Among homeowners surveyed by the Insurance Research Council (IRC), 88 percent recognize that aerial imagery is a beneficial tool for insurers.

Nearly all respondents said they recognize the value of using satellite, drone, and aircraft images for early problem detection, claims processing, and hazard identification before costly damage occurs. Most also said they believe aerial imaging can lead to fairer pricing.

Key findings:

Nine out of 10 respondents said they see at least one benefit from aerial imagery’s use in insurance. More than half said it leads to fairer insurance pricing.

While 60 percent have some awareness that insurers use aerial imagery, 40 percent know little or nothing about it.

When homeowners are familiar with the use of aerial imagery for underwriting, they are nearly twice as likely to think it makes insurance pricing fairer.

Homeowners worry more about accuracy than privacy in the context of aerial imagery. Accuracy emerges as the top individual concern, with 31 percent citing it as their biggest worry, compared to 24 percent who cite privacy as their primary concern.

Education and transparency are key to acceptance of this technology, the survey found. Homeowners who were already familiar with aerial imagery applications were found to show consistently higher confidence levels, greater benefit recognition, and more positive sentiment across all insurance uses. Younger homeowners also demonstrated greater acceptance and higher confidence in the technology’s accuracy.

“Consumers see value in aerial imagery when they understand how it’s used in insurance,” said IRC President Pat Schmid. “Efforts to increase transparency and consumer knowledge can bridge the confidence gap, improve customer trust, and help homeowners realize the benefits of faster claims, fairer pricing, and better risk prevention.”

The IRC, like Triple-I, is an affiliate of The Institutes.

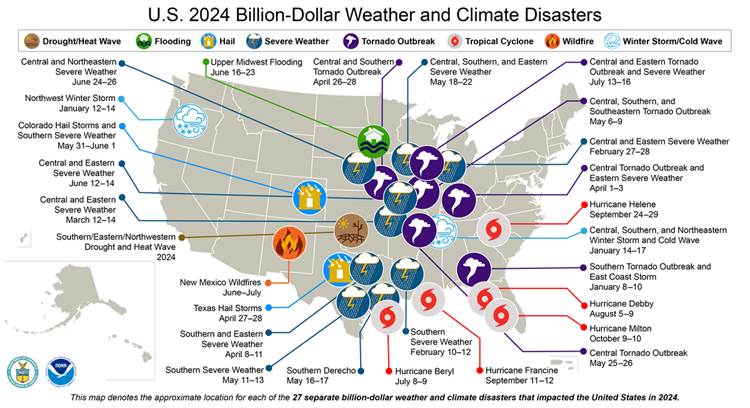

A climate nonprofit plans to revive a key federal database tracking billion-dollar weather and climate disasters that the Trump Administration stopped updating in May, Bloomberg reported.

The database captures the financial toll of increasingly intense weather events and was used by insurers and others to understand, model, and predict weather perils across the United States. Dr. Adam B. Smith, the former NOAA climatologist who spearheaded the database for more than a decade, has been hired to manage it for the nonprofit, Climate Central.

NOAA in May announced it would stop tracking the cost of the country’s most expensive disasters, those which cause at least $1 billion in damage – a move that would leave insurers, researchers, and government policymakers with less reliable information to help understand the patterns of major disasters like hurricanes, drought or wildfires, and their economic consequences.

Climate Central plans to expand beyond the database’s original scope by tracking disasters as small as $100 million and calculating losses from individual wildfires, rather than simply reporting seasonal regional totals.

A record 28 billion-dollar disasters hit the United States in 2023, including a drought that caused $14.8 billion in damages. In 2024, 27 incidents of that scale occurred. Since 1980, an average of nine such events have struck in the United States annually.

This summer – amid deadly wildfires and floods – the Trump Administration has appeared to be rolling back some of its DOGE-driven NOAA funding cuts. NOAA recently announced that it would be hiring 450 meteorologists, hydrologists, and radar technicians for the National Weather Service (NWS), after having terminated over 550 such positions in the already-understaffed agency in the spring.

