Hosted by Triple-I Chief Economist and Data Scientist Dr. Michel Léonard, PhD, CBE, the series equips listeners with insights to manage economic uncertainty at the intersection of economics and insurance. It features interviews with insurance practitioners, technologists, academics, educators, analysts, and economists from various industries who discuss their perspectives and how they integrate economic trends and developments into their day-to-day responsibilities.

Early episodes include discussions with:

Jennifer Kyung, Chief Underwriting Officer at USAA,

Ken Simonson, Chief Economist of the Associated General Contractors of America,

Dale Porfilio, Triple-I Chief Insurance Officer,

Sean Kevelighan, Triple-I CEO, and

Pete Miller, President and CEO at The Institutes.

Dr. Léonard brings more than 20 years’ expertise in senior and leadership positions as Chief Economist for Trade Credit and Political Risk at Aon; Chief Economist at JLT; Chief Economist and Data Scientist at Alliant; and Chief Data Scientist at MaKro. He also is adjunct faculty in New York University’s Economics Department.

Several metrics that influence auto insurance premium rates are starting to improve, but it will take time for these improvements to be reflected in flattening rates, according to a recent Triple-I Issues Brief.

Direct premiums written and underwriting profitability improved dramatically in 2023. Additionally, 2023 net written premium growth of 14.3 percent is the highest in over 15 years. These are great gains, but it’s important to remember that they come on top of results in 2022 that were the worst in recent years.

The number of drivers on the road and miles driven have returned to pre-pandemic levels – but the risky driving behaviors that led to high losses during the pandemic have not improved. More accidents with severe injuries and fatalities have driven up claims and losses in terms of both vehicle damage and liability, while attracting greater attorney involvement and legal system abuse. Compounding these conditions has been historically high inflation, which puts upward pressure on the material and labor costs, increasing the cost of claims.

Telematics technologies, which allow insurers to analyze risk profiles and tailor rates based on individual driving habits, offer the possibility of some relief. By providing feedback that can influence driving behavior, telematics has been shown to lower risk and help reduce the cost of insurance. An Insurance Research Council survey found 45 percent of drivers said they made significant safety-related changes in how they drove after participating in a telematics program. Another 35 percent said they made small changes.

But broader risk and economic factors are likely to keep premium rates high in most cases for the foreseeable future.

William Nibbelin, Senior Research Actuary, Triple-I

The recent National Council on Compensation Insurance (NCCI) Annual Insights Symposium (AIS) in Orlando, Fla., provided important context and clarity around the state of the workers compensation line of business. As a new senior research actuary for Triple-I, my prior knowledge of this line could best be summarized by the following words from one peer-reviewed study of a reserving project I conducted more than two decades ago: Long-tail, unprofitable.

I recently assumed responsibility for forecast modeling of the property/casualty industry, which includes workers comp. In this role, I’d seen the line’s 2023 net combined ratio at 87 – the lowest (ie., most profitable) in the past five years. But I did not yet have deep understanding of the underlying trends driving these numbers.

I saw the AIS as an opportunity to gain that knowledge, and the event delivered.

The net combined ratio of 87 – as reported by Triple-I using National Association of Insurance Commissioners (NAIC) data sourced by S&P Global Market Intelligence – was also the ninth straight calendar year in a row under 100. According to NCCI, the success of the workers comp line in recent years represents the convergence of three factors:

Payroll increases

Moderate severity increases, and

Larger-than-expected frequency declines.

“The overall numbers for workers compensation show a financially healthy system,” said Donna Glenn, NCCI’s chief actuary.

Payroll increases

The line’s 2023 direct written premium (DWP) increased 2.6 percent nationally – due primarily to another strong year of payroll growth at 6.2 percent, according to NCCI.Rising wages contributed the most to that figure, with increases in all industry sectors resulting in a combined wage growth of 3.9 percent. Improved job creation contributed 2.3 percent, with all sectors except transportation and warehousing seeing increased employment. Payroll growth was partially offset by state-approved premium rate decreases.

Moderate severity increases

Claim severity remains moderate year over year, at 3 percent in 2023, despite indemnity claim severity at 5 percent. Medical claim severity for 2023 trended at a low 2 percent, in line with the 20-year trend of 1.8 percent and below the 3.5 percent in 2022. Medical claims less than $500,000 increased 5 percent; however, claims above $500,000 decreased 16 percent, driven primarily by several large losses in 2022.

