Hurricane Beryl’s rapid escalation from a tropical storm to a Category 5 hurricane does not bode well for the 2024 Atlantic Hurricane season, which is already projected to be of above-average intensity, warns Triple-I non-resident scholar Dr. Philip Klotzbach.

“This early-season storm activity is breaking records that were set in 1933 and 2005, two of the busiest Atlantic hurricane seasons on record,” Dr. Klotzbach, a research scientist in the Department of Atmospheric Science at Colorado State University, recently told The New York Times.

The quick escalation was a result of above-average sea surface temperatures. A hurricane that intensifies faster can be more dangerous as it leaves less time for people in its path to prepare and evacuate. Last October, Hurricane Otis moved up by multiple categories in just one day before striking Acapulco, Mexico, as a Cat-5 that killed more than 50 people.

After weakening to a tropical storm, Beryl made landfall as a Cat-1 hurricane near Matagorda, Texas, around 4 a.m. on July 8, according to the National Hurricane Center, making it the first named storm in the 2024 season to make landfall in the United States. Beryl unleashed flooding rains and winds that transformed roads into rivers and ripped through power lines and tossed trees onto homes, roads, and cars. Restoring power to millions of Texans could take days or even weeks, subjecting residents who will not have air conditioning to further risk as a sweltering heatwave settles over the state.

Extreme heat was just one climate-related topic addressed by Triple-I Chief Insurance Officer Dale Porfilio in an interview with CNBC’s “Last Call” on July 9. While most farmers are insured against crop damage due to heat conditions and homeowners insurance typically covers wildfire-related losses, Porfilio noted, a “more subtle impact is on roofs that we thought were built to a 20-year lifespan.”

When subjected to extreme heat, roofs can become more brittle and prone to damage from wind or hail.

“So, you have to think about the roof coverage on your home insurance policy,” Porfilio said.

He also pointed out that flood risk represents “one of the biggest insurance gaps in this country. Over 90 percent of homeowners do not have the coverage.”

Many people incorrectly believe homeowners insurance covers flood damage or that they don’t need the coverage if their mortgage lender does not require it.

In an interview on CNBC’s “Squawk Box,” Triple-I CEO Sean Kevelighan discussed the potential impact of the predicted “well above-average” 2024 season on the U.S. property/casualty market.

“This is what the insurance industry is prepared for,” Kevelighan said. “It keeps capital on hand after writing policies to make sure that those promises can be kept.” The P/C industry has $1.1. trillion in surplus as of March 31, 2024.

Kevelighan pointed out that the challenges to the industry go beyond climate-related trends, explaining how legal system abuse, regulatory environments, shifting populations, and inflation are impacting insurers’ loss costs.

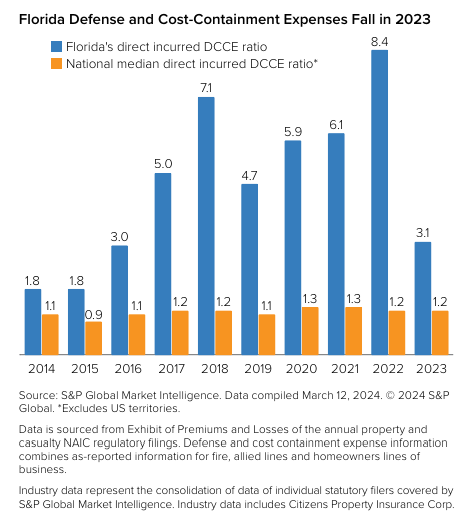

In Florida, for example, “you’ve got over 70 percent of all homeowners insurance litigation residing in that state, whereas it represents less than 10 percent of the overall claims.”

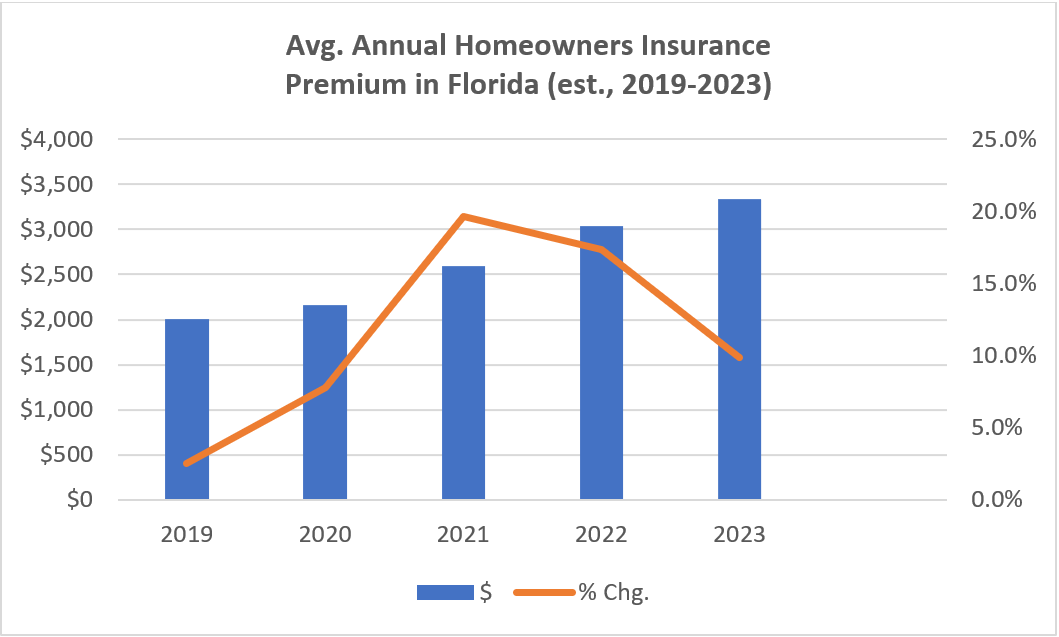

He pointed out that Florida’s insurance market has improved – with homeowners insurance premium growth flattening somewhat – as a result of tort reform legislation and added that Louisiana’s legislature addressed insurance reform during its most recent session.

“In California, insurers can’t catch up with inflationary costs because of regulatory constraints,” Kevelighan noted. “They are not able to model [climate risk] and are not able price reinsurance into their policies.”

California’s wildfire situation is complex, and the state’s Proposition 103 has hindered insurers’ ability to profitably write homeowners coverage in that disaster-prone state. In late September 2023, California Insurance Commissioner Ricardo Lara announced a package of executive actions aimed at addressing some of the challenges included in Proposition 103. Lara has given the department a deadline of December 2024 to have the new rules completed.

Learn More:

Florida Homeowners Premium Growth Slows as Reforms Take Hold, Inflation Cools

Lightning-Related Claims Up Sharply in 2023

Less Severe Wildfire Season Seen; But No Less Vigilance Is Required

Accurately Writing Flood Coverage Hinges on Diverse Data Sources

IRC: Homeowners Insurance Affordability Worsens Nationally, Varies Widely by State

Legal Reforms Boost Florida Insurance Market; Premium Relief Will Require More Time

2024 Wildfires Expected to Be Up From Last Year, But Still Below Average

CSU Researchers Project “Extremely Active” 2024 Hurricane Season

Triple-I Issues Brief: Hurricanes

Triple-I Issues Brief: Attacking Florida’s Property/Casualty Risk Crisis

Triple-I Issues Brief: California’s Risk Crisis

Triple-I Issues Brief: Legal System Abuse

Triple-I Issues Brief: Wildfires