Global insurtech funding hit $1.01 billion in the third quarter of 2025, marking three consecutive years of average quarterly funding near $1.1 billion, according to a recent Gallagher Re report. Raising $751.72 million, A.I.-based insurtechs accounted for almost 75 percent of all funding across 49 deals, raising $751.72 million, largely attributed to the commercial insurance industry’s evolving risk profile.

Fewer, bigger deals

Though down 7.3 percent from the previous quarter, third-quarter results reflected less quarterly volatility compared to the preceding three-year period, which fluctuated with greater uncertainty around a higher average of $2.7 billion. Deal count also dropped to 76 – the lowest total count since the second quarter of 2020 – as average deal size rose from $12.83 million in the second quarter of 2025 to $15.70 million.

Property/casualty insurers financed eight of the quarter’s 10 largest deals, propelling the industry’s total third-quarter funding to $690.28 million – a 90.5 percent increase from its seven-year low in the prior quarter.

Reinsurers led another dramatic market shift by backing a record sector high of 51 tech investments, suggesting “the appetite for pure venture risk is alive and well” even as investors place fewer “massive, high-risk bets” in favor of “a more balanced approach,” said Andrew Johnston, global head of InsurTech at Gallagher Re.

A.I. takes center stage

With over 25 percent of commercial lines now sold through digital channels, the report outlines how insurers can meet the demands of changing customer expectations and business practices – particularly the digital collection and storage of customer data – by leveraging A.I.

By improving data extraction, pattern identification, and fraud detection, A.I. tools streamline routine decision-making while freeing up underwriters’ capacity to build client relationships and assess complicated, high-value risks, the study found. On a concrete level, such efficiency gains include high-resolution aerial imagery to quickly verify property damages, dashcams to monitor real-time driving behaviors, and wearable IoT solutions to prevent workplace injuries, demonstrating the utility of A.I.-powered insurtechs across commercial lines.

Effective integration, however, transcends simple adoption. Freddie Scarratt, Gallagher Re’s global deputy head of InsurTech, emphasized the enduring challenges of applying A.I. to legacy administration systems and of an emerging talent gap to bridge data and A.I. literacy expertise with traditional underwriting.

Business leaders expressed similar concerns in a Gallagher Re survey released earlier this year, highlighting a skills shortage and pervasive ethical implications as barriers to A.I. adoption.

Underscoring the industry’s goal to “supercharge” underwriting judgement rather than replace it, Scarratt concluded that “the most successful (re)insurers of the future will be those that combine their expertise in relationship management, complex deal structuring, and cycle management with the speed, scale, and analytical power of A.I.”

