Deadly floods swept through the United States at a record pace in 2025, triggering more flash flood warnings than any year to date. With flood events in 99 percent of U.S. counties over the past 20 years, more communities are vulnerable to flooding than ever before, especially as exposure spreads increasingly inland.

Many homeowners, however, remain unprotected from the risk, underscoring a growing coverage gap as more people move into harm’s way. A new Triple-I Issues Brief explores the insurance industry’s role in closing that gap, as well as the public outreach and mitigation investment needed to reduce losses for all co-beneficiaries of flood resilience.

Extreme weather on the rise

Floods – alongside severe convective storms and wildfires – accounted for nearly all insured global losses last year, at $98 billion of $108 billion, according to Munich Re estimates. In the United States, inland flooding from both tropical and severe convective storms caused much of the devastation, led by the unprecedented Central Texas flood that claimed more than 130 lives.

Defined by NOAA as a rapid swing between two extreme environmental conditions, “weather whiplash” is becoming increasingly frequent in states like Texas and California, where prolonged droughts collide with periods of heavy rains and flooding, amplifying their effects. Fueled by increased tropical moisture from higher ocean temperatures, these drought-to-flood/hot-to-cold transitions drove many of the 21 billion-dollar severe convective storms in 2025, more than any prior year on record.

Flood market growth continues

Many homeowners remain unaware that a standard homeowners’ policy doesn’t cover flood damage or believe flood coverage is unnecessary unless their mortgage lender requires it. A separate 2023 study from Munich Re, in collaboration with Triple-I, found 64 percent of homeowners believed they were not at risk for flooding. It also is not uncommon for homeowners to drop flood insurance coverage once their mortgage is paid off to save money.

Though more than half of all homeowners with flood insurance are covered by FEMA’s National Flood Insurance Program (NFIP), federal regulations introduced in 2019 allowed mortgage lenders to accept private flood insurance if policies abided by regulatory definitions, steering a greater percentage of private insurers to the flood market. Between 2016 and 2024, the total flood market grew by nearly 43 percent – from $3.29 billion in direct premiums written to $4.7 billion – with 79 private companies writing just over 27 percent of the business.

Public-private partnerships are crucial

Comprehensive flood protection, however, entails more than adequate coverage. A joint study from the U.S. Chamber of Commerce and Allstate found every dollar invested in disaster resilience can save up to $33 in avoided economic costs down the line. The study emphasized the need for collective action at all levels – individual, commercial, and government – to minimize climate and weather losses.

The NFIP’s Community Rating System (CRS) is one such collaboration, which rewards homeowners with premium discounts of up to 45 percent when their communities invest in floodplain management practices exceeding the organization’s minimum standards. By incentivizing improved building codes, citizen awareness campaigns, and other mitigation initiatives, the CRS can strengthen at-risk areas while offering relief where still needed after the cancellation of programs like FEMA’s Building Resilient Infrastructure and Communities (BRIC).

Though producing no U.S. landfalls for the first time in a decade, the 2025 Atlantic hurricane season generated deadly tropical storms, above-average days of major hurricane activity, and millions in economic losses, underscoring the enduring community preparedness required against this evolving peril.

Among the five hurricanes that did form, four reached Category 3 strength or higher, including three Category 5 storms – marking only the second year on record that more than two such storms occurred in the Atlantic. A new Triple-I Issues Brief examines their impacts and how they align with emerging climate and weather trends, particularly within inland areas hit by flooding from remnants of the storms.

Flood exposure spreads inland

While not to the scale of U.S. hurricanes in 2024, the year’s tropical storms were similarly destructive, with remnant moisture from Tropical Storm Chantal contributing to $500 million in damage, Gallagher Re estimates. In many affected North Carolina counties, less than 1 percent of households were covered by the National Flood Insurance Program (NFIP), highlighting a growing flood protection gap in areas once considered low-risk.

Demographic shifts also play a crucial role in the devastation as more people move into harm’s way and build their homes bigger and more expensive than before. While various flood-prone areas along the coasts lost more residents than they gained in 2024 – for the first time since 2019 – it is critical to remind home and business owners about rising flood risks throughout the country and the importance of staying protected.

Stronger, wetter weather

Warming oceans also fuel “rapid intensification,” or an increase in maximum sustained winds by at least 35 mph in a 24-hour period. Since 1980, over 80 percent of landfalling U.S. hurricanes – altogether costing at least $5 billion in damages – underwent rapid intensification at some point during their lifecycle, according to a 2025 American Geophysical Union (AGU) study.

