Flood risk is not only one of the most destructive perils facing property owners; it is among the most complicated forms of coverage for property/casualty insurers to underwrite. For decades, the private market wouldn’t cover flood risk, which is why the National Flood Insurance Program had to be established.

But improved data collection and the availability of practically unlimited computing power have changed the equation for insurers, according to Anil Vasagiri, senior vice president for property solutions at Swiss Re. In a recent Executive Exchange with Triple-I CEO Sean Kevelighan, Vasagiri discussed the developments that have helped turn flood from a nearly untouchable peril to a burgeoning area of opportunity for insurers.

Over 90 percent of natural catastrophes involve flood in some way or another. Vasagiri said the ability to use multiple data sources in understanding flood conditions of specific properties helps insurers more accurately underwrite flood and help policyholders proactively address their own exposure to the peril.

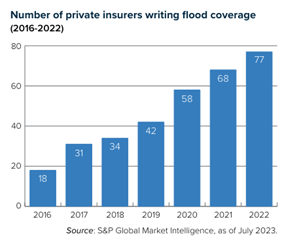

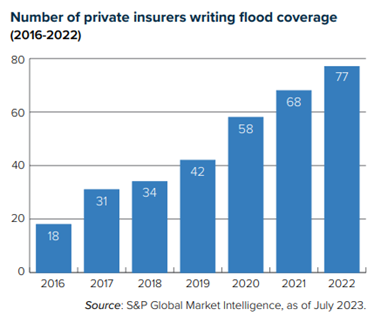

“Increased information leads to increased capacity,” Vasagiri said – a fact that bodes well for improving insurance availability and affordability and evidenced by the increased number of private insurers writing flood coverage since 2016.

The timing of the private market’s increasing appetite for flood risk is fortuitous, as it coincides with Risk Rating 2.0, NFIP’s new pricing methodology that aims to make the government agency’s flood insurance premium rates more actuarially sound and equitable by better aligning them with individual properties’ flood risk. As NFIP rates become more aligned with principles of risk-based pricing, some policyholders’ prices are expected to fall, while many are going to rise.

In the Executive Exchange, Vasagiri discussed the Swiss Re’s acquisition of Fathom – a U.K.-based company specializing in water-related risks – as part of the company’s ongoing commitment to helping close the flood protection gap.

Colorado State University hurricane researchers predict an “extremely active” Atlantic hurricane season in their initial 2024 forecast. The team cites record-warm tropical and eastern subtropical Atlantic sea surface temperatures as a primary factor for their prediction of 11 hurricanes this year.

Led by senior research scientist and Triple-I non-resident scholar Phil Klotzbach, Ph.D, the CSU Tropical Meteorology Project forecasts 23 named storms, 11 hurricanes, and five major hurricanes during the 2024 season, which starts on June 1 and continues through Nov. 30. A typical Atlantic season has 14 named storms, seven hurricanes, and three major hurricanes.

The 2023 season produced 20 named storms and seven hurricanes. Three reached “major hurricane” intensity. Major hurricanes are defined as those with wind speeds reaching Category 3, 4 or 5 on the Saffir-Simpson Hurricane Wind Scale.

“We anticipate a well above-average probability for major hurricanes making landfall along the continental United States coastline and in the Caribbean this season,” Klotzbach said. “Current El Niño conditions are likely to transition to La Niña conditions this summer/fall, leading to hurricane-favorable wind-shear conditions. Sea surface temperatures in the eastern and central Atlantic are currently at record-warm levels and are anticipated to remain well above average for the upcoming hurricane season. A warmer-than-normal tropical Atlantic provides a more conducive dynamic and thermodynamic environment for hurricane formation and intensification.”

One hurricane and two tropical storms made continental U.S. landfalls last year. Category 3 Hurricane Idalia struck Florida’s Big Bend region near Keaton Beach on Aug. 30 with wind speeds of 115 mph. It was the third hurricane, and second major hurricane, to make a Florida landfall over the past two seasons. Idalia caused storm surge inundation of 7 to 12 feet and widespread flooding in Florida and throughout the Southeast.