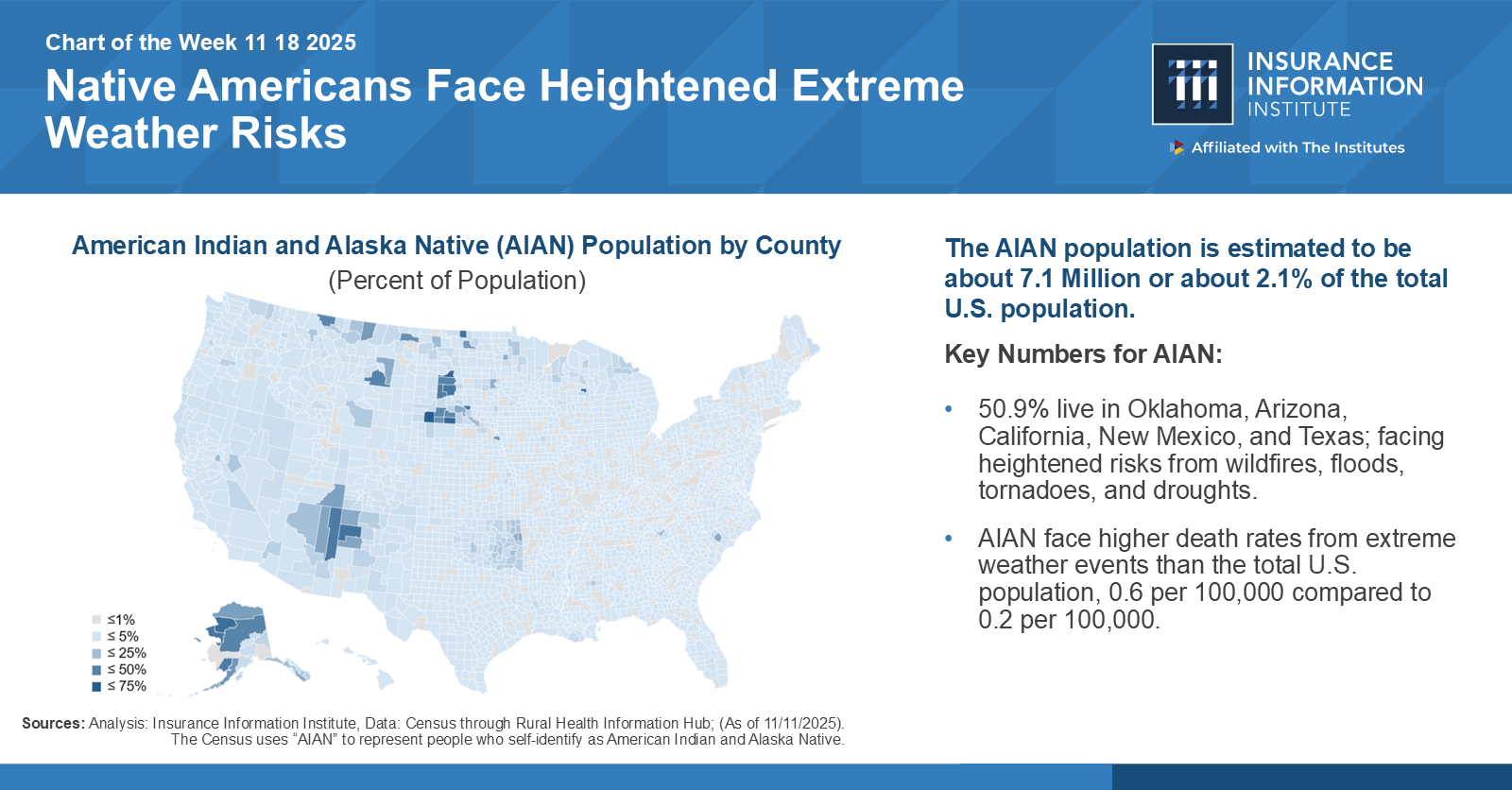

Chart of the Week 11 18 2025:

Native Americans Face Heightened Extreme Weather Risks

As part of an ongoing discussion on the link between the housing and insurance markets, the Insurance Information Institute (Triple-I) released a Chart of the Week (COTW) that provides a snapshot of climate risk concerns for American Indian and Alaska Native (AIAN) population.

The provided estimate for the number of Native Americans in the U.S. is 7.1 million – about 2.1 percent of the total population. As much as 95 percent of the general U.S. population lives in a county that has experienced a natural disaster since 2011. However, this COTW says at least 50.9 percent of Native Americans live in states facing heightened risks from wildfires, floods, tornadoes, and droughts. The chart also reveals that Indigenous people in the U.S. face higher death rates from extreme weather events than the total national population, at 0.6 per 100,000 compared to 0.2 per 100,000.

Native communities are situated on the front line of climate risk.

As insurance is designed to help policyholders and their communities recover from insurable events, coverage availability and affordability can contribute to resilience. However, states that are home to at least half of the U.S. Native American population rank high on the Insurance Research Council (IRC) report, Homeowners Insurance Expenditures as a Percent of Median Household Income – Oklahoma (4th), Arizona (5th), Texas, (6th), New Mexico (14th), California (25th) – indicating comparatively less coverage affordability in those states. While availability and affordability can ultimately be driven by a mix of key underlying cost drivers, climate risk and home-ownership challenges can play a crucial role in access for many Native American homeowners.

Extreme weather events, such as hurricanes and typhoons, have shaped the way colonization of North America unfolded, beginning in the early centuries of European contact. For thousands of years prior, Native Americans had thrived in their homelands by taking measures to survive long-term severe weather, such as seasonally migrating away from flood-prone areas or building nature-based infrastructure as needed. Colonial expansion, in which Indigenous people lost nearly 99 percent of their historical land base over time, decimated Indigenous populations and pushed survivors into high-severe-weather-risk areas or lands, in many cases previously unknown to their respective tribal groups.

As a result of centuries of these forced removal policies and government-directed or sanctioned land dispossession, present-day Native American lands “are also generally far from historical lands, averaging a distance of roughly 150 miles” and are often in inherently more climate risk-prone areas today – i.e., low-lying, exposed, less habitable due to drought, etc. Living today on the front lines of climate risk across the U.S. means frequently experiencing acute effects, such as thawing permafrost, rising sea levels, increased flooding, stronger storms, erosion, and shifting ecosystems.

For instance, a 2024 study indicates that Oklahoma, home to 39 federally recognized tribal nations, “faces climate and demographic changes that disproportionately put many Native Americans at risk. The heavy rainfall, 2-year floods, and flash floods are all projected to have increased risks by 501.1 percent, 632.6 percent, and 296.4 percent, respectively.”

