The Institutes’ Pete Miller and Francis Bouchard of Marsh McLennan discuss how AI is transforming property/casualty insurance as the industry attacks theclimate crisis.

“Climate” is not a popular word in Washington, D.C., today, so it would take a certain audacity to hold an event whose title prominently includes it in the heart of the U.S. Capitol.

For two days, expert panels at the Ronald Reagan Building and International Trade Center discussed climate-related risks – from flood, wind, and wildfire to extreme heat and cold – and the role of technology in mitigating and building resilience against them. Given the human and financial costs associated with climate risks, it was appropriate to see the property/casualty insurance industry strongly represented.

Peter Miller, CEO of The Institutes, was on hand to talk about the transformative power of AI for insurers, and Triple-I President and CEO Sean Kevelighan discussed – among other things – the collaborative work his organization and its insurance industry members are doing in partnership with governments, non-profits, and others to promote investment in climate resilience. Triple-I is an affiliate of the Institutes.

Sean Kevelighan of Triple-I and Denise Garth, Majesco’s chief strategy officer, discuss how to ensure equitable coverage against climate events.

You can get an idea of the scope and depth of these panels by looking at the agenda, which included titles like:

Building Climate-Resilient Futures: Innovations in Insurance, Finance, and Real Estate;

Fire, Flood, and Wind: Harnessing the Power of Advanced Data-Driven Technology for Climate Resilience;

The Role of Technology and Innovation to Advance Climate Resilience Across our Cities, States and Communities;

Pioneers of Parametric: Navigating Risks with Parametric Insurance Innovations;

Climate in the Crosshairs: How Reinsurers and Investors are Redefining Risk; and

Safeguarding Tomorrow: The Regulator’s Role in Climate Resilience.

As expected, the panels and “fireside chats” went deep into the role of technology; but the importance of partnership, collaboration, and investment across stakeholder groups was a dominant theme for all participants. Coming as the Trump Administration takes such steps as eliminating FEMA’s Building Resilient Infrastructure and Communities (BRIC) program; slashing budgets of federal entities like the National Oceanographic and Atmospheric Administration (NOAA) and the National Weather Service (NWS); and revoking FEMA funding for communities still recovering from last year’s devastation from Hurricane Helene, these discussions were, to say the least, timely.

Helge Joergensen, co-founder and CEO of 7Analytics, talks about using granular data to assess and address flood risk.

In addition to the panels, the event featured a series of “Shark Tank”-style presentations by Insurtechs that got to pitch their products and services to the audience of approximately 500 attendees. A Triple-I member – Norway-based 7Analytics, a provider of granular flood and landslide data – won the competition.

Earth Day 2025 is a good time to recognize organizations that are working hard and investing in climate-risk mitigation and resilience – and to recommit to these efforts for the coming years. What better place to do so than walking distance from both the White House and the Capitol?

The Trump Administration’s unwinding of the Building Resilient Infrastructure and Communities (BRIC) program and cancellation of all BRIC applications from fiscal years 2020-2023 reinforce the need for collaboration among state and local government and private-sector stakeholders in climate resilience investment.

Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters. FEMA announced on April 4 that it is ending BRIC .

Chad Berginnis, executive director of the Association of State Floodplain Managers (ASFPM), called the decision “beyond reckless.”

“Although ASFPM has had some qualms about how FEMA’s BRIC program was implemented, it was still a cornerstone of our nation’s hazard mitigation strategy, and the agency has worked to make improvements each year,” Berginnis said. “Eliminating it entirely — mid-award cycle, no less — defies common sense.”

While the FEMA press release called BRIC a “wasteful, politicized grant program,” Berginnis said investments in hazard mitigation programs “are the opposite of ‘wasteful.’ “ He pointed to a study by the National Institute of Building Sciences (NIBS) that showed flood hazard mitigation investments return up to $8 in benefits for every $1 spent.

“At this very moment, when states like Arkansas, Kentucky, and Tennessee are grappling with major flooding, the Administration’s decision to walk away from BRIC is hard to understand,” Berginnis said.

Heading into hurricane season

Especially hard hit will be catastrophe-prone Florida. Nearly $300 million in federal aid meant to help protect communities from flooding, hurricanes, and other natural disasters has been frozen since President Trump took office in January, according to an article in Government Technology.

The loss of BRIC funding leaves dozens of Florida projects in limbo, from a plan to raise roads in St. Augustine to a $150 million effort to strengthen canals in South Florida. According to Government Technology, the agency most impacted is the South Florida Water Management District, responsible for maintaining water quality, controlling the water supply, ecosystem restoration and flood control in a 16-county area that runs from Orlando south to the Keys.

“The district received only $6 million of its $150 million grant before the program was canceled,” the article said. “The money was intended to help build three structures on canals and basins in North Miami -Dade and Broward counties to improve flood mitigation.”

Florida’s Division of Emergency Management must return $36.9 million in BRIC money that was earmarked for management costs and technical assistance. Jacksonville will lose $24.9 million targeted to raise roads and make improvements to a water reclamation facility.

