building resilience; and exploring the role and impact of government policy – gave panelists the opportunity to share their insights with a diverse audience focused on collaborative action.

The agenda was:

Climate Risk Is Spiraling: What Can Be Done?

Moderator: David Wessel, Senior Fellow and Director at the Brookings Institution and former Economics Editor for The Wall Street Journal.

Panelists:

Dr. Philip Klotzbach, Colorado State University, researcher and Triple-I non-resident scholar.

Dan Kaniewski, Managing Director, Public Sector at Marsh McLennan, Former FEMA Deputy Administrator.

Jacqueline Higgins, Head, North America & Senior Vice President, Public Sector Solutions, Swiss Re

Jim Boccher, Chief Development Officer, ServiceMaster.

Jeff Huebner, Chief Risk Officer, CSAA.

Innovation, High- and Low-Tech: How Insurers Are Driving Solutions

Moderator: Jennifer Kyung, VP, Chief Underwriter, USAA.

Panelists:

Partha Srinivasa, EVP, CIO, Erie Insurance.

Sam Krishnamurthy, CTO, Digital Solutions, Crawford.

Bob Marshall, CEO, Whisker Labs.

Stephen DiCenso, Principal,Milliman.

Charlie Sidoti, Executive Director, InnSure.

Outdated Regs to Legal System Abuse: It Will Take Villages to Fix This

Parr Schoolman, SVP and Chief Risk Officer, Allstate.

Tim Judge, SVP, Head Modeler, Chief Climate Officer, Fannie Mae.

Dan Coates, Deputy Director, DRS, Federal Housing Finance Agency.

Fred Karlinsky, Co-Chair of Greenberg Traurig’s Global Insurance Regulatory & Transactions Practice Group.

Panelists and participants alike appreciated the compact, action-focused, conversational nature of the single-afternoon event, as well as the opportunity to discuss areas in which their diverse industry- or sector-specific priorities and efforts overlapped.

If you weren’t able to join us in Washington, don’t worry. In his closing remarks, Kevelighan announced plans to take the program on the road with a local and regional focus, so stay tuned. You can contact us if you’re interested in participating in future Town Halls or other Triple-I events. You also can join the “Attacking the Risk Crisis” LinkedIn Group to be part of the ongoing conversation.

Of all the challenges facing property casualty insurers today – from growing catastrophe losses to social inflation – Church Mutual president Alan Ogilvie sees the “war for talent” as one of the most pressing.

“For us, the old adage is very true. Our best assets walk in the door in the morning, at the end of the day they leave, and you just hope and pray they come back,” Ogilvie said in a recent Executive Exchange conversation with Triple-I CEO Sean Kevelighan.

Ogilvie called talent acquisition and retention “our number one challenge.”

“We like to think we bring something a little bit unique to our employees, and that’s a sense of mission,” he said.

He pointed to Church Mutual’s status as 126-year-old mutual company – the largest writer of insurance for religious institutions, which has expanded to include coverage for health, educational, and nonprofit organizations – and said, “It’s pretty easy to get up in the morning when you’re protecting organizations that you know are doing tremendous things in our communities.”

Ogilvie is committed to busting the myth that insurance is a boring business. Among the features of insurance he emphasizes to people early in their careers is the focus on technology and addressing the challenges of climate risk. Catastrophe management – viewed through the lens of artificial intelligence and predictive analytics – has become a cutting-edge discipline.

This, combined with the fact that many insurance professionals are expected to be retiring over the next decade, “creates an incredible amount of opportunity,” Ogilvie said.

The insurance industry’s efforts on behalf of people struggling in the wake of disasters doesn’t end with paying policyholder claims.

The nonprofit Insurance Industry Charitable Foundation (IICF) has launched the IICF Hurricane Ian Relief Fund to support those in need in the wake of Hurricane Ian. Funds will benefit Team Rubicon, a nonprofit providing emergency response and relief throughout affected areas, and SW FL Emergency Relief Fund, which provides critical support to nonprofits and people in areas experiencing immediate need.

Through these nonprofits, IICF will provide funds for recovery support, temporary shelter and basic necessities, along with non-perishable food, toiletry items and diapers for children impacted by the storm.

“The insurance industry is rooted in helping others at their time of need,” said Bill Ross, CEO of IICF. “As tens of thousands of Floridians struggle to recover from the devastation of Hurricane Ian, we as an industry are moved to support those impacted through charitable giving.”

With the help of the insurance industry, IICF has been able to raise $2.3 million over the past few years to benefit nonprofits responding to disaster and pandemic needs across the United States and the United Kingdom. To donate to the current effort, please visit https://give.iicf.org/campaigns/23664-iicf-hurricane-ian-relief-fund.