The commercial auto insurance line has struggled to achieve underwriting profitability for years, even before the inflationary conditions that have been affecting property/casualty lines more recently. This trend has been accompanied by steady growth in net written premiums (NWP).

This weakness in underwriting profitability has been driven by several causes, according to a new Triple-I Issues Brief. One is the fact that vehicles – both commercial vehicles and personal vehicles they collide with – have become increasingly expensive to repair, thanks to new materials and increased reliance on sensors and computer systems designed to make driving more comfortable and safer. This well-established trend has been exacerbated by supply-chain disruptions during COVID-19 and continuing inflation in the pandemic’s aftermath.

Distracted driving and litigation trends also have played a role.

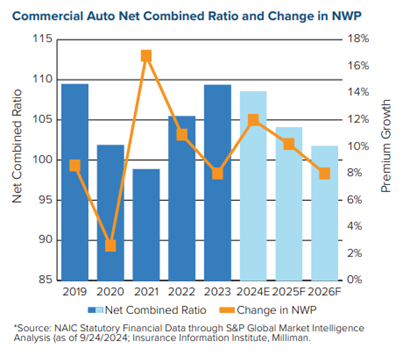

However, Triple-I sees some light on the horizon for commercial auto in terms of the line’s net combined ratio – a standard measure of underwriting profitability calculated by dividing the sum of claim-related losses and expenses by earned premium. A ratio under 100 indicates a profit and one above 100 indicates a loss.

As the chart below shows, the estimated 2024 net combined ratio for commercial auto insurance has improved slightly since 2023, and further improvement is expected over the next two years.

These projected improvements are based on an expectation of continued premium growth – due more to aggressive premium rate increase than to increased exposure – as the rate of insured losses levels off.