Also, more states have adopted physician medical fee schedules from 2012 to 2022, which has shifted medical cost category shares from more expensive inpatient claims to outpatient claims, as well as lower drug claims. Outpatient claims increased from 23 percent of all claims to 27 percent and drug claims decreased from 12 percent to 7 percent of all claims.

Larger-than-expected frequency declines

Overall claim frequency decreased 8 percent in 2023, compared to the 20-year average decrease of 3.4 percent. Workers compensation claims frequency has only increased twice in the past 20 years – once in 2010 from the destabilization in the construction sector in 2009 and again in 2021 from COVID-19 impacts in 2020.

From 2015 to 2022, workers comp claims frequency benefited from workplace safety improvements and technology advances, which helped the decline in all cause of injury categories, including the two largest shares of strain and slip/falls. During this same period, the largest decline in claim frequency by part of the body was in lower-back claims. Finally, the recent slowing employment market churn has also improved claim frequency as claims decline when job tenure rises.

Stephen Cooper, senior economist at NCCI, speaking on the state of the economy and its impact on workers comp, said job growth and steadily increasing wage rates continue to favor the workers compensation system. He also gave an overview of the contribution to labor force by age and generation from 1980 to 2030, including changes in claim share from 2020 actuals to 2030 forecasts. Overall, the double-digit growth in labor force of 24 percent in 2000 over 1980 and 18 percent in 2020 over 2000 is expected to fall to only 4 percent in 2030 over 2020.

The only age group with an expected increasing contribution to the labor force from 2020 to 2030 are those age 65 and older. The contribution to labor force for the age group 16 to 24 is expected to remain flat from 2020 to 2030 however their representative share of Workers Compensation claims has the largest expected increase from 9% to 11 percent.

Beyond the numbers

The symposium provided valuable insight into several factors affecting workers comp, including the role of AI and innovation in workplace safety technology. In a panel moderated by Damian England, NCCI’s executive director of affiliate services, the audience got to see a demonstration of AI camera monitoring of warehouse employee activity and the use of wearable technology to highlight improper lifting techniques.

“It is clear that safety technologies will be a vital part of future safety initiatives,” England said. “They may even be a gamechanger for evaluating and improving workplaces and reducing injuries.”

AIS also touched on challenges facing today’s workers, from climate to mental health.

“Our new NCCI research shows worker injuries increase by as much as 10 percent on very hot days, as well as on wet and freezing days, compared to mild weather,” said Patrick Coate, NCCI senior economist. “High temperatures impact construction and other outdoor workers most, while cold and wet weather leads to a lot more slip and fall injuries.”

Anae Myers, assistant actuary at NCCI, focused on the difference between claims that include mental health diagnosis versus those that do not.

“New research from NCCI shows that claims exceeding $500,000 are 12 times more likely to be diagnosed with an associated mental condition during the course of treatment, underscoring the potential for the impact of mental health in large claims,” Myers said.

I left the conference with a better understanding of workers comp rate making and the indices to track for future forecasts. Many thanks to Cristine Pike and Madison White at NCCI for their hospitality and guidance, as well as to all the attendees who patiently provided their expertise and generously offered their support when I introduced myself to them and to this stunning line of insurance.

An annual report on securities class actions from Cornerstone Research indicates the median settlement amount increased 11%, and the proportion of settlements of at least $100 million climbed to nearly two-thirds of the total settlement dollars in 2023.

Research from Westfleet Advisors focused on third-party litigation funding (TPLF) for US commercial litigation suggests the David versus Goliath narrative surrounding the early years of the market is growing tenuous. The overall percentage of commitments allocated to Big Law continues to increase, from 28% in 2022 to 35% in 2023.

These and other persistent upward trends in litigation, settlement, and other legal costs continue to have implications for insurers, the policyholders they serve, and, ultimately, consumer prices.

Mega settlements and institutional investors as lead plaintiffs are increasing.

Cornerstone reports that despite a more than 20% decline in the number of settlements, total settlement dollars remained approximately the same, standing at little over half of the 2016 peak.

There were 83 securities class action settlements in 2023, with an approximate total value of $3.9 billion, versus 105 settlements in 2022, totaling $4.0 billion. Other highlights in the 2023 data:

The median settlement amount of $15 million is the highest since 2010.