FEMA announced the decision to end BRIC the day after Colorado State University’s (CSU) Department of Atmospheric Science released a forecast projecting an above-average Atlantic hurricane season for 2025. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach CSU research team forecasts 17 named storms, nine hurricanes – four of them “major” (Category 3, 4, or 5). A typical season has 14 named storms, seven hurricanes – three of them major.

Nationwide impacts

More than $280 million in federal funding for flood protection and climate resilience projects across New York City — “including critical upgrades in Central Harlem, East Elmhurst, and the South Street Seaport” – is now at risk, according to an article in AMNY. The cuts affect over $325 million in pending projects statewide and another $56 million of projects where work has already begun.

Senate Majority Leader Chuck Schumer and Gov. Kathy Hochul warned that the move jeopardizes public safety as climate-driven disasters become more frequent and severe.

“In the last few years, New Yorkers have faced hurricanes, tornadoes, blizzards, wildfires, and even an earthquake – and FEMA assistance has been critical to help us rebuild,” Hochul said. “Cutting funding for communities across New York is short-sighted and a massive risk to public safety.”

According to the National Association of Counties, cancellation of BRIC funding has several implications for counties, including paused or canceled projects, budget and planning adjustments, and reduced capacity for long-term risk reduction.

North Dakota, for example, has 10 projects that were authorized for federal funding. Those dollars will now be rescinded. Impacted projects include $7.1 million for a water intake project in Washburn; $7.8 million for a regional wastewater treatment project in Lincoln; and $1.9 million for a wastewater lagoon project in Fessenden.

“This is devastating for our community,” said Tammy Roehrich, emergency manager for Wells County. “Two million dollars to a little community of 450 people is huge.”

The cancellation of BRIC roughly coincides with FEMA’s decision to deny North Carolina’s request to continue matching 100 percent of the state’s spending on Hurricane Helene recovery.

“The need in western North Carolina remains immense — people need debris removed, homes rebuilt, and roads restored,” said Gov. Josh Stein. “Six months later, the people of western North Carolina are working hard to get back on their feet; they need FEMA to help them get the job done.”

Resilience key to insurance availability

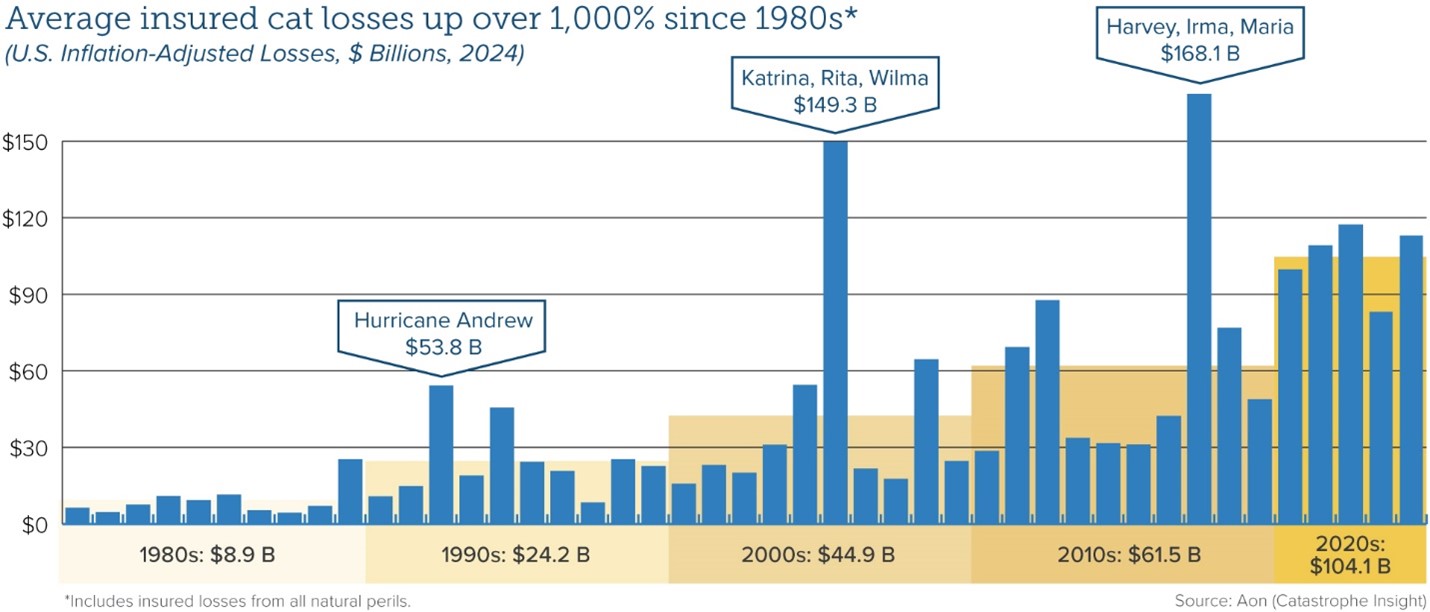

Average insured catastrophe losses have been on the rise for decades, reflecting a combination of climate-related factors and demographic trends as more people have moved into harm’s way.