In addition, the administration’s announced termination of the Building Resilient Infrastructure and Communities (BRIC) program — run by the Federal Emergency Management Agency (FEMA) — has been held up by a court injunction while legislators debate its future. Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters.

Regarding the rescue of the NOAA dataset, Colorado State University researcher and Triple-I non-resident scholar Dr. Phil Klotzbach said, “The billion-dollar disaster dataset is important for those of us working to better understand the impacts of tropical cyclones. It uses a consistent methodology to estimate damage caused by natural disasters from 1980 to the present and was a critical input to our papers investigating the relationship between landfalling wind, pressure and damage. I’m very happy to hear that this dataset will continue!”

Parents are increasingly open to using technology to keep their teen drivers safe on the road, a recent survey from Nationwide finds.

The survey found 4 out of 5 parents would enroll their teens in telematics programs that reward safe driving. This enthusiasm for tech-based solutions comes despite mixed parental assessments of their teens’ driving abilities: While 42 percent rate their teen’s driving as “good” or “excellent”, similar percentages express concerns about distracted driving and reckless behavior.

“Parents want to feel confident that their teens are making smart choices behind the wheel,” says Casey Kempton, Nationwide president of P&C personal lines. “These tools help make that possible—not just by monitoring behavior, but by encouraging better habits through positive reinforcement.”

Despite recognizing the value of safety technology, adoption remains limited. While 96 percent of parents said they believe dashcams provide valuable evidence after accidents, only 26 percent of teen drivers actually have them installed.

The survey reveals a broader trend in which consumers are drawn to telematics and monitoring technologies, though motivations vary. While parents prioritize safety benefits, many consumers are equally interested in the insurance premium discounts these programs can provide.

“This isn’t just about technology,” Kempton says. “It’s about creating a culture of accountability and shared responsibility on the road.”

As comfort with AI-enabled monitoring grows, it appears that families are embracing a future in which technology supports — but does not replace — good judgment.

As property/casualty insurers increase their focus on predicting and preventing costly damage that drives up claims and premiums, telematics technology has come to play an increasing role. From video doorbells that reduce theft and vandalism to “smart plumbing” solutions that detect leaks and shut off water before in-home flooding can occur, these technologies clearly offer value to homeowners and insurers.

But how much value?

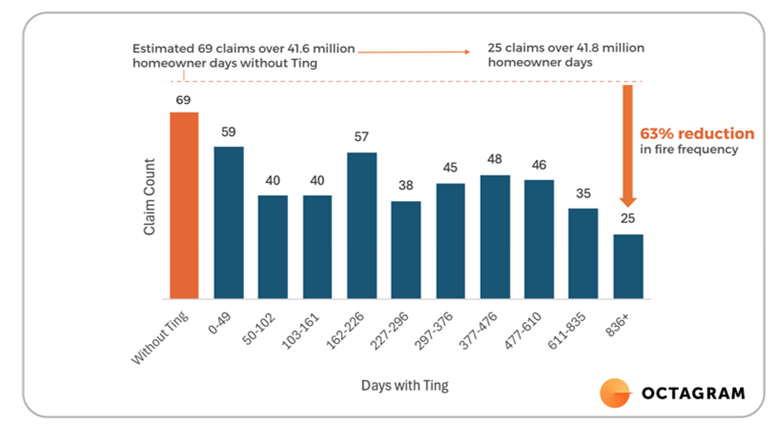

Whisker Labs – maker of the Ting home fire prevention solution – has taken on the challenge of quantifying its product’s efficacy and return on investment. In a research partnership with Octagram Analytics for independent data analysis and modeling and Triple-I for its insurance industry expertise and insight, Whisker Labs found that Ting reduced fire claims within the study sample by an estimated 63 percent, resulting in 0.39 fewer electrical fire claims per 1,000 home years of experience, in the third year after installation. This translates into a fire claims reduction benefit of $81 per customer.