Describing rapid intensification events as “a pronounced increasing trend,” AGU study coauthor Dr. Phil Klotzbach – a senior research scientist in the Department of Atmospheric Science at Colorado State University and Triple-I non-resident scholar – said such storms “tend to weaken at a slower rate as they move inland,” compounding challenges for residents who “aren’t necessarily as prepared as they should be.”

Hurricane Melissa – 2025’s strongest and deadliest storm – showcased the toll from this mounting intensity. Claiming more than 100 lives across the Caribbean, Melissa rapidly intensified before hitting Jamaica as a Category 5 hurricane, becoming one of the fastest-intensifying Atlantic storms ever recorded and the most powerful hurricane to make landfall in the country’s history.

Cutting-edge analytics

As advances in computing power and data collection have improved traditional tools in recent years, forecasters and insurers have built up their arsenal to combat the unpredictability of climate and weather risks. For instance, barometric pressure – found both more accurate and easier to gauge than the wind speeds traditionally used to predict storm damage – served as the primary trigger for a $150 million parametric policy for Jamaica which paid out in full after Hurricane Melissa.

“Displaying the kind of predictive power that can help insurers price risk and mitigate costly claims, these technologies can inform conversations at all levels to encourage investment in resilience,” the brief states.

A climate nonprofit plans to revive a key federal database tracking billion-dollar weather and climate disasters that the Trump Administration stopped updating in May, Bloomberg reported.

The database captures the financial toll of increasingly intense weather events and was used by insurers and others to understand, model, and predict weather perils across the United States. Dr. Adam B. Smith, the former NOAA climatologist who spearheaded the database for more than a decade, has been hired to manage it for the nonprofit, Climate Central.

NOAA in May announced it would stop tracking the cost of the country’s most expensive disasters, those which cause at least $1 billion in damage – a move that would leave insurers, researchers, and government policymakers with less reliable information to help understand the patterns of major disasters like hurricanes, drought or wildfires, and their economic consequences.

Climate Central plans to expand beyond the database’s original scope by tracking disasters as small as $100 million and calculating losses from individual wildfires, rather than simply reporting seasonal regional totals.

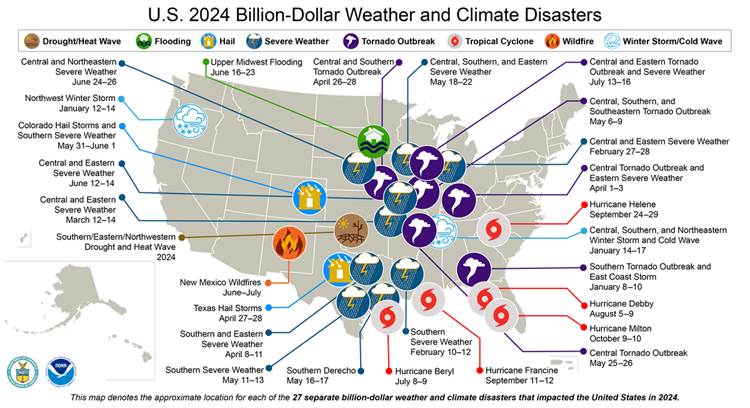

A record 28 billion-dollar disasters hit the United States in 2023, including a drought that caused $14.8 billion in damages. In 2024, 27 incidents of that scale occurred. Since 1980, an average of nine such events have struck in the United States annually.

This summer – amid deadly wildfires and floods – the Trump Administration has appeared to be rolling back some of its DOGE-driven NOAA funding cuts. NOAA recently announced that it would be hiring 450 meteorologists, hydrologists, and radar technicians for the National Weather Service (NWS), after having terminated over 550 such positions in the already-understaffed agency in the spring.

In addition, the administration’s announced termination of the Building Resilient Infrastructure and Communities (BRIC) program — run by the Federal Emergency Management Agency (FEMA) — has been held up by a court injunction while legislators debate its future. Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters.

Regarding the rescue of the NOAA dataset, Colorado State University researcher and Triple-I non-resident scholar Dr. Phil Klotzbach said, “The billion-dollar disaster dataset is important for those of us working to better understand the impacts of tropical cyclones. It uses a consistent methodology to estimate damage caused by natural disasters from 1980 to the present and was a critical input to our papers investigating the relationship between landfalling wind, pressure and damage. I’m very happy to hear that this dataset will continue!”