“Investing in the resilience of homes, businesses, and communities is the most proactive strategy to reducing the damage caused by climate,” said Triple-I Chief Insurance Officer Dale Porfilio. “Defunding federal resilience grants will slow the essential investments being made by communities across the U.S.”

Flood is a particularly pressing problem, as 90 percent of natural disasters involve flooding, according to the National Flood Insurance Program (NFIP). The devastation wrought by Hurricane Helene in 2024 across a 500-mile swath of the U.S. Southeast – including Florida, Georgia, the Carolinas, Virginia, and Tennessee – highlighted the growing vulnerability of inland areas to flooding from both tropical and severe convective storms, as well as the scale of the flood-protection gap in non-coastal areas.

Coastal flooding in the U.S. now occurs three times more frequently than 30 years ago, and this acceleration shows no signs of slowing, according to recent research. By 2050, flood frequency is projected to increase tenfold compared to current levels, driven by rising sea levels that push tides and storm surges higher and further inland.

In addition to the movement of more people and property into harm’s way, climate-related risks are exacerbated by inflation (which drives up the cost of repairing and replacing damaged property); legal system abuse, (which delays claim settlements and drives up insurance premium rates); and antiquated regulations (like California’s Proposition 103) that discourage insurers from writing business in the states subject to them.

Thanks to the engagement and collaboration of a range of stakeholders, some of these factors in some states are being addressed. Others – for example, improved building and zoning codes that could help reduce losses and improve insurance affordability – have met persistent local resistance.

As frequently reported on this blog, the property/casualty insurance industry has been working hard with governments, communities, businesses, and others to address the causes of high costs and the insurance affordability and availability challenges that flow from them. Triple-I, its members, and partners are involved in several of these efforts, which we’ll be reporting on here as they progress.

The efficacy of collaboration and investment by “co-beneficiaries” in resilience initiatives was a dominant theme throughout Triple-I’s 2024 Joint Industry Forum – particularly in the final panel, which celebrated leaders behind recent real-world impacts of such investments.

Moderated by Dan Kaniewski, Marsh McLennan (MMC) managing director for public sector, the panelists discussed how their multi-industry backgrounds inform their innovative mindsets, as well as their knowledge on the profound ripple effects of targeted resilience planning.

The panel included:

Jonathan Gonzalez, co-founder and CEO of Raincoat;

Bob Marshall, co-founder and CEO of Whisker Labs;

Dawn Miller, chief commercial officer of Lloyd’s and CEO of Lloyd’s Americas; and

Lars Powell, director of the Alabama Center for Insurance Information and Research (ACIIR) at the University of Alabama and a Triple-I Non-Resident Scholar.

Productive partnership

Kaniewski – who spent most of his career in emergency management, previously serving as the second-ranking official at the Federal Emergency Management Agency (FEMA) and the agency’s first deputy administrator for resilience – kicked off the panel by raising the question “how do we define success?”

He characterized success as “putting theory into practice” and “having elected officials taking steps to reduce risk and transfer some of this risk from federal, state, or local taxpayers.”

But, as participants in earlier panels and this one made clear, government efforts can only go so far without private-sector collaboration.

“It doesn’t matter who makes that investment, whether it’s the homeowner, the business owner, or the government,” Kaniewski explained. “The reality is we all benefit from that one investment. If we can acknowledge that we benefit from those investments, we should do our best to incentivize them.”

Kaniewski and Raincoat’s Gonzalez were both integral in the development of community-based catastrophe insurance (CBCI), developed in the wake of Superstorm Sandy in 2012.

“A lot of the neighborhoods that experienced flooding due to Sandy didn’t have access to insurance prior to the flooding – and then, post flooding, the government really had to step up to figure out how to keep those families in those houses,” Gonzalez said.

In collaboration with the city, a nonprofit called the Center for NYC Neighborhoods developed the concept of buying parametric insurance on behalf of these communities, with any payouts going toward helping families stay in their homes after disasters. Unlike traditional indemnity insurance, a parametric policy pays out if certain agreed-upon conditions are met – for example, a specific wind speed or earthquake magnitude in a particular area – regardless of damage. Parametric insurance eliminates the need for time-consuming claim adjustment. Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders.

In this case, Kaniewski said, success was reflected in the fact that the pilot program received sufficient funding not only for renewal but expansion, bringing needed protection to even more vulnerable communities.

Powell reinforced this sentiment in explaining ACIIR’s research on the FORTIFIED method, a set of voluntary construction standards created by the Insurance Institute for Business and Home Safety (IBHS) for durability against severe weather. The insurance industry-funded Strengthen Alabama Homes program issues grants and substantial insurance premium discounts to homeowners to retrofit their houses along these guidelines, prompting multiple states to replicate the program.

Such homes in Alabama sustained 54 to 76 percent reduced loss frequency from Hurricane Sally compared to standard homes, Powell reported, and an estimated 65 to 73 percent could have been saved in claims if standard homes were FORTIFIED.