In a village in western Alaska, where permafrost is thawing, buildings (including a preschool) are shifting, water intrusion is increasing, and relocation is becoming a real threat. Recently, nearly 50 Alaska Native communities experienced “towering wind speeds, record storm surge, and widespread flooding”, resulting in at least one death and the displacement of 1,500 people. Initial estimates have reported that the storm decimated 90 percent of homes in the coastal village of Kipnuk and 35 percent in Kwigillingok, “which has also experienced toxic chemicals spilling into its freshwater supply.”

Climate risk can threaten lives and property, of course, but also regional economies, one of the key ingredients in building capacity for resilience. For example, a study of climate-driven economic challenges posed to Navajo Nation, the largest Indian reservation in the U.S., shows that “drought has a larger impact on cattle production than hay production, resulting in total economic losses of $8.2 million and $0.4 million for the cattle and hay sectors, respectively.” Without robust regional economies, infrastructure, or policy support, Native American homeowners and their communities may struggle to adapt or relocate effectively.

Homeownership costs may contribute to the protection gap.

Are homeowners living in New Mexico and certain rural areas of Texas

have manufactured homes, or

own inherited homes.

Data collected through the Home Mortgage Disclosure Act (HMDA) reveals that Native Americans, on average, pay more to finance their homes – in some contexts up to two times more. While that disparity can be attributed to several factors, one major driver is the loan type that appears to be more common among Native borrowers, home-only loans. “Nearly 40 percent of loans to Native American borrowers on reservations were for manufactured homes, compared to 3 percent of loans to White borrowers”. Further, about 8 out of 10 manufactured-home loans were home-only loans.

Home-only loans, a financing tool used for movable personal property in which the lender retains ownership of the property until the borrower fully pays the loan, can make financial sense in some instances. Nonetheless, borrowers typically pay higher interest rates and have fewer consumer protections, such as federal guarantees, than regular mortgages. The pressure of these circumstances may compel the homeowners to carry insufficient coverage, or, when they pay off the loan, none at all.

Federal funding freezes can impede resilience.

Data from the National Congress of American Indians show that “U.S. citizens receive, on average, about $26 per person, per year, from the federal government, while tribal citizens receive approximately $3 per person, per year.” Recent federal disinvestment in 2025 from crucial risk prevention and management programs and other supportive infrastructure – including public radio stations which can be used for advance severe weather warnings and coordination of disaster recovery efforts – has exacerbated the burden from longstanding disparities. This decrease in support can also heighten the need for insurance coverage and closing the protection gap.

Amy Cole-Smith, Executive Director for BIIC/ Director of Diversity at The Institutes says, “the numbers are clear: Native Americans face higher exposure to extreme weather, higher insurance burdens, and higher rates of being uninsured. These factors reflect not just climate trends but historical inequities that continue to shape outcomes today. Strengthening coverage access is essential to protecting lives, homes, and cultural continuity.”

As Smith has often expressed, one way the industry can start closing the protection gap is “by having people at the table who understand the lived experiences behind the numbers.”

Triple-I works to advance the conversation around crucial issues in the insurance industry. We invite you to follow our blog to learn more about trends in insurance affordability and availability across the property/casualty market.

With last week’s end of the longest U.S. government shutdown in history, Congress reauthorized FEMA’s National Flood Insurance Program (NFIP).

During the shutdown, the NFIP continued to pay claims using available funds, but it could not sell or renew policies until reauthorized. These restrictions affected an estimated 1,300 property sales each day, as prospective property owners must purchase flood coverage in Special Flood Hazard Areas (SFHA), where private flood options – despite gaining traction – are still limited.

With millions of homeowners and countless communities relying on the NFIP, many organizations across the risk and insurance industry sent a letter urging congressional leaders to reauthorize NFIP ahead of its expiration, writing that a lapse “could further impact affordable housing, create additional challenges for small businesses, unnecessarily further increase the cost of homeownership, and must be avoided.”

While reauthorization allows NFIP insurers to retroactively issue policies for applications received during the shutdown, the measure extends their authority only through Jan. 30, 2026, leaving the program’s fate an open question. Absent a long-term NFIP authorization bill, Congress has now reauthorized the program 34 times since fiscal year 2017.

Incentivizing risk reduction

Flood risk was long considered untouchable by private insurers, which is a large part of the reason NFIP exists. While private participation in the flood market has grown in recent years, NFIP remains a critical source of protection for this growing and underinsured peril.