The nine “mega” settlements in 2023–the highest annual frequency since 2016–ranged from $102.5 million to $1 billion.

All of the mega settlements included an institutional investor as the lead plaintiff.

Only 6% of cases settled for less than $2 million, the lowest percentage since 2013.

Analysis indicates that settlements were also higher in cases involving certain factors: “accounting allegations, a corresponding SEC action, criminal charges, an accompanying derivative action, an institutional investor lead plaintiff, or securities.” Further, an increasing number of cases that settle at later stages involved an institutional lead plaintiff, continuing the trend from 2022.

Results also suggest that drawing out cases can amplify other factors, such as total assets and median “simplified tiered damages,” a Cornerstone term that refers to the model used to estimate settlement amounts. For both of these categories in 2023, median amounts for cases after class certification rulings were twice that of cases that settled before these rulings were made. However, in the five-year period from 2019 through 2023, over 90% of cases were settled before filing a motion for summary judgment.

Accompanying derivative actions are down.

Whereas a securities class action is filed on behalf of shareholders, a shareholder derivative action is typically brought by a shareholder on behalf of and (arguably) for the benefit of the company (usually against the company’s directors and/or officers). Derivative actions typically only happen in parallel with class action lawsuits, and the majority don’t result in monetary settlements (except for attorney fees). Instead, the plaintiff wins tend to center around measures for reforming corporate governance or operational controls.

Otherresearch from Cornerstone shows the probability of a monetary settlement for these lawsuits increases when the associated class action settlement is rather large. Also, historically, securities actions with accompanying derivative litigation tend to settle for higher amounts than those that don’t carry parallel derivative claims. Thus, Cornerstone also tracks the percentage of cases involving accompanying derivative actions. In 2023, the portion was 40%, the lowest since 2011.

New capital commitments decreased for commercial litigation TPLF, but claim monetization increased.

With a reported 39 active funders, 353 new deals, and $15.2 billion AUM, commercial litigation (versus consumer litigation) receives the majority of third-party litigation funding (TPLF). Investors target intellectual property, arbitration, business torts, contract breaches, and, of course, class action suits. These TPLF deals, also referred to as transactions or commitments, are arranged between funders and corporate litigants or law firms. Westfleet Advisors’ most recent market report on TPLF is the fifth edition, and it covers transactions from July 1, 2022, to June 30, 2023. Some noted exceptions and data adjustments are described in the report.

The report reveals that despite some funders leaving the market and a 14% decrease in new capital commitments, key data points remained close to amounts tracked for last year. For example, attorneys still make the majority of these deals with a 64% share of the agreements, in contrast to only 36% for clients. Patent litigation is still reaping the largest amount of funds for a single legal area, about 19% of new commitments. Figures for type of deal and average deal size also remain fairly stable.

However, some annual numbers have increased, highlighting an ongoing strategic shift in TPLF use. For the third year in a row, the report noted a rise in capital allocated for the monetization of claims, with 21% (versus 14% in 2022) going to new commitments. The biggest law firms (ranked in the AmLaw 200 according to gross revenue) have increased their use of TPLF, snagging 35% of the new deals. Arguably, both trends weaken the “David vs Goliath” narrative, and commercial TPLF may evolve to be less about helping scrappy firms and plaintiffs and more about extracting profits from litigation.

Drawn out litigation and more outsized settlements may have implications for insurance coverage.

Triple-I and other industry thought leaders define Legal System Abuse as policyholder or plaintiff attorney actions that unnecessarily increase the costs and time to settle insurance claims. Qualifying actions can arise from attorneys or clients drawing out litigation to reap a larger settlement simply because TPLF investors take such a giant piece of the settlement pie. As there is little transparency around the use of TPLF, insurers and courts have virtually no leeway in mitigating any of this risk.

Thus, as with other channels for potential legal system abuse, TPLF use is nearly impossible to forecast and mitigate. Increases in litigation and claim costs have threatened the affordability and availability of many other areas of insurance coverage. TPLF can impact product lines such as Directors and Officers (D&O) in commercial litigation via securities class actions. TPLF can produce a financially counterproductive effect for plaintiffs byextracting a disproportionate amount of value from settlements, weakening the primary purpose of a financial payout: to enable the claimant to restore losses.

