Insurance coverage has long been “a grudge purchase – a once-or-twice-a-year transaction that many consumers didn’t want to think about,” Triple-I CEO Sean Kevelighan said in a recent episode of the “All Eyes on Economics” podcast.

But in today’s dynamic economic environment – marked by inflation the likes of which most insurance purchasers have never experienced – it has become more important than ever for consumers and policymakers to understand how insurance is underwritten and priced.

One of Triple-I’s chief objectives is “helping people understand what insurance can do for you, but also what you can do to change the situation,” Kevelighan told podcast host and Triple-I Chief Economist and Data Scientist Michel Léonard. “The narrative seems, at least from my standpoint, to be less about, ‘Why is my insurance so high?’ It’s more about, ‘What can we do to get it lower?’”

Rising insurance premium rates are the effect of risk levels, loss costs, and economic considerations like inflation. Too often, though, they’re discussed as if they were the cause.

High property/casualty premium rates are the result of numerous coalescing factors: Increased litigation, inflation, antiquated state regulations, losses from natural catastrophes, and pervasive post-pandemic high-risk behaviors, to name a few.

Every dollar invested in disaster resilience could save 13 in property damage, remediation, and economic impact costs, according to a recent joint report from Allstate and the U.S. Chamber of Commerce. As areas vulnerable to climate disasters become increasingly populated, it’s important for policyholders to develop resilience measures against the wildfire, hurricane, severe convective storm, and flood risks their property faces.

Consumer education and community involvement in mitigation and resilience offer a path toward greater control over claims.

However, regulatory barriers to fair, accurate underwriting also contribute to higher insurance costs. Despite tort reforms, rampant litigation has kept upward pressure on rates in Florida and Louisiana. California’s outdated Proposition 103 – by barring insurers from using modeling to price risk prospectively and from taking reinsurance costs into account when setting rates – has impeded insurers from using actuarially sound insurance pricing.

Confusion around industry practices and effective mitigation is understandable, and during periods of economic instability and unforeseen disasters, blaming the insurance industry may seem the most direct way to regain control.

But rising rates are “not just an insurance problem,” Kevelighan said. “It’s a risk problem, and we all play a role in addressing that risk.”

Hurricane Beryl’s rapid escalation from a tropical storm to a Category 5 hurricane does not bode well for the 2024 Atlantic Hurricane season, which is already projected to be of above-average intensity, warns Triple-I non-resident scholar Dr. Philip Klotzbach.

“This early-season storm activity is breaking records that were set in 1933 and 2005, two of the busiest Atlantic hurricane seasons on record,” Dr. Klotzbach, a research scientist in the Department of Atmospheric Science at Colorado State University, recently told The New York Times.

The quick escalation was a result of above-average sea surface temperatures. A hurricane that intensifies faster can be more dangerous as it leaves less time for people in its path to prepare and evacuate. Last October, Hurricane Otis moved up by multiple categories in just one day before striking Acapulco, Mexico, as a Cat-5 that killed more than 50 people.

After weakening to a tropical storm, Beryl made landfall as a Cat-1 hurricane near Matagorda, Texas, around 4 a.m. on July 8, according to the National Hurricane Center, making it the first named storm in the 2024 season to make landfall in the United States. Beryl unleashed flooding rains and winds that transformed roads into rivers and ripped through power lines and tossed trees onto homes, roads, and cars. Restoring power to millions of Texans could take days or even weeks, subjecting residents who will not have air conditioning to further risk as a sweltering heatwave settles over the state.

Extreme heat was just one climate-related topic addressed by Triple-I Chief Insurance Officer Dale Porfilio in an interview with CNBC’s “Last Call” on July 9. While most farmers are insured against crop damage due to heat conditions and homeowners insurance typically covers wildfire-related losses, Porfilio noted, a “more subtle impact is on roofs that we thought were built to a 20-year lifespan.”

When subjected to extreme heat, roofs can become more brittle and prone to damage from wind or hail.

“So, you have to think about the roof coverage on your home insurance policy,” Porfilio said.

He also pointed out that flood risk represents “one of the biggest insurance gaps in this country. Over 90 percent of homeowners do not have the coverage.”

Many people incorrectly believe homeowners insurance covers flood damage or that they don’t need the coverage if their mortgage lender does not require it.