“The widespread damage incurred from Idalia last year highlighted the importance of being financially protected from catastrophic losses – and that includes having adequate levels of property insurance and flood coverage,” said Triple-I CEO Sean Kevelighan. “Beyond Florida, we saw significant impacts from Idalia in southern Georgia and the Carolinas. All it takes is one storm to make it an active season for you and your family, so it is time to prepare as the 2024 Atlantic hurricane season’s start nears.”

With this forecast in mind, now is ideal time for homeowners and business owners to review their policies with an insurance professional to ensure they have the right amount and types of coverage. That includes exploring whether they need flood coverage, which is not part of a standard homeowners, condo, renters or business insurance policy.

Homeowners also can make their residences more resilient to windstorms and torrential rain by installing roof tie-downs and a good drainage system. Installation of a wind-rated garage door and storm shutters also boost a home’s resilience to a hurricane’s damaging winds and may generate savings on a homeowner’s insurance premium.

Private-passenger vehicles damaged or destroyed by either wind or flooding are covered under the optional comprehensive portion of an auto insurance policy.

Property owners in Lee County, Fla., could lose their flood insurance premium discounts under the National Flood Insurance Program (NFIP) Community Rating System (CRS), according to a recent announcement by FEMA.

CRS is a voluntary program that recognizes and encourages community floodplain management practices that exceed NFIP minimum requirements. Over 1,500 communities participate nationwide.

FEMA informed leaders in the affected communities – which include Cape Coral, Bonita Springs, Estero, Fort Myers Beach, and unincorporated Lee County – that they would begin losing their discounts starting October 1. Under CRS, these communities currently receive discounts of up to 25 percent. Unincorporated Lee County and the City of Cape Coral get the biggest benefit due to their Class 5 ratings. Rates will increase by approximately $300 annually for the 115,000 homeowners impacted by FEMA’s decision.

“This retrograde is due to the large amount of unpermitted work, lack of documentation, and failure to properly monitor activity in special flood hazard areas, including substantial damage compliance,” FEMA said in a statement.

FEMA officials told the Miami Herald that the problems began shortly after Hurricane Ian in 2022, when federal teams visited the communities hit the hardest and looked at the properties they thought were most likely to be substantially damaged, including older homes built in flood zones, some with previous flood damage.

“What the team found, unfortunately, is there was a lot of unpermitted work, lack of documentation,” said Robert Samaan, the regional administrator for FEMA’s Region 4, including Florida. “It was just a failure to properly monitor the activity in the special flood hazard area.”

FEMA shared with the Herald three letters it sent Lee County in 2023 — one in February, one in June and one in December — asking for information on the number of damaged homes and warning that not providing the information could result in the county losing its flood insurance discounts.

In recent months, a number of Florida communities, including Miami-Dade County, have benefited from lower flood insurance premiums as a result of improved CRS scores that reflect resilience-related investment. CRS has become particularly beneficial as NFIP pricing reforms – known as Risk Rating 2.0 –that more closely align premium rates with property-specific risks – have contributed to rising premiums for some property owners. Before these reforms, it was not uncommon for lower-risk owners to be subsidizing higher-risk ones through their premium rates.

Rising NFIP rates have been accompanied by another trend: increased involvement by private insurers in the flood insurance market.

“Florida has the most robust private flood insurance market in the United States, which provides consumers with numerous options for coverage,” said Mark Friedlander, director of corporate communications for Triple-I. “Nearly a third of Florida flood policies are written by private carriers, and many private flood insurers offer better pricing and more robust policies than NFIP. It’s worth taking the time to shop for coverage and obtain multiple quotes.”

As recently as 2018, private insurers provided only 3 percent of flood coverage in Florida.

This growth mirrors a national trend. Between 2016 and 2022 the total flood market grew 24 percent – from $3.29 billion in direct premiums written to $4.09 billion – with 77 private companies writing 32.1 percent of the business, up from 18 companies writing 12.5 percent. Private insurers are accounting for a bigger piece of a growing pie.

Florida’s Office of Insurance Regulation has heavily promoted the availability of private flood insurance in the state over the past several years, and many private flood insurers are domiciled in the state, Friedlander said.

“We are committed to helping these communities take appropriate remediation actions to participate in the Community Rating System again and work towards future policy discounts,” FEMA said in its statement.