Devastating flooding in central Texas over the July 4, 2025, weekend highlighted several aspects of the state’s risk profile that also are relevant to the rest of the country, according to the latest Triple-I Issues Brief. One is the rising incidence of severe inland flooding related to tropical storms.

Tropical Storm Barry made landfall in Mexico on June 29 and weakened quickly, but its remnant moisture drifted northward into Texas, according to Dr. Phil Klotzbach, a research scientist in the Department of Atmospheric Science at Colorado State University and a Triple-I non-resident scholar.

“A slow-moving low-pressure area developed and helped bring up the moisture-rich air rom Barry and concentrated it over the Hill Country of central Texas,” Klotzbach said. “The soil was also extremely hard from prior drought conditions, which exacerbated the flash flooding that occurred.”

Such flooding far from landfall has become more frequent and severe in recent years. In Texas – as in much of the United States, particularly far from the coasts – few homeowners have flood insurance. Many believe flood damage is covered by their homeowners’ or renters’ insurance. Others believe the coverage is not worth buying if their mortgage lender doesn’t require it. In Kerr County, where much of the July 4 flooding took place, flood insurance take-up rates through the National Flood Insurance Program (NFIP) were 2.5 percent.

Convective storms, fires, and freezes

But tropical storms aren’t always the impetus for flooding. In July 2023, a series of intense thunderstorms resulted in heavy rainfall, deadly flash floods, and severe river flooding in eastern Kentucky and central Appalachia. The conditions that lead to such severe convective storms also are prevalent in Texas.

Severe convective storms are a growing source of losses for property/casualty insurers. According to Gallagher Re, severe convective storm events in 2023 and 2024 “have cost global insurers a remarkable US$143 billion, of which US$120 billion occurred in the U.S. alone.”

Given its aridity and winds, it should be no surprise that Texas is highly subject to wildfire – but the state also has been increasingly prone to severe winter storms and debilitating freezes. On Valentine’s Day 2021, snow fell across most of Texas, accumulating as temperatures stayed below freezing and precipitation continued through the night. A catastrophic failure of the state’s independent electric grid exacerbated these conditions as snow and ice shut down roads and many homes suffered pipe bursts and multiple days without power.

Texas’s 2021 experience illustrates how grid instability can act as a “risk multiplier” for natural disasters. The entire U.S. electric power grid is increasingly vulnerable as the infrastructure ages and proliferating AI data centers increase demand.

Need for data and collaboration

The severe damage and loss of life from the July 4 flooding have naturally raised the question of whether the Trump Administration’s reductions in National Weather Service staffing contributed to the high human cost of this event. While it is hard to say with certainty, these cuts have affected how NWS works – for example, in its use of weather balloons to monitor weather. As early as April, staffing data gathered by NWS indicated that field offices were “critically understaffed”.

In June, panelists at Triple-I’s Joint Industry Forum expressed concern about the impact of the federal cuts on weather monitoring and modeling, as well as programs to help communities adequately prepare for and recover from disasters. Triple-I has published extensively on the need for insurers to shift from exclusively focusing on repairing and replacing property to predicting events and preventing damage.

Collective action at all levels – individual, commercial, and government – is needed to mitigate risks, build resilience, and reduce fraud and legal system abuse. Triple-I and its members are committed to fostering such action and regularly provide data and analysis to inform the necessary conversations.

Recent developments in the atmosphere over the Caribbean Sea have led researchers at Colorado State University (CSU) to make slight improvements to their hurricane forecast for the 2025 Atlantic-basin season, in an update published Wednesday.

Triple-I non-resident scholar Phil Klotzbach, Ph.D., a senior research scientist in the Department of Atmospheric Science at CSU, and the CSU TC-RAMS research team are now predicting 16 total named storms through the end of the year, a small drop from their original forecast of 17.

“The primary reason for the slight decrease in our outlook is both observed and predicted high levels of Caribbean wind shear,” Klotzbach said. “High levels of Caribbean shear in June and July are typically associated with less active hurricane seasons.”

Klotzbach warned, however, that peak hurricane season – which typically occurs from mid-August through late October – could still be very active, despite current atmospheric conditions.

“The subtropical eastern Atlantic and portions of the tropical Atlantic are warmer than normal,” he said. “The current Atlantic sea surface temperature pattern is fairly similar to what we typically observe in July prior to active Atlantic hurricane seasons.”

Insurance industry executives and thought leaders gathered yesterday for Triple-I’s Joint Industry Forum (JIF) in Chicago to discuss the trends, economics, geopolitics, and policy influencing the market today, as well as ways to navigate these complexities while focusing on making their products affordable and available for consumers.