Nonetheless, insurers seek to carefully manage these risks through underwriting practices, policy exclusions, and setting appropriate reserves to mitigate the financial impact. Meanwhile, Triple-I and various other stakeholders have called for a regulatory rein-in on TPLF to increase transparency. To keep abreast of the conversation, follow our blog and check out our regularly updated knowledge hub for Legal System Abuse.

Strong improvements in personal auto insurance results helped drive the U.S. property and casualty insurance industry to its second-highest net underwriting gain in any quarter since at least 2000, according to an S&P Global Market Intelligence analysis.

Just 12 months from its worst-on-record start to a calendar year – with a combined ratio of 102.2 – the industry generated a ratio of approximately 94.0. Combined ratio is a measure of underwriting profitability in which a ratio under 100 indicates a profit and one above 100 represents a loss.

While quarterly statutory data is insufficient to calculate combined ratios at the line-of-business level, S&P previously estimated that a direct incurred loss ratio of approximately 71.3 percent in the personal auto sector would have produced break-even underwriting results in the first quarter.

“Applying the same methodology to the first-quarter result of 66.7% yields an estimated combined ratio of 95.6,” S&P said. The industry’s full-year 2023 private auto combined ratio was 104.9.

On a consolidated basis across business lines, incurred losses increased only modestly, while net premiums earned continued to rise rapidly. This reflects the combination of continued top-line strength in many commercial lines of business and what S&P called “the hardest private auto pricing environment in 47 years.”

The industry also benefited from relatively mild catastrophe activity compared with the comparable prior-year period.

While these strong first-quarter results are noteworthy, it will take time to know whether they represent the start of a trend. Multiple severe convective storm events already have occurred in the second quarter, and the 2024 Atlantic hurricane season is forecast to be “extremely active.”

Personal auto’s recent improvements follow 2022 results that were among the worst in recent years. The number of drivers on the road has returned to pre-pandemic levels, and the risky driving behavior that led to high losses during the pandemic has not improved. More accidents with severe injuries and fatalities have driven up claims and losses in terms of both vehicle damage and liability, attracting greater attorney involvement and legal system abuse.

Compounding these loss drivers has been historically high inflation, which puts upward pressure on the material and labor costs for both the auto and property lines.

Favorable first-quarter results are good news, but it’s important for policyholders and policymakers to remember that the current hard market wasn’t created overnight. It will take time for insurers’ performance and drivers’ rates to stabilize.

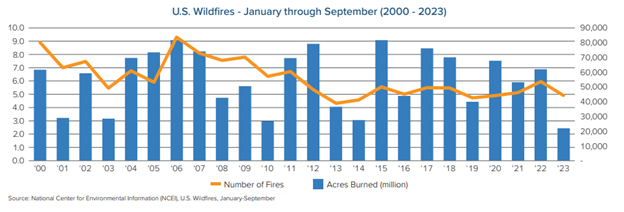

This wildfire season is expected to be less intense than normal, but people in high-risk areas should be aware of and prepared for potential damage, according to Craig Clements, a professor of meteorology and climate science at San José State University.

“There are days people really need to be careful,” said Dr. Clements, who directs the Wildfire Interdisciplinary Research Center and is a Triple-I non-resident scholar. “High fire days are typically hot, dry, and windy. If there’s ignition, these fires can spread quickly, depending on the fuel type.”

Despite record-breaking conflagrations across the Northern Hemisphere in recent years, U.S. wildfire frequency (number of fires) and severity (acres burned) have been declining in recent years and in 2023 were among the lowest in the past two decades.

While that trend is positive – reflecting progress in prevention of human-ignited wildfires – it isn’t a reason for complacency. Another long-term trend has been the doubling of the share of natural catastrophe insured losses from wildfires over the past 30 years, according to Swiss Re. This reflects the impact of a growing number of people living in the wildland-urban interface – the zone of transition between unoccupied and developed land, where structures and human activity intermingle with wildland and vegetative fuels.

A 2022 study in the journal Frontiers in Human Dynamics found that people are moving to areas that are increasingly vulnerable to catastrophic wildfires.

“They’re attracted by maybe a beautiful, forested mountain landscape and lower housing costs somewhere in the wildland-urban interface,” said University of Vermont environmental scientist Mahalia Clark, the paper’s lead author. “But they’re just totally unaware that wildfire is something they should even think about.”