Beyond providing economic protection for policyholders, the NFIP also plays a critical role in promoting climate resilience, particularly through its Community Rating System (CRS). A voluntary program, the CRS rewards homeowners with premium discounts when their communities invest in floodplain management practices that exceed the NFIP’s minimum standards, with the program’s highest rating qualifying residents for a 45 percent premium reduction.

After the cancellation of other FEMA-managed initiatives like BRIC, the CRS can help provide relief where still needed. For instance, Jefferson Parish homeowners displaced following Hurricane Ida in 2021 had secured BRIC grants to elevate and reconstruct their homes shortly before the program ended, leaving these projects in limbo. But the CRS now offers residents and businesses more than $12 million in flood insurance savings annually after the parish secured a Class 3 rating – the first of its kind in Louisiana.

By incentivizing improved building codes, citizen awareness campaigns, and other resilience solutions, the CRS can ensure that vulnerable communities “will continue to benefit from a comprehensive floodplain management and mitigation plan that helps make us more resilient in the face of disasters,” said Jefferson Parish President Cynthia Lee Sheng in a statement. Notably, however, the parish earned its rating mere weeks ahead of the NFIP lapse, which delayed the discounts from appearing in new and renewed policies.

As climate and weather-related events become increasingly frequent and severe, the success of these investments will depend on proactive strategies informed by timely, granular data. Though NOAA announced it would cease tracking the country’s costliest disasters earlier this year, nonprofit Climate Central aims to fill the gap by rebuilding NOAA’s database and expanding it to track smaller catastrophes, providing insurers and other stakeholders more reliable information to understand individual disasters.

Taken together, such efforts can help insurers accurately reflect rising risks in insurance pricing while engaging with communities and businesses in solutions to keep coverage accessible. Sustaining this balance involves continuous collaboration between public and private sectors.

An atmospheric river system dumped up to six inches of heavy rains and claimed multiple lives in California last weekend, with thunderstorms on the horizon posing outsized risks for communities still recovering from January’s devastating wildfires.

Triggering mudflows and flash flooding across streets and highways, the multiday storm highlights the added complexity of insuring and preventing disasters in the state’s many wildfire-prone areas.

Coverage confusion

Californians grappling with this destruction may be unaware that homeowners and commercial policies typically exclude flood, mudslide, debris flow, and similar catastrophes, or of the distinctions between these events. Though media outlets may use these terms interchangeably, insurers differentiate between mudflows and mudslides for coverage eligibility.

Essentially rivers of mud, mudflows are covered by flood insurance, which is available from FEMA’s National Flood Insurance Program (NFIP) and a growing number of private insurers. Mudslides – or masses of rock and earth pulled downhill by gravity – typically do not involve much liquid and remain ineligible for flood coverage.

But if recent perils covered by standard insurance policies either directly or indirectly cause any of these events, insurers must cover ensuing damages, as explained in a notice from California Insurance Commissioner Ricardo Lara shortly before the storms. Such protections can help residents bracing for possible mudslides later this week – particularly those living in Southern California neighborhoods scorched by wildfires earlier this year.

Noting that “it is critical to prepare for flooding, mud, and debris flow when heavy wind and rain, also called atmospheric rivers, are forecast,” Janet Ruiz – Triple-I’s California-based director of strategic communication – advises policyholders to “check your insurance coverage, as you will need a separate flood policy for flooding and mudflow. Use sandbags – most communities provide them free of charge. Be safe, and don’t drive into flooded areas.”

These recommendations are especially vital for fire-scarred areas, where heat-damaged soil repels water and even minor showers can escalate into dangerous flash flooding and debris flows. An absence of vegetation to absorb rain exacerbates both, leaving nearby homes, businesses, and other infrastructure more vulnerable.

From one system to another

Beyond facilitating substantial flooding, the wet weather also weakened elevated fire conditions that emerged during the fall – a reoccurring interplay in California’s climate that complicates developing effective mitigation and resilience strategies. Within the Golden State alone, factors like temperature, humidity, wind, and topography vary too widely to apply a singular mitigation approach, underscoring the importance of property-specific data analysis.

Using case studies from three distinct California areas, research from Triple-I and Guidewire shows how granular data can help identify properties with attractive risk profiles despite these evolving risks. Noting “every property being assessed for wildfire risk is unique,” their report found that home hardening reduces wildfire damage by as much as 70 percent but emphasized proactive collaboration between insurers, regulators, and policyholders as key to long-term success.

With more people moving into the wildland urban interface and communities increasingly hit with inland flooding, such partnerships are crucial to bridge protection gaps while keeping insurance affordable and available.

By William Nibbelin, Senior Research Actuary, Triple-I

The rate-filing process for homeowners’ insurance has become less efficient and effective, a new study by the Insurance Research Council (IRC) shows.

