The Institutes’ Predict & Prevent® podcast has been named to PropertyCasualty360’s Insurance Luminaries Class of 2024 in the category of Risk Management Innovation. This annual recognition celebrates people and initiatives driving meaningful progress within the insurance sector, highlighting key advancements and forward-thinking approaches.

The podcast explores new ways to respond to some of the biggest risk challenges facing society today by working to better predict and prevent losses before they occur. This proactive approach is crucial in a rapidly changing world in which traditional risk-management methods – which focus on risk financing and responding after a loss – are becoming less sufficient.

By exploring new technologies and resilience strategies, the podcast addresses the urgency of mitigating current risk landscapes and paves the way for future advancements in risk prevention.

The Institutes is a nonprofit organization made up of diverse affiliates – including Triple-I – that educate, elevate, and connect people in the essential disciplines of risk management and insurance.

As the podcast rounds out its second year, its focus remains to empower the risk-management and insurance community with actionable insights and forward-thinking strategies. Those interested in exploring innovative technology and resilience solutions can listen to podcast episodes, access articles, and subscribe to the Predict & Prevent newsletter here.

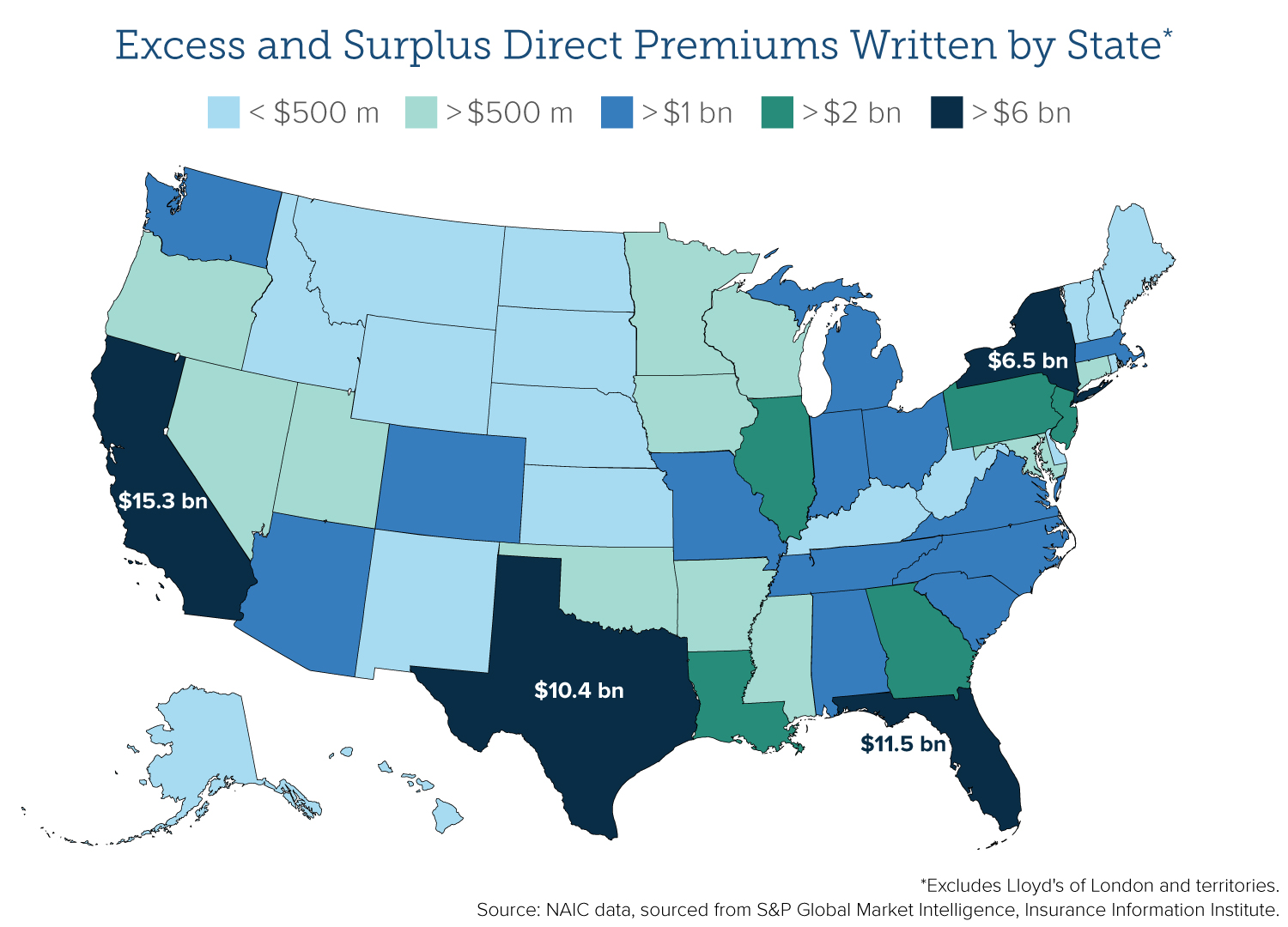

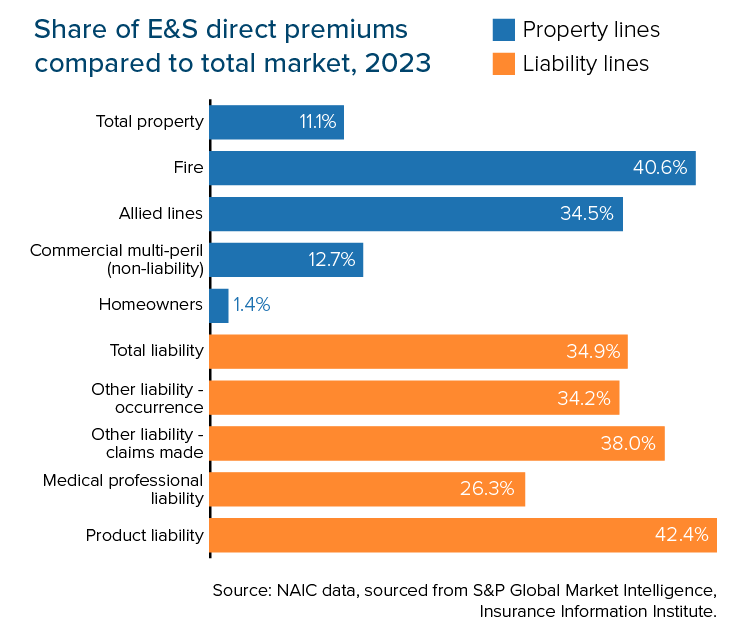

The Excess and Surplus (E&S) market has grown for five consecutive years by double-digit percentage rates. While expansion appears to have slowed, ample growth likely to continue if major trends persist, according to Triple-I’s latest issue brief, Excess and Surplus: State of the Risk.

As reported byS&P Global Intelligence, total premiums for 2023 reached $86.47 billion, up from $75.51 billion in 2022. The growth rate for direct premiums in 2023 climbed to 14.5 percent, down from the peak year-over-year (YoY) increase of 32.3 percent in 2021 and 20.1 percent in 2022. The share of U.S. total direct premiums written (DPW) for P/C in 2023 grew to 9.2 percent, up from 5.2 percent in 2013.

The brief summarizes how these outcomes are driven by the niche segment’s capacity to take advantage of coverage gaps in the admitted market and quickly pivot to new product development in the face of emerging or novel risks. Analysis and takeaways, based on data from US-based carriers, highlight dynamics that may support continued market expansion:

The rising frequency of climate disasters and catastrophes that overwhelm the admitted market

The increasing number and amount of outsized verdicts (awards over $10 million)

The sustainability of amenable regulatory frameworks

Outlook for the reinsurance segment

These factors can also converge to enhance or aggravate conditions.