Incentivizing contractors to learn FORTIFIED standards was especially critical, Powell explained, because they further advertised these skills and expanded the presence of FORTIFIED homes beyond the grant program.

“A lot of companies have said for several years, ‘we don’t know if we’re comfortable writing these…we haven’t seen it on the ground,’” Powell said. “Well, now we’ve seen it on the ground. We need to have houses that don’t burn down or blow over. We know how to do it, it’s not that expensive.”

Addressing concerns to drive adoption

Miller described how Lloyd’s Lab works to ease that discomfort by creating a space for businesses to nurture and integrate novel insights and products without fear. With mentor support, companies are encouraged to test new ideas while free from the usual degree of financial and/or intellectual property risks attached to innovation investments.

“It’s about having an avenue out to try,” Miller said. “Having that courage, as we continue to work together, to try to understand what’s working, what’s not, and being brave to say, ‘this isn’t working, but we can course correct.’”

Whisker Labs’ Marshall noted that numerous insurance carriers have taken a chance on his company’s front-line disaster mitigation devices, Ting, by paying for and distributing them to their customers.

Ting plug-in sensors detect conditions that could lead to electrical fires through continuous monitoring of a home’s electrical system. Statistically preventing more than 80 percent of electrical fires, communities benefit – not only by preventing individual home fires but also by providing data about the electrical grid and potentially heading off grid-initiated wildfires.

“There are so many applications for the data,” Marshall said, but “to have a true impact on society…we have to prove that we’re preventing more losses than the cost, and we have to do that in partnership with insurance carriers.”

Everyone wins if everyone plays

Cultivating innovative solutions is pivotal to enhancing resilience, the panelists agreed – but driving them forward requires more than just the insurance industry’s support.

He pointed to a project last year – funded by Fannie Mae and developed by the National Institute of Building Science (NIBS) – that culminated in a roadmap for resilience investment incentives, focusing on urban flooding.

The co-authors of the project, including Triple-I subject-matter experts, represented a cross-section of “co-beneficiary” groups, such as the insurance, finance, and real estate industries and all levels of government, Kaniewski said.

Implementation of the roadmap requires participation from communities and multiple co-beneficiaries. Triple-I and NIBS are exploring such collaborations with potential co-beneficiaries in several areas of the United States.

The devastation wrought by Hurricane Helene in September 2024 across a 500-mile swath of the U.S. Southeast highlighted the growing vulnerability of inland areas to flooding from both tropical storms and severe convective storms, according to the latest Triple-I “State of the Risk” Issues Brief.

These events also highlight the scale of the flood-protection gap in non-coastal areas. Private insurers are stepping up to help close that gap, but increased homeowner awareness and investment in flood resilience across all co-beneficiary groups will be needed as more and more people move into harm’s way.

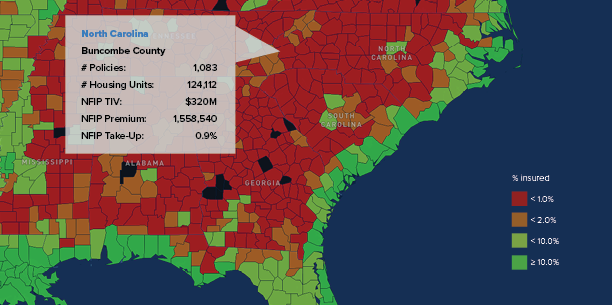

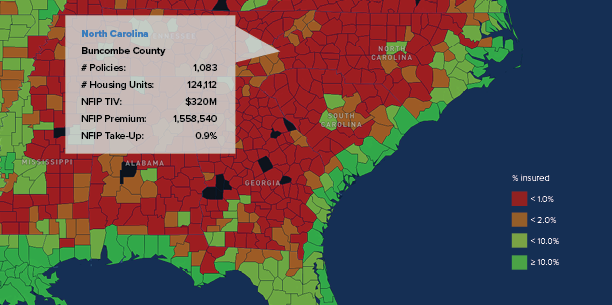

Helene dumped 40 trillion gallons of water across Florida, Georgia, the Carolinas, Virginia, and Tennessee, causing hundreds of deaths and billions in insured losses. Much of the loss was concentrated in western North Carolina, with parts of Buncombe County – home to Asheville and its historic arts district – left virtually unrecognizable. Less than 1 percent of residents in Buncombe County had federal flood insurance when Helene struck.

The experience of these states far inland echoed those of New York, New Jersey, and Pennsylvania in August 2021, when remnants of Hurricane Ida brought rains that flooded subways and basement apartments, with more than 40 people killed in those states.

“The whole swath going up the East Coast” that Hurricane Ida struck in the days after it made landfall “had less than 5 percent flood insurance coverage,” said Triple-I CEO Sean Kevelighan at the time.

Then, in July 2023, a series of intense thunderstorms resulted in heavy rainfall, deadly flash floods, and severe river flooding in eastern Kentucky and central Appalachia. Flooding led to 39 fatalities and federal disaster-area declarations for 13 eastern Kentucky counties. According to the Federal Emergency Management Agency (FEMA), only a few dozen federal flood insurance policies were in effect in the affected areas before the storm.