The report – Rate Regulation in Homeowners Insurance: A Comparison of State Systems – analyzed industry data from 2010 through 2024 across all states, including the District of Columbia. The study found that, not only is it taking longer for insurers to get rate increases approved, but the increases are lower than requested, with bigger gaps between the request and the granted amount than had previously been the case.

Key findings:

The number of rate filings is growing at a compound annual growth rate of 3.3 percent from 2018 to 2024 nationwide.

The average number of days to approval grew from 44 to 63 days.

The number of filings withdrawn increased from 2.9 percent of filings to 3.9 percent of filings.

The percentage of filings receiving less rate impact than requested grew by more than 10 points.

The disparity in approved rate impact grew by nearly 1 point.

Market concentration (as measured by the Herfindahl-Hirschman Index, or HHI) decreased by 14.6 percent.

The residual share of direct written premium has grown at a compound annual growth rate of 10.5 percent from 2020 to 2024

A strong-to-moderate correlation exists between net underwriting losses and premium shortfalls within states and across time.

Filing process measures and market outcomes vary by regulatory systems.

During this same period from 2010 through 2024, the homeowners’ insurance industry experienced a net combined ratio over 100 in 10 of the 15 years. Combined ratio – calculated as losses and expenses divided by earned premium plus operating expenses divided by written premium – is a key measure of underwriting profitability. A combined ratio over 100 represents an underwriting loss.

The IRC report includes the determination of a strong correlation between underwriting loss and premium shortfalls, defined as the potential dollar difference between the effective filed rate impact and approved rate impact.

In California, for example, the time to approval exceeds that of the next highest state – New York – by more than four months. California also has the second-fastest-growing residual market share from 2.1 percent in 2019 to 8.2 percent in 2024 and the second-fastest-growing excess and surplus homeowners market share from 0.3 percent in 2010 to 6.3 percent in 2024. This means that, at most, only 85 percent of California homeowners’ insurance is covered by a standard policy.

By Loretta Worters, Vice President – Media Relations, Triple-I

On a crisp October morning, volunteers gather at a local farm in New Jersey, gloves on, baskets in hand, ready to harvest rows of beets. These volunteers aren’t just picking produce, they’re helping ensure that families in need have access to fresh, healthy food this Thanksgiving and throughout the holiday season.

AGAR’s mission is simple yet powerful: To positively impact as many lives as possible through a volunteer effort of planting, picking, rescuing, and delivering free, fresh produce to those who need it most. At a recent IICF volunteer event, insurance industry volunteers joined forces at AGAR to harvest 31,000 pounds of fresh beets—providing 124,000 servings of nutritious produce for families in need. It’s an extraordinary example of what can happen when an industry comes together in service of its community.

“Every day, millions of people face food insecurity. Our volunteers and partners help us deliver fresh, healthy food to those who might otherwise go without,” said Chip Paillex, president and founder of AGAR. Paillex started the nonprofit in 2002 after realizing the need for fresh produce at local food pantries, inspiring the “grow a row for the hungry” concept that has since spread across the state.

Food insecurity is a serious issue nationwide. Every day, 47 million people across the United States, including 14 million children, face food insecurity. Many must rely on low‑quality diets lacking fresh fruits and vegetables, and food banks often report that produce is the hardest item to obtain. According to the Centers for Disease Control and Prevention (CDC), people facing food insecurity are at higher risk of chronic diseases such as diabetes, hypertension, and obesity. Children who lack proper nutrition face developmental delays and mental health challenges.

In New Jersey, food insecurity is also a serious challenge: nearly 1.1 million people, including more than 270,000 children, are estimated to be food insecure.

Rescuing Food, Rescuing Hope: Table to Table

Table to Table continues its vital work rescuing food that might otherwise be discarded from grocery store produce to prepared meals from corporate cafeterias, and delivering it directly to food pantries, shelters, and community centers.

“We are so grateful for the long-time and ongoing support we receive from the IICF,” said Julie Kinner, vice president of operations at Table to Table. “Their partnership has helped us rescue more than 120,000 tons of surplus food from food donors, the equivalent of more than 241 million meals. Thanks to IICF’s recent grant, we were also able to develop our new app, which is allowing us to locate and recover a significantly greater amount of food across the state.”

The app has already proven transformative, streamlining communication between food donors and drivers to ensure that more meals make it to tables instead of landfills.

Kinner noted that food pantries and emergency food providers across New Jersey are facing growing and unprecedented demand, as the need for food assistance continues to climb.

“Together, it’s possible to bridge the gap, nourish our community, and make sure no good food goes to waste, and no neighbor goes hungry,” Kinner added.