Triple-I CEO Sean Kevelighan in his opening remarks, noted that effective risk management depends on collaboration across stakeholder groups, as interconnected perils “present a community problem, not just an industry problem.”

JIF keynote speaker Louisiana Insurance Commissioner Tim Temple said facilitating community resilience planning is a top priority for the National Association of Insurance Commissioners (NAIC). The NAIC’s 2025 initiative – “Securing Tomorrow: Advancing State-Based Regulation” – aims to improve disaster mitigation and recovery by consolidating “the collective expertise of experienced state regulators from across the country, who can share real-time insights and proven strategies,” Temple said.

Among the initiative’s goals is aggregating more data from insurers to better understand challenges to affordability and availability on state levels, which the NAIC can then translate into actionable policy proposals. Such data calls, Temple said, help regulators, legislators, and policyholders focus on improving the cost drivers of insurance rates.

Louisiana has consistently been among the least affordable states for homeowners and auto insurance, according to the Insurance Research Council (IRC), in part because of its reputation for being plaintiff-friendly in civil litigation. Significant tort legislation has been approved in the state, but resistance to reform remains a challenge.

Getting to the roots of high premiums

After a recent data call in his home state, Temple told the JIF audience, “For the first time in Louisiana, we’re not talking about only premiums. We’re talking about why premiums are where they are.”

A critical lack of transparency surrounding cost drivers persists, however. Temple criticized the National Flood Insurance Program’s Risk Rating 2.0 reforms for not publicly disclosing more information “for individuals and communities to identify and address factors driving up their premiums,” such as “whether increased rates take into account levee systems, pump stations, and other things designed to help mitigate against floods.”

Conversely, government programs like Strengthen Alabama Homes – and the numerous programs it inspired, including in Louisiana – have demonstrated success in communicating the benefits of resilience investments for consumers and policymakers.

“We’re seeing major positive results after just a few short years,” Temple said, noting that, since early 2024, over 5,000 homeowners not chosen for Louisiana’s grant program still decided to invest in the same hazard mitigation, as they may still qualify for the corresponding state-mandated insurance discounts.

“As natural disasters become more frequent and severe, state regulators will continue to drive forward common-sense policies that protect consumers and ensure that insurance remains available and reliable for at-risk communities,” Temple concluded. Developing the database required for such policies is a necessary first step.

Keep an eye on the Triple-I Blog for further JIF coverage.

Established by Congress through the Disaster Recovery Reform Act of 2018, the BRIC program has allocated more than $5 billion for investment in mitigation projects to reduce economic losses from floods, wildfires, and other disasters for hundreds of communities. Ending BRIC will cancel all applications from 2020-2023 and rescind more than $185 million in grants intended for Louisiana, leaving the 34 submitted and accepted projects funded by those grants in limbo.

Whereas the FEMA press release described BRIC as “wasteful and ineffective,” Cassidy identified “not doing the program and then having to rescue communities when the inevitable flood occurs – that is waste, because we could have prevented that from happening in the first place.”

A 2024 study backed by the U.S. Chamber of Commerce supports this claim, which found that disaster mitigation investments save $13 in benefits for every dollar spent.

FEMA’s decision coincides with recovery efforts in Natchitoches, a small Louisiana city, after flash flooding inundated homes and downed power lines just weeks before. BRIC was set to fund improvements to the city’s backup generator system to pump out floodwater during severe weather.

Similarly, Lafourche Parish will lose $20 million to strengthen 16 miles of power lines, which Cassidy noted toppled “like dominos” during last year’s Hurricane Francine. Jefferson Parish residents displaced following Hurricane Ida in 2021 will lose the home elevation disaster grants they finally secured earlier this year.

“Louisiana was the third-largest recipient of BRIC’s most recent round of funding and is the largest recipient on a per capita basis,” Cassidy said. “Without BRIC, none of these projects would be possible.”

A national problem

Beyond Louisiana, Cassidy pointed to numerous states ravaged by severe storms so far this year, particularly inland communities where flooding is traditionally unexpected. At least 25 people died amid a severe weather outbreak across the southern and midwestern U.S. last month, underscoring a growing need for resiliency planning in non-coastal areas.

BRIC is one of many programs facing sudden termination under the Trump Administration. Twenty-two states and the District of Columbia have filed a lawsuit demanding the federal government unfreeze essential funding, including BRIC grants. Though the administration is reportedly complying with a federal judge’s order blocking the freeze, the states involved claim funding remains inaccessible.