In an interview on CNBC’s “Squawk Box,” Triple-I CEO Sean Kevelighan discussed the potential impact of the predicted “well above-average” 2024 season on the U.S. property/casualty market.

“This is what the insurance industry is prepared for,” Kevelighan said. “It keeps capital on hand after writing policies to make sure that those promises can be kept.” The P/C industry has $1.1. trillion in surplus as of March 31, 2024.

Kevelighan pointed out that the challenges to the industry go beyond climate-related trends, explaining how legal system abuse, regulatory environments, shifting populations, and inflation are impacting insurers’ loss costs.

In Florida, for example, “you’ve got over 70 percent of all homeowners insurance litigation residing in that state, whereas it represents less than 10 percent of the overall claims.”

He pointed out that Florida’s insurance market has improved – with homeowners insurance premium growth flattening somewhat – as a result of tort reform legislation and added that Louisiana’s legislature addressed insurance reform during its most recent session.

“In California, insurers can’t catch up with inflationary costs because of regulatory constraints,” Kevelighan noted. “They are not able to model [climate risk] and are not able price reinsurance into their policies.”

California’s wildfire situation is complex, and the state’s Proposition 103 has hindered insurers’ ability to profitably write homeowners coverage in that disaster-prone state. In late September 2023, California Insurance Commissioner Ricardo Lara announced a package of executive actions aimed at addressing some of the challenges included in Proposition 103. Lara has given the department a deadline of December 2024 to have the new rules completed.

Home and auto insurance premium rates have been a topic of considerable public discussion as rising replacement costs and other factors – from climate-related losses to fraud and legal system abuse – have driven rates up and, in some states, crimped availability and affordability of coverage.

It’s important for policyholders and policymakers to understand the role of economic conditions and trends in setting rates. Jennifer Kyung, Property and Casualty Chief Underwriting Officer at USAA, opens a window into the complex world of underwriting and economics in a recent episode of Triple-I’s All Eyes on Economics podcast.

Kyung told podcast host and Triple-I Chief Economist and Data Scientist Dr. Michel Léonard that economic analysis “is critical to us in underwriting and as we manage our plan.” She described economics as “part of our muscle memory as underwriters” – adding that the economic uncertainty of recent years reinforces the need for underwriters to have “a very agile mindset.”

Underwriting and economics are “a little bit art and science,” representing a balancing act between sophisticated data analytics and creative problem-solving.

“When we think about sales and premiums for homeowners, we may look at things like mortgage rates or new home starts to indicate how the market is going,” Kyung said. “In auto, we might look at new vehicle sales or auto loan rates. These, in combination, help us look at macro-economic trends and the environment and how that might interplay with our volume projections. That helps us with financial planning, as well as operational planning.”

“It’s really critical to keep these on the forefront on an ongoing basis throughout the year,” she said, “so we can adjust as needed…. As our results come in, this gives context to the results.”

Through continual analyses of external market conditions and the internal quality and growth of your business, Kyung said, underwriters “can manage and mitigate some of the volatility and risk for our organizations.”

A tool she recommends for evaluating economic indicators is Triple-I’s replacement cost indices, which track the evolution of replacement costs throughout time across various lines of insurance and geographic regions. These indices enable insurers to synthesize raw economic data and insurance market trends, providing an auxiliary framework to bolster financial and operational planning.

Kyung said Triple-I offers additional insight into “local flavor,” or “understanding what the emerging issues are…related to the local environment,” through such tools as Issues Briefs and Insurance Economics Profilers. Recent supply-chain disruptions have accentuated the relationship between local and global economies, revealing the importance of employing local economic analytics to interpretations of broader insurance market patterns.

Such fusions can help facilitate efficient planning in the face of shifts in the insurance landscape.

The full interview is available now on Spotify, Audible, and Apple.

