Inflation, litigation, and talent concerns are three major drivers of the specialty-lines trends the Argo Group explores in a recent report.

Labor inflation is outpacing material costs, with U.S. labor costs rising 1.42 percent year over year, compared to 0.93 percent for materials, Argo reported. This surge in labor costs affects both claims payouts and policy pricing.

“For brokers,” Argo says, “that means underpriced risks are more vulnerable than ever.”

This trend underscores the need for actuarial precision and disciplined underwriting. Long-term profitability now hinges on the ability to anticipate inflationary impacts and adjust rates proactively.

In the construction space, tariff-driven material cost spikes make claims more costly. Workers’ compensation – while still profitable – is feeling the bite of medical inflation.

Legal volatility is another growing concern. The Argo report cited a surge in “nuclear verdicts” — outsized jury awards that exceed actual damages – whose unpredictability makes risk pricing more complex and forces insurers to invest more heavily in legal expertise and claims discipline.

Stephen Perrella, Argo’s chief claims officer and a former trial lawyer, said, “In law school, you learn that our justice system is designed to make a plaintiff whole – no more, no less. But today…in many jurisdictions, verdicts far exceed actual damages.”

Perella pointed to states like Georgia and Florida, where outsized verdicts and systemic inefficiencies have triggered tort reform only after insurers began pulling out of the market.

“The problem is we’re implementing tort reform once those abuses have begun to overwhelm a just system,” he said.

For specialty insurers, talent constraints remain an operational risk.

“With large portions of the workforce retiring and a limited pipeline of experienced underwriters, claims professionals, and actuaries entering the field, competition for expertise is intense,” the report says. “That pressure is especially acute for carriers navigating complex risks and high-touch broker relationships.”

That means hiring the right people is only part of the solution. Argo emphasizes the need to build teams that work seamlessly together and develop talent that is ready for whatever comes next.