Low inland take-up rates largely reflect consumer misunderstandings about flood insurance. Though approximately 90 percent of all U.S. natural disasters involve flooding, many homeowners are unaware that a standard homeowners policy doesn’t cover flood damage. Similarly, many believe flood coverage is unnecessary unless their mortgage lenders require it. It also is not uncommon for homeowners to drop flood insurance coverage once their mortgage is paid off to save money.

Private insurers stepping up

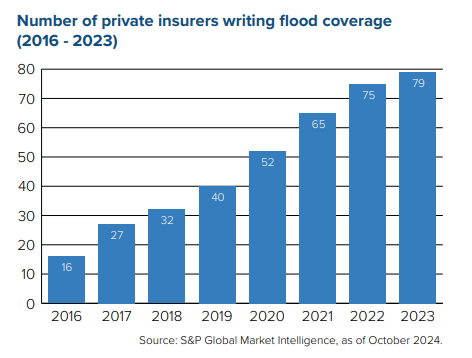

More than half of all homeowners with flood insurance are covered by NFIP, which is part of FEMA and was created in 1968 – a time when few private insurers were willing to write flood coverage. In recent years, however, insurers have grown more comfortable taking on flood risk, thanks in large part to improved data and analytics capabilities.

The private flood market has changed since 2016, when only 12.6 percent of coverage was written by 16 insurers. In 2019, federal regulators allowed mortgage lenders to accept private flood insurance if the policies abided by regulatory definitions. The already-growing private appetite for flood risk gained steam after that. Private insurers are gradually accounting for a bigger piece of a growing flood risk pie.

Insurance necessary – but not sufficient

Insurance can play a major role in closing the protection gap, but, with increasing numbers of people moving into harm’s way and storms behaving more unpredictably, the current state of affairs is not sustainable. Greater investment in mitigation and resilience is essential to reducing the personal and financial losses associated with flooding.

Such investment has paid off in Florida, where the communities of Babcock Ranch and Hunters Point survived Hurricanes Helene and Milton relatively unscathed. Babcock Rance made headlines for sheltering thousands of evacuees from neighboring communities and never losing power during Milton, which devastated numerous neighboring cities and left more than three million people without power.

Both of these communities were designed and built in recent years with sustainability and resilience in mind.

Incentives and public-private partnership will be critical to reducing perils and improving insurability in vulnerable locations. Recent research on the impact of removing development incentives from coastal areas can improve flood loss experience in the areas directly affected by the removal of such incentives, as well as neighboring areas where development subsidies remain in place.

Spanning over 500 miles of the southeastern United States, Hurricane Helene’s path of destruction has drawn public attention to inland flood risk and the need for improved resilience planning and insurance purchase (“take up”) to confront the protection gap.

Extreme rainfall and wind inflicted a combination of catastrophic flooding, landslides, and extreme rainfall and wind gusts dumped an unparalleled 40 trillion gallons of water across Florida, Georgia, North Carolina, South Carolina, Virginia, and Tennessee, causing hundreds of deaths and billions in insured losses.

Most losses are concentrated in western North Carolina, with much of Buncombe County – home to Asheville and its historic arts district – left virtually unrecognizable. Torrential rain and mountain runoff submerged Asheville under nearly 25 feet of water as rivers swelled, while neighboring communities were similarly flattened or swept away.

Rebuilding will take years, especially as widespread lack of flood insurance forces most victims to seek federal grants and loans for assistance, slowing recovery. Compounding these challenges, misinformation about assistance from the Federal Emergency Management Agency (FEMA) has impeded aid operations in certain areas, leading FEMA to issue a fact sheet clarifying the reality on the ground.

A persistent protection gap

Less than 1 percent of residents in Buncombe County had federal flood insurance as Helene struck, as illustrated in the map below, which is based on National Flood Insurance Program (NFIP) take-up rate data. Inland flooding isn’t new, and neither is the inland flood-protection gap.

In August 2021, the National Weather Service issued its first-ever flash-flood warning for New York City as remnants of Hurricane Ida brought rains that flooded subway lines and streets in New York and New Jersey. More than 40 people were killed in those states and Pennsylvania as basement apartments suddenly filled with water.

Then, in July 2023, a series of intense thunderstorms resulted in heavy rainfall, deadly flash floods, and severe river flooding in eastern Kentucky and central Appalachia, with hourly rainfall rates exceeding four inches over the course of several days. Subsequent flooding led to 39 fatalities and federal disaster-area declarations for 13 eastern Kentucky counties. According to FEMA, only a few dozen federal flood insurance policies were in effect in the affected areas before the recent storm.

“We’ve seen some pretty significant changes in the impact of flooding from hurricanes, very far inland,” Keith Wolfe, Swiss Re’s president for U.S. property and casualty, told Triple-I CEO Sean Kevelighan in a Triple-I Executive Exchange. “Hurricanes have just behaved very differently in the past five years, once they come on shore, from what we’ve seen in the past 20.”