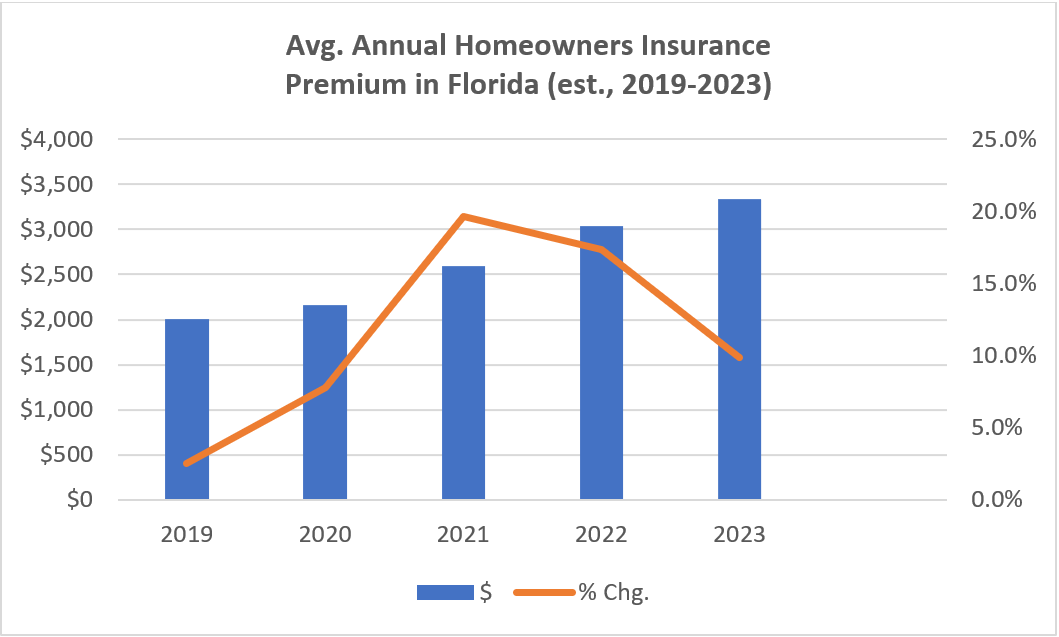

Homeowners insurance premium growth in Florida has slowed since the state implemented legal system abuse reforms in 2022, according to a Triple-I analysis.

As shown in the chart below, average annual premiums climbed sharply after 2020. This was due in part to inflation spurred by the COVID-19 pandemic and the war in Ukraine as well as longtime challenges in the state with claim fraud and legal system abuse.

Source: Triple-I analysis of NAIC and OIR data

According to the state’s Office of Insurance Regulation (OIR), Florida accounted for nearly 71% of the nation’s homeowners claim-related litigation, despite representing only 15% of homeowners claims in 2022, the year Category 4 Hurricane Ian struck the state. In that same year, and prior to Ian making landfall in the state as a first major hurricane since 2018’s Hurricane Michael, six insurers declared insolvency. Hurricane Ian became the second largest on record by insured losses, in large part because of the extraordinary litigation costs estimated to result in Florida in the aftermath.

The Florida Legislature responded to the growing crisis by passing several pieces of insurance reform, primarily tackling problems with assignment of benefits (AOB), bad-faith claims, and excessive fees. For example, the new laws eliminated one-way attorney fees in property insurance litigation, forbid using appraisal awards to file a bad-faith lawsuit, and prohibited third parties from taking AOBs for any property claims. The legislation also ensures transparency and efficiency in the claims process and encourages more efficient, less costly alternatives to litigation.

A surge in litigation

Litigation spiked when backlogged courts reopened following the pandemic, then again when the reforms were passed in 2022 and 2023, as plaintiffs’ attorneys raced to file suits ahead of implementation of the legislation.

This increase in litigation, combined with persistently strong inflation, contributed to increased loss costs and premium increases. In 2022, average homeowners premium rates rose more than 17 percent, to $3,040. Premiums continued to rise in 2023, although at a decreasing rate, as inflation has moderated and legal reforms have kicked in.

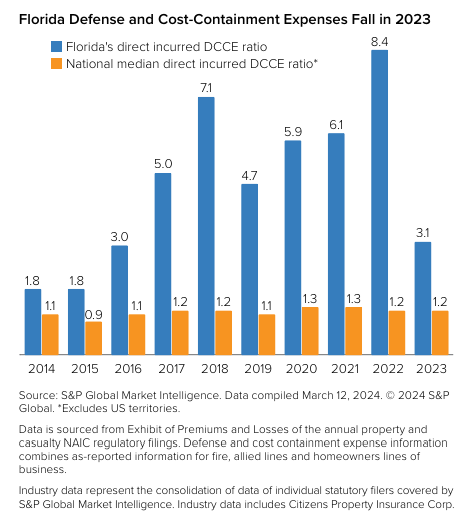

There are early signs that the reforms are beginning to bear fruit. In 2023, Florida’s defense and cost-containment expense (DCCE) ratio – a key measure of the impact of litigation – fell to 3.1, from 8.4 in 2022, according to S&P Global. In dollar terms, 2023 saw $739 million in direct incurred legal defense expenses – a major decline from 2022’s $1.6 billion. For perspective, incurred defense costs in the two largest U.S. insurance markets in 2023 were $401.6 million in California, followed by $284.7 million in Texas. As the chart below shows, Florida’s DCCE ratio – even during its best years – regularly exceeds the nation’s.