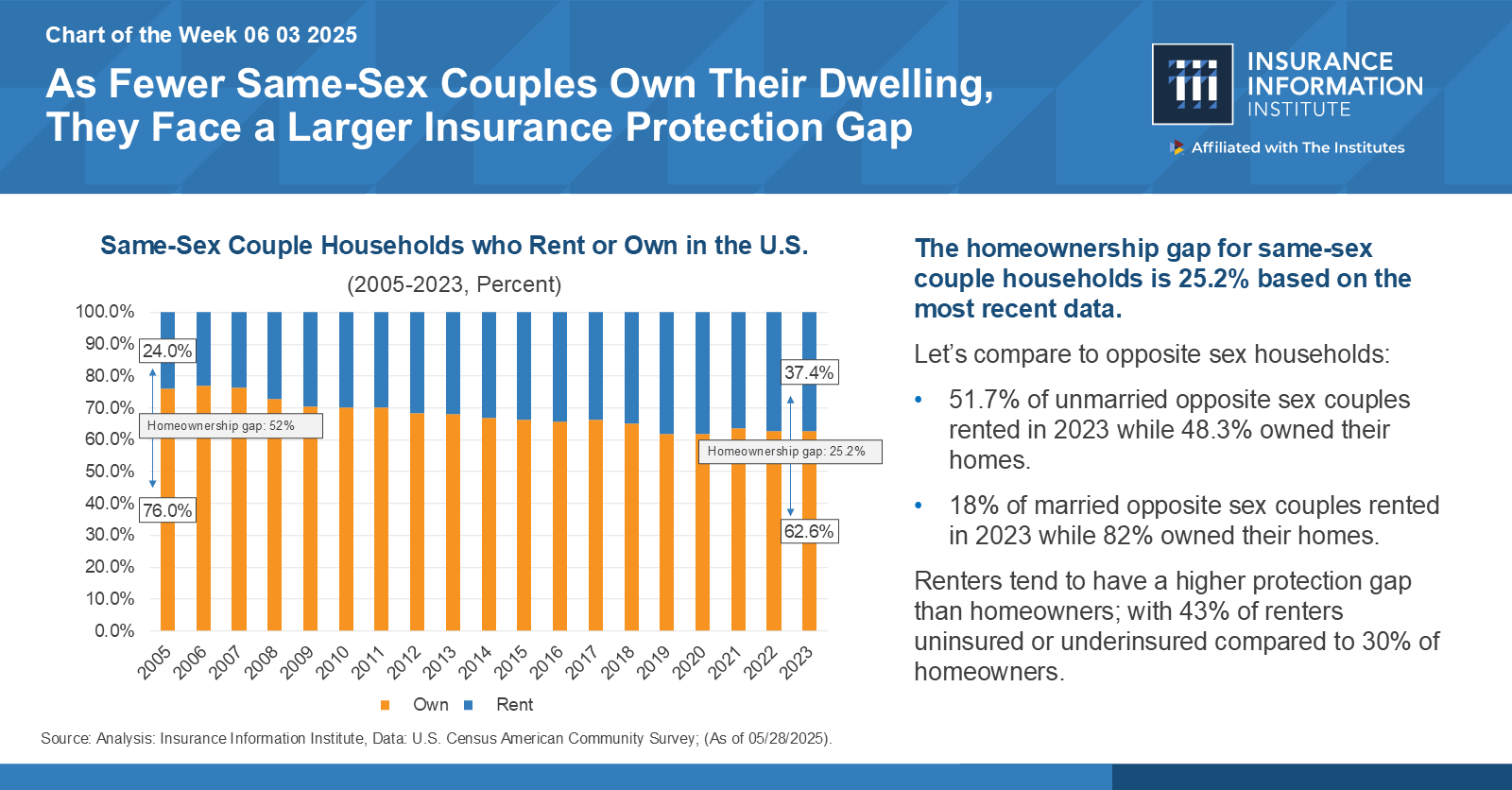

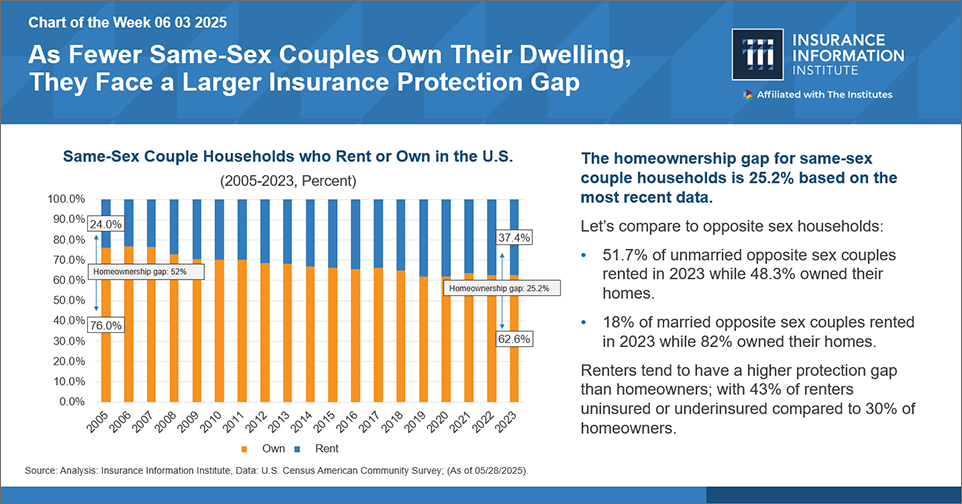

The homeownership gap for same-sex couple households is 25.2% based on the most recent data.

As part of an ongoing discussion on the link between the housing and insurance markets, the Insurance Information Institute (Triple-I) released a Chart of the Week (COTW), “As Fewer Same-Sex Couples Own Their Dwelling, They Face a Larger Insurance Protection Gap.” Based on data from 2023, 62.6 percent of same-sex households own their homes and 37.4 percent rent, representing a homeownership gap of 25.2 percentage points within this community. In comparison, 82 percent of married opposite-sex households own their homes, while only 18 percent rent.

In the United States, homeownership offers several benefits (versus renting) to those with the financial resources to achieve and sustain it. Owners can accrue equity to increase their chances of making a profit when they sell their home. They can reap tax benefits through mortgage deductions. Mortgage holders can also lower monthly housing costs when interest rates drop. Ultimately, a home can increase personal net worth and offer a mechanism to transfer wealth to the next generation. Protecting this asset and its contents makes good financial sense.