Louisiana has not joined the lawsuit, but Cassidy emphasized the congressional appropriation of the program and requested the fulfillment of preexisting BRIC applications. He argued that “to do anything other than use that money to fund flood mitigation projects is to thwart the will of Congress.”

As President Trump weighs disbanding FEMA entirely – even as FEMA responds to record-breaking numbers of billion-dollar disasters – it is imperative to recognize the vast co-beneficiary benefits of disaster resilience, and develop our partnerships across these stakeholder groups.

The Institutes’ Pete Miller and Francis Bouchard of Marsh McLennan discuss how AI is transforming property/casualty insurance as the industry attacks theclimate crisis.

“Climate” is not a popular word in Washington, D.C., today, so it would take a certain audacity to hold an event whose title prominently includes it in the heart of the U.S. Capitol.

For two days, expert panels at the Ronald Reagan Building and International Trade Center discussed climate-related risks – from flood, wind, and wildfire to extreme heat and cold – and the role of technology in mitigating and building resilience against them. Given the human and financial costs associated with climate risks, it was appropriate to see the property/casualty insurance industry strongly represented.

Peter Miller, CEO of The Institutes, was on hand to talk about the transformative power of AI for insurers, and Triple-I President and CEO Sean Kevelighan discussed – among other things – the collaborative work his organization and its insurance industry members are doing in partnership with governments, non-profits, and others to promote investment in climate resilience. Triple-I is an affiliate of the Institutes.

Sean Kevelighan of Triple-I and Denise Garth, Majesco’s chief strategy officer, discuss how to ensure equitable coverage against climate events.

You can get an idea of the scope and depth of these panels by looking at the agenda, which included titles like:

Building Climate-Resilient Futures: Innovations in Insurance, Finance, and Real Estate;

Fire, Flood, and Wind: Harnessing the Power of Advanced Data-Driven Technology for Climate Resilience;

The Role of Technology and Innovation to Advance Climate Resilience Across our Cities, States and Communities;

Pioneers of Parametric: Navigating Risks with Parametric Insurance Innovations;

Climate in the Crosshairs: How Reinsurers and Investors are Redefining Risk; and

Safeguarding Tomorrow: The Regulator’s Role in Climate Resilience.

As expected, the panels and “fireside chats” went deep into the role of technology; but the importance of partnership, collaboration, and investment across stakeholder groups was a dominant theme for all participants. Coming as the Trump Administration takes such steps as eliminating FEMA’s Building Resilient Infrastructure and Communities (BRIC) program; slashing budgets of federal entities like the National Oceanographic and Atmospheric Administration (NOAA) and the National Weather Service (NWS); and revoking FEMA funding for communities still recovering from last year’s devastation from Hurricane Helene, these discussions were, to say the least, timely.

Helge Joergensen, co-founder and CEO of 7Analytics, talks about using granular data to assess and address flood risk.

In addition to the panels, the event featured a series of “Shark Tank”-style presentations by Insurtechs that got to pitch their products and services to the audience of approximately 500 attendees. A Triple-I member – Norway-based 7Analytics, a provider of granular flood and landslide data – won the competition.

Earth Day 2025 is a good time to recognize organizations that are working hard and investing in climate-risk mitigation and resilience – and to recommit to these efforts for the coming years. What better place to do so than walking distance from both the White House and the Capitol?

The Trump Administration’s unwinding of the Building Resilient Infrastructure and Communities (BRIC) program and cancellation of all BRIC applications from fiscal years 2020-2023 reinforce the need for collaboration among state and local government and private-sector stakeholders in climate resilience investment.

Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters. FEMA announced on April 4 that it is ending BRIC .

Chad Berginnis, executive director of the Association of State Floodplain Managers (ASFPM), called the decision “beyond reckless.”

“Although ASFPM has had some qualms about how FEMA’s BRIC program was implemented, it was still a cornerstone of our nation’s hazard mitigation strategy, and the agency has worked to make improvements each year,” Berginnis said. “Eliminating it entirely — mid-award cycle, no less — defies common sense.”

While the FEMA press release called BRIC a “wasteful, politicized grant program,” Berginnis said investments in hazard mitigation programs “are the opposite of ‘wasteful.’ “ He pointed to a study by the National Institute of Building Sciences (NIBS) that showed flood hazard mitigation investments return up to $8 in benefits for every $1 spent.

“At this very moment, when states like Arkansas, Kentucky, and Tennessee are grappling with major flooding, the Administration’s decision to walk away from BRIC is hard to understand,” Berginnis said.