As insurers have failed or left the state, Citizens Property Insurance Corp. – the state-run insurer of last resort and currently Florida’s largest residential insurance writer – has swelled with new business and lawsuits. Citizens’ depopulation efforts to move policyholders to private insurers contributed to policy counts falling to 1.23 million by the end of 2023.

It’s important to remember that all premium estimates are based on the best information available at the time and actual results may differ due to changes in market conditions. For example, earlier Triple-I projections that average annual homeowners premiums in Florida would exceed $4,300 in 2022 and $6,000 in 2023 assumed significant rate increases would be needed to restore profitability to the state’s homeowners market. These projections did not assume legislative reform or that Citizens would become the state’s largest homeowners insurance company, with many risks priced below the admitted and excess and surplus markets. Our projections also assumed inflation would continue to grow at rates similar to those prevailing at the time.

In light of the reforms and moderating inflation, we are now reporting lower average annual premiums of $3,040 (2022) and $3,340 (2023). The Florida OIR has reported average premium rate filings are running below 2.0 percent in 2024 year-to-date in the private market. Further, OIR indicated eight domestic carriers have filed for rate decreases and 10 have filed for no increase this year. Additionally, eight property insurers have been approved to enter the Florida market, with more expected this year.

Triple-I will continue to monitor and report on the evolving property insurance market in Florida.

Triple-I has published a great deal regarding the potential impact of TPLF on costs for insurers and policyholders. Bellino’s gaze focused on potential risks for the judiciary:

Increased judicial workload

More fraudulent claims

Longer litigation and slower settlements

Creation of potential appellate issues

And, like many insurance industry stakeholders, Lisa M. Bellino (VP Claims Judicial & Legislative Affairs for Zurich North America in Philadelphia) is fundamentally concerned about the lack of transparency surrounding TPLF’s involvement in a lawsuit.

TPLF is a growing and costly aspect of legal system abuse, a problem that Triple-I and other industry thought leaders define as policyholder or plaintiff attorney actions that unnecessarily increase the costs and time to settle insurance claims. Qualifying actions can arise, for example, when clients or attorneys draw out litigation in hopes of a larger settlement simply because TPLF investors take such a giant piece of the payout. As there is little transparency around the use of TPLF, insurers and the courts have virtually no leeway in mitigating any of this risk.

TPLF can lead to undue judicial burden and waste.

When judges are unaware of the funding arrangement, they would likely also be in the dark about potential conflicts of interest or improper claims and, therefore, be unable to mitigate these risks. However, Bellino argues that the de facto practice of secrecy can cause judicial waste even in the limited number of jurisdictions and courts that require disclosure. Judges may feel compelled to spend a significant amount of time ascertaining attorney compliance. As funding often involves parties not directly related to the case, the judiciary may need to hold additional hearings and reviews to uncover the real parties in interest. Bellino cites a case in which the real parties were not the named plaintiffs.

TPLF can be a driving factor behind lawsuit generation.

When law firms pursue class action litigation, they may engage “lead generators,” companies that help find plaintiffs for a specific tort. Advertising tactics can include traditional and social media. When prospective claimants respond to these ads, they are directed to a law firm or a call center that distributes the recruited claimants to law firms. This service comes at a steep price – in dollars and justice. As funding may often come from TPLF, Bellino describes how the profit model behind lead generation companies working with law firms can increase the risk of fraudulent claims.

The risk of bogus claims and claimants can surge with TPLF.

Funders of class action litigation have a financial incentive to drive up the number of plaintiffs. As neither the defense nor the judge is typically aware of the third party’s potential conflict of interests, judicial resources can be wasted, and justice can be delayed for legitimate claimants. Bellino cites, among other examples, a New York case to illustrate how litigation funders and attorneys may even collaborate in multi-million dollar fraud schemes.