Renters may not own their dwelling, but they keep personal belongings in it. They can face serious financial risks in the event of a loss, theft, disaster, or personal liability event. Yet, according to the COTW, 43 percent of renters are uninsured or underinsured, compared to 30 percent of homeowners. There are several reasons attributable to this difference, but it’s essential to keep one at the forefront: insurance coverage requirements are commonplace in mortgage agreements but not in lease agreements. Thus, homeownership status can drive participation in the insurance market.

Examining factors that impede homeownership for same-sex couples might shed light on how to attract and retain more policyholders in this demographic. Looking closely at the interplay of just three of these – housing prices, geography, and legislative environment – reveals that housing tends to be more expensive in LGBTQIA+-friendly areas. Prospective buyers may need to earn at least $150,000 a year – as much as 50 percent more – to avoid living in regions without basic legal protections, according to a recent study of real estate market data across 54 major U.S. metropolitan areas.

High monthly housing costs strain budgets, pushing homeowners and renters out of the insurance market. It can also put the financial qualifications for home buying – i.e., building credit and savings – out of reach. Households are considered cost-burdened when they spend more than 30 percent of their income on rent, mortgage payments, and other housing costs, according to the U.S. Department of Housing and Urban Development (HUD).

Nationwide, renters hadhigher median housing costs as a percentage of their income (31.0 percent) compared to homeowners (21.1 percent for homeowners with a mortgage and 11.5 percent for those without a mortgage). In metropolitan areas that welcome and protect diversity, renters are more likely to behousing cost-burdened, particularly in New York (52.1 percent of residents pay more than 30 percent of their income) and San Francisco (37.6 percent of residents). Renters in states and municipalities where legislation is considerably less welcoming but rents are lower can face comparativelyhigher premiums for rental coverage.

Despite the legalization of same-sex marriage and various anti-discrimination laws, the LGBTQ community still battles considerable discrimination and systemic biases in many areas of life, including housing. Insurers can work to better understand the diverse needs of LGBTQIA+ individuals, couples, and their families, facilitating more effective solutions for managing financial risks. And most importantly, the industry can improve communication around potential coverage benefits for these households.

“We can start closing the protection gap by having people at the table who understand the lived experiences behind the numbers,” says Amy Cole-Smith, Executive Director for BIIC/ Director of Diversity at The Institutes.

For example, renters might find it helpful to know their policy covers a loss event linked to discrimination against them, such as malicious damage or vandalism to the property by a third party. Even when it’s evident the destruction isn’t the renter’s fault, the landlord might still attempt to hold them responsible, either through a lawsuit, a rent increase, or eviction. Additionally, unmarried couples should be informed about whether the insurer includes both partners’ names on a policy and how this provision affects them in the event of a claim.

“Cultivating an inclusive workforce drives smarter solutions, like renters’ insurance that aligns with the realities of same-sex couples, more equitable underwriting, and marketing that truly resonates,” Cole-Smith says. “This isn’t just about equity—it’s about unlocking growth and staying competitive in a changing market. When the insurance workforce reflects the diversity of the market, we’re in a stronger position to build products that meet people where they are.”

Triple-I works to advance the conversation around crucial issues in the insurance industry, including Talent and Recruitment. To join the discussion, register for JIF 2025. We also invite you to follow our blog to learn more about trends in insurance affordability and availability across the property/casualty market.

By Loretta L. Worters, Vice President, Media Relations, Triple-I

Vacant homes often carry more risk than meets the eye. From burst pipes and property theft to liability and squatter intrusion, a home left unoccupied for an extended period is exposed to a unique set of hazards, many of which may not be covered by a standard homeowners’ insurance policy.

Consider a recent case involving a homeowner who inherited a family property located several states away. With plans to sell the home, they left it unoccupied while it sat on the market through the winter months. After more than 60 days without a visit, the homeowner returned to find a devastating scene: a pipe had burst during a hard freeze, flooding much of the house.

Without anyone home to detect the issue, water had leaked for days — possibly weeks —causing severe damage to ceilings, walls, flooring, heating and electrical systems. The estimated cost of repairs exceeded $60,000.