Heading into hurricane season

Especially hard hit will be catastrophe-prone Florida. Nearly $300 million in federal aid meant to help protect communities from flooding, hurricanes, and other natural disasters has been frozen since President Trump took office in January, according to an article in Government Technology.

The loss of BRIC funding leaves dozens of Florida projects in limbo, from a plan to raise roads in St. Augustine to a $150 million effort to strengthen canals in South Florida. According to Government Technology, the agency most impacted is the South Florida Water Management District, responsible for maintaining water quality, controlling the water supply, ecosystem restoration and flood control in a 16-county area that runs from Orlando south to the Keys.

“The district received only $6 million of its $150 million grant before the program was canceled,” the article said. “The money was intended to help build three structures on canals and basins in North Miami -Dade and Broward counties to improve flood mitigation.”

Florida’s Division of Emergency Management must return $36.9 million in BRIC money that was earmarked for management costs and technical assistance. Jacksonville will lose $24.9 million targeted to raise roads and make improvements to a water reclamation facility.

FEMA announced the decision to end BRIC the day after Colorado State University’s (CSU) Department of Atmospheric Science released a forecast projecting an above-average Atlantic hurricane season for 2025. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach CSU research team forecasts 17 named storms, nine hurricanes – four of them “major” (Category 3, 4, or 5). A typical season has 14 named storms, seven hurricanes – three of them major.

Nationwide impacts

More than $280 million in federal funding for flood protection and climate resilience projects across New York City — “including critical upgrades in Central Harlem, East Elmhurst, and the South Street Seaport” – is now at risk, according to an article in AMNY. The cuts affect over $325 million in pending projects statewide and another $56 million of projects where work has already begun.

Senate Majority Leader Chuck Schumer and Gov. Kathy Hochul warned that the move jeopardizes public safety as climate-driven disasters become more frequent and severe.

“In the last few years, New Yorkers have faced hurricanes, tornadoes, blizzards, wildfires, and even an earthquake – and FEMA assistance has been critical to help us rebuild,” Hochul said. “Cutting funding for communities across New York is short-sighted and a massive risk to public safety.”

According to the National Association of Counties, cancellation of BRIC funding has several implications for counties, including paused or canceled projects, budget and planning adjustments, and reduced capacity for long-term risk reduction.

North Dakota, for example, has 10 projects that were authorized for federal funding. Those dollars will now be rescinded. Impacted projects include $7.1 million for a water intake project in Washburn; $7.8 million for a regional wastewater treatment project in Lincoln; and $1.9 million for a wastewater lagoon project in Fessenden.

“This is devastating for our community,” said Tammy Roehrich, emergency manager for Wells County. “Two million dollars to a little community of 450 people is huge.”

The cancellation of BRIC roughly coincides with FEMA’s decision to deny North Carolina’s request to continue matching 100 percent of the state’s spending on Hurricane Helene recovery.

“The need in western North Carolina remains immense — people need debris removed, homes rebuilt, and roads restored,” said Gov. Josh Stein. “Six months later, the people of western North Carolina are working hard to get back on their feet; they need FEMA to help them get the job done.”