“This study provides concrete evidence of the value that telematics technology can deliver,” said Patrick Schmid, chief insurance officer at Triple-I. “While IoT solutions are gaining traction with many success stories, rigorous analysis of claims reduction has been harder to find until now. This analysis clearly shows Ting reduces claims and provides a positive return on investment for insurers.”

Ting helps protect homes from electrical fires by using advanced AI to detect arcing, the precursor to most electrical fires. Once connected to a single outlet, Ting analyzes 30 million measurements per second, analyzing voltage at high frequencies to detect tiny electrical anomalies and power quality problems. These hazards can originate from wiring in the home, connected devices and appliances, or even the power coming in from the utility. On average, Ting detects and mitigates fire hazards in 1 out of every 60 homes it protects.

“Ting is about saving lives and homes – that’s always been our mission,” said Bob Marshall, CEO and cofounder of Whisker Labs. “By analyzing verified claims data over time, this analysis shows that what’s best for families also delivers a strong financial return for insurers. Prevention is better for everyone.”

Whisker Labs works with a growing community of 30 insurers who provide Ting to their customers for free. More than one million Tings are deployed in the United States, and approximately 50,000 new Tings are installed each month.

In addition to monitoring voltage and features of voltage at high frequencies to detect arcing that is indicative of fire hazards, Ting has a temperature sensor that monitors the temperature within the home.

“When the temperature drops below 42 degrees, an alert is issued,” Marshall said. “Thus, Ting detects and warns about conditions that can result in frozen and burst pipes and alerts the homeowner to correct the situation before damage occurs. Over the past three years, we have issued low-temperature warnings to about 1 in 560 customers per year.”

Measuring the value

Like Ting, other peril-based IoT solutions issue alerts and warnings when a hazard is detected. Thousands of hazards are detected and alerts sent, but how do you know that this reduces claims? How do you estimate the return on investment for these devices? How can you prove that the bad thing, a loss and a claim, didn’t occur?

“We developed a methodology to do this in the real world with existing customers and experience data,” said Whisker Labs Chief Scientist Stan Heckman.

Whisker Labs and Octagram had to overcome challenges related to limited data and sampling bias. To address these, a self-controlled study was developed that assesses claims over time in homes with Ting in place. (See paper for a fuller explanation of the methodology).

The chart below shows how the number of fire claims in Ting-equipped homes declines over time. The claims frequencies observed and associated percent reduction in claims are highly dependent on the definition of the sample of non-cat fire claims provided by carriers that participated in the analysis. However, this does not affect the observed absolute reduction.

Using data from Triple-I and Verisk, Whisker Labs determined that Ting provides a loss-prevention benefit of $81 per home per year. (See paper for details).

“Add in benefits associated with reduction in water-related losses from frozen pipes and failing sump pumps and water heaters,” and the benefits are likely substantially higher, Marshall said. Insurers who provide Ting to their policyholders also may enjoy improvements in customer retention.

Analysis based on granular, cutting-edge data is essential to staying ahead in our rapidly shifting risk landscape. During Triple-I’s Joint Industry Forum in Chicago, two “Risk Take” presenters dove deep into the innovative data initiatives they engaged in to help turn these challenges into new opportunities for insurers.

Balancing consumer needs

With natural catastrophe frequency and supply chain uncertainty on the rise, so are home maintenance costs. Estimated to exceed $10,000 annually in 2024 – at a 5.9 percent year-over-year increase – home maintenance further weighs against the mounting costs of premium rates and property taxes across the U.S., leading many homeowners to forgo investing in at-home risk mitigation like smart home telematics.

“Across the providers we’ve talked to, adoption of telematics falls somewhere between the single digits,” said presenter James Bilodeau, CEO and founder of PreFix Inc. “The reason is simple: the value proposition of what we would like homeowners to do isn’t important enough compared to what homeowners actually need.”

For Bilodeau, the solution is also simple: combine advanced technology with routine preventative maintenance. By providing personalized, year-round home repair, Bilodeau’s Texas-based firm aims to mitigate losses while gathering unique primary data on the properties they service. Insurers can use this data to develop telematics technology and more accurately price the associated risks.