Earlier this year, Sea Isle City, N.J., had its Class 3 rating restored after a brief demotion in 2023. Sea Isle City and Avalon are the only towns in the state to have Class 3 ratings.

Sea Isle City, N.J., has regained its Class 3 rating under FEMA’s National Flood Insurance Program (NFIP) Community Rating System (CRS) after a brief demotion last year. Being rated Class 3 enables the coastal town’s property owners to receive a 35 percent discount on their federal flood insurance.

CRS is a voluntary incentive-based program designed to encourage strong floodplain management. Class 1 is the highest rating, enabling residents to obtain a 45 percent reduction in their premiums. Class 10 indicates that a community doesn’t participate in CRS. To date, only two of the 1,500 participating communities nationwide have achieved the highest rating: Tulsa, Okla., and Roseville, Calif.

High ratings are not easy to obtain or maintain. Sea Isle City first reached Class 3 in 2018, and the rating was briefly lowered to Class 4 last year after points awarded to communities after Superstorm Sandy expired. The city quickly regained Class 3 status through additional flood-management activities.

In the mid-1990s, conditions were so bad for Sea Isle City that it was nearly ejected from the NFIP. If this had happened, property owners wouldn’t have had access to federal flood insurance. Neil Byrne, the city’s floodplain manager, construction official, building sub-code official, and zoning officer, attributes the improvement to strengthened zoning ordinances that require structures to be elevated higher than FEMA recommends, as well as investment in berms and bulkheads.

“The history of Sea Isle City going from facing expulsion from the NFIP to now leading the charge in the CRS in New Jersey is truly inspirational,” said Thomas Song, FEMA resiliency specialist. “What does not get enough attention is that success in the CRS program has to start with a strong understanding of the day-to-day compliance with NFIP requirements. It is extremely difficult to advance in CRS status without a strong foundation in floodplain-management practices.”

Achieving higher CRS rankings has become something of a friendly competition among coastal New Jersey towns, and only one other New Jersey community – Avalon – has a Class 3.

“Both Sea Isle City and Avalon have demonstrated their commitment in planning for future flooding, implementing higher building standards, and engaging in extensive public outreach,” Song said. “These efforts create an environment geared towards reducing flood damage and enhancing the safety and well-being of residents.”

As NFIP – through its Risk Rating 2.0 reforms – attempts to better align premium rates with risk, CRS discounts become even more significant to owners in flood-prone communities.

Last year, 17 Florida jurisdictions achieved Class 3 ratings. In Cutler Bay – a town on Miami’s southern flank with about 45,000 residents – the average premium dropped by $338. Citywide, that represented a savings of $2.3 million. In January 2024, Miami-Dade County became the latest municipality in the flood- and hurricane-prone state to achieve Class 3, leapfrogging from Class 5 due to the county’s flood-mitigation investments.

Meanwhile, back in New Jersey, Byrne says Sea Isle City hopes to become the state’s first Class 2 community.

“It’s very hard to get to the next level,” he said, but adds that flood pumps could help the city over the hump.

“Ninety-nine percent of our flooding is tidal flooding,” Byrne said, referring to inundation that happens during high tide events. “A lot of it goes away on its own, but we have little areas that need help getting the water out.”

About 90 percent of all U.S. natural disasters involve flooding. For decades, NFIP was practically the only available option for homeowners to obtain flood coverage. Before Risk Rating 2.0, however, coverage for higher-risk properties was often unfairly subsidized by lower-risk property owners.

In recent years, improved data, analysis, and modeling have helped drive increased private-sector interest in flood risk. This, combined with the NFIP reforms, should foster a more competitive flood insurance market in which coverage is both more available and more fairly priced.

“Collective responsibility and multi-disciplinary collaboration are necessary to build resilience around climate-related perils like flood,” said Triple-I CEO Sean Kevelighan. “FEMA’s CRS program is just one example of how communities can make themselves safer and save money through targeted investments that reduce the likelihood and size of catastrophic losses.”

Even as the Smokehouse Creek Fire – the largest wildfire ever to burn across Texas – was declared “nearly contained” this week, the Texas A&M Service warned that conditions are such that the remaining blazes could spread and even more might break out.