Bringing Resources to the Table: IICF Support

The Insurance Industry Charitable Foundation supports these efforts through both funding and volunteerism. IICF’s grants empower community organizations to build capacity, expand technology, and scale their impact, while volunteers contribute thousands of service hours each year.

“Supporting these programs allows our community to have a measurable impact,” said Elizabeth (Betsy) Myatt, vice president, chief program officer, and executive director of IICF’s Northeast Division. “When we combine funding with volunteer action, we create stronger, more sustainable solutions to fight hunger. It’s a great example of what the insurance industry can accomplish together.”

From the farm fields of AGAR to the rescue routes of Table to Table, volunteers and staff work together to create a circle of giving. One crate of harvested beets, one basket of rescued bread, one hour of volunteer time all translate into meals for children, seniors, and families in need.

“This Thanksgiving, we’re reminded that gratitude isn’t just something we feel, it’s something we act on,” said Myatt. “Thanks to volunteers and organizations like AGAR and Table to Table, we’re helping ensure that families in these communities have the food and support they need this holiday season.”

Insurance is a trust-based business. Providing safety and security in a risky, unpredictable world is the core function of our industry, which hinges on engendering consumer peace of mind.

Yet trust has become a scarce commodity as U.S. adults report successively lower average levels of trust by generation, with only 34 percent agreeing that “most people can be trusted” in 2018 compared to 46 percent in 1972. Trust in institutions appears similarly bereft, according to a global survey from SAS and Economist Impact that links the current $1.8 trillion protection gap to pervasive distrust in insurers.

To improve public and cross-sector relationships, Allstate and the Aspen Institute recently launched the Trust in Practice Awards, a grant program honoring non-profit organizations that support civic engagement, volunteering, and bridging differences with intergenerational participants. Backed by the Allstate finding that 74 percent of Americans remain optimistic about their community’s future, the initiative aims to broadly recoup trust by first establishing a strong foundation in neighborhoods, schools, and local organizations.

By reversing community distrust – which “undermines democracy, increases anxiety, and reduces personal freedom,” said Tom Wilson, Allstate president and CEO – the program could motivate collective action and resilience efforts on a larger scale, sending ripple effects of greater trust nationwide.

Fueling economic outcomes

Such effects can further stimulate measurable economic growth. A 2025 PwC survey indicates that introducing “trust or safety” features substantially increases engagement and purchase intent, with 72 percent more likely to engage, 68 percent open to new products, and 59 percent open to related merchandise.

Despite clear benefits, trust-building investments continue to face widespread scrutiny as a perceived barrier rather than facilitator of growth, the survey notes. Whereas AI, for instance, might quantifiably boost operational efficiency and reduce costs, pinpointing similar results from specific trust and safety measures can be more challenging, potentially leading organizations to overlook their importance.

Triple-I and SAS centered the insurance industry’s role in guiding these conversations in their 2024 research on ethical AI implementation, highlighting the technology as an opportunity for insurers to educate businesses less experienced with complex safety regulations. Prioritizing data privacy and integrity must occur alongside any innovation, the report emphasizes, to alleviate these concerns for consumers across all industries.

Transparent discussions are also key to combating legal system abuse, valued at $6,664 per family of four in added costs for basic goods and services. Commandeering the trust once associated with insurers, predatory “billboard” attorneys invest billions of dollars annually into advertising inflated settlements that often yield only marginal awards for the injured party, creating a more uncertain and deceptive litigious environment.

To bolster stakeholder education on the reality of legal system abuse, Triple-I founded an awareness campaign that includes brick-and-mortar interstate billboards in Atlanta and Baton Rouge and a consumer guide, co-authored by Munich Re, that explains its economic impacts. A consumer microsite additionally promotes various state reform movements.

Trust is neither automatic nor unilateral. While legal reform momentum and cutting-edge insurance products can help restore affordable and widely available coverage, closing the protection gap will require ongoing coordinated efforts that can translate for modern audiences the industry’s dedication to putting people first.

By William Nibbelin, Senior Research Actuary, Triple-I

Economic and social inflation have added a staggering $231.6 billion to $281.2 billion in increased liability insurance losses and Defense and Cost Containment expenses in auto and general liability lines, a new report by Triple-I and the Casualty Actuarial Society.

The analysis focuses on the total impact of increasing inflation determined through actuarial methods that are unable to decompose the precise contribution of economic inflation versus the role of what Triple-I characterizes as “legal system abuse” — policyholder or plaintiff attorney practices that increase costs and time to settle claims to the detriment of consumers, businesses, and the economy. These practices include increasing litigiousness, third-party litigation financing, and soaring jury awards.