Such data collection “creates a flywheel in which we help our partners delight their customers with exceptional service and hit directly at affordability issues, both with home maintenance and in premium reduction,” Bilodeau said.

After a successful pilot program, USAA expanded its partnership with the company to offer discounted maintenance services to members who sign up for PreFix. Noting that the company is pursuing partnerships with other major insurers, Bilodeau highlighted that industry collaboration is crucial to not only facilitate more refined coverage but to lower the cost of entry to enhancing resilience.

Emerging public safety risks

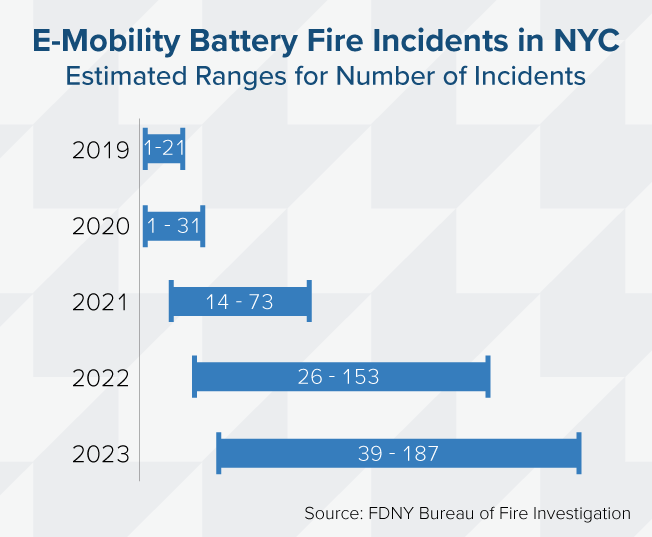

An eightfold increase in New York City fire incidents between 2019 and 2023 correlates strongly with the growing popularity of e-mobility devices, according to a joint report by UL Standards & Engagement (ULSE) and Oxford Economics that is based in part on Triple-I data.

Presenting on the report, ULSE Director of Insights Sayon Deb explained how lithium-ion battery fires linked to e-bikes and scooters became a mainstream risk for COVID-era urban environments, due in part to the booming online food and grocery delivery market.

“Nearly $519 million worth of damages were caused in just four years from structural property damage, injuries, and loss of life,” Deb said, pointing out that this figure does not account for “the additional cost of communal fear, in terms of fires happening across the hallway from you, and also the loss in economic opportunities and the community toll that it takes as we respond to these fires.”

Inadequate public safety awareness, paired with the easy availability of uncertified devices, helped fuel the crisis. Beyond overusing or incorrectly charging the devices, e-mobility users often left them in dangerous locations, with “66 percent of those who charge at home charging their devices near their exit,” Deb explained – effectively “blocking your exit from your home in the event of a fire.”

E-mobility regulations vary wildly by state. Though New York City regulations passed in 2023 show progress, ULSE recommends more proactive public outreach, safety standard enforcement, and incident reporting to better track e-mobility risk data.

“The better the data we collect, the better we can understand where, how, and why these battery fires occur, so that we can prevent future fires from happening,” Deb concluded.

Global economic uncertainty emerging from recent U.S. policy actions was a major concern for thought leaders on the “Economics, Underwriting, and Geopolitics” panel at Triple-I’s Joint Industry Forum in Chicago.

Despite recently posting its most favorable underwriting performance since 2013, the property/casualty insurance industry faces several obstacles to continued progress, particularly from tariffs issued by the Trump Administration.

Short-term economic impacts

“Tariffs aren’t inherently good or bad,” said Triple-I Chief Economist and Data Scientist Dr. Michel Léonard, who co-moderated the discussion. “Where there is consensus among economists is that, in the short term, tariffs do lead to inflation and disruption.”

Put simply, tariffs can raise revenue for the issuing government while costing the domestic businesses that rely on imported goods. In advance of pending tariffs, companies up and down the supply chain are purchasing such goods at a record pace, which boosts the demand and prices of these materials. Consumers will inevitably shoulder some or all of the added cost.

