By Max Dorfman, Research Writer, Triple-I

The property/casualty insurance industry is expected to achieve underwriting profitability in 2025, according to the latest research from the Triple-I and Milliman, a collaborating partner. The report, Insurance Economics and Underwriting Projections: A Forward View, which was presented at a members-only webinar on July 11, also projects a small underwriting loss in 2024.

Michel Léonard, Ph.D., CBE, chief economist and data scientist at Triple-I, discussed how P/C replacement costs continue to increase more slowly than overall inflation.

“For the last 12 months, economic drivers of insurance performance have been favorable to the industry, with P/C insurance’s underlying growth catching up to overall U.S. economic growth rates, and its replacement costs increasing at a sluggish pace compared to overall inflation,” Dr. Léonard said. “We expected this favorable window to last into 2025.”

That may not be the case anymore for two reasons, according to Léonard.

“First, U.S. economic growth slowed more than expected in Q1 2024, largely because of the Fed’s lack of clarity about the timing of interest rate cuts,” he said. “Second, global supply chains are again showing stress due to ongoing and increasing geopolitical risk, such as the tensions in and around the Suez Canal. These causes may be threatening to send inflation back toward pandemic-era levels. Geopolitical risk never left, and supply chains are on a lifeline.”

Dale Porfilio, FCAS, MAAA, Triple-I’s chief insurance officer, discussed the split between personal and commercial lines, noting that, “The ongoing performance gap between personal and commercial lines remains, but that gap is closing.”

“This quarter, we are projecting commercial lines underwriting results to outperform personal lines premium growth by over five points in 2024,” Porfilio added. “The difference, in large part, illustrates how regulatory scrutiny on personal lines has curbed the ability for insurers to increase prices to reflect the significant amount of inflation that impacted replacement costs through and coming out of COVID.”

Jason B. Kurtz, FCAS, MAAA, a principal and consulting actuary at Milliman – a global consulting and actuarial firm – points out how commercial multi-peril is one line that continues to face long-term challenges.

“While the expected net combined ratio of 106.2 is one point better than 2023, matching the eight-year average, the line has not been profitable since 2015. And with a Q1 direct incurred loss ratio of 52 percent and premium growth rates continuing to slow, we see some improvement but continuing unprofitability through 2026,” Kurtz said.

In juxtaposition, Kurtz pointed out the continuing robust performance of workers’ compensation.

“The expected 90.3 net combined ratio is nearly a one-point improvement from prior estimates and would mark 10 consecutive years of profitability for workers’ comp,” he said. “We continue to forecast favorable underwriting results through 2026.”

“Medical costs are going up, but they have not experienced the same type of inflation as the broader economy,” added Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance (NCCI). NCCI produces the Medical Inflation Insights report, which provides detailed information specific to workers’ compensation on a quarterly basis. “Since 2015, both workers’ compensation severity and medical inflation, as measured by NCCI’s Workers’ Compensation Weighted Medical Price index, have grown at a similar rate, a quite moderate 2 percent per year.”

Other highlights of the report include:

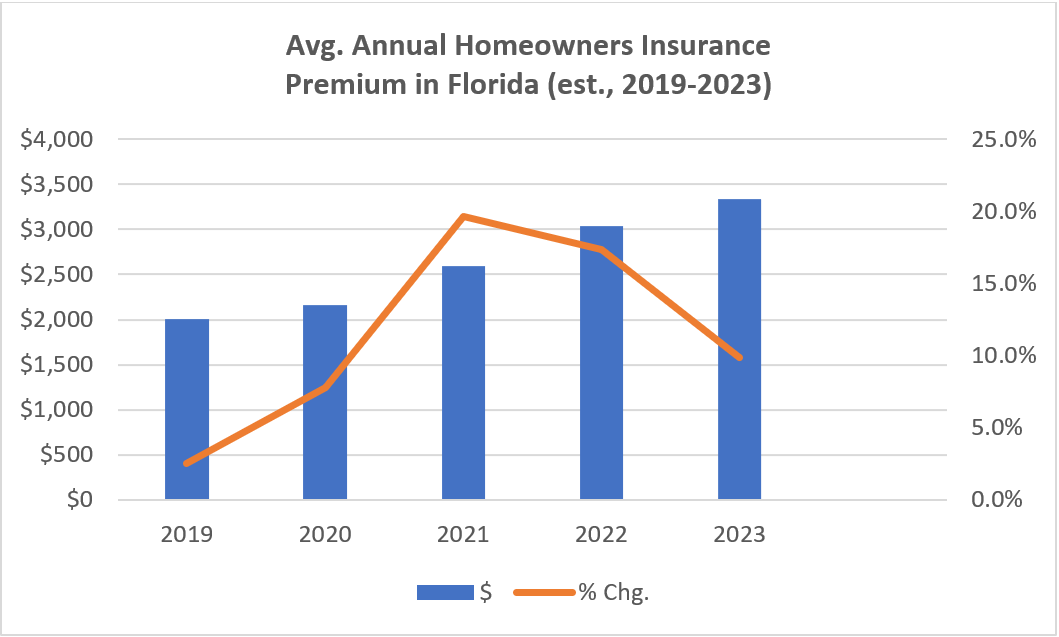

- Homeowners insurance underwriting losses expected to continue for 2024-2025, but the line is expected to become profitable in 2026, with continued double-digit net written premium growth for 2024-2025.

- Personal auto net combined ratio improved slightly from prior estimates and is on track to achieve profitability in 2025.

- Commercial lines 2024 net combined ratio remained unchanged despite shifts in commercial property (-1 point), workers’ compensation (-1 point), and general liability (+1 point).

- Net written premium growth rate for personal lines is expected to continue to surpass commercial lines by over 8 percentage points in 2024.