Unfortunately, their standard homeowners insurance policy excluded coverage due to a vacancy clause, which had been triggered by the home’s unoccupied status.

Understanding Vacancy Clauses

Most homeowners insurance policies include a vacancy clause, which limits or excludes coverage if the property is unoccupied for typically 30 to 60 consecutive days. This is because vacant properties present heightened risks, including:

Undetected water leaks or burst pipes;

Increased likelihood of theft, vandalism, or trespassing;

Greater exposure to fire damage or electrical deficiencies; and

Liability if someone is injured on the property.

If a home will be vacant for an extended period, whether due to a sale, relocation, inheritance, or renovation, it’s essential to inform your insurance carrier and review your coverage options.

Water damage is one of the most common and expensive issues in unoccupied homes. Repairing damage from a burst pipe can cost $10,000 to $70,000 or more, depending on how long the issue goes unnoticed. In vacant homes, where regular checks are infrequent, leaks can continue for extended periods before detection, significantly increasing repair and remediation costs.

Vacant properties also are more susceptible to theft and unauthorized occupancy. Copper piping, appliances, and even fixtures can be attractive to criminals. Squatters present another challenge: in some jurisdictions, they can gain tenant rights if not removed promptly, leading to legal costs and delays.

Many standard policies exclude or limit coverage for theft and vandalism once a home is deemed vacant. This makes proper coverage even more important for homeowners who leave properties unoccupied, even temporarily.

Homeowners may be surprised to learn that liability exposure continues even when no one lives there. Injuries on vacant property can lead to significant financial losses.

Common examples include:

A delivery person slips on an icy walkway and seeks damages;

A contractor or realtor trips and is injured during a property showing; or

A child enters the home and is hurt while exploring.

In such cases, the homeowner may be held liable, and, if the home is classified as vacant under the policy, liability coverage could be denied. Legal expenses and settlements can easily run into six figures.

Vacancy endorsements are available

To manage the elevated risks of a vacant property, insurers offer vacant home insurance policies or vacancy endorsements. These policies are designed to cover unoccupied properties and typically include:

Water damage from plumbing or heating failures;

Fire, lightning, windstorm, and hail damage;

Theft, vandalism, and damage caused by trespassers; and

Coverage for legal liability in the event of injury on the property.

While these policies tend to be more expensive than standard homeowners insurance, they provide critical protection.

Vacant home policies often still include protection for “sudden and accidental” events, such as a pipe bursting due to freezing temperatures. However, insurers typically require proof that reasonable steps were taken to maintain the property. Failing to heat the home during the winter, for example, could void coverage even under a vacant home policy.

Whether a home is vacant for weeks or months, the following steps can help reduce your exposure:

Maintain indoor heat: Keep the thermostat at least 55°F during winter months.

Shut off the water supply: Or fully winterize the plumbing system.

Secure all entry points: Lock doors and windows; consider reinforced locks.

Install remote monitoring systems: Leak detectors, thermostats, and cameras can provide early warnings.

Schedule regular visits: Have a neighbor, family member, or property manager check the home weekly.

Maintain walkways and lighting: Reduce the risk of slip-and-fall injuries with proper upkeep.

Communicate with insurer: Always notify an insurer if the home will be unoccupied for an extended period.

Leaving a home unoccupied for months without adjusting your insurance coverage can expose you to significant financial risk. From costly repairs and legal liability to denied claims, the consequences can be catastrophic.

Before leaving a property vacant, whether due to sale, inheritance, or temporary relocation, homeowners should consult their insurance agent to identify the appropriate coverage. Obtaining a vacant home insurance policy or endorsement can protect both the property and the homeowner’s financial security.

By Loretta L. Worters, Vice President of Media Relations, Triple-I

When Karla Scott first entered the insurance industry, she didn’t set out with a grand plan to become a leader in marine underwriting.

“I fell into it,” she admits. Starting at a brokerage firm focused on logistics insurance, she quickly discovered a passion for global trade and cargo underwriting.

“It’s different every day,” says Scott, who is global logistics product leader and senior managing director, Ocean Marine, The Hartford. She joined the company after The Hartford acquired Navigators in 2019.

“The technical work keeps my skills sharp, while the camaraderie and shared purpose offer personal and professional fulfillment.”