Resilience key to insurance availability

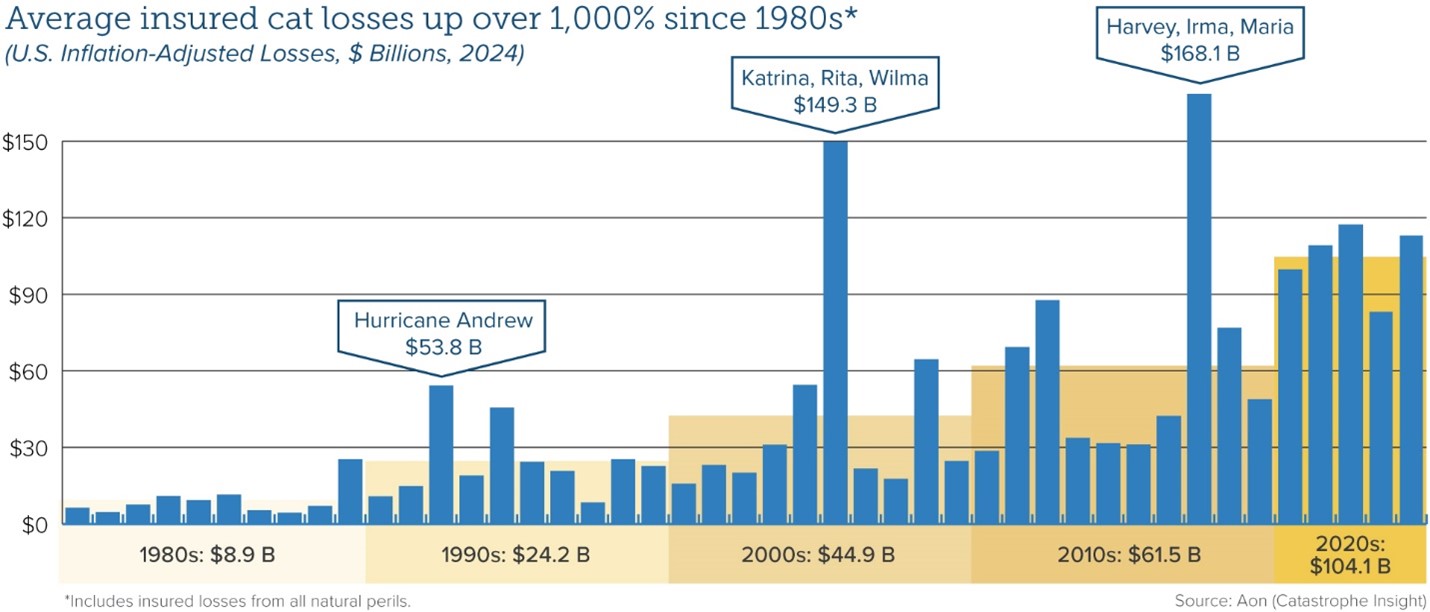

Average insured catastrophe losses have been on the rise for decades, reflecting a combination of climate-related factors and demographic trends as more people have moved into harm’s way.

“Investing in the resilience of homes, businesses, and communities is the most proactive strategy to reducing the damage caused by climate,” said Triple-I Chief Insurance Officer Dale Porfilio. “Defunding federal resilience grants will slow the essential investments being made by communities across the U.S.”

Flood is a particularly pressing problem, as 90 percent of natural disasters involve flooding, according to the National Flood Insurance Program (NFIP). The devastation wrought by Hurricane Helene in 2024 across a 500-mile swath of the U.S. Southeast – including Florida, Georgia, the Carolinas, Virginia, and Tennessee – highlighted the growing vulnerability of inland areas to flooding from both tropical and severe convective storms, as well as the scale of the flood-protection gap in non-coastal areas.

Coastal flooding in the U.S. now occurs three times more frequently than 30 years ago, and this acceleration shows no signs of slowing, according to recent research. By 2050, flood frequency is projected to increase tenfold compared to current levels, driven by rising sea levels that push tides and storm surges higher and further inland.

In addition to the movement of more people and property into harm’s way, climate-related risks are exacerbated by inflation (which drives up the cost of repairing and replacing damaged property); legal system abuse, (which delays claim settlements and drives up insurance premium rates); and antiquated regulations (like California’s Proposition 103) that discourage insurers from writing business in the states subject to them.

Thanks to the engagement and collaboration of a range of stakeholders, some of these factors in some states are being addressed. Others – for example, improved building and zoning codes that could help reduce losses and improve insurance affordability – have met persistent local resistance.

As frequently reported on this blog, the property/casualty insurance industry has been working hard with governments, communities, businesses, and others to address the causes of high costs and the insurance affordability and availability challenges that flow from them. Triple-I, its members, and partners are involved in several of these efforts, which we’ll be reporting on here as they progress.

The efficacy of collaboration and investment by “co-beneficiaries” in resilience initiatives was a dominant theme throughout Triple-I’s 2024 Joint Industry Forum – particularly in the final panel, which celebrated leaders behind recent real-world impacts of such investments.

Moderated by Dan Kaniewski, Marsh McLennan (MMC) managing director for public sector, the panelists discussed how their multi-industry backgrounds inform their innovative mindsets, as well as their knowledge on the profound ripple effects of targeted resilience planning.

The panel included:

Jonathan Gonzalez, co-founder and CEO of Raincoat;

Bob Marshall, co-founder and CEO of Whisker Labs;

Dawn Miller, chief commercial officer of Lloyd’s and CEO of Lloyd’s Americas; and

Lars Powell, director of the Alabama Center for Insurance Information and Research (ACIIR) at the University of Alabama and a Triple-I Non-Resident Scholar.

