The devastation wrought by Hurricane Helene in September 2024 across a 500-mile swath of the U.S. Southeast highlighted the growing vulnerability of inland areas to flooding from both tropical storms and severe convective storms, according to the latest Triple-I “State of the Risk” Issues Brief.

These events also highlight the scale of the flood-protection gap in non-coastal areas. Private insurers are stepping up to help close that gap, but increased homeowner awareness and investment in flood resilience across all co-beneficiary groups will be needed as more and more people move into harm’s way.

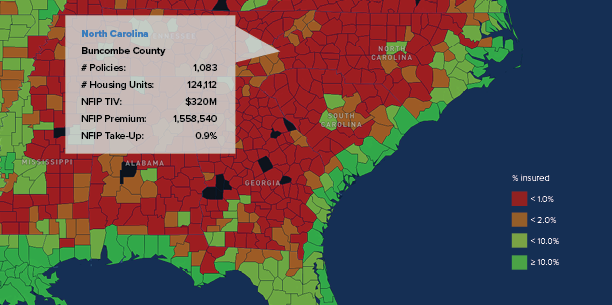

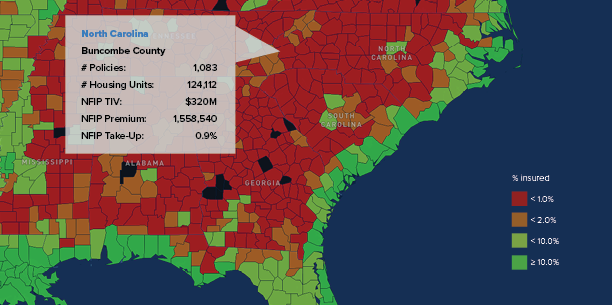

Helene dumped 40 trillion gallons of water across Florida, Georgia, the Carolinas, Virginia, and Tennessee, causing hundreds of deaths and billions in insured losses. Much of the loss was concentrated in western North Carolina, with parts of Buncombe County – home to Asheville and its historic arts district – left virtually unrecognizable. Less than 1 percent of residents in Buncombe County had federal flood insurance when Helene struck.

The experience of these states far inland echoed those of New York, New Jersey, and Pennsylvania in August 2021, when remnants of Hurricane Ida brought rains that flooded subways and basement apartments, with more than 40 people killed in those states.

“The whole swath going up the East Coast” that Hurricane Ida struck in the days after it made landfall “had less than 5 percent flood insurance coverage,” said Triple-I CEO Sean Kevelighan at the time.

Then, in July 2023, a series of intense thunderstorms resulted in heavy rainfall, deadly flash floods, and severe river flooding in eastern Kentucky and central Appalachia. Flooding led to 39 fatalities and federal disaster-area declarations for 13 eastern Kentucky counties. According to the Federal Emergency Management Agency (FEMA), only a few dozen federal flood insurance policies were in effect in the affected areas before the storm.

Low inland take-up rates largely reflect consumer misunderstandings about flood insurance. Though approximately 90 percent of all U.S. natural disasters involve flooding, many homeowners are unaware that a standard homeowners policy doesn’t cover flood damage. Similarly, many believe flood coverage is unnecessary unless their mortgage lenders require it. It also is not uncommon for homeowners to drop flood insurance coverage once their mortgage is paid off to save money.

Private insurers stepping up

More than half of all homeowners with flood insurance are covered by NFIP, which is part of FEMA and was created in 1968 – a time when few private insurers were willing to write flood coverage. In recent years, however, insurers have grown more comfortable taking on flood risk, thanks in large part to improved data and analytics capabilities.

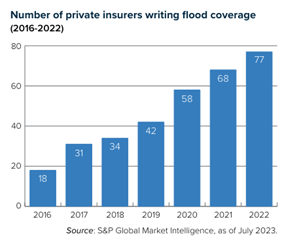

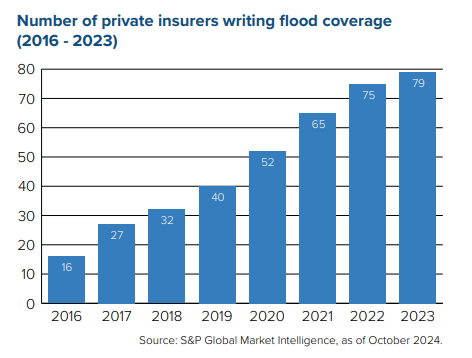

The private flood market has changed since 2016, when only 12.6 percent of coverage was written by 16 insurers. In 2019, federal regulators allowed mortgage lenders to accept private flood insurance if the policies abided by regulatory definitions. The already-growing private appetite for flood risk gained steam after that. Private insurers are gradually accounting for a bigger piece of a growing flood risk pie.

Insurance necessary – but not sufficient

Insurance can play a major role in closing the protection gap, but, with increasing numbers of people moving into harm’s way and storms behaving more unpredictably, the current state of affairs is not sustainable. Greater investment in mitigation and resilience is essential to reducing the personal and financial losses associated with flooding.

Such investment has paid off in Florida, where the communities of Babcock Ranch and Hunters Point survived Hurricanes Helene and Milton relatively unscathed. Babcock Rance made headlines for sheltering thousands of evacuees from neighboring communities and never losing power during Milton, which devastated numerous neighboring cities and left more than three million people without power.

Both of these communities were designed and built in recent years with sustainability and resilience in mind.

Incentives and public-private partnership will be critical to reducing perils and improving insurability in vulnerable locations. Recent research on the impact of removing development incentives from coastal areas can improve flood loss experience in the areas directly affected by the removal of such incentives, as well as neighboring areas where development subsidies remain in place.

Learn More:

Executive Exchange: Using Advanced Tools to Drill Into Flood Risk

Accurately Writing Flood Coverage Hinges on Diverse Data Sources

Lee County, Fla., Towns Could Lose NFIP Flood Insurance Discounts

Miami-Dade, Fla., Sees Flood-Insurance Rate Cuts, Thanks to Resilience Investment

Milwaukee District Eyes Expanding Nature-Based Flood-Mitigation Plan

Attacking the Risk Crisis: Roadmap to Investment in Flood Resilience