“Today, the fire environment will support the potential for multiple, high impact, large wildfires that are highly resistant to control” in the Texas Panhandle, the service said.

This year’s historic Texas fires – like the state’s 2021 anomalous winter storms, California’s recent flooding after years of drought, and a surge in insured losses due to severe convective storms across the United States – underscore the variability of climate-related perils and the need for insurers to be able to adapt their underwriting and pricing to reflect this dynamic environment. It also highlights the importance of using advanced data capabilities to help risk managers better understand the sources and behaviors of these events in order to predict and prevent losses.

For example, Whisker Labs – a company whose advanced sensor network helps monitor home fire perils, as well as tracking faults in the U.S. power grid – recorded about 50 such faults in Texas ahead of the Smokehouse Creek fires.

Bob Marshall, Whisker Labs founder and chief executive, told the Wall Street Journal that evidence suggests Xcel Energy’s equipment was not durable enough to withstand the kind of extreme weather the nation and world increasingly face. Xcel – a major utility with operations in Texas and other states — has acknowledged that its power lines and equipment “appear to have been involved in an ignition of the Smokehouse Creek fire.”

“We know from many recent wildfires that the consequences of poor grid resilience can be catastrophic,” said Marshall, noting that his company’s sensor network recorded similar malfunctions in Maui before last year’s deadly blaze that ripped across the town of Lahaina.

Role of government

Government has a critical role to play in addressing the risk crisis. Modernizing building and land-use codes; revising statutes that facilitate fraud and legal system abuse that drive up claim costs; investing in infrastructure to reduce costly damage related to storms – these and other avenues exist for state and federal government to aid disaster mitigation and resilience.

Too often, however, the public discussion frames the current situation as an “insurance crisis” – confusing cause with effect. Legislators, spurred by calls from their constituents for lower premiums, often propose measures that would tend to worsen the problem because they fail to reflect the importance of accurately valuing risk when pricing coverage.

The federal “reinsurance” proposal put forth in January by U.S. Rep. Adam Schiff of California is a case in point. If enacted, it would dismantle the National Flood Insurance Program (NFIP) and create a “catastrophic property loss reinsurance program” that, among other things, would set coverage thresholds and dictate rating factors based on input from a board in which the insurance industry is only nominally represented.

U.S. Rep. Maxine Waters (also of California) has proposed a Wildfire Insurance Coverage Study Act to research issues around insurance availability and affordability in wildfire-prone communities. During House Financial Services Committee deliberations, Waters compared current challenges in these communities to conditions related to flood risk that led to the establishment of NFIP in 1968. She said there is a precedent for the federal government to step in when there is a “private market failure.”

However, flood risk in 1968 and wildfire risk in 2024 could not be more different. Before FEMA established the NFIP, private insurers were generally unwilling to underwrite flood risk because the peril was considered too unpredictable. The rise of sophisticated computer modeling has since given private insurers much greater confidence covering flood (see chart).

In California, some insurers have begun rethinking their appetite for writing homeowners insurance – not because wildfire losses make properties in the state uninsurable but because policy and regulatory decisions made over 30 years ago have made it hard to write the coverage profitably. Specifically, Proposition 103 and its regulatory implementation have blocked the use of modeling to inform underwriting and pricing and restricted insurers’ ability to incorporate reinsurance costs into their premium pricing.

California’s Insurance Commissioner Ricardo Lara last year announced a Sustainable Insurance Strategy for the state that includes allowing insurers to use forward-looking risk models that prioritize wildfire safety and mitigation and include reinsurance costs into their pricing. It is reasonable to expect that Lara’s modernization plan will lead to insurers increasing their business in the state.

It’s understandable that California legislators are eager to act on climate risk, given their long history with drought, fire, landslides and more recent experience with flooding due to “atmospheric rivers.” But it’s important that any such measures be well thought out and not exacerbate existing problems.

Partners in resilience

Insurers have been addressing climate-related risks for decades, using advanced data and analytical tools to inform underwriting and pricing to ensure sufficient funds exist to pay claims. They also have a natural stake in predicting and preventing losses, rather than just continuing to assess and pay for mounting claims.