TPLF funders may encourage drawn-out litigation and hinder settlements

Bellino cites a case highlighting how funders might control litigation and delay resolutions to maximize their returns. A publicly traded TPLF giant allegedly blocked a settlement agreement between a plaintiff and the defendants, resulting in prolonged litigation across multiple jurisdictions. The interference may have led to additional motions, hearings, and opinions, diverting judicial resources from resolving the dispute between the named parties. As a result, costs for the plaintiff, defendant, and the courts likely would’ve soared.

Undisclosed TPLF involvement can spark appellate concerns.

Undisclosed funding agreements can also prevent parties from adequately preparing their cases and preserving appellate issues. For example, a TPLF investor may fund medical testing that leads to recruiting plaintiffs for a class action against a drug manufacturer. If this fact wasn’t disclosed to the defendants or court, at the very least, the defendant wouldn’t have access to information needed for defense or subsequent appeals. Also, the judiciary wouldn’t be able to perform its duty to monitor red flags for potential bias or fraud. It is also possible that the interests of the plaintiff will be affected by other appellate concerns, too.

Increases in litigation and claim costs have threatened the affordability and availability of many areas of insurance coverage. TPLF involvement, like other channels for potential legal system abuse, is nearly impossible to forecast and mitigate. And despite its original intended purpose–to help plaintiffs seek justice– it can extract a disproportionate amount of value from settlements, weakening the primary purpose of a financial payout.

Overall, the shroud of secrecy around TPLF can undermine the legal system, posing threats to unbiased and fair legal outcomes. Bellino strongly advocates for mandatory disclosure of TPLF agreements at the beginning of litigation. A system-wide requirement for early transparency would allow courts and involved parties to address potential conflicts, biases, and fraud early in the process. In her words, “Disclosure may restore reality and close the door on the TPLF Twilight Zone.”

Several metrics that influence auto insurance premium rates are starting to improve, but it will take time for these improvements to be reflected in flattening rates, according to a recent Triple-I Issues Brief.

Direct premiums written and underwriting profitability improved dramatically in 2023. Additionally, 2023 net written premium growth of 14.3 percent is the highest in over 15 years. These are great gains, but it’s important to remember that they come on top of results in 2022 that were the worst in recent years.

The number of drivers on the road and miles driven have returned to pre-pandemic levels – but the risky driving behaviors that led to high losses during the pandemic have not improved. More accidents with severe injuries and fatalities have driven up claims and losses in terms of both vehicle damage and liability, while attracting greater attorney involvement and legal system abuse. Compounding these conditions has been historically high inflation, which puts upward pressure on the material and labor costs, increasing the cost of claims.

Telematics technologies, which allow insurers to analyze risk profiles and tailor rates based on individual driving habits, offer the possibility of some relief. By providing feedback that can influence driving behavior, telematics has been shown to lower risk and help reduce the cost of insurance. An Insurance Research Council survey found 45 percent of drivers said they made significant safety-related changes in how they drove after participating in a telematics program. Another 35 percent said they made small changes.

But broader risk and economic factors are likely to keep premium rates high in most cases for the foreseeable future.

Legislative reforms put in place in 2022 and early 2023 to address legal system abuse and assignment-of-benefits claim fraud in Florida are beginning to help the state’s property/casualty insurance market recover from its crisis of recent years, according to a new Triple-I Issues Brief.

Claims-related litigation is down, the “depopulation” of the state’s insurer of last resort continues apace, and underwriting profitability – while still in negative territory – has improved significantly. Insurers also benefited from a relatively mild 2023 Atlantic hurricane season and a meaningful increase in investment income, posting a net profit for the first time in seven years.

But it’s important to remember that the crisis wasn’t created overnight and that it will take time for the reforms and other developments to be reflected in policyholder premiums. Homeowners should not expect their rates to decline in 2024, despite the improved industry performance, although some regional insurers have filed for small decreases.

“Rates may moderate some compared to prior years,” said Mark Friedlander, Triple-I director of corporate communications, “but rising replacement costs – combined with expected higher reinsurance costs for the June 1 renewals – are going to continue to drive average premiums upward in 2024.”

