By Jeff Dunsavage, Head of Research Publications and Insights, Triple-I

Gender is one of many factors insurers consider when looking at a driver’s risk profile, as permitted or prohibited by state laws and regulations, using the gender indicated on drivers’ licenses. Twenty-two states currently provide – in addition to “male” and “female” designations – non-binary gender identity options or do not require gender to be listed at all.

What are the insurance implications, if any and where permissible by state law, of a non-binary gender marker or the absence of any gender marker on a driver’s license? The short answer is that state-by-state differences in the relevant data limit the impact.

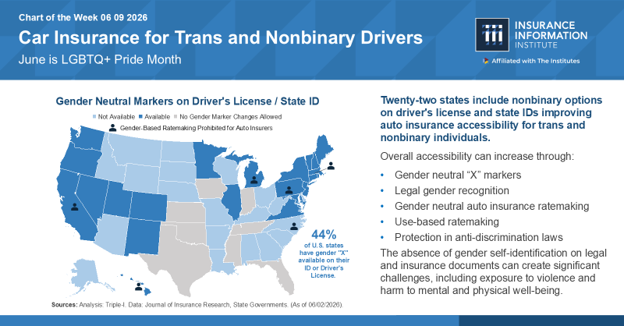

State use of gender markers

As of June 2026, 22 states allow an “X” gender marker on state IDs and driver’s licenses, representing 44 percent of the country. Interpreted in some states as a “not specified” gender, the X marker is widely regarded as a gender-neutral option for those who are not exclusively male (“M”) or female (“F”), which may include trans, nonbinary, and/or intersex individuals. Oregon became the first state to authorize the designation in 2017, following in the footsteps of similar laws in several other countries.

Within states that offer X markers, residents may update their gender marker to F, M, or X with varying degrees of ease, depending on state process requirements. Residents outside these states are limited to F or M designations, with gender marker corrections on state IDs and driver’s licenses altogether prohibited in at least eight states.

By population, 51 percent of trans adults live in states that allow these F, M, or X marker updates. Twenty-two percent live in states that bar these changes, according to estimates from the Movement Advancement Project. This figure could grow as legislation restricting the legal recognition and rights of trans people ramps up across the country, with nearly 800 such bills under consideration so far this year, 60 of which have passed. More than one thousand were considered in 2025, marking the sixth consecutive record-breaking year for such proposals.

Risk-based pricing

“Risk-based pricing” is a basic insurance concept that might seem intuitively obvious when described – yet misunderstandings about it frequently sow confusion. Simply put, it means offering different prices for the same level of coverage, based on risk factors specific to the insured person or property. If policies were not priced this way – if, for example, insurers had to come up with a one-size-fits-all price for auto coverage that didn’t consider vehicle type and use, where and how much the car will be driven, and so forth – lower-risk drivers would subsidize riskier ones.

Little uniform data currently exists, however, on accident trends among trans and nonbinary drivers. As a result, it’s unclear whether or how rates might be affected for those with an X gender marker or for those without an updated gender marker of any kind.

Telematics can help

A 2021 article from the National Association of Insurance Commissioners’ (NAIC) Journal of Insurance Regulation, as well as a 2024 Casualty Actuarial Society (CAS) study, point to the promise offered by telematics and usage-based technologies. The NAIC Journal article recommends abandoning gender as a rating factor, arguing that “technology has advanced the opportunity to more directly measure actual driving behavior and exposure through other predictors.” The CAS study suggests telematics can “significantly reduce the need to include age, sex, and marital status in the claims frequency and severity models.”

While acknowledging “not all of the sensitive variables we tested could be eliminated from the model,” the CAS study went on to say, “The analysis shows there is still value in insurers testing the addition of telematics to their models to potentially reduce reliance on sensitive information that could result in actual or perceived bias.”

Commitment to fairness

Fair, accurate pricing and underwriting are at the heart of the risk-based approach, and property/casualty insurance industry is committed to ensuring fairness and promoting trust across all the communities it serves. Insurers and the actuaries and data scientists that support them are well positioned to continue helping policymakers and decisionmakers understand the complex science of risk and play a constructive role in the policy discussion.

Learn More:

LGBTQIA+ Homeownership Gap May Be Fueling Insurance Protection Gap

Diversity and Inclusion in the Insurance Industry

Clarifying Drivers of Rising Auto Premiums

Allstate, Aspen Initiative Seeks to Ease Trust Gap

Human Needs Drive Insurance and Should Drive Tech Solutions

Triple-I Issues Brief: Risk-Based Pricing of Insurance (Members only content)