For example, some states, such as Florida and California, are dealing with significant obstacles to P/C affordability and availability in the admitted market posed by catastrophe and climate risk while also experiencing large respective shares of outsized verdict activity. Also, 13 of the 15 largest U.S. E&S underwriters for commercial auto liability experienced a YoY increase in 2023 direct premiums written. In contrast, eight of the largest 15 underwriters of commercial auto physical damage coverage experienced a decline. Given 2023 research from the Insurance Information Institute showing how inflationary factors from legal costs amplify claim payouts for commercial auto liability, it appears that E&S is flourishing off the struggles of the admitted market.

At the state level, the top three states based on E&S property premiums as portion of the total property market were Louisiana (22.7 percent), Florida (21.1 percent), and South Carolina (19.4 percent) in 2023. The states experiencing the highest growth rates in E&S share of property premiums were South Carolina (9.0 percent), California (8.8 percent), and Louisiana (8.3 percent).

Since the publication of Triple-I’s brief, AM Best released its2024 Market Segment Report on U.S. Surplus Lines. One of the key updates: after factoring in numbers from regulated alien insurers and Lloyd’s syndicates, the E&S market exceeded the $100 billion premium ceiling for the first time, climbing past $115 billion. The share size in the P/C market has more than tripled, from 3.6 percent total P/C DPW in 2000 to 11.9 percent in 2023. Findings also indicate that DPW is concentrated heavily within the top 25 E&S carriers (ranked by DPW), with about 68% of the total E&S market DPW coming from this group.

The E&S market typically provides coverage across three areas:

Nonstandard risks: potential liabilities that have unconventional underwriting characteristics

Unique risks: admitted carriers don’t offer a filed policy form or rate, or there is limited loss history information available

Capacity risks: the customer to be insured seeks a higher level of coverage than most insurers are willing to provide

Thus, E&S carriers offer coverage for hard-to-place risks, stepping in where admitted carriers are unwilling or unable to tread. It makes sense that the policies typically come with higher premiums, which can boost DPW.

However, the value proposition for E&S policyholders hinges on the lack of coverage in the admitted market and the insurer’s financial stability – especially since state guaranty funds don’t cover E&S policies. Therefore, minimum capitalization requirements tend to higher for E&S than for admitted carriers. Ratings from A&M Best over the past several years indicate that most surplus insurers stand secure. Robust underwriting and strong reinsurance capital positions will play a role in the market’s capacity for continued expansion.

To learn more, read our issue brief and follow our blog for the latest insights.

Targeting of the demographic with the most to lose increases.