Need for education and awareness

Low inland take-up rates largely reflect consumer misunderstandings about flood insurance. Though approximately 90 percent of all U.S. natural disasters involve flooding, many homeowners are unaware that a standard homeowners policy doesn’t cover flood damage. Similarly, many believe flood coverage is unnecessary unless their mortgage lenders require it. It also is not uncommon for homeowners to drop flood insurance coverage once their mortgage is paid off to save money.

More than half of all homeowners with flood insurance are covered by NFIP, which is part of the FEMA and was created in 1968 – a time when few private insurers were willing to write flood coverage.

In recent years, insurers have grown more comfortable taking on flood risk, thanks in large part to improved data and analytics capabilities. This increased interest in flood among private insurers offers hope for improved affordability of coverage at a time when NFIP’s Risk Rating 2.0 reforms have driven up flood insurance premium rates for higher-risk property owners.

New tools and techniques

New tools – such as parametric insurance and community-based catastrophe insurance – also offer ways of improving flood resilience. Unlike traditional indemnity insurance, parametric structures cover risks without the complications of sending adjusters to assess damage after an event. Instead of paying for damage that has occurred, it pays out if certain agreed-upon conditions are met – for example, a specific wind speed or earthquake magnitude in a particular area. If coverage is triggered, a payment is made, regardless of damage.

Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders. Alone, or as part of a package including indemnity coverage, parametric insurance can provide liquidity that businesses and communities need for post-catastrophe resilience.

While localized insurance approaches can support flood resilience, coordinated investments in public education and preemptive mitigation are crucial to reducing risk and making insurance more available and affordable. Intergovernmental collaboration with insurers on development zoning and building codes, for instance, can promote the creation of safer and climate-adaptive infrastructure, lowering human and economic losses.

Despite warnings from two leading insurance rating agencies that Hurricane Milton weakened or threatened Florida’s recovering home insurance market, the market “can manage losses” from the Category 4 storm “and are ready to cover yet another hurricane,” if one should come this season, according to industry experts who spoke with the South Florida Sun Sentinel.

AM Best and Fitch Ratings each issued reports last week warning that Milton could stretch liquidity of Florida-based residential insurers that are primarily focused on protecting in-state homeowners. But experts closer to Florida’s insurance industry cast doubt on those assertions. One reason is the two companies don’t rate most of the domestic Florida insurers whose financial strength they question, the Sun Sentinel reported.

While cautioning that loss estimates haven’t been released yet from catastrophe modelers, Florida market experts said the state’s insurers have sufficient reinsurance capital to weather not only hurricanes Debby, Helene, and Milton but another Milton-sized storm if one emerges during the latter portion of the 2024 Atlantic season.

Karen Clark, president of catastrophe modeler Karen Clark & Co., told the Sun Sentinel, “Florida insurers and the reinsurers that protect them use sophisticated tools to understand the probabilities of hurricane losses of different sizes.”

Joe Petrelli, president of Demotech – the only rating firm that reviews the financial health of most Florida-based property insurers – said insurers can purchase additional reinsurance capacity if they use up what they purchased to get them through the year.

“Carriers will have catastrophe reinsurance in place for another event, so it should not be an issue,” Petrelli told the Sun Sentinel.

“While we expect Milton to be a larger wind loss event compared to hurricanes Debby and Helene, we do not anticipate it to be near the level of insured losses caused by Hurricane Ian,” Mark Friedlander, Triple-I’s director of corporate communications said.

Ian was a Category 4 major hurricane that made landfall in Southwest Florida in September 2022 and caused an estimated $50 billion to $60 billion in private insured losses. The estimate accounted for up to $10 billion in litigated claims due to one-way attorney fees that were in effect at the time of the storm.

“The market is in its best financial condition in many years due to state legislative reforms in 2022 and 2023 that addressed the man-made factors which caused the Florida risk crisis – legal system abuse and claim fraud,” Friedlander said. “Florida residential insurers also have adequate levels of reinsurance to cover catastrophic loss events like Milton.”

Withdrawing federal subsidies in climate-vulnerable areas can deter development and promote disaster resilience, according to a recent Nature Climate Change study. The study found that these benefits extend beyond the targeted areas.

These findings underscore the utility of land conservation as hazard protection, as well as the critical role financial incentives play in driving – or obstructing – resilience.

A natural experiment

“Empirical research into this question is limited because few policy experiments exist where a clear comparison can be made of ‘treatment’ settings, where incentives for development have been removed, and ‘control’ settings, similar areas where such incentives remain,” the study states. “One such experiment does exist, however.”

The 1982 Coastal Barrier Resources Act (CBRA) rendered more than one million acres along U.S. coasts ineligible for various incentives, including access to flood insurance through the National Flood Insurance Program (NFIP). Though development in these high-risk areas remains legal, the CBRA shifts total responsibility onto property owners to manage that risk.

Decades later, areas under the CBRA have 83 percent fewer buildings per acre than similar non-designated areas, leading to higher development densities in less risky neighboring areas. Subsequent reductions in flood damages have generated hundreds of millions in NFIP savings per year – due not only to NFIP ineligibility in CBRA areas, but also to fewer and less costly flood claims filed in neighboring areas.

