By Lewis Nibbelin, Contributing Writer, Triple-I

Spanning over 500 miles of the southeastern United States, Hurricane Helene’s path of destruction has drawn public attention to inland flood risk and the need for improved resilience planning and insurance purchase (“take up”) to confront the protection gap.

Extreme rainfall and wind inflicted a combination of catastrophic flooding, landslides, and extreme rainfall and wind gusts dumped an unparalleled 40 trillion gallons of water across Florida, Georgia, North Carolina, South Carolina, Virginia, and Tennessee, causing hundreds of deaths and billions in insured losses.

Most losses are concentrated in western North Carolina, with much of Buncombe County – home to Asheville and its historic arts district – left virtually unrecognizable. Torrential rain and mountain runoff submerged Asheville under nearly 25 feet of water as rivers swelled, while neighboring communities were similarly flattened or swept away.

Rebuilding will take years, especially as widespread lack of flood insurance forces most victims to seek federal grants and loans for assistance, slowing recovery. Compounding these challenges, misinformation about assistance from the Federal Emergency Management Agency (FEMA) has impeded aid operations in certain areas, leading FEMA to issue a fact sheet clarifying the reality on the ground.

A persistent protection gap

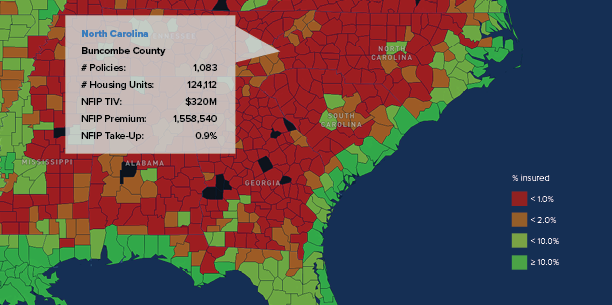

Less than 1 percent of residents in Buncombe County had federal flood insurance as Helene struck, as illustrated in the map below, which is based on National Flood Insurance Program (NFIP) take-up rate data. Inland flooding isn’t new, and neither is the inland flood-protection gap.

In August 2021, the National Weather Service issued its first-ever flash-flood warning for New York City as remnants of Hurricane Ida brought rains that flooded subway lines and streets in New York and New Jersey. More than 40 people were killed in those states and Pennsylvania as basement apartments suddenly filled with water.

Then, in July 2023, a series of intense thunderstorms resulted in heavy rainfall, deadly flash floods, and severe river flooding in eastern Kentucky and central Appalachia, with hourly rainfall rates exceeding four inches over the course of several days. Subsequent flooding led to 39 fatalities and federal disaster-area declarations for 13 eastern Kentucky counties. According to FEMA, only a few dozen federal flood insurance policies were in effect in the affected areas before the recent storm.

“We’ve seen some pretty significant changes in the impact of flooding from hurricanes, very far inland,” Keith Wolfe, Swiss Re’s president for U.S. property and casualty, told Triple-I CEO Sean Kevelighan in a Triple-I Executive Exchange. “Hurricanes have just behaved very differently in the past five years, once they come on shore, from what we’ve seen in the past 20.”

Need for education and awareness

Low inland take-up rates largely reflect consumer misunderstandings about flood insurance. Though approximately 90 percent of all U.S. natural disasters involve flooding, many homeowners are unaware that a standard homeowners policy doesn’t cover flood damage. Similarly, many believe flood coverage is unnecessary unless their mortgage lenders require it. It also is not uncommon for homeowners to drop flood insurance coverage once their mortgage is paid off to save money.

More than half of all homeowners with flood insurance are covered by NFIP, which is part of the FEMA and was created in 1968 – a time when few private insurers were willing to write flood coverage.

In recent years, insurers have grown more comfortable taking on flood risk, thanks in large part to improved data and analytics capabilities. This increased interest in flood among private insurers offers hope for improved affordability of coverage at a time when NFIP’s Risk Rating 2.0 reforms have driven up flood insurance premium rates for higher-risk property owners.

New tools and techniques

New tools – such as parametric insurance and community-based catastrophe insurance – also offer ways of improving flood resilience. Unlike traditional indemnity insurance, parametric structures cover risks without the complications of sending adjusters to assess damage after an event. Instead of paying for damage that has occurred, it pays out if certain agreed-upon conditions are met – for example, a specific wind speed or earthquake magnitude in a particular area. If coverage is triggered, a payment is made, regardless of damage.

Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders. Alone, or as part of a package including indemnity coverage, parametric insurance can provide liquidity that businesses and communities need for post-catastrophe resilience.

While localized insurance approaches can support flood resilience, coordinated investments in public education and preemptive mitigation are crucial to reducing risk and making insurance more available and affordable. Intergovernmental collaboration with insurers on development zoning and building codes, for instance, can promote the creation of safer and climate-adaptive infrastructure, lowering human and economic losses.

Learn More:

Removing Incentives for Development From High-Risk Areas Boosts Flood Resilience

Miami-Dade, Fla., Sees Flood Insurance Rate Cuts, Thanks to Resilience Investment

Attacking the Risk Crisis: Roadmap to Investment in Flood Resilience