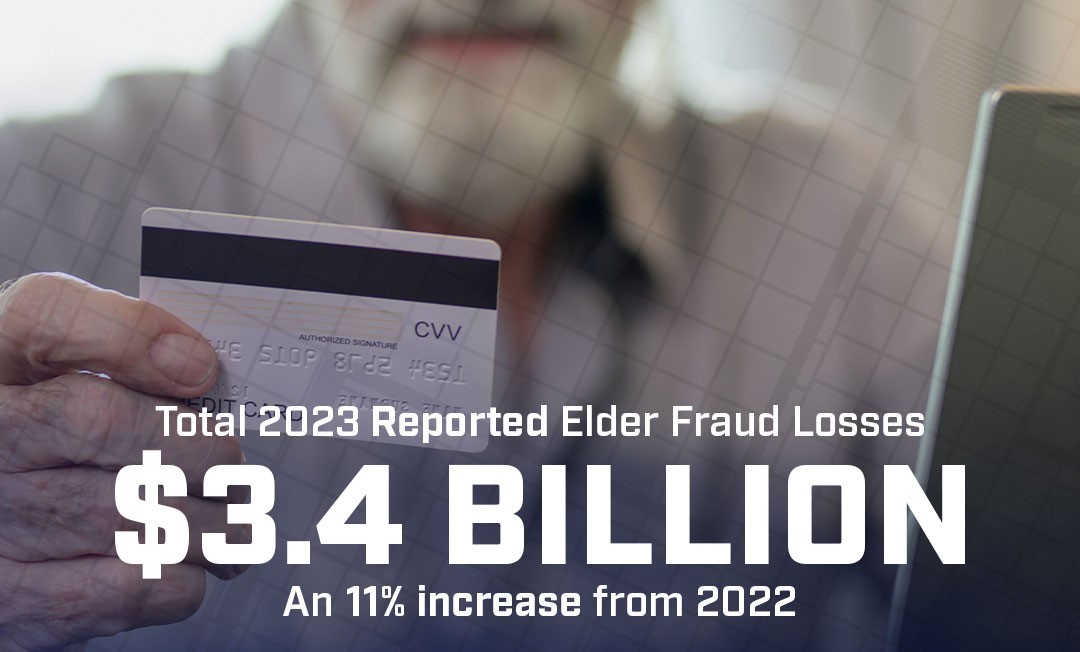

In 2023, total losses reported to the FBI’s Internet Crime Complaint Center (IC3) by people over the age of 60 topped $3.4 billion, an almost 11 percent increase in reported losses from 2022. The number of complaints, the highest attributed to a single age group, increased by 14 percent. The average dollar loss per complaint was $33,915, with nearly 6,000 people losing over $100,000 per claim.

The IC3 report outlined several common cyber fraud activities that impact individuals over 60, including:

Call Center/Tech Support Scam

Confidence/Romance Scams

Cryptocurrency Scams

Investment Scams

The IC3 notes the actual figures around these and other cyber crimes targeting the elderly may be higher since only about half of the more than 880,000 total complaints it received (with total losses exceeding $12.5 billion) included age data.

A major reason for the proliferation of elder fraud may simply be that members of this age group are plentiful while also having comparatively the most to steal. Adults 65 and up are expected to make up 22 percent of the US population by 2024. Federal Reserve data indicates that their asset accumulation outpaces that of other age groups, with median and average net worth figures for adults 65-74 at $409,900 and $1.8 million, respectively, and for adults 75 and over, $335,600 and $1.6 million respectively.

Increasing digital lives and advancing technology create new threats.

The transition to the smart mobile and app economy, along with the rise of big data and predictive analytics/AI, and (due to the pandemic) remote working, have transformed the way we engage with the world on a social, professional, and financial level. The Internet of Things (IoT) and each person’s expanding network of personal devices — smart TVs, video game consoles, appliances, home climate control systems, etc. — have propelled the digitization of our existence. All these advancements can make life easier but also increase points of cybersecurity vulnerability for people of all ages.

However, data indicates that different age groups can be susceptible to different methods of targeting by cyber scammers. For example, phishing, which relies on the human tendency to repay what another person has provided, can be more effective for targeting older vs younger adults. Also, today’s consumer under age 25 may never have the need to write a paper check, but many over 65 today have spent a significant portion of their lives handling their financial affairs that way. Thus, the trust placed in tech support people and other personnel whom they are supposed to rely on for assistance is understandable.

Unfortunately, according to the IC3, people over 60 lost more to call center and tech support scams than all other age groups combined, with this group reporting 40% of these incidents and 58% of the related financial losses (about $770 million). Common schemes involved using phone calls, texts, emails, or pop-up windows (or a combination of these) to connect with victims, manipulating them to download malicious software, reveal private account information, or transfer assets. The fallout included remortgaged homes, emptied retirement accounts, and, in some cases, suicide.

New tools and methods increase cyber security threats.

A financial services professional at a Hong Kong-based firm sent US$25 million to fraudsters after she believed she was instructed to do so by her chief financial officer on a video call that also included other colleagues. Deepfakes, one of 2024’s increasingly common cyber risks for businesses and organizations, is on track to become a major threat to personal cyber liability. A technology known as “deep” learning (hence the name) can generate images, videos, texts, or sound files specifically designed to be highly convincing despite being entirely made up.

This content can turn up anywhere on social media, the internet, or even in emails and phone calls, fooling unsuspecting humans, and, all too often, even detection software. Deepfakes aren’t always produced for malicious activities; some are used widely for entertainment. However, the growing sophistication of deepfakes and the availability of the technology needed to make it may have serious implications for cyber risk.

Cyber criminals can leverage this technology to trick victims into divulging sensitive information, transferring money, or performing other activities. Reputations can be damaged by fabricated images of victims engaged in illegal or controversial acts. This type of deep fake can also enable blackmail in exchange for not releasing the material. In addition to impersonating individuals, cyber criminals can use deep fakes to bypass biometric verification or create false advertising.

The options for managing personal cyber risk can differ in crucial ways.

Personally identifiable information (PII) is the primary driver of identity theft and most other cyber fraud. Major data breaches are becoming common place, such as the incident that happened in 2023 (but wasn’t reported until August 2024) that credit exposed 2.7 billion records. Bad actors exploit this kind of information to directly engage in fraudulent transactions or create trust with their targets in more complex schemes.

Thanks to heavy marketing and wide availability from banks and card issuers, consumers tend to be familiar with Identity Theft Protection (ITP). As the name implies, such plans revolve around the risk of stolen identity and can alleviate some of the work and costs related to monitoring and mitigating the fallout from identity theft.