One factor keeping upward pressure on rates is fraud and legal system abuse. With only 15 percent of U.S. homeowners insurance claims, the state accounts for nearly 71 percent of the nation’s homeowners claim-related litigation, according to Florida’s Office of Insurance Regulation.

There are early signs that recent legislative reforms are beginning to bear fruit. In 2023, Florida’s defense and cost-containment expense (DCCE) ratio – a key measure of the impact of litigation – fell to 3.1, from 8.4 in 2022, according to S&P Global.

But the catastrophe-prone state faces a number of natural challenges, from a projected “extremely active” 2024 hurricane season to wildfires, flooding, and severe convective storms.

“Hurricanes get the most media attention,” Friedlander said, “but severe convective storms inflict comparable losses. And it only takes one bad hurricane season to wipe out the benefits of one or more mild years.”

Auto premiums continue to increase as rising labor and material prices, alongside natural disasters, are forcing insurers to contend with significant losses.

As Triple-I previously found in its January report, Insurance Economics and Underwriting Projections: A Forward View, “commercial auto underwriting losses continue, with a projected 2023 net combined ratio of 110.2, the highest since 2017,” according to Jason B. Kurtz, FCAS, MAAA, a Principal and Consulting Actuary at Milliman. Combined ratio is a standard measure of underwriting profitability, in which a result below 100 represents a profit and one above 100 represents a loss.

Insurers are now having to increase rates in response to losses that are expected to keep rising.

“Nobody wants to have that higher-price bill,” said Sean Kevelighan, Triple-I’s CEO. However, he added companies “need to price insurance according to the risk level that’s out there.”

While inflation is partially to blame for these increases, natural disasters are also contributing to rising costs—and not only in traditionally disaster-prone areas like Florida and California.

As the overall P&C industry has struggled with severe convective storms, hurricanes, and other natural disasters, these losses have also been felt in commercial auto. In fact, 2023 witnessed around two dozen U.S. storms, each with losses of around a billion dollars or more. This included major lightning, hail, and damaging winds around many areas of the of the U.S.

“While a lot of these storms don’t make national headlines, they do tend to be very costly at the local level,” says Tim Zawacki, principal research analyst for insurance at S&P Global Market Intelligence. “And the breadth of where these storms are occurring is something that I think the industry is quite concerned about.”

While disasters and economic inflation continue to roil commercial auto, so too does social inflation. As the Triple-I previously reported, “social inflation,” which is the presence of inflation in excess of economic inflation, has also significantly contributed to increases in commercial auto premiums.

Triple-I found that “from 2013 to 2022, increasing inflation drove losses up by between $35 billion and $44 billion, or between 19 percent and 24 percent. The pandemic brought significant change to commercial auto liability, decreasing claim frequency while increasing claim severity more dramatically.”

This increased claim severity is at least partially due to changing driving patterns since the pandemic, including distracted driving, which involves behaviors like cellphone use while behind the wheel. A Triple-I Issues Brief, Distracted Driving: State of the Risk, enumerated these concerns, which have undoubtedly played a role in rising commercial auto premiums.

Indeed, a confluence of issues are playing into rising auto premiums. While natural disasters are out of the control of insurance providers and their policyholders, other factors must be addressed to steady the cost of this line of insurance. This includes telematics and usage-based insurance, which has gained more acceptance since the pandemic.

Still, it is incumbent on insurers, policyholders, and policymakers to create a more sustainable market for auto insurance, working together to tackle the challenges of both climate risk and dangerous driving behavior.

Even as the Smokehouse Creek Fire – the largest wildfire ever to burn across Texas – was declared “nearly contained” this week, the Texas A&M Service warned that conditions are such that the remaining blazes could spread and even more might break out.

“Today, the fire environment will support the potential for multiple, high impact, large wildfires that are highly resistant to control” in the Texas Panhandle, the service said.

This year’s historic Texas fires – like the state’s 2021 anomalous winter storms, California’s recent flooding after years of drought, and a surge in insured losses due to severe convective storms across the United States – underscore the variability of climate-related perils and the need for insurers to be able to adapt their underwriting and pricing to reflect this dynamic environment. It also highlights the importance of using advanced data capabilities to help risk managers better understand the sources and behaviors of these events in order to predict and prevent losses.

For example, Whisker Labs – a company whose advanced sensor network helps monitor home fire perils, as well as tracking faults in the U.S. power grid – recorded about 50 such faults in Texas ahead of the Smokehouse Creek fires.