Claim severity powers losses

Across all lines analyzed, claim severity – not frequency – emerges as the primary driver of the escalating losses in liability lines of insurance. While the number of claims (frequency) has either generally declined or remained below pre-pandemic levels across the study period, the average cost per claim (severity) has soared. In commercial auto liability, for example, frequency has fallen dramatically since the pandemic, yet losses have still increased relentlessly because severity has risen 93.5 percent between 2015 and 2024.

Auto Liability

The report’s traditional focus on auto liability lines continues to show the most significant dollar-based impacts.

Personal auto liability: Increasing Inflation added between $91.6 billion and $102.3 billion to losses and DCC for the 2015–2024 period. This represents 8.7 percent to 9.7 percent of losses and DCC for the period and an increase of 20 percent to 26 percent from the previous analysis on years 2014 through 2023. While the implied compound annual impact is lower than in the commercial sector, the dollar amount is huge due to the line’s immense underlying size. Personal auto severity has accelerated significantly post-2019, nearly tripling its compounded annual growth rate to 10.9 percent from 2019 to 2024. Premiums are only just beginning to rebound from pandemic-era lows, lagging the rise in losses.

Commercial Auto Liability: This line continues to sustain higher inflation rates in percentage terms. The total impact of increasing inflation reached $52.0 billion to $70.8 billion (22.6 percent to 30.8 percent of booked losses). This represents an increase of 22 percent to 27 percent from the previous analysis.

A compelling cross-data set comparison with the Triple-I 2025 report, Review of Motor Vehicle Tort Cases Across the Federal And State Civil Courts, suggests that the “excess value” extracted by motor vehicle tort lawsuits—a clear measure of legal system abuse—was approximately $42.8 billion between 2014 and 2023. This quantitative finding suggests legal system abuse accounts for roughly one-third of the total Increasing Inflation effect in auto liability losses.

General liability lines

This year’s analysis expands to quantify the impact across broader general liability lines for the first time, revealing inflationary rates that are equally, if not more, dramatic in percentage terms.

Other Liability – Occurrence: Increasing inflation added between $83.4 billion and $103.3 billion to losses and DCC for the 2015–2024 period. This inflationary problem is comparable in dollar terms to personal auto liability, despite having only about one-third of the loss volume. Its implied annual impact of 3.7 percent on a paid basis is the highest of all the lines studied. Severity in this line grew at a compound annual rate of 6.8% from 2015 to 2024, far outpacing the Consumer Price Index All-Urban (CPI-U).

Product Liability – Occurrence: Increasing inflation added between $4.6 billion and $4.8 billion to losses and DCC for the 2015–2024 period. The smallest line examined exhibits the most dramatic severity trend with a compound annual growth rate of 22.3 percent between 2015 and 2024, resulting in a 512.5 percent severity increase overall. The effects appear to be accelerating, with the impact on Accident Year 2024 alone estimated at over 50% of that year’s booked losses.

For the “claims-made” categories of these liability lines (“other liability” and “product liability”), the study was unable to develop credible quantitative estimates due to shifts in business mix, data variability, and the inherent heterogeneity of the underlying risks. However, these lines have certainly not escaped the increasing inflationary environment.

Looking ahead

The data confirms a difficult truth: Even as general consumer price inflation (CPI-U) moderated to 3.0 percent in 2024—a reduction from the 2021-2023 average of 5.6 percent—the loss inflation in liability insurance remains structurally elevated. This means the economic tailwinds that temporarily exacerbated the problem are lessening, but the foundational issues of legal system abuse persist, locking in a higher rate of loss for the foreseeable future.

For consumers and businesses, this translates directly into higher premiums and a greater strain on their financial well-being. The challenge for insurers is the need to adapt to an elevated inflationary environment to effectively manage future liabilities. Recognizing and addressing the pervasive influence of legal system abuse is therefore essential for both managing risk and protecting consumers and businesses from ever-rising costs.

Triple-I continues to foster a research-based conversation around legal system abuse. For an overview of the topic and other helpful resources about its potential impact on insurers, policyholders, and the economy, check out our knowledge hub.

By Michael Menapace, Triple-I Non-Resident Scholar

Michael Menapace is a professor of insurance law at Quinnipiac University School of Law, a Fellow of the American College of Coverage Counsel, and co-chair of the Insurance Practice Group at Wiggin & Dana LLP.

Brokers and companies routinely work to assemble multiple insurance policies to build towers of general liability (GL) coverage. They now have a new option that eliminates much of the friction that can occur in underwriting and claims.