In contrast, Personal Cyber Insurance (PCI) offers coverage for a broader range of losses. Covered risks, in addition to ITP, can include cyber extortion, online fraud and deceptive transfers, data breaches, cyberbullying, and more. An important aspect of PCI is that it can help provide financial reimbursment from covered “cyber scams” or related social engineering risk not directly tied to identity theft, cyber crimes which are on the rise. It also offers assistance and financial reimbursment for compromised devices. For example, if a policyholder is hacked, personal cyber insurance may help cover the costs of hiring a professional to reformat the hard drive, reinstall the operating system, and restore data from the backup.

“Social engineering and other cyber-related threats against consumers continue to grow and evolve, and insurance carriers are offering affordable personal cyber coverage that can be easily added to a homeowners or renters insurance policy,” says James Hajjar, Chief Product Officer at Hartford Steam Boiler (HSB).

HSB, which has been offering personal cyber insurance since 2015, has evolved its coverage multiple times over the years to stay ahead of cyber risk trends and the dynamic threat landscape. Given the increasing complexity of cyber risks and the rise of sophisticated scams — such as phishing and ransomware — that kind of protection shouldn’t be limited to identity theft. Robust PCI coverage safeguards against a range of other cyber-related issues and provides critical support to ensure policyholders aren’t left to deal with the financial aftermath of a cyber incident alone.

“It’s crucial that cyber insurance is specifically designed to help individuals protect themselves against these evolving threats and provides financial security and additional programs and services if someone is hacked,” Hajjar says.

Historically, ITP has been widely offered through banks, credit unions, credit card issuers, and credit reporting agencies. Either product type may be purchased as either standalone or optional add-on coverage for homeowners, rental, or condo insurance policies.

The IC3 says it receives about 2,412 complaints daily, but many more cybercrimes likely go unreported for various reasons. Complaints tracked over the past five years have impacted at least 8 million people. The 2023 Data Breach Report, which details the larger dataset of cyber crime complaints to the FBI’s Identity Theft Resource Center (ITRC), reveals that last year delivered a bumper crop of cybersecurity failures – 3,205 publicly reported data compromises, impacting an estimated 353,027,892 individuals.

A new conversation about personal cyber insurance begins.

Triple-I and HSB are teaming up to uncover ways to enhance support and resources for insurance agents while improving personal cyber insurance options for policyholders. If you are an agent, please take three minutes to help by participating in our survey. Your contribution will be invaluable in shaping the future of personal cyber insurance.

By Loretta Worters, Vice President, Media Relations, Triple-I

One in five U.S. children is unsure where they will get their next meal, according to the U.S. Department of Agriculture. In 2022, 33 percent of single-parent families experienced food insecurity, and the problem is especially acute for families of color and households headed by single mothers.

The Insurance Industry Charitable Foundation is observing Hunger Action Month – a nationwide effort held every September– by raising funds in its ongoing fight against childhood hunger throughout its 30th anniversary year in 2024.

On average, IICF provides up to five meals for every dollar contributed, working with 11 nonprofit partners that serve communities across the United States and United Kingdom. Donors to the IICF 30th Anniversary Celebration are recognized on its website as IICF Children’s Champions for contributions of $1,000 or greater and all donors contributing $30 or more.

Donors giving $30 or more can enroll for a complimentary year of IICF Global Membership, which provides exclusive volunteer opportunities and a network of philanthropically minded insurance professionals, noted IICF CEO Bill Ross.

“We convened an IICF 30th Anniversary Committee of 35 industry leaders in the new year to help lead and advance our 30th campaign to raise funds for hungry children,” Ross said. “Seven insurance companies are leading internal company campaigns in support of IICF’s 30th, raising and matching funds for hungry children: CNA, Burns & Wilcox, Falvey Insurance Group, Lockton, Markel, RT Specialty and The Hartford. We hope more companies and individuals will participate.”

The IICF has approximately 400 individual donors to date. For every 100 new donors, at only $30 each, that’s thousands of meals they can deliver to children in need.

“As we look back at 30 years of the IICF, it is encouraging to know we have grown from an effort primarily serving California, with approximately 20 board members, to now expanding as a national and growing international industry foundation with more than 800 insurance professionals, providing personal leadership and volunteer support, serving on IICF’s international and local boards and committees,” said Ross.

“Throughout our 30 years, IICF has maintained a focus on children at risk, education and food insecurity. Each of our divisions encompasses these focus areas, as well as additional areas of need specific to each region, including military veterans, the environment, and social mobility,” he said.

“It is always important to recognize where we started as a foundation, and our vision remains the same today. The IICF is here to represent the insurance industry in a united philanthropic effort by providing grants in local communities, industrywide volunteer service and ongoing opportunities for leadership in our communities and our industry.”

More Work Needs to be Done

Since 2020, IICF has raised $1.8 million and delivered three million meals through its Children’s Relief Fund, which was launched in response to the global pandemic. But more needs to be done. For those that wish to donate, the IICF is grateful to these acts of kindness.

Ross summed it up best: “When we unite to help others, great things happen for everyone – communities, our neighbors in need and our industry!”

Michigan personal auto insurance affordability improved markedly after enacting substantial auto insurance reform in 2019, according to a new report by the Insurance Research Council (IRC) – like the Triple-I, a division of The Institutes

The study, Personal Auto Insurance Affordability in Michigan, found that personal auto insurance expenditures accounted for 1.9 percent of the median household income in Michigan in 2022 (the last year the data is available), a decline of half-a-percent from the pre-reform peak. Michigan’s expenditure share remains higher than the percentage in the overall U.S. and forty-four other states.

Other key findings from the report include:

Before the reforms, Michigan drivers were required to purchase unlimited personal injury protection (PIP) coverage; in comparison, the second highest mandated amount of PIP coverage was $50,000 in New York. The unlimited medical benefits and other features, such as attendant care benefits and no medical fee schedule, led to Michigan’s extremely high average auto injury claim severity, which has been the primary cost driver in the state.