Neighboring areas benefit from the natural infrastructure provided by undeveloped wetlands, which can ease flood risk severity by impeding the rate and flow of flooding.

Housing demand a challenge

Despite the evident value of limiting development in high-risk areas, such limitations are challenging to implement during a nationwide affordable housing shortage. Navigating housing demands in tandem with a rise in natural disasters will require a coordinated effort on local, state, and federal levels.

One approach is FEMA’s Community Rating System (CRS), a voluntary program that incentivizes local floodplain management practices exceeding the NFIP’s minimum standards. Class 1 is the highest rating, qualifying residents for a 45 percent reduction in their premiums. Of the nearly 23,000 participating NFIP communities, only 1,500 participate in the CRS. Of those 1,500, only two have achieved the highest rating: Tulsa, Okla., and Roseville, Calif.

While high ratings are difficult to secure, investments in flood planning yield long-term gains via safer infrastructure and more affordable premiums, with discounts in lower-rated jurisdictions still equating to millions in savings.

CRS discounts are especially advantageous following NFIP’s Risk Rating 2.0 reforms and increased private-sector interest in flood risk. Both have contributed to a more representative and actuarially sound flood insurance market that sets rates based on property-specific risks, thereby raising the premiums of riskier property owners.

Concerns about effective climate risk mitigation strategies persist, however – especially in the wake of unprecedented destruction wrought by Hurricane Helene.

While NFIP reforms are making flood insurance more equitable, many homeowners – including many of those most impacted by Hurricane Helene – are unaware that flood coverage is not offered by a standard homeowners policy. Likewise, many believe that flood insurance is necessary only if required by their lenders, leaving inland residents more susceptible to costly flood damages.

This lack of common knowledge about insurance is not a failure of consumers – rather, it represents the insurance industry’s urgent need to provide greater outreach, public education, and stakeholder collaboration.

Incentivizing public-private collaboration has demonstrated success, so removing federal incentives from additional high-risk areas would require extensive multidisciplinary coordination to prevent inadvertently widening the insurance protection gap. Emerging approaches to risk mitigation and resilience – such as community-based catastrophe insurance, New York City’s recent parametric insurance flood pilot, and the nation’s first public wildfire catastrophe model in California – offer opportunities for fairer rates and targeted local resilience.

If paired with policies based on the CBRA, such innovations could help ensure that appropriate risk transfer occurs alongside substantial risk reduction.

As work continues to address the harm inflicted by Hurricane Helene, researchers at Colorado State University (CSU) warn that the next two weeks “will be characterized by [tropical storm] activity at above normal levels.”

The CSU researchers define “above normal” by accumulated cyclone energy (ACE) of more than 10. This level of hurricane intensity has been reached in less than one-third of two-week periods in early October since records have been kept.

Hurricane Kirk, they wrote, is “extremely likely” to generate more than 10 ACE during its lifetime in the eastern/central Atlantic. Tropical Depression 13 has just formed and is likely to generate considerable ACE in its lifetime across the Atlantic. The National Hurricane Center is monitoring an additional area for formation in the Gulf of Mexico that should be monitored for potential U.S. impacts.

“Hurricane Kirk is forecast to track northwestward across the open Atlantic over the next few days, likely becoming a powerful major hurricane in the process,” said CSU research scientist and Triple-I Non-resident Scholar Phil Klotzbach. “The system looks to generate approximately an additional 20 ACE before dissipation, effectively guaranteeing the above-normal category for the two-week period.”

With more than 160 people confirmed dead in Florida, Georgia, South Carolina, North Carolina, Virginia, and Tennessee, Helene is now the second-deadliest hurricane to strike the mainland United States in the past 55 years, topped only by Hurricane Katrina in 2005.

Reinsurance broker Gallagher Re predicts that private insurance market losses from Helene will rise to the mid-to-high single-digit billion dollar level, higher than its pre-landfall forecast of $3 billion to $6 billion, according to Chief Science Officer and Meteorologist Steve Bowen.

As always – and with particular urgency in the wake of Helene’s devastation – Triple-I urges everyone in hurricane-prone areas to stay informed, be prepared, and follow the instructions of local authorities. We also ask that people be mindful of the potential for flood danger far inland, as reflected in the experiences of many non-coastal communities during Hurricane Ida and Helene.

Analysis based on precise, granular data is key to fair, accurate insurance pricing – and is more important than ever before in an era of increased climate-related risks. In a recent Executive Exchange discussion with Triple-I CEO Sean Kevelighan, a co-founder of Norway-based 7Analytics discussed how his company’s methodology – honed by use in the oil and gas industry – can help insurers identify opportunities to profitably write flood coverage in what might seem to be “untouchable” areas.

7Analytics uses hydrology, geology, and data science to develop high-precision flood risk data tools.

“We are four oil and gas geologists behind 7Analytics,” said Jonas Torland, who also is the company’s chief commercial officer, “and between us we’ve spent 100 years chasing fluids in the very complicated subsurface.”