For example, when a mass-casualty event occurs, insurers at the primary and lower excess layers may be incentivized to seek an early exit from the claim with as little claim expense as possible; as a result, they may overpay to resolve one claim while providing minimal support to the policyholder defending the other claims. Tension between layers also can arise when upper-layer carriers seek to place as much responsibility as possible on the lower-level carriers who are seeking to minimize their role.

On the coverage side, policyholders can find that their traditional layers of excess coverage may be subject to differing terms, such as whether they provide for a defense. Even when the excess tower contains follow-form policies, inconsistencies can occur when carriers take different positions on coverage, claim value, litigation/settlement strategy, and so forth.

As a result of all of this is, gaps can open in the multilayer tower. For example, a recent claim that was the subject of a lawsuit arising from a large casualty loss in Florida involved one excess insurer seeking to enforce an anti-stacking provision that limited coverage for an event to one payment from the insurers equal to the highest policy limit among the tower participants. In another claim, the higher-layer insurers argued that their layers were not triggered because the lower layer insurer had improperly exhausted.

In addition to these examples, we’ve seen situations in which various excess layers contain different dispute resolution procedures, are subject to varying states’ laws, or have requirements of being resolved in differing jurisdictions. Brokers and policyholders can find managing their excess tower time-consuming and challenging at a time when they could be focusing on the defense of the mass casualty event or other large loss.

Addressing these challenges

Chubb, Zurich, and National Indemnity (the reinsurance arm of Berkshire Hathaway) have formed a new facility that seeks to eliminate some of these challenges. It provides a single layer of commercial umbrella coverage up to $100 million, typically following a $10 million primary layer. Many of the terms will be familiar to brokers and policyholders: Coverage A for Bodily Injury and Property Damage, Coverage B for Personal and Advertising Injury, and an Optional Coverage C for Auto and Employers Liability.

A unique feature in the United States, the program has “single-desk” underwriting style so that brokers can work with one point of contact for the underwriting of the entire layer of excess coverage. Flexibility is also an advantage because the program is being written on a surplus lines basis, which means more discussions can be had on terms and conditions.

Traditionally, general liability coverage is written on an occurrence basis, which can keep the insurer on the risk for decades after the policy period expires. Insurers price that long-tail exposure into premiums. This new program can be more affordable because it is written on a claims-made basis, while including a multi-year extended reporting period to protect the policyholder. This can save the policyholder money when compared to traditional programs.

Just like underwriting, claims will be handled with single point of contact, with one of the carriers taking the lead. Once the claim is tendered and being defended, the fact that this group of leading insurers is on the risk means the collective experience of some of the industry’s biggest, most sophisticated carriers is at the disposal of the insured. If a coverage dispute does arise, the policy provides for resolution via a single arbitration that applies consistent procedures and the law of a single state – again, streamlining the process and resolution for the policyholder.

While some of the features are offered in the London market, this provides brokers and policyholders with a U.S.-based solution with added benefits and features.

Illinois insurers narrowly avoided increased government involvement in insurance pricing as state legislators rejected “an extreme prior-approval system found nowhere else in the country,” according to a joint statement from the American Property Casualty Insurance Association, the National Association of Mutual Insurance Companies, and the Illinois Insurance Association.

If approved, the bill would have given regulators the authority to block rate change and order refunds from insurers for premiums deemed excessive, effectively generating “fewer choices and greater instability,” the statement continued.

While calls for the bill began in July, following homeowners’ insurance rate hikes, Illinois has a history of legislative challenges to actuarially sound pricing. Similar legislation in Louisiana passed that same month, amid record rate filing rejections in Pennsylvania and two California lawsuits accusing insurers of deliberately underinsuring policyholders to maximize profits.

Such trends underscore pervasive misunderstandings surrounding risk-based pricing, the practice under which insurers offer different prices for the same coverage based on risk factors specific to the insured. Without it, insurers could not adequately cover mounting natural catastrophe losses, inflationary pressures, and other rising costs, leading to an insufficient policyholder surplus to pay claims. When surplus falls below a certain threshold, insurers must raise premium rates, adjust their coverage availability, or, in extreme cases, become insolvent.

Under this pricing methodology, Illinois benefits from better coverage affordability compared to the national average and a competitive insurance market of more than 200 operating insurers.

“Illinois has a very stable insurance marketplace,” said Triple-I CEO Sean Kevelighan. “Restrictive legislation could lead to a California-like regulatory environment that would impact insurance affordability and availability in the state, rather than help consumers as intended.”

Rather than involve themselves in the complexity of insurance pricing, policymakers in Illinois and elsewhere would do a greater service to their constituents by exploring and investing in risk reduction through cost-saving mitigation and resilience investments. The property/casualty insurance industry can be a valuable partner in such beneficial approaches.