Bob Marshall, Whisker Labs founder and chief executive, told the Wall Street Journal that evidence suggests Xcel Energy’s equipment was not durable enough to withstand the kind of extreme weather the nation and world increasingly face. Xcel – a major utility with operations in Texas and other states — has acknowledged that its power lines and equipment “appear to have been involved in an ignition of the Smokehouse Creek fire.”

“We know from many recent wildfires that the consequences of poor grid resilience can be catastrophic,” said Marshall, noting that his company’s sensor network recorded similar malfunctions in Maui before last year’s deadly blaze that ripped across the town of Lahaina.

Role of government

Government has a critical role to play in addressing the risk crisis. Modernizing building and land-use codes; revising statutes that facilitate fraud and legal system abuse that drive up claim costs; investing in infrastructure to reduce costly damage related to storms – these and other avenues exist for state and federal government to aid disaster mitigation and resilience.

Too often, however, the public discussion frames the current situation as an “insurance crisis” – confusing cause with effect. Legislators, spurred by calls from their constituents for lower premiums, often propose measures that would tend to worsen the problem because they fail to reflect the importance of accurately valuing risk when pricing coverage.

The federal “reinsurance” proposal put forth in January by U.S. Rep. Adam Schiff of California is a case in point. If enacted, it would dismantle the National Flood Insurance Program (NFIP) and create a “catastrophic property loss reinsurance program” that, among other things, would set coverage thresholds and dictate rating factors based on input from a board in which the insurance industry is only nominally represented.

U.S. Rep. Maxine Waters (also of California) has proposed a Wildfire Insurance Coverage Study Act to research issues around insurance availability and affordability in wildfire-prone communities. During House Financial Services Committee deliberations, Waters compared current challenges in these communities to conditions related to flood risk that led to the establishment of NFIP in 1968. She said there is a precedent for the federal government to step in when there is a “private market failure.”

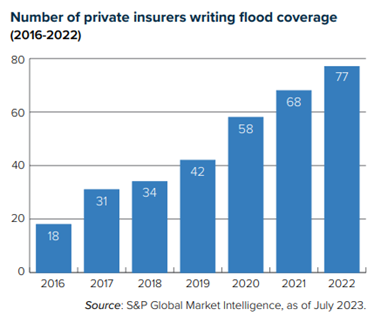

However, flood risk in 1968 and wildfire risk in 2024 could not be more different. Before FEMA established the NFIP, private insurers were generally unwilling to underwrite flood risk because the peril was considered too unpredictable. The rise of sophisticated computer modeling has since given private insurers much greater confidence covering flood (see chart).

In California, some insurers have begun rethinking their appetite for writing homeowners insurance – not because wildfire losses make properties in the state uninsurable but because policy and regulatory decisions made over 30 years ago have made it hard to write the coverage profitably. Specifically, Proposition 103 and its regulatory implementation have blocked the use of modeling to inform underwriting and pricing and restricted insurers’ ability to incorporate reinsurance costs into their premium pricing.

California’s Insurance Commissioner Ricardo Lara last year announced a Sustainable Insurance Strategy for the state that includes allowing insurers to use forward-looking risk models that prioritize wildfire safety and mitigation and include reinsurance costs into their pricing. It is reasonable to expect that Lara’s modernization plan will lead to insurers increasing their business in the state.

It’s understandable that California legislators are eager to act on climate risk, given their long history with drought, fire, landslides and more recent experience with flooding due to “atmospheric rivers.” But it’s important that any such measures be well thought out and not exacerbate existing problems.

Partners in resilience

Insurers have been addressing climate-related risks for decades, using advanced data and analytical tools to inform underwriting and pricing to ensure sufficient funds exist to pay claims. They also have a natural stake in predicting and preventing losses, rather than just continuing to assess and pay for mounting claims.

As such, they are ideal partners for businesses, communities, governments, and nonprofits – anyone with a stake in climate risk and resilience. Triple-I is engaged in numerous projects aimed at uniting diverse parties in this effort. If you represent an organization that is working to address the risk crisis and your efforts would benefit from involvement with the insurance industry, we’d love to hear from you. Please contact us with a brief description of your work and how the insurance industry might help.