To prepare, people should keep an eye out on the National Weather Service, social media, or watch the news, to ensure they are ready for any potential risks, and be on the lookout for Red Flag Warning days.

Dr. Clements also recommends referring to the National Interagency Fire Center website, which is updated daily for fire risks in particular regions. Triple-I suggests looking into the Wildfire Prepared Home designation program, which helps homeowners take protective measures for their home and yard to mitigate wildfire risks.

It’s also important for homeowners to remember that, following wildfires, rains can result in landslides and debris flows that often are not covered by insurance policies. It’s especially important to understand the difference between “mudslides” and “mudflow” and to discuss your coverage with an insurance professional.

Flood risk is not only one of the most destructive perils facing property owners; it is among the most complicated forms of coverage for property/casualty insurers to underwrite. For decades, the private market wouldn’t cover flood risk, which is why the National Flood Insurance Program had to be established.

But improved data collection and the availability of practically unlimited computing power have changed the equation for insurers, according to Anil Vasagiri, senior vice president for property solutions at Swiss Re. In a recent Executive Exchange with Triple-I CEO Sean Kevelighan, Vasagiri discussed the developments that have helped turn flood from a nearly untouchable peril to a burgeoning area of opportunity for insurers.

Over 90 percent of natural catastrophes involve flood in some way or another. Vasagiri said the ability to use multiple data sources in understanding flood conditions of specific properties helps insurers more accurately underwrite flood and help policyholders proactively address their own exposure to the peril.

“Increased information leads to increased capacity,” Vasagiri said – a fact that bodes well for improving insurance availability and affordability and evidenced by the increased number of private insurers writing flood coverage since 2016.

The timing of the private market’s increasing appetite for flood risk is fortuitous, as it coincides with Risk Rating 2.0, NFIP’s new pricing methodology that aims to make the government agency’s flood insurance premium rates more actuarially sound and equitable by better aligning them with individual properties’ flood risk. As NFIP rates become more aligned with principles of risk-based pricing, some policyholders’ prices are expected to fall, while many are going to rise.

In the Executive Exchange, Vasagiri discussed the Swiss Re’s acquisition of Fathom – a U.K.-based company specializing in water-related risks – as part of the company’s ongoing commitment to helping close the flood protection gap.

The property and casualty insurance industry posted its second consecutive year of underwriting losses, driven primarily by personal lines, according to the latest industry underwriting projections by actuaries at Triple-I and Milliman.

The net combined ratio for 2023 was 101.6, according to Insurance Economics and Underwriting Projections: A Forward View, a Triple-I members-only webinar. Combined ratio is a standard measure of underwriting profitability, in which a result below 100 represents a profit and one above 100 represents a loss.

The newest results are an improvement from 2022. Additionally, premium growth is expected to further improve underwriting results in 2024, with the 2024 industry net combined ratio forecast at 100.2.

Michel Léonard, PhD, CBE, Triple-I’s chief economist and data scientist, discussed how P&C replacement costs are increasing more slowly than the consumer price index (CPI).

“P&C replacement costs benefited from greater deceleration of key CPI components, such as construction material and used auto costs,” he said. “We expect this trend to continue until early 2026.”

Léonard noted that personal and commercial auto replacement costs decreased in the first four months of 2024, continuing their 2023 trend, largely due to double-digit declines in used auto prices.

“Even homeowners’ replacement cost changes – the segment subject to some of the highest replacement cost increases over the past few years – is now lower than overall CPI,” Léonard said.

Dale Porfilio, FCAS, MAAA, Triple-I’s chief insurance officer, discussed the overall P&C industry underwriting projections and premium growth.

“The overall picture from prior quarters remains the same with commercial lines performing better than personal, but to a lesser extent,” Porfilio said.

The 2023 commercial lines net combined ratio was 96.2, 1.4 points worse than the 2022 result. While still unprofitable, personal lines improved 3.2 points relative to 2022. For 2023, the personal lines expense ratio improved by almost 2 points over 2022, most dramatically in personal auto. The net written premium growth rate for personal lines surpassed commercial lines by over 7 points in 2023.

“Continued personal lines premium growth should lead to further convergence in underwriting performance in 2024,” Porfilio said.