– Karla Scott

Scott works with clients, agents, and brokers around the world to ensure that businesses have the protection they need through the product’s entire supply-chain life cycle. Her team insures raw materials and finished goods that are transported on containerships, planes, trains, and trucks. From geopolitics to commodity shifts, it’s an ever-evolving, complex industry that demands constant awareness and adaptation.

Now, with 24 years in marine insurance, Scott reflects on a career shaped by resilience, strong mentorship, and a deep commitment to community. Her journey underscores both the opportunities and challenges faced by women in a traditionally male-dominated field.

“Disrupting trade with…China, Canada, or Mexico would affect cost and the availability of insurance coverage.”

– Karla Scott

A Sea Change for Women

“Fifteen years ago, I sat at a table with 35 industry leaders and was the only woman,” Scott says. “But progress is happening. While marine insurance remains a niche within the broader insurance world, more women are entering the field and rising into leadership roles.”

There continues to be a gender pay gap and lack of career advancement opportunities, but Scott says “part of the reason, frankly, is that women tend not to self-advocate. It’s critical in the marine insurance space to promote yourself, but women often feel uncomfortable doing that. Self-advocacy is not boastfulness. No one is going to put you in the spotlight unless you step into it. Those are the skills we need to teach women coming up in this business.”

Being a woman on the West Coast in an East Coast-dominated industry meant navigating additional hurdles.

“There’s a current you swim against,” she says.

Overcoming Barriers

Support from forward-thinking male mentors and advisors helped her stay the course.

“I am indebted to three mentors who presented different strengths,” Scott says. “I learned how to manage people, to motivate people, technical skills, how important your reputation is in this industry, and how to push hard and be aggressive in certain situations and not aggressive in other situations.”

She also candidly addresses the internal battles many women face — imposter syndrome.

“I’ve experienced it myself and have reached out to my mentors, who are great at listening to my frustrations,” she says. “Having a strong network can help you work through those issues. Now that I’m on the other side, I’m pushing my mentees through those obstacles, helping them find their voice and teaching them to self-advocate—skills critical to closing the gender pay gap.”

The Power of Community

Scott’s involvement with the American Institute of Marine Underwriters (AIMU) and the Board of Marine Underwriters in San Francisco has been instrumental in her career. She has served as president of the latter twice and speaks passionately about the importance of collaboration in the insurance industry.

“One of the most unique parts of marine insurance is that we work in partnership with competitors to solve industry problems,” she says. “The technical work keeps my skills sharp, while the camaraderie and shared purpose offer personal and professional fulfillment.”

Trade Tensions and Industry Impacts

As global trade faces increasing scrutiny and tariff battles, Scott is already seeing the effects.

“Clients are canceling freight contracts, and volumes are dropping,” she says. “The result means lower trade volume, higher valuation of goods, and potential inflationary cycles may hit consumers hard.”

She points out that the lack of federal stimulus (unlike during the pandemic) leaves little room for economic cushioning.

“It’s a ‘hold your breath’ kind of moment,” Scott says.

Cargo theft is another growing concern.

“It spikes when inflation rises,” Scott notes, pointing out how easy it has become to resell stolen goods on platforms like Amazon and eBay.

Talk of reshoring manufacturing often overlooks the complexity of global trade.

“You can’t flip a light switch and manufacture everything in the U.S.,” she explains. “Machinery to build those goods often comes from Germany or Japan.

“Disrupting trade with top partners like China, Canada, or Mexico would significantly affect both cost and the availability of insurance coverage,” Scott says. “If consumer confidence drops and trade volumes fall, insurance demand will, too.”

Scott also highlights a deeper economic risk: the potential erosion of the U.S. dollar’s dominance in global trade. “If that shifts, the American economy could face even greater challenges.”

South Carolina’s liquor liability insurance market is in crisis, with insurers losing an average of $1.77 for every $1.00 of premium earned since 2017, while claim frequencies significantly outpace neighboring states, according to a recent study by the state’s Department of Insurance.

The comprehensive analysis, initiated following a 2019 request by the South Carolina Senate Judiciary Committee, reveals a deeply troubled marketplace where insurers are losing money.