In 2022, Michigan households spent $1,319 to insure each vehicle, nearly 20 percent above the national average. However, in the years since reform, expenditures have fallen in Michigan while increasing in almost every other state. From 2019 to 2022, the average expenditure for auto insurance in Michigan fell 12 percent compared with an increase of five percent in the U.S. overall.

Uninsured and underinsured motorists are both a symptom and cause of affordability issues. In 2019, Michigan had the highest rate of uninsured drivers in the country, with more than one in four motorists lacking the required liability coverage. The uninsured motorist rate in Michigan dropped by 5 percent between 2020 and 2022.

“Efforts to improve auto insurance affordability in Michigan must begin with the underlying cost drivers: injury claim severity and litigation,” said Dale Porfilio, FCAS, MAAA, president of the IRC. “The average amount paid per auto claim for auto injury insurance is dramatically higher in Michigan, more than double the U.S. average and one and a half times the second highest state.”

Porfilio, who is also Chief Insurance Officer of the Insurance Information Institute (Triple-I), noted that the 2022 affordability data does not fully reflect many recent countrywide challenges to affordability, such as economic inflation, higher replacement costs, legal system abuse, and deteriorating driving behavior. “However, the movement of several key indicators illustrate the positive effect of the Michigan policymakers’ efforts to improve affordability in their state.”

Reinsurers experienced near-record returns in 2023, and continued to post strong results in the first quarter of 2024, with up to a 12% improvement in combined loss ratios, according to Gallagher Re’s 1st View report.

The report attributes these positive outcomes to several factors, including relatively benign natural catastrophe activity, adjustments in the reinsurance market, improved conditions in primary markets, and higher reinvestment rates. Improved results have created a more favorable market for reinsurance buyers, with sufficient capital available to meet increased demand, Gallagher Re observed.

“This more comfortable market for buyers has been underpinned by an increasing supply of capital to meet increased demand as reinsurers balance sheets have expanded on the back of strong 2023 and Q1 2024 results,” commented Gallagher Re CEO Tom Wakefield.

Non-life insurance-linked securities (ILS) capital reached a record level of $107 billion at the end of 2023 and continued to grow in the first half of 2024, driven by successful catastrophe bonds and increased investor interest.

However, ILS capacity became less abundant by midyear, as the Atlantic hurricane season approached, Gallagher Re noted.

“ILS capacity became scarce as ILS investors were ‘unnerved’ by forecasts of an active hurricane season,” the report stated.

Property outlook

The property reinsurance market has experienced increased competitiveness and capacity due to reinsurers’ strong performance in recent years, the report noted.

While reinsurers were not significantly impacted by natural catastrophe losses in Q1, there were an estimated $43 billion of economic losses and $20 billion insured losses in Q1 with both numbers being near the 10-year average.

The first quarter is not traditionally a major driver of the annual natural catastrophe loss burden, historically only representing 14% of the full-year total. Losses in Q1 have been dominated by severe convective storm losses (34% of insured losses) and other secondary perils of wildfire, drought and flood making up another 29%.

At July 1 renewals, risk-adjusted catastrophe pricing for Florida property was down 0% to 10% on average, and additional capacity demands of $3 billion to $5 billion in Florida were all met.

“Following three consecutive years of double-digit risk-adjusted rate increases, reinsurers were looking to hold the line from a procing perspective,” the reinsurance intermediary said of the Florida property catastrophe market.

The report also highlighted that buyers of property catastrophe insurance have been able to negotiate better terms and conditions on their reinsurance contracts due to the “risk on” approach taken by reinsurers. Risk-adjusted catastrophe placements in the U.S. generally were down 0% to 12% at July 1, Gallagher Re reported.

Non-catastrophe property pricing in the U.S. was down 0 to 10% for loss free accounts, but up 5% to 15% with losses.

Casualty outlook

“Casualty underwriters appear less confident than property underwriters outlined above, although this warrants its own caveat. The issues driving stakeholder concerns are regionally nuanced as the frequency and severity of casualty losses are driven by local societal, economic, judicial, legislative, and behavioral factors,” the report stated.

In the casualty insurance sector, concerns over rate adequacy in the U.S. have increased, following adverse development reported by liability insurers in the fourth quarter of 2023 and the first quarter of 2024. The lengthening and deteriorating tail of liability claims have exacerbated reinsurers’ concerns, as the market is already dealing with economic and non-economic loss inflation.

At July 1 renewals, risk adjusted excess of loss rates for U.S. general liability business were up 5% to 10% with no losses, and up 5% to 15% with emerging losses.

For U.S. health care liability, increased loss severity was seen across the health care sector. Excess of loss rates were up 0 to 5% for limited-exposed layers, and up 3% to 8% for catastrophe layers, without emerging losses. Rate increases were greater — up 5% to 20% — for layers with emerging losses.

Professional liability lines with no emerging losses saw excess of loss rates decline 0% to 5%, while accounts with losses experienced 0% to 10% increases.

Workers compensation has seen continued pressure for increases, even on loss-free layers, Gallagher Re noted. Excess of loss rates with no loss emergence were up 0 to 5% and with loss emergence, increased 5% to 10% at July 1.

The full report can be downloaded on the Gallagher Re website.

