The global digital payments landscape, projected to hit $16.6 trillion by 2028, is grappling with a surge in security breaches and scams, with U.S. consumers reporting losses of $1.8 billion due to bank transfer and payment scams in 2023 alone, according to a new report from Chubb.

Despite widespread adoption, only one in three users fully trust digital payment technologies, underscoring the need for enhanced security measures and consumer education, the report found.

Concerns about security of digital payments creates an opportunity for insurers to provide personal cyber coverage that offers consumers greater peace of mind, the report noted.

“In this dynamic environment, insurance plays a pivotal role in fostering trust and enabling the continued growth of the digital payments ecosystem. By providing protection against financial losses resulting from cyber scams, technology malfunctions and data breaches, insurance empowers individuals and businesses to embrace digital payments with confidence,” said Sean Ringsted, chief digital business officer of Chubb.

The Growth and Risks of Digital Payments

The total transaction value of digital payments is projected to be $11.6 trillion in 2024, with continued growth expected at a 9.5% annual rate through 2028, according to Chubb. This underscores the magnitude of the shift toward digital payments globally.

In the U.S. alone, the number of noncash payments, excluding checks, has increased more than 500% between 2000 and 2021, according to the Federal Reserve System. Digital wallets are projected to account for more than $25 trillion in global transaction value, or 49% of all online and point-of-sale sales combined, by 2027.

As reliance on digital payment technologies grows, so does the prevalence of security breaches and scams, Chubb warned.

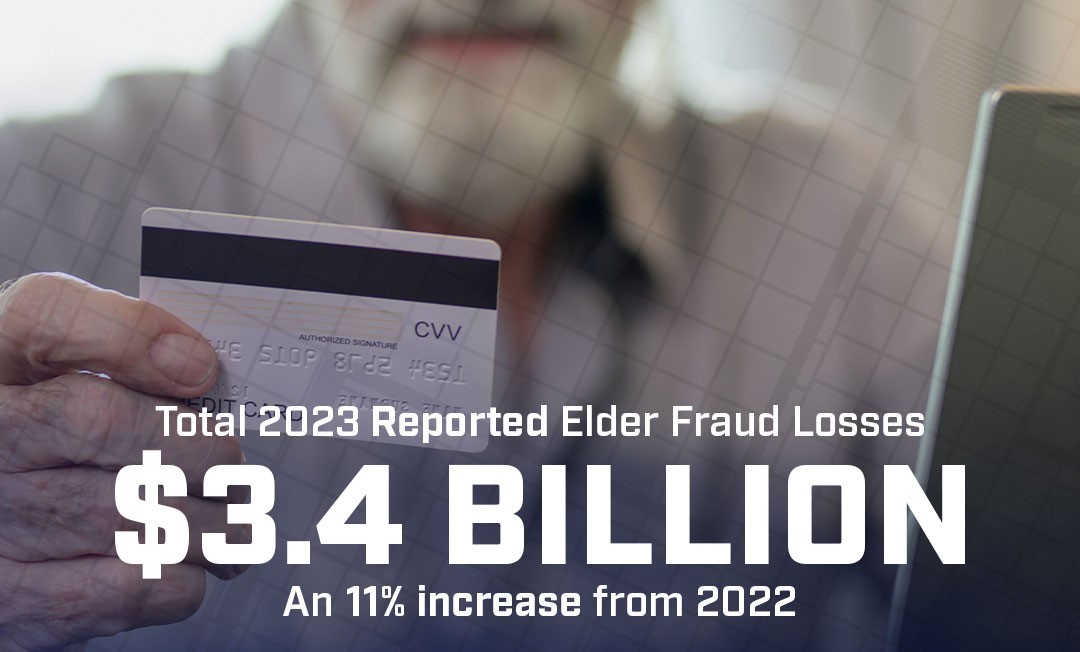

Data compromise incidents involving financial institutions increased by more than 330% from 2019 to 2023. In 2023, U.S. consumers reported losing $1.8 billion due to scams involving bank transfers and payments. The three largest banks that offer the Zelle payment network rejected scam disputes worth approximately $560 million from 2021 to 2023, according to a U.S. Senate Subcommittee analysis.

Businesses are also feeling the financial pain, with merchant losses due to online payment fraud predicted to surpass $362 billion globally between 2023 and 2028. Juniper Research anticipates $91 billion in losses in 2028 alone.

“From the U.S. perspective, the survey results suggest that some consumers have been lulled into a false sense of security around digital payments,” said Robert Poliseno, president of North America Digital Insurance at Chubb. “To protect all consumers, key ecosystem participants — including financial institutions, merchants and insurers — should educate users about potential risks, including the diverse range of cyber scams, and emphasize protective measures, such as adopting secure digital practices, raising awareness of common pitfalls and utilizing various forms of available risk transfer products-like insurance.”

The Trust Gap in Digital Payments

Despite widespread adoption, trust in digital payment technologies is relatively low, according to the survey. Nearly one-third of respondents globally lack confidence in digital payment providers’ security measures. Concerns about the adequacy of customer support (36%) and confidentiality (29%) are also among the main impediments to full trust, the survey found.

The possibility of being scammed is a leading barrier to fully trusting digital payments. Globally, 64% of respondents are very or quite concerned about cyber scams when using digital technology to transfer money, the survey found. In the U.S., 49% of respondents are very or quite concerned.

Most respondents concerned about cyber scams indicate that they have altered their behavior or reduced their usage of certain platforms: 61% globally, 60% in the U.S., 56% in Latin America and 65% in Asia.

The Role of Insurance in Promoting Trust and Adoption

A significant portion of digital payment users mistakenly believe they are protected against losses in various scenarios, such as technology malfunctions or data breaches. Younger respondents, frequent users, and those engaging in risky behaviors could be especially at risk of incorrectly assuming they have automatic protection.

However, the Chubb survey found that actual usage of insurance is relatively low — only 16% globally have personal cyber scam or fraud insurance, while 23% have payment protection insurance.

The presence of transaction insurance plays a critical role in increasing users’ trust in digital payment technologies, Chubb reported. Holding such insurance significantly boosts confidence for three-quarters of consumers.

Consumers are willing to pay for this peace of mind, Chubb found, with the highest proportion willing to spend 6% or more of the transaction amount on insurance.

View the full report here.