Many proposed or enacted tariffs involve materials essential to construction and auto manufacturing. Earlier this month, for instance, the administration doubled its new steel and aluminum tariff to 50 percent – including on Canada, the largest steel supplier to the United States. P/C replacement costs will likely rise throughout the industry, leading to higher claim payouts and, consequently, premium rates.

Amid various tariff reductions, increases, impositions, and pauses, President Trump’s trade policies remain difficult to determine or predict. This lingering ambiguity – paired with impending replacement cost increases – creates a “double whammy” for insurers, said Aaron Klein, Miriam K. Carliner Chair and senior fellow in Economic Studies at the Brookings Institution.

“Other markets can adapt to that more quickly,” Klein said. “When I renew my auto policy in February, the insurer on the other side has to guess what the costs are going to be over six months.”

While in a period of extraordinary performance, the workers compensation line also faces potential risks from oncoming tariffs, noted Donna Glenn, chief actuary at the National Council on Compensation Insurance (NCCI). Mitigated by investments in technology and safety, workplace incidents could rise, she explained, as “a lot of the uncertainty puts businesses back in a defensive mode and asking, ‘how should I spend my money?’”

“I caution and say there will be some temporary lack of investment in safety,” Glenn continued.

Talent and technology

An evolving workforce poses additional risks.

“Workers comp has benefited from a very strong labor market,” Glenn said, pointing to consistently low U.S. unemployment rates, but current mass deportation efforts could undermine this trend. “We are accustomed to having a significant influx of foreign-born workers,” Glenn explained. “When we don’t – and when we shift to not having them – the labor market could stifle to some degree.”

Bridging the talent gap lends further urgency to this issue, as roughly 400,000 workers are projected to leave the insurance industry through attrition by 2026 in the U.S. alone, according to the U.S. Bureau of Labor Statistics. And with generative AI automating more processes across the insurance value chain, cultivating a workforce possessing the necessary skillset to oversee them compounds the problem.

“AI can certainly help improve productivity,” said Triple-I Chief Insurance Officer and co-moderator Dale Porfilio, “but we’re going to need people to do an awful lot of those jobs. We’re still going to have that talent gap.”

Embracing advanced technology, then, gives insurers an opportunity to both develop that expertise and rebuild the workforce by attracting younger tech professionals who might otherwise overlook the industry. Innovative companies like Argo Group are already paving the way for this collaboration.

Patrick Schmid, president of The Institutes’ RiskStream Collaborative, acknowledged that “getting clarity about how significantly you can leverage AI is very important.”

Concern about using AI in underwriting, Schmid said, given an absence of AI regulatory guidance, which does not exist federally and is set to be blocked on a state level.

To provide insight into these efficiencies, Schmid described how RiskStream – a consortium of insurers, brokers, reinsurers, and other industry leaders – applies AI to streamline data processing, lower operating costs, and enhance customer experiences. Beyond expediting business operations, AI offers potential solutions to a range of challenges plaguing insurers, Schmid said – including one application that might help mitigate legal system abuse by facilitating earlier claims intervention, preventing excessive attorney involvement.

The panelists agreed that insurers will continue to adapt their underwriting and pricing to reflect this dynamic environment and emphasized the economy’s strong, steady recovery post-COVID.

“There’s not been a single case of an economic expansion in recorded history dying of old age,” Klein said. “Are we near the tipping point? I don’t think so.”

Identifying key risk trends amid an increasingly complex risk landscape was a dominant theme throughout Triple-I’s 2025 Joint Industry Forum – particularly during the panel spotlighting some of the insurance industry’s C-suite leaders.

Moderated by CNBC correspondent Contessa Brewer, the panel consisted of:

J. Powell Brown, president and CEO of Brown & Brown Inc.;

John J. Marchioni, chairman, president, and CEO of Selective Insurance Group;

Susan Rivera, CEO of Tokio Marine HCC (TMHCC); and

Rohit Verma, president and CEO of Crawford & Co.