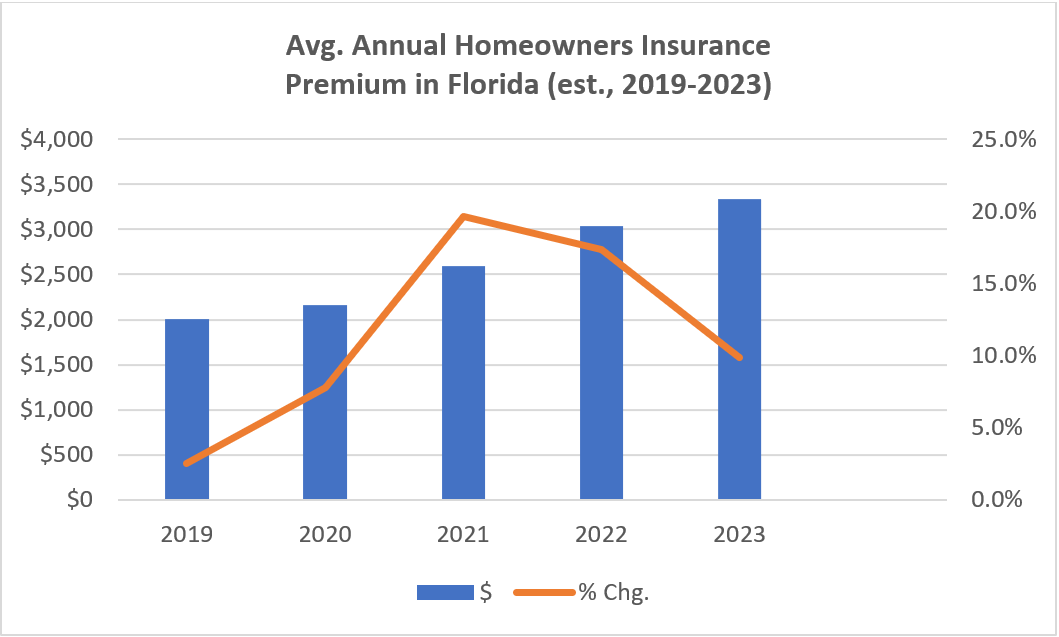

Homeowners insurance premium growth in Florida has slowed since the state implemented legal system abuse reforms in 2022, according to a Triple-I analysis.

As shown in the chart below, average annual premiums climbed sharply after 2020. This was due in part to inflation spurred by the COVID-19 pandemic and the war in Ukraine as well as longtime challenges in the state with claim fraud and legal system abuse.

Source: Triple-I analysis of NAIC and OIR data

According to the state’s Office of Insurance Regulation (OIR), Florida accounted for nearly 71% of the nation’s homeowners claim-related litigation, despite representing only 15% of homeowners claims in 2022, the year Category 4 Hurricane Ian struck the state. In that same year, and prior to Ian making landfall in the state as a first major hurricane since 2018’s Hurricane Michael, six insurers declared insolvency. Hurricane Ian became the second largest on record by insured losses, in large part because of the extraordinary litigation costs estimated to result in Florida in the aftermath.

The Florida Legislature responded to the growing crisis by passing several pieces of insurance reform, primarily tackling problems with assignment of benefits (AOB), bad-faith claims, and excessive fees. For example, the new laws eliminated one-way attorney fees in property insurance litigation, forbid using appraisal awards to file a bad-faith lawsuit, and prohibited third parties from taking AOBs for any property claims. The legislation also ensures transparency and efficiency in the claims process and encourages more efficient, less costly alternatives to litigation.

A surge in litigation

Litigation spiked when backlogged courts reopened following the pandemic, then again when the reforms were passed in 2022 and 2023, as plaintiffs’ attorneys raced to file suits ahead of implementation of the legislation.

This increase in litigation, combined with persistently strong inflation, contributed to increased loss costs and premium increases. In 2022, average homeowners premium rates rose more than 17 percent, to $3,040. Premiums continued to rise in 2023, although at a decreasing rate, as inflation has moderated and legal reforms have kicked in.

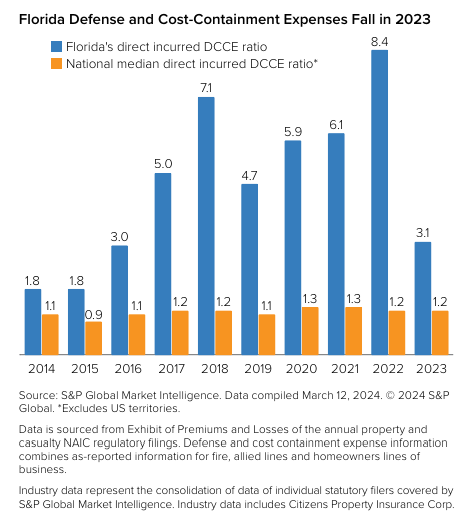

There are early signs that the reforms are beginning to bear fruit. In 2023, Florida’s defense and cost-containment expense (DCCE) ratio – a key measure of the impact of litigation – fell to 3.1, from 8.4 in 2022, according to S&P Global. In dollar terms, 2023 saw $739 million in direct incurred legal defense expenses – a major decline from 2022’s $1.6 billion. For perspective, incurred defense costs in the two largest U.S. insurance markets in 2023 were $401.6 million in California, followed by $284.7 million in Texas. As the chart below shows, Florida’s DCCE ratio – even during its best years – regularly exceeds the nation’s.

As insurers have failed or left the state, Citizens Property Insurance Corp. – the state-run insurer of last resort and currently Florida’s largest residential insurance writer – has swelled with new business and lawsuits. Citizens’ depopulation efforts to move policyholders to private insurers contributed to policy counts falling to 1.23 million by the end of 2023.

It’s important to remember that all premium estimates are based on the best information available at the time and actual results may differ due to changes in market conditions. For example, earlier Triple-I projections that average annual homeowners premiums in Florida would exceed $4,300 in 2022 and $6,000 in 2023 assumed significant rate increases would be needed to restore profitability to the state’s homeowners market. These projections did not assume legislative reform or that Citizens would become the state’s largest homeowners insurance company, with many risks priced below the admitted and excess and surplus markets. Our projections also assumed inflation would continue to grow at rates similar to those prevailing at the time.