As such, they are ideal partners for businesses, communities, governments, and nonprofits – anyone with a stake in climate risk and resilience. Triple-I is engaged in numerous projects aimed at uniting diverse parties in this effort. If you represent an organization that is working to address the risk crisis and your efforts would benefit from involvement with the insurance industry, we’d love to hear from you. Please contact us with a brief description of your work and how the insurance industry might help.

Communities, businesses, and government at all levels to invest in mitigating flood risk and in improving resilience.

It’s important to amplify this message, especially in light of a recent proposal by Rep. Adam Schiff that would, among other things, disband NFIP and require property/casualty insurers to provide “all-risk policies” based on coverage thresholds and rating factors dictated by a board in which the insurance industry is only nominally represented. Last year’s budget uncertainty – in which a potential government shutdown was threatened – left open the very real possibility of funding for NFIP expiring if Congress failed to reach a deal.

“Federal policies and programs, including NFIP, are essential,” said Daniel Kaniewski, managing director, public sector, for Marsh McLennan in his testimony. “But all disasters are local, and so too are resilience investment decisions.”

Before joining Marsh McLennan, Kaniewski was the second-ranking official at FEMA, where he was the agency’s first deputy administrator for resilience.

“To increase the resilience of communities against the pervasive risk of flooding,” Kaniewski testified, “we believe that risk transfer— including from the NFIP, private flood insurance, reinsurance, and parametric insurance — should be paired with risk reduction.”

In this regard, Kaniewski emphasized NFIP’s Community Rating System (CRS), which encourages and rewards community floodplain management practices that exceed the NFIP’s minimum requirements. He cited Tulsa, Okla., as one of two U.S. communities to have achieved the highest CRS rating (the other is Roseville, Calif.), making residents eligible for the program’s greatest flood insurance discount of 45 percent.

Even without achieving the maximum rating, citizens save on flood insurance when their communities invest in resilience. For example, Miami-Dade County, Fla., recently became the latest jurisdiction in the hurricane- and flood-prone state to benefit from CRS program. The county’s new Class 3 rating will result in an estimated $12 million savings annually by giving qualifying residents and business owners in unincorporated parts of the county a 35 percent discount on flood insurance premiums.

Last year, 17 other Florida jurisdictions achieved Class 3 ratings. In Cutler Bay – a town on Miami’s southern flank with about 45,000 residents – the average premium dropped by $338. Citywide, that represented a savings of $2.3 million.

Unfortunately, only 1,500 communities nationwide participate in CRS, underscoring the importance of awareness-building, education, and collaboration.

Kaniewski also highlighted the opportunity presented by community-based catastrophe insurance (CBCI), which uses parametric insurance to provide coverage to local government entities that wish to cover a group of properties. Such programs enhance financial resilience by simultaneously providing affordable coverage and creating incentives for risk reduction.

“Our recent CBCI pilot in New York City was developed in partnership with the City of New York and several nonprofit and insurance industry partners and funded by the National Science Foundation,” Kaniewski said. “It provides a level of financial protection for low-to-moderate-income households that previously lacked flood insurance.”

Kaniewski called on other industries – such as finance and real estate – to encourage flood resilience investments, along with the insurance industry and all levels of government. He cited the recent roadmap for resilience incentives issued by the National Institute of Building Sciences (NIBS) – funded by Fannie Mae and co-authored by representatives of a cross-section of “co-beneficiary industries” – that focused on residential structures prone to flooding. Triple-I subject-matter experts were co-authors on the NIBS project.

Sen. Tim Scott of South Carolina, committee co-chair – along with Sen. Sherrod Brown of Ohio – spoke from the perspective of a former insurance professional who has sold flood insurance about his state’s recent investment in mitigation.

“In 2023, the state’s budget included significant funding for mitigation efforts that would reduce flood damage from future storms,” Scott said.“Backing up that investment, the South Carolina Office of Resilience released a nationally praised Statewide Risk Reduction Plan, identifying the communities most vulnerable to floods and targeting mitigation resources to protect those residents. These are local solutions to local challenges – and they will make a huge difference in the lives of South Carolinians.”