Torland believes his firm can bring a new level of refined expertise to U.S. insurers seeking to pinpoint pockets of insurability against flood.

“Instead of analyzing faults and carrier beds, we’re now analyzing streams and culverts and changing land-use features,” Torland told Kevelighan. “I think the approach we bring is brilliant for problems related to climate and population migration and urban pluvial flooding in particular.”

Torland said he hopes his company can help close the U.S. flood protection gap by giving private insurers the comfort levels and incentives they need to write the coverage. While more insurers have been covering flood risk in recent years, the National Flood Insurance Program (NFIP) still underwrites the lion’s share of flood risk.

NFIP’s recently reformed pricing methodology, Risk Rating 2.0 – which aims to make the government agency’s premium rates more actuarially sound and equitable by better aligning them with individual properties’ risk – has created concerns among policyholders whose premiums are rising as rates become more aligned with principles of risk-based pricing.

As the cost of participating in NFIP rises for some, it is reasonable to expect that private insurers will recognize the market opportunity and respond by applying cutting-edge data and analytics capabilities and more refined pricing techniques to seize those opportunities. This is where Torland believes 7Analytics can help, and he noted that the company had already had some positive test results in flood-prone Florida.

Kevelighan agreed that solutions like those provided by 7Analytics are what is needed to help private insurers close the flood insurance gap. Insurers are telling Triple-I as much.

“I think we can all agree that the current way we review flood risk is antiquated,” Kevelighan said. “So we’ve got to bring that new technology, that new innovation to begin changing behaviors and changing how and where we develop and how we live.”

Hurricane Beryl’s rapid escalation from a tropical storm to a Category 5 hurricane does not bode well for the 2024 Atlantic Hurricane season, which is already projected to be of above-average intensity, warns Triple-I non-resident scholar Dr. Philip Klotzbach.

“This early-season storm activity is breaking records that were set in 1933 and 2005, two of the busiest Atlantic hurricane seasons on record,” Dr. Klotzbach, a research scientist in the Department of Atmospheric Science at Colorado State University, recently told The New York Times.

The quick escalation was a result of above-average sea surface temperatures. A hurricane that intensifies faster can be more dangerous as it leaves less time for people in its path to prepare and evacuate. Last October, Hurricane Otis moved up by multiple categories in just one day before striking Acapulco, Mexico, as a Cat-5 that killed more than 50 people.

After weakening to a tropical storm, Beryl made landfall as a Cat-1 hurricane near Matagorda, Texas, around 4 a.m. on July 8, according to the National Hurricane Center, making it the first named storm in the 2024 season to make landfall in the United States. Beryl unleashed flooding rains and winds that transformed roads into rivers and ripped through power lines and tossed trees onto homes, roads, and cars. Restoring power to millions of Texans could take days or even weeks, subjecting residents who will not have air conditioning to further risk as a sweltering heatwave settles over the state.

Extreme heat was just one climate-related topic addressed by Triple-I Chief Insurance Officer Dale Porfilio in an interview with CNBC’s “Last Call” on July 9. While most farmers are insured against crop damage due to heat conditions and homeowners insurance typically covers wildfire-related losses, Porfilio noted, a “more subtle impact is on roofs that we thought were built to a 20-year lifespan.”

When subjected to extreme heat, roofs can become more brittle and prone to damage from wind or hail.

“So, you have to think about the roof coverage on your home insurance policy,” Porfilio said.

He also pointed out that flood risk represents “one of the biggest insurance gaps in this country. Over 90 percent of homeowners do not have the coverage.”

Many people incorrectly believe homeowners insurance covers flood damage or that they don’t need the coverage if their mortgage lender does not require it.

In an interview on CNBC’s “Squawk Box,” Triple-I CEO Sean Kevelighan discussed the potential impact of the predicted “well above-average” 2024 season on the U.S. property/casualty market.

“This is what the insurance industry is prepared for,” Kevelighan said. “It keeps capital on hand after writing policies to make sure that those promises can be kept.” The P/C industry has $1.1. trillion in surplus as of March 31, 2024.

Kevelighan pointed out that the challenges to the industry go beyond climate-related trends, explaining how legal system abuse, regulatory environments, shifting populations, and inflation are impacting insurers’ loss costs.

In Florida, for example, “you’ve got over 70 percent of all homeowners insurance litigation residing in that state, whereas it represents less than 10 percent of the overall claims.”

He pointed out that Florida’s insurance market has improved – with homeowners insurance premium growth flattening somewhat – as a result of tort reform legislation and added that Louisiana’s legislature addressed insurance reform during its most recent session.

“In California, insurers can’t catch up with inflationary costs because of regulatory constraints,” Kevelighan noted. “They are not able to model [climate risk] and are not able price reinsurance into their policies.”

California’s wildfire situation is complex, and the state’s Proposition 103 has hindered insurers’ ability to profitably write homeowners coverage in that disaster-prone state. In late September 2023, California Insurance Commissioner Ricardo Lara announced a package of executive actions aimed at addressing some of the challenges included in Proposition 103. Lara has given the department a deadline of December 2024 to have the new rules completed.