In light of the reforms and moderating inflation, we are now reporting lower average annual premiums of $3,040 (2022) and $3,340 (2023). The Florida OIR has reported average premium rate filings are running below 2.0 percent in 2024 year-to-date in the private market. Further, OIR indicated eight domestic carriers have filed for rate decreases and 10 have filed for no increase this year. Additionally, eight property insurers have been approved to enter the Florida market, with more expected this year.

Triple-I will continue to monitor and report on the evolving property insurance market in Florida.

Triple-I has published a great deal regarding the potential impact of TPLF on costs for insurers and policyholders. Bellino’s gaze focused on potential risks for the judiciary:

Increased judicial workload

More fraudulent claims

Longer litigation and slower settlements

Creation of potential appellate issues

And, like many insurance industry stakeholders, Lisa M. Bellino (VP Claims Judicial & Legislative Affairs for Zurich North America in Philadelphia) is fundamentally concerned about the lack of transparency surrounding TPLF’s involvement in a lawsuit.

TPLF is a growing and costly aspect of legal system abuse, a problem that Triple-I and other industry thought leaders define as policyholder or plaintiff attorney actions that unnecessarily increase the costs and time to settle insurance claims. Qualifying actions can arise, for example, when clients or attorneys draw out litigation in hopes of a larger settlement simply because TPLF investors take such a giant piece of the payout. As there is little transparency around the use of TPLF, insurers and the courts have virtually no leeway in mitigating any of this risk.

TPLF can lead to undue judicial burden and waste.

When judges are unaware of the funding arrangement, they would likely also be in the dark about potential conflicts of interest or improper claims and, therefore, be unable to mitigate these risks. However, Bellino argues that the de facto practice of secrecy can cause judicial waste even in the limited number of jurisdictions and courts that require disclosure. Judges may feel compelled to spend a significant amount of time ascertaining attorney compliance. As funding often involves parties not directly related to the case, the judiciary may need to hold additional hearings and reviews to uncover the real parties in interest. Bellino cites a case in which the real parties were not the named plaintiffs.

TPLF can be a driving factor behind lawsuit generation.

When law firms pursue class action litigation, they may engage “lead generators,” companies that help find plaintiffs for a specific tort. Advertising tactics can include traditional and social media. When prospective claimants respond to these ads, they are directed to a law firm or a call center that distributes the recruited claimants to law firms. This service comes at a steep price – in dollars and justice. As funding may often come from TPLF, Bellino describes how the profit model behind lead generation companies working with law firms can increase the risk of fraudulent claims.

The risk of bogus claims and claimants can surge with TPLF.

Funders of class action litigation have a financial incentive to drive up the number of plaintiffs. As neither the defense nor the judge is typically aware of the third party’s potential conflict of interests, judicial resources can be wasted, and justice can be delayed for legitimate claimants. Bellino cites, among other examples, a New York case to illustrate how litigation funders and attorneys may even collaborate in multi-million dollar fraud schemes.

TPLF funders may encourage drawn-out litigation and hinder settlements

Bellino cites a case highlighting how funders might control litigation and delay resolutions to maximize their returns. A publicly traded TPLF giant allegedly blocked a settlement agreement between a plaintiff and the defendants, resulting in prolonged litigation across multiple jurisdictions. The interference may have led to additional motions, hearings, and opinions, diverting judicial resources from resolving the dispute between the named parties. As a result, costs for the plaintiff, defendant, and the courts likely would’ve soared.

Undisclosed TPLF involvement can spark appellate concerns.

Undisclosed funding agreements can also prevent parties from adequately preparing their cases and preserving appellate issues. For example, a TPLF investor may fund medical testing that leads to recruiting plaintiffs for a class action against a drug manufacturer. If this fact wasn’t disclosed to the defendants or court, at the very least, the defendant wouldn’t have access to information needed for defense or subsequent appeals. Also, the judiciary wouldn’t be able to perform its duty to monitor red flags for potential bias or fraud. It is also possible that the interests of the plaintiff will be affected by other appellate concerns, too.

Increases in litigation and claim costs have threatened the affordability and availability of many areas of insurance coverage. TPLF involvement, like other channels for potential legal system abuse, is nearly impossible to forecast and mitigate. And despite its original intended purpose–to help plaintiffs seek justice– it can extract a disproportionate amount of value from settlements, weakening the primary purpose of a financial payout.

Overall, the shroud of secrecy around TPLF can undermine the legal system, posing threats to unbiased and fair legal outcomes. Bellino strongly advocates for mandatory disclosure of TPLF agreements at the beginning of litigation. A system-wide requirement for early transparency would allow courts and involved parties to address potential conflicts, biases, and fraud early in the process. In her words, “Disclosure may restore reality and close the door on the TPLF Twilight Zone.”

Hosted by Triple-I Chief Economist and Data Scientist Dr. Michel Léonard, PhD, CBE, the series equips listeners with insights to manage economic uncertainty at the intersection of economics and insurance. It features interviews with insurance practitioners, technologists, academics, educators, analysts, and economists from various industries who discuss their perspectives and how they integrate economic trends and developments into their day-to-day responsibilities.

Early episodes include discussions with:

Jennifer Kyung, Chief Underwriting Officer at USAA,

Ken Simonson, Chief Economist of the Associated General Contractors of America,

Dale Porfilio, Triple-I Chief Insurance Officer,

Sean Kevelighan, Triple-I CEO, and

Pete Miller, President and CEO at The Institutes.

Dr. Léonard brings more than 20 years’ expertise in senior and leadership positions as Chief Economist for Trade Credit and Political Risk at Aon; Chief Economist at JLT; Chief Economist and Data Scientist at Alliant; and Chief Data Scientist at MaKro. He also is adjunct faculty in New York University’s Economics Department.