Two bills proposed in Illinois this year illustrate yet again the need for lawmakers to better understand how insurance works. Illinois HB 4767 and HB 4611 – like their 2023 predecessor, HB 2203 – would harm the very policyholders the measures aim to help by driving up the cost for insurers to write personal auto coverage in the state.

“These bills, while intended to address rising insurance costs, would have the opposite impact and likely harm consumers by reducing competition and increasing costs for Illinois drivers,” said a press release issued by the American Property Casualty Insurance Association, the Illinois Insurance Association, and the National Association of Mutual Insurance Companies. “Insurance rates are first and foremost a function of claims and their costs. Rather than working to help make roadways safer and reduce costs, these bills seek to change the state’s insurance rating law and prohibit the use of factors that are highly predictive of the risk of a future loss.”

The proposed laws would bar insurers from considering nondriving factors that are demonstrably predictive of claims when setting premium rates.

“Prohibiting highly accurate rating factors…disconnects price from the risk of future loss, which necessarily means high-risk drivers will pay less and lower-risk drivers will pay more than they otherwise would pay,” the release says. “Additionally, changing the rating law and factors used will not change the economics or crash statistics that are the primary drivers of the cost of insurance in the state.”

Triple-I agrees with the key concerns raised by the other trade organizations. As we have written previously, such legislation suggests a lack of understanding about risk-based pricing that is not isolated to Illinois legislators – indeed, similar proposals are submitted from time to time at state and federal levels.

What is risk-based pricing?

Simply put, risk-based pricing means offering different prices for the same level of coverage, based on risk factors specific to the insured person or property. If policies were not priced this way – if insurers had to come up with a one-size-fits-all price for auto coverage that didn’t consider vehicle type and use, where and how much the car will be driven, and so forth – lower-risk drivers would subsidize riskier ones. Risk-based pricing allows insurers to offer the lowest possible premiums to policyholders with the most favorable risk factors. Charging higher premiums to insure higher-risk policyholders enables insurers to underwrite a wider range of coverages, thus improving both availability and affordability of insurance.

This simple concept becomes complicated when actuarially sound rating factors intersect with other attributes in ways that can be perceived as unfairly discriminatory. For example, concerns have been raised about the use of credit-based insurance scores, geography, home ownership, and motor vehicle records in setting home and car insurance premium rates. Critics say this can lead to “proxy discrimination,” with people of color in urban neighborhoods sometimes charged more than their suburban neighbors for the same coverage.

The confusion is understandable, given the complex models used to assess and price risk and the socioeconomic dynamics involved. To navigate this complexity, insurers hire teams of actuaries and data scientists to quantify and differentiate among a range of risk variables while avoiding unfair discrimination.

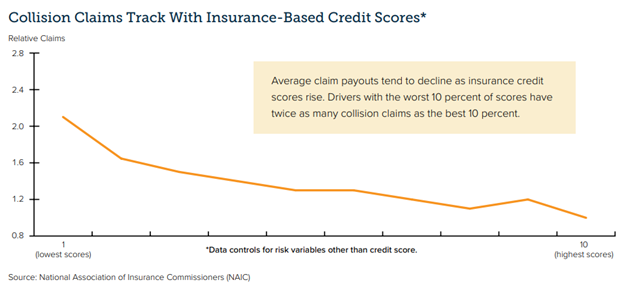

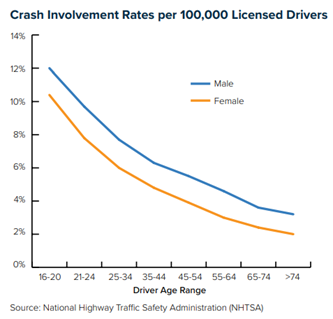

While it may be hard for policyholders to believe factors like age, gender, and credit score have anything to do with their likelihood of filing claims, the charts below demonstrate clear correlations.

Policyholders have reasonable concerns about rising premium rates. It’s important for them and their legislators to understand that the current high-rate environment has nothing to do with the application of actuarially sound rating factors and everything to do with increasing insurer losses associated with higher frequency and severity of claims. Frequency and claims trends are driven by a wide range of causes – such as riskier driving behavior and legal system abuse – that warrant the attention of policymakers. Legislators would do well to explore ways to reduce risks, contain fraud other forms of legal system abuse, and improve resilience, rather than pursuing “solutions” to restrict pricing that will only make these problem worse.