Productive partnership

Kaniewski – who spent most of his career in emergency management, previously serving as the second-ranking official at the Federal Emergency Management Agency (FEMA) and the agency’s first deputy administrator for resilience – kicked off the panel by raising the question “how do we define success?”

He characterized success as “putting theory into practice” and “having elected officials taking steps to reduce risk and transfer some of this risk from federal, state, or local taxpayers.”

But, as participants in earlier panels and this one made clear, government efforts can only go so far without private-sector collaboration.

“It doesn’t matter who makes that investment, whether it’s the homeowner, the business owner, or the government,” Kaniewski explained. “The reality is we all benefit from that one investment. If we can acknowledge that we benefit from those investments, we should do our best to incentivize them.”

Kaniewski and Raincoat’s Gonzalez were both integral in the development of community-based catastrophe insurance (CBCI), developed in the wake of Superstorm Sandy in 2012.

“A lot of the neighborhoods that experienced flooding due to Sandy didn’t have access to insurance prior to the flooding – and then, post flooding, the government really had to step up to figure out how to keep those families in those houses,” Gonzalez said.

In collaboration with the city, a nonprofit called the Center for NYC Neighborhoods developed the concept of buying parametric insurance on behalf of these communities, with any payouts going toward helping families stay in their homes after disasters. Unlike traditional indemnity insurance, a parametric policy pays out if certain agreed-upon conditions are met – for example, a specific wind speed or earthquake magnitude in a particular area – regardless of damage. Parametric insurance eliminates the need for time-consuming claim adjustment. Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders.

In this case, Kaniewski said, success was reflected in the fact that the pilot program received sufficient funding not only for renewal but expansion, bringing needed protection to even more vulnerable communities.

Powell reinforced this sentiment in explaining ACIIR’s research on the FORTIFIED method, a set of voluntary construction standards created by the Insurance Institute for Business and Home Safety (IBHS) for durability against severe weather. The insurance industry-funded Strengthen Alabama Homes program issues grants and substantial insurance premium discounts to homeowners to retrofit their houses along these guidelines, prompting multiple states to replicate the program.

Such homes in Alabama sustained 54 to 76 percent reduced loss frequency from Hurricane Sally compared to standard homes, Powell reported, and an estimated 65 to 73 percent could have been saved in claims if standard homes were FORTIFIED.

Incentivizing contractors to learn FORTIFIED standards was especially critical, Powell explained, because they further advertised these skills and expanded the presence of FORTIFIED homes beyond the grant program.

“A lot of companies have said for several years, ‘we don’t know if we’re comfortable writing these…we haven’t seen it on the ground,’” Powell said. “Well, now we’ve seen it on the ground. We need to have houses that don’t burn down or blow over. We know how to do it, it’s not that expensive.”

Addressing concerns to drive adoption

Miller described how Lloyd’s Lab works to ease that discomfort by creating a space for businesses to nurture and integrate novel insights and products without fear. With mentor support, companies are encouraged to test new ideas while free from the usual degree of financial and/or intellectual property risks attached to innovation investments.

“It’s about having an avenue out to try,” Miller said. “Having that courage, as we continue to work together, to try to understand what’s working, what’s not, and being brave to say, ‘this isn’t working, but we can course correct.’”

Whisker Labs’ Marshall noted that numerous insurance carriers have taken a chance on his company’s front-line disaster mitigation devices, Ting, by paying for and distributing them to their customers.

Ting plug-in sensors detect conditions that could lead to electrical fires through continuous monitoring of a home’s electrical system. Statistically preventing more than 80 percent of electrical fires, communities benefit – not only by preventing individual home fires but also by providing data about the electrical grid and potentially heading off grid-initiated wildfires.

“There are so many applications for the data,” Marshall said, but “to have a true impact on society…we have to prove that we’re preventing more losses than the cost, and we have to do that in partnership with insurance carriers.”

Everyone wins if everyone plays

Cultivating innovative solutions is pivotal to enhancing resilience, the panelists agreed – but driving them forward requires more than just the insurance industry’s support.

He pointed to a project last year – funded by Fannie Mae and developed by the National Institute of Building Science (NIBS) – that culminated in a roadmap for resilience investment incentives, focusing on urban flooding.

The co-authors of the project, including Triple-I subject-matter experts, represented a cross-section of “co-beneficiary” groups, such as the insurance, finance, and real estate industries and all levels of government, Kaniewski said.

Implementation of the roadmap requires participation from communities and multiple co-beneficiaries. Triple-I and NIBS are exploring such collaborations with potential co-beneficiaries in several areas of the United States.