Jason B. Kurtz, FCAS, MAAA, a principal and consulting actuary at Milliman – a global consulting and actuarial firm – said that for commercial auto, the 2023 net combined ratio of 109.2 is 3.8 points higher than 2022, and 10.3 points higher than 2021.

“The improved underwriting results following the COVID-19 pandemic appear to have been short-lived, as the commercial auto underwriting results have once again deteriorated and adverse prior year development has returned to pre-COVID levels,” Kurtz said.

Looking at the workers compensation line, Kurtz noted that the 2023 net combined ratio of 87.3 is nearly identical to 2022 and the second lowest in over 15 years.

“2023 net written premium growth rate of 1 percent is expected to increase to 2 percent in 2024 and remain at that level of growth through 2026,” Kurtz said. “Favorable underwriting results are expected for our forecast horizon, which in turn will dampen premium growth going forward.”

Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance (NCCI), said the workers comp system is in a period of extraordinary performance.

“WC leads the P&C industry with the lowest combined ratio compared to all other lines of business,” Glenn said.

Further highlighting the strong results, she said, 2023 is the tenth straight year of underwriting gains and seventh consecutive year with combined ratios under 90.

Average U.S. homeowners insurance premiums have increased at a rate that has outpaced household income from 2001 to 2021, according to a new report by the Insurance Research Council (IRC). In 2021 – the latest year for which data is available – homeowners spent an average of 1.99 percent of their income on homeowners insurance, up from 1.54 percent in 2001.

Affordability varies widely from state to state, and affordability rankings have fluctuated over time. In 2021, Utah was the most affordable state and Florida was the least affordable. Kansas, New York, and Washington, D.C., have demonstrated improvements from 2015 to 2021, and California, Montana, and Wyoming saw the greatest deterioration during the same period. Florida and Louisiana have consistently been the least-affordable states in the nation.

The analysis by IRC – like Triple-I, an affiliate of The Institutes – looks at homeowners insurance affordability at national and state levels and examines underlying cost drivers by state. It does not address affordability for specific demographic or geographic risk profiles. The report found that frequency and severity of natural disasters, economic conditions, rising construction costs, and litigation all significantly contributed to rising homeowners insurance costs.

“An understanding of what drives the cost of insurance is essential for consumers navigating the current insurance market,” said Dale Porfilio, FCAS, MAAA, IRC president and chief insurance officer for Triple-I. “Efforts to promote homeowner awareness and adoption of protective measures, strengthen state and local building codes, and encourage community resilience programs can all improve insurance affordability.”

Legislative reforms put in place in 2022 and early 2023 to address legal system abuse and assignment-of-benefits claim fraud in Florida are beginning to help the state’s property/casualty insurance market recover from its crisis of recent years, according to a new Triple-I Issues Brief.

Claims-related litigation is down, the “depopulation” of the state’s insurer of last resort continues apace, and underwriting profitability – while still in negative territory – has improved significantly. Insurers also benefited from a relatively mild 2023 Atlantic hurricane season and a meaningful increase in investment income, posting a net profit for the first time in seven years.

But it’s important to remember that the crisis wasn’t created overnight and that it will take time for the reforms and other developments to be reflected in policyholder premiums. Homeowners should not expect their rates to decline in 2024, despite the improved industry performance, although some regional insurers have filed for small decreases.

“Rates may moderate some compared to prior years,” said Mark Friedlander, Triple-I director of corporate communications, “but rising replacement costs – combined with expected higher reinsurance costs for the June 1 renewals – are going to continue to drive average premiums upward in 2024.”

One factor keeping upward pressure on rates is fraud and legal system abuse. With only 15 percent of U.S. homeowners insurance claims, the state accounts for nearly 71 percent of the nation’s homeowners claim-related litigation, according to Florida’s Office of Insurance Regulation.

There are early signs that recent legislative reforms are beginning to bear fruit. In 2023, Florida’s defense and cost-containment expense (DCCE) ratio – a key measure of the impact of litigation – fell to 3.1, from 8.4 in 2022, according to S&P Global.

But the catastrophe-prone state faces a number of natural challenges, from a projected “extremely active” 2024 hurricane season to wildfires, flooding, and severe convective storms.

“Hurricanes get the most media attention,” Friedlander said, “but severe convective storms inflict comparable losses. And it only takes one bad hurricane season to wipe out the benefits of one or more mild years.”