While solutions that work in South Carolina might not work in other states, Scott said, “I’m confident that similar, locally based solutions and approaches could make a huge difference.”

Sen. Katie Britt of Alabama invited Kaniewski to elaborate on her state’s Strengthen Alabama Homes program, which provides grants and insurance discounts to homeowners who make qualifying retrofits to their houses. Britt cited research that found the program had “directly resulted in lower insurance premiums and higher home resale values.”

Kaniewski spoke in detail about Alabama’s efforts, including Strengthen Alabama Homes – which, he pointed out, is now being emulated by other states, including hurricane- and flood-prone Louisiana. He also cited by name the author of the research Britt referenced – Dr. Lars Powell, executive director of the Alabama Center for Insurance Information and Research at the University of Alabama and a Triple-I Non-resident Scholar – for producing “the first study that I’ve seen that gives empirical data — real evidence that mitigation pays.”

Steve Patterson, mayor of Athens, Ohio, described a range of nature-based solutions his city has taken – from rerouting the Hocking River, which runs through the middle of the city, to removing invasive plants and restoring native trees along the bank.

“That’s been very effective in reducing flooding in different neighborhoods throughout the city,” Patterson said. “There are a lot of things cities and villages can do.”

The work done by Athens – like green infrastructure work by the Milwaukee Metropolitan Sewerage District in Wisconsin and municipal entities – offers opportunities to reduce flood risk while improving quality of life for citizens. But, as Patterson points out, not all municipalities have the financial capacity to engage in such projects.

That is where the engagement of co-beneficiaries of resilience investment as partners becomes so crucial.

Miami-Dade County, Fla., has become the latest jurisdiction in the hurricane- and flood-prone state to benefit from participation in FEMA’s Community Rating System (CRS) – an incentive program that recognizes and encourages floodplain management practices that exceed the minimum requirements of FEMA’s National Flood Insurance Program (NFIP).

The county’s new Class 3 rating will result in an estimated $12 million savings annually by giving qualifying residents and business owners in unincorporated parts of the county a 35 percent discount on flood insurance premiums.

“This is a huge step forward in resilience for our county,” Miami-Dade County Mayor Daniella Levine Cava said after FEMA announced that Miami Dade had leaped ahead two rankings in the flood-risk rating. “It indicates that we have been able to demonstrate that we can create more resilience, more protection for our community.”

Miami-Dade County has invested $1 billion in stormwater infrastructure over the past 33 years since the inception of the county’s stormwater utility. Under Mayor Levine Cava’s administration, the county has planned to invest an additional $1 billion in stormwater infrastructure. In the past two years, the county has accelerated projects to upgrade Miami-Dade’s infrastructure and implement critical flood mitigation activities.

Last year, 17 Florida jurisdictions achieved Class 3 ratings. In Cutler Bay – a town on Miami’s southern flank with about 45,000 residents – the average premium dropped by $338. Citywide, that represented a savings of $2.3 million.

Over 1,500 communities nationwide participate in the CRS program, but only Tulsa, Okla., and Roseville, Calif., have taken sufficient steps to achieve Class 1 status and have their citizens receive the greatest premium discount of 45 percent. Both of these communities previously experienced disastrous flooding. Tulsa spent decades developing and implementing stormwater management improvements before receiving its Class 1 designation in 2022.

About 90 percent of all U.S. natural disasters involve flooding. Whether related to coastal and inland inundation due to hurricanes, extreme rainfall, snowmelt, mudflows, or other events, floods cause billions of dollars in losses each year.

As reported in a recent Triple-I “State of the Risk” Issues Brief, flood is no longer an “untouchable” risk for private insurers. For decades, the federally run NFIP was the only place where homeowners could buy flood insurance. But improved data, analysis, and modeling have helped drive private-sector interest in flood risk.

That’s good news for homeowners who understand the evolving nature of this peril, especially as FEMA’s new pricing methodology – Risk Rating 2.0 – applies more actuarially sound pricing to make NFIP’s premium rates more equitable. As NFIP rates become more aligned with principles of risk-based pricing, some policyholders’ prices are expected to fall, while many are going to rise.