“The data seem to confirm the anecdotal assertions, made by both insurance companies and small businesses, of a very troubled and challenged marketplace,” the report stated.

Current Market Landscape

The liquor liability insurance market in South Carolina has maintained a relatively stable number of participants in recent years. Since 2019, the number of insurance groups operating in this sector has held steady at around 48 participants. This consistency in market players suggests a mature, albeit challenging, insurance environment.

Despite the overall stability in participant numbers, the market is characterized by the dominance of three major insurance groups.

Premium Trends

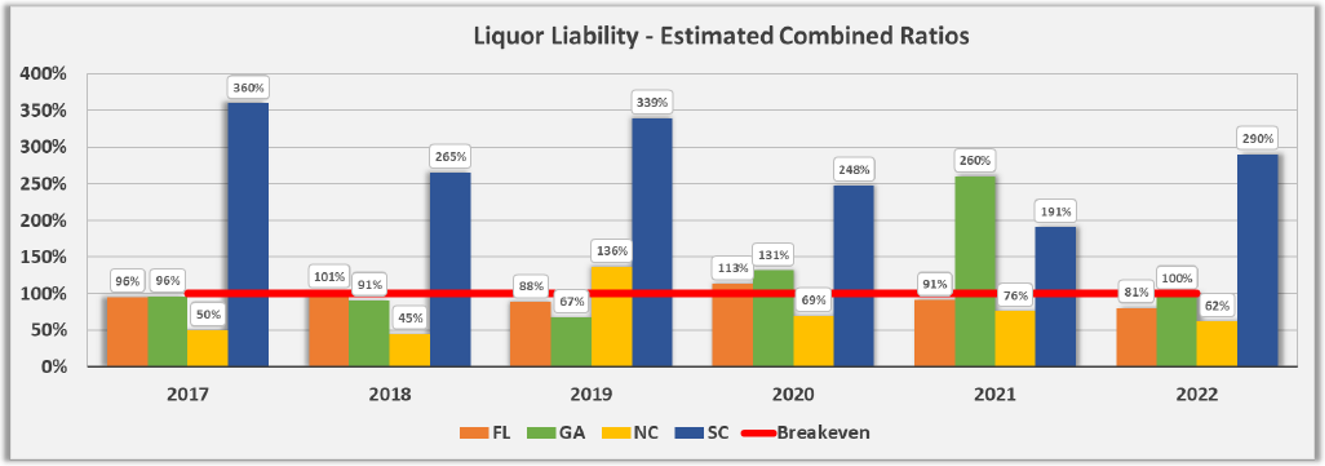

While the number of market participants has remained relatively constant, earned premiums have experienced remarkable growth over a five-year period. From 2017 to 2022, earned premiums in the South Carolina liquor liability insurance market more than doubled to $17.0 million from $7.6 million.

This dramatic surge in premiums can be attributed to various factors, but rising insurance rates play a crucial role, the report noted.

Profitability Crisis in South Carolina

Since 2017, liquor liability insurers have lost about $1.77 for every $1.00 of premium earned over the six years observed. In the best performing of those six years (2018), the industry lost roughly $0.91 per $1.00 of premiums earned, while losing about $2.60 per $1.00 of premiums earned in the worst performing year, 2022.

“Combined ratios for the industry make it clear that this sub-line of insurance is being written at massive underwriting losses,” the report’s authors stated.

Source: South Carolina Department of Insurance

The severity of South Carolina’s liquor liability insurance crisis becomes even more apparent when compared to their neighboring states, where these same insurers have realized a net profit over time, the report noted.

Over the same 2017-2022 period analyzed, for example, North Carolina’s estimated liquor liability combined ratio ranged between 45% and 76%. In 2022, when South Carolina’s estimated combined ratio hit 290%, North Carolina’s stood at 62%.

Claims Severity and Frequency

The liquor liability insurance market in South Carolina also has experienced significant fluctuations in claim severity over recent years. In 2022, the average incurred claim per $1 million of earned premium reached $281,071, a substantial increase from $121,761 the previous year. This figure, however, falls within a broader historical context of volatility. The state witnessed its highest average claim of $338,244 in 2017, followed by a dramatic drop to $121,761 in 2021.