An annual report on securities class actions from Cornerstone Research indicates the median settlement amount increased 11%, and the proportion of settlements of at least $100 million climbed to nearly two-thirds of the total settlement dollars in 2023.

Research from Westfleet Advisors focused on third-party litigation funding (TPLF) for US commercial litigation suggests the David versus Goliath narrative surrounding the early years of the market is growing tenuous. The overall percentage of commitments allocated to Big Law continues to increase, from 28% in 2022 to 35% in 2023.

These and other persistent upward trends in litigation, settlement, and other legal costs continue to have implications for insurers, the policyholders they serve, and, ultimately, consumer prices.

Mega settlements and institutional investors as lead plaintiffs are increasing.

Cornerstone reports that despite a more than 20% decline in the number of settlements, total settlement dollars remained approximately the same, standing at little over half of the 2016 peak.

There were 83 securities class action settlements in 2023, with an approximate total value of $3.9 billion, versus 105 settlements in 2022, totaling $4.0 billion. Other highlights in the 2023 data:

The median settlement amount of $15 million is the highest since 2010.

The nine “mega” settlements in 2023–the highest annual frequency since 2016–ranged from $102.5 million to $1 billion.

All of the mega settlements included an institutional investor as the lead plaintiff.

Only 6% of cases settled for less than $2 million, the lowest percentage since 2013.

Analysis indicates that settlements were also higher in cases involving certain factors: “accounting allegations, a corresponding SEC action, criminal charges, an accompanying derivative action, an institutional investor lead plaintiff, or securities.” Further, an increasing number of cases that settle at later stages involved an institutional lead plaintiff, continuing the trend from 2022.

Results also suggest that drawing out cases can amplify other factors, such as total assets and median “simplified tiered damages,” a Cornerstone term that refers to the model used to estimate settlement amounts. For both of these categories in 2023, median amounts for cases after class certification rulings were twice that of cases that settled before these rulings were made. However, in the five-year period from 2019 through 2023, over 90% of cases were settled before filing a motion for summary judgment.

Accompanying derivative actions are down.

Whereas a securities class action is filed on behalf of shareholders, a shareholder derivative action is typically brought by a shareholder on behalf of and (arguably) for the benefit of the company (usually against the company’s directors and/or officers). Derivative actions typically only happen in parallel with class action lawsuits, and the majority don’t result in monetary settlements (except for attorney fees). Instead, the plaintiff wins tend to center around measures for reforming corporate governance or operational controls.

Otherresearch from Cornerstone shows the probability of a monetary settlement for these lawsuits increases when the associated class action settlement is rather large. Also, historically, securities actions with accompanying derivative litigation tend to settle for higher amounts than those that don’t carry parallel derivative claims. Thus, Cornerstone also tracks the percentage of cases involving accompanying derivative actions. In 2023, the portion was 40%, the lowest since 2011.

New capital commitments decreased for commercial litigation TPLF, but claim monetization increased.

With a reported 39 active funders, 353 new deals, and $15.2 billion AUM, commercial litigation (versus consumer litigation) receives the majority of third-party litigation funding (TPLF). Investors target intellectual property, arbitration, business torts, contract breaches, and, of course, class action suits. These TPLF deals, also referred to as transactions or commitments, are arranged between funders and corporate litigants or law firms. Westfleet Advisors’ most recent market report on TPLF is the fifth edition, and it covers transactions from July 1, 2022, to June 30, 2023. Some noted exceptions and data adjustments are described in the report.

The report reveals that despite some funders leaving the market and a 14% decrease in new capital commitments, key data points remained close to amounts tracked for last year. For example, attorneys still make the majority of these deals with a 64% share of the agreements, in contrast to only 36% for clients. Patent litigation is still reaping the largest amount of funds for a single legal area, about 19% of new commitments. Figures for type of deal and average deal size also remain fairly stable.

However, some annual numbers have increased, highlighting an ongoing strategic shift in TPLF use. For the third year in a row, the report noted a rise in capital allocated for the monetization of claims, with 21% (versus 14% in 2022) going to new commitments. The biggest law firms (ranked in the AmLaw 200 according to gross revenue) have increased their use of TPLF, snagging 35% of the new deals. Arguably, both trends weaken the “David vs Goliath” narrative, and commercial TPLF may evolve to be less about helping scrappy firms and plaintiffs and more about extracting profits from litigation.

Drawn out litigation and more outsized settlements may have implications for insurance coverage.

Triple-I and other industry thought leaders define Legal System Abuse as policyholder or plaintiff attorney actions that unnecessarily increase the costs and time to settle insurance claims. Qualifying actions can arise from attorneys or clients drawing out litigation to reap a larger settlement simply because TPLF investors take such a giant piece of the settlement pie. As there is little transparency around the use of TPLF, insurers and courts have virtually no leeway in mitigating any of this risk.

Thus, as with other channels for potential legal system abuse, TPLF use is nearly impossible to forecast and mitigate. Increases in litigation and claim costs have threatened the affordability and availability of many other areas of insurance coverage. TPLF can impact product lines such as Directors and Officers (D&O) in commercial litigation via securities class actions. TPLF can produce a financially counterproductive effect for plaintiffs byextracting a disproportionate amount of value from settlements, weakening the primary purpose of a financial payout: to enable the claimant to restore losses.

Nonetheless, insurers seek to carefully manage these risks through underwriting practices, policy exclusions, and setting appropriate reserves to mitigate the financial impact. Meanwhile, Triple-I and various other stakeholders have called for a regulatory rein-in on TPLF to increase transparency. To keep abreast of the conversation, follow our blog and check out our regularly updated knowledge hub for Legal System Abuse.