CRS provides one avenue for communities to help their citizens get lower rates while proactively reducing flood risk.

By Jeff Dunsavage, Senior Research Analyst, Triple-I

I’m pleased and proud to have been part of Triple-I’s Town Hall — “Attacking the Risk Crisis” — in Washington, D.C. In an intimate setting at the Mayflower Hotel on November 30, 120-plus attendees got to hear from experts representing insurance, government, academia, nonprofits, and other stakeholder groups on climate risk, what’s being done to address it, and what remains to be done.

Triple-I’s first-ever Town Hall was designed as a logical step in its multi-disciplinary, action-oriented effort to change behavior to drive resilience. Capping a year in which headlines about “insurance crises” in several states garnered major media attention, Triple-I and its members and partners recognized the need for clarification.

“What we’re seeing is not an ‘insurance crisis’,” Triple-I CEO Sean Kevelighan told the standing-room-only audience. “We’re in the midst of a risk crisis. Rising insurance premium rates and availability difficulties are not the cause but a symptom of this crisis.”

Whisker Labs CEO Bob Marshall discusses innovation with moderator Jennifer Kyung, Vice President and Chief Underwriter at USAA.

While the insurance industry has a critical role to play and is uniquely well equipped to lead the attack, simply transferring risk is not enough. A recurring theme at the Town Hall was the need to shift from a focus on assessing and repairing damage to one of predicting and preventing losses.

Three moderated discussions – examining the nature of climate risk and its costs; highlighting the need of strategic innovation in mitigating those risks and building resilience; and exploring the role and impact of government policy – gave panelists the opportunity to share their insights with a diverse audience focused on collaborative action.

The agenda was:

Climate Risk Is Spiraling: What Can Be Done?

Moderator: David Wessel, Senior Fellow and Director at the Brookings Institution and former Economics Editor for The Wall Street Journal.

Panelists:

Dr. Philip Klotzbach, Colorado State University, researcher and Triple-I non-resident scholar.

Dan Kaniewski, Managing Director, Public Sector at Marsh McLennan, Former FEMA Deputy Administrator.

Jacqueline Higgins, Head, North America & Senior Vice President, Public Sector Solutions, Swiss Re

Jim Boccher, Chief Development Officer, ServiceMaster.

Jeff Huebner, Chief Risk Officer, CSAA.

Innovation, High- and Low-Tech: How Insurers Are Driving Solutions

Moderator: Jennifer Kyung, VP, Chief Underwriter, USAA.

Panelists:

Partha Srinivasa, EVP, CIO, Erie Insurance.

Sam Krishnamurthy, CTO, Digital Solutions, Crawford.

Bob Marshall, CEO, Whisker Labs.

Stephen DiCenso, Principal,Milliman.

Charlie Sidoti, Executive Director, InnSure.

Outdated Regs to Legal System Abuse: It Will Take Villages to Fix This

Parr Schoolman, SVP and Chief Risk Officer, Allstate.

Tim Judge, SVP, Head Modeler, Chief Climate Officer, Fannie Mae.

Dan Coates, Deputy Director, DRS, Federal Housing Finance Agency.

Fred Karlinsky, Co-Chair of Greenberg Traurig’s Global Insurance Regulatory & Transactions Practice Group.

Panelists and participants alike appreciated the compact, action-focused, conversational nature of the single-afternoon event, as well as the opportunity to discuss areas in which their diverse industry- or sector-specific priorities and efforts overlapped.

If you weren’t able to join us in Washington, don’t worry. In his closing remarks, Kevelighan announced plans to take the program on the road with a local and regional focus, so stay tuned. You can contact us if you’re interested in participating in future Town Halls or other Triple-I events. You also can join the “Attacking the Risk Crisis” LinkedIn Group to be part of the ongoing conversation.

Of the findings in Triple-I’s recent report on consumer perceptions of weather risk, the Weather Channel’s experts were most struck by the fact that 60 percent of homeowners said they’d taken no steps to prepare – so, they asked Triple-I Chief Insurance Officer Dale Porfilio for his perspective.

Ultimately, Porfilio said, it comes down to perceptions.