Despite these fluctuations, recent data suggests that South Carolina’s claim severity is aligning more closely with neighboring states in recent years, according to the report.

While severity trends show signs of alignment with regional norms, claim frequency in South Carolina presents a more pressing challenge.

From 2019 to 2022, South Carolina’s claim frequency (number of incurred claims per $1 million of earned premium) has outpaced that observed in the other states considerably. The claims frequency rate was nine in 2022, 13 in 2021, 10 in 2020 and 12 in 2019. During that same period, none of its neighboring states — Florida, Georgia and North Carolina — reported a claims frequency rate higher than five.

Did you know that December 14 is international monkey day? This delightful holiday to honor everyone’s favorite simians was invented by two Michigan State art students in 2000.

Of course, here at the Triple-I, the holiday naturally got us thinking about people who keep monkeys and other exotic and unusual pets, and the insurance implications.

Nevertheless, according to one animal advocacy group, about 15,000 primates are kept as pets in the U.S., and the American Veterinary Medical Association estimates that 1 in 10 American households has an exotic pet (defined as any animal native to a foreign country).

Injuries caused by pets, if they are covered by insurance, would be covered under a comprehensive homeowners insurance policy. However it’s important to read your policy and see exactly what’s covered. If you’re not sure, speak to your insurance agent. You should expect to pay more for coverage and carry higher liability limits if you legally own exotic animals. And homeowners insurance also frequently excludes any physical damage caused by pets.

Exotic animals can require expensive veterinary treatments. While pet health insurance is becoming increasingly available and affordable, many insurers cover a restricted list of species. Pet Assure, a discount program available through some employers, is accepted for many kinds of animals.

Most people don’t like to think about risk — especially when planning a holiday abroad. If they think about travel risk at all, it tends to be in terms of nuisances like flight cancellations or misrouted luggage.

The collapse of British travel company Thomas Cook, which left many thousands of travelers stranded, highlights the types of risks travelers rarely think about.

This week’s seemingly overnight collapse of British travel company Thomas Cook – leaving approximately 600,000 travelers stranded worldwide and leading U.K. authorities to launch what has been called be the “largest peacetime repatriation ever” – underscores several of the myriad risks that most travelers rarely think about.

For better or worse, when I hear “repatriation” the word is typically followed in my mind by “of remains.” While mass repatriations like the one occurring this week are rare, people often die while traveling for pleasure or business. Whether it’s headline-grabbing strings of mysterious deaths like those in the Dominican Republic earlier this year or more common, less publicized deaths by auto, drowning, or natural causes, the cost and complexity of returning the bodies of loved ones can compound the stresses typically experienced by grieving families. A travel policy with adequate coverage for repatriation of remains is a relatively inexpensive way to help address this burden.

Now, you’re even more likely to become ill or injured while traveling than you are to die. Have you checked your current health insurance to see what it does and doesn’t cover when you’re traveling outside your country? Depending on what you learn, you may want to consider buying medical travel insurance. If your health policy does provide international coverage, the U.S. State Department advises that you remember to carry your insurance policy identity card and a claim form.

In the case of a serious illness or injury, the State Department says, medical evacuation can cost more than $50,000, depending on your location and condition. A policy that covers medical evacuation and emergency extraction (say, in the event of natural disaster or political unrest) also is worth considering for international trips.

Perhaps the most important lesson to draw from the “surprise” collapse of 178-year-old Thomas Cook is that it wasn’t exactly a surprise for those who were paying attention. As the U.K.-based Guardian news site reports, “The tour operator’s woes go back much further” than its inability to secure a £200 million lifeline from its bankers. The Guardian calls Thomas Cook “a victim of a disastrous merger in 2007, ballooning debts and the internet revolution in holiday booking. Add in Brexit uncertainty, and it was perhaps only a matter of time before the giant of the industry collapsed.”

Travelers often are so focused on capturing bargains that they don’t take the time to research the organizations bringing them great deals or the safety considerations in the lovely destinations being marketed to them. In travel, as in other adventures, it’s often the case that “you get what you pay for.”

Maybe a bit of research might have kept some of the hundreds of thousands of inconvenienced Thomas Cook clients from putting all their holiday eggs in a single overstuffed basket.

{kind=link}