“Two thirds of the people surveyed said they don’t expect to be affected by weather risk in the next five years,” Porfilio told the Weather Channel. “If you don’t think you’re going to be impacted, why would you prepare with a home evacuation plan or a home inventory?”

Of course, anyone who is exposed to weather is exposed to weather-related risk, and it’s essential for homeowners to understand and address the most relevant risks in order to protect their investments and their families.

Porfilio also addressed a question regarding availability of flood insurance, explaining that coverage is generally available through the Federal Emergency Management Agency’s National Flood Insurance Program, as well as a growing number of private insurers, but “might be perceived as too expensive.”

It is possible, however, that some insurers might not be willing to offer coverage in areas that have been hit repeatedly by flood.

Awareness and preparation are key. The Triple-I survey, published in coordination with global reinsurer Munich Re, found that, among the 22 percent of respondents who reported understanding their level of flood risk, 78 percent said they had purchased flood insurance. The report, Homeowners Perception of Weather Risks, provides insights into trends, behavior and how experiencing a weather event impacts consumer perceptions of future events.

Litigation costs could add between $10 billion and $20 billion to insured losses from Hurricane Ian, adding to the woes of Florida’s already struggling homeowners’ insurance market, says Mark Friedlander Triple-I’s corporate communications director.

Early estimates put Ian’s insured losses above $50 billion.

“Based on the past history of lawsuits following Florida hurricanes and the state’s very litigious environment, we expect a large volume of lawsuits to be filed in the wake of Hurricane Ian,” Friedlander said in an interview with Insurance BusinessAmerica.

Most suits are expected to involve the distinction between flood and windstorm losses. Standard homeowners’ policies exclude flood-related damage from coverage, but differentiating between wind and flood damage in the aftermath of a major hurricane can be challenging.

Flood insurance is available from FEMA’s National Flood Insurance Program, as well as from a growing number of private carriers.

Trial attorneys are “already on the ground” and soliciting business in some of the hardest hit areas, Friedlander said. “This will be a key element in the solvency of struggling regional insurers who are already facing financial challenges.”

Six Florida-based insurers have already failed this year. Florida accounts for 79 percent of all U.S. homeowners’ claims litigation despite representing only 9 percent of insurance claims, according to figures shared by the Florida governor’s office. Litigation has contributed to double-digit premium-rate increases for home insurance in recent years, with Florida’s average annual home-insurance premium of $4,231 being among the nation’s highest.

“Floridians are seeing homeowners’ insurance become costlier and scarcer because for years the state has been the home of too much litigation and too many fraudulent roof-replacement schemes,” Triple-I CEO Sean Kevelighan said. “These two factors contributed enormously to the net underwriting losses Florida’s homeowners’ insurers cumulatively incurred between 2017 and 2021.”

Trevor Burgess, CEO of Neptune Flood Insurance, a St. Petersburg, Fla.-based private flood insurer, said that in all locations pummeled by Ian, the percentage of homes covered by flood policies is down from five years ago. Friedlander told Fox Weather that, while more than 50 percent of properties along Florida’s western Gulf Coast are insured for flood, “inland…the take-up rates for flood insurance are below five percent.”

While Florida is at particularly severe and persistent risk of hurricane-related flooding, the protection gap is by no means unique to the Sunshine State. Inland flooding due to hurricanes is causing increased damage and losses nationwide – often in areas where homeowners tend not to buy flood insurance.

In the days after Hurricane Ida made landfall in August 2021, massive amounts of rain fell in inland, flooding subway lines and streets in New York and New Jersey. More than 40 people were killed in those states and Pennsylvania as basement apartments suddenly filled with water. In the hardest-hit areas, flood insurance take-up rates were under five percent.

Damaging floods that hit Eastern Kentucky in late July 2022 and led to the deaths of 38 people also were largely uninsured against. A mere 1 percent of properties in the counties most affected by the flooding have federal flood insurance.

“We’ve seen some pretty significant changes in the impact of flooding from hurricanes, very far inland,” Keith Wolfe, Swiss Re’s president for U.S. property and casualty, said in a recent Triple-I Executive Exchange. “Hurricanes have just behaved very differently in the past five years, once they come on shore, from what we’ve seen in the past 20.”