Their discussion provided insight into how insurers can transform these uncertainties into opportunities for business development and for cultivating deeper connections with consumers.

Recouping policyholder trust

Given the volatility of the current risk environment – exacerbated by various ongoing geopolitical conflicts and the rising frequency and severity of natural catastrophes – it is more imperative than ever to reaffirm the intrinsic human element of insurance, the panelists agreed.

“That’s one of the most underappreciated aspects of our industry,” Marchioni said. “We make communities safer and put people’s lives and businesses back together after an unexpected loss. Being the calming force when you have unsettling events like this happen around the world is a big part of what we do.”

Yet prevailing public perception continues to indicate otherwise, even as insurers report repeated losses or nominal profits compared to other industries.

“The insurance industry may be the only industry where record profits are a problem,” CNBC’s Brewer added, because consumers tend to “not care whether it’s coming from your investments, or whether it’s coming from your underwriting business or your reinsurance. They just hear that you’re making record profits.”

Brown noted that consumer mistrust derives, in part, from “a very active plaintiffs’ bar,” which the American Tort Reform Association estimates spent over $2.5 billion for nearly 27 million ads across the United States last year. He further discussed how, though the average homeowners’ insurance premium rate in Florida will increase this year, his home state has enjoyed far more stable rates after tort reforms eased litigation costs on insurers.

Previous research by the Insurance Research Council (IRC) – like Triple-I, an affiliate of the Institutes – showed that most consumers perceive the link between attorney advertising and higher insurance costs. Crawford’s Verma, however, emphasized that this awareness does not necessarily translate into consumers understanding their own agency.

“It’s easier for homeowners to understand how the weather impacts potential losses and the fact that weather patterns have changed,” Verma said. “But when it comes to [legal system abuse], I don’t think that connection is as well understood.”

Reflecting on a record high in nuclear verdicts last year, Rivera suggested insurers must reconfigure how they communicate legal system abuse to consumers.

“Where are those hospital professional liability verdicts going to go?” he said. “They’re going to go back into the cost of health care at the end of the day.”

Leading the AI charge

Maintaining consumer centricity while implementing or experimenting with technological innovations – especially generative AI – was a unifying objective for all the panelists.

“We look at AI as an enabler,” Brown said, “so we can put teammates in a position to spend more time with customers, which is the most important thing.”

For Tokio Marine’s Rivera, AI “ultimately helps all of our insureds” by boosting operational efficiency while reducing operational costs, as well as facilitating more proactive risk management than ever before. A growing percentage of insurance executives appear to agree, as generative AI models continue to expedite data processing across the insurance value chain, reshaping underwriting, pricing, claims, and customer service.

Such efficiency, paired with the potential for improved decision-making, is crucial “in our dramatically changing environment,” Marchioni stressed.

“We have thousands of claims every day,” he said. “Thinking about lawsuit abuse as a backdrop – a claims adjuster, every day, has to make decisions regarding, ‘Do I settle this claim based on injuries or venue? What’s the value of the injury and of the claim? Who’s the plaintiffs’ attorney?’ These tools give more refined information so your knowledge workers can make better, more timely decisions.”

Generative AI fails, however, when base datasets are insufficient, outdated, or inaccurate, Brown pointed out. Training AI models uncritically can lead to outputs containing false and/or nonsensical information, commonly known as “hallucinations”.

At their current capacity, at least, AI models cannot draw the kinds of salient conclusions that adjustors and underwriters can, meaning AI could “change the way we work, but it’s not going to replace the jobs,” Verma said.

Though they do not currently exist in the United States at the federal level, AI regulations have already been introduced in some states, following a comprehensive AI Act enacted last year in Europe. With more legislation on the horizon, insurers must help lead these conversations to ensure that AI regulations suit the complex needs of insurance, without hindering the industry’s commitments to equity and security.

A 2024 report by Triple-I and SAS, a global leader in data and AI, centers the insurance industry’s role in guiding conversations around ethical AI implementation on a global, multi-sector scale, given insurers’ unique expertise in analyzing and preserving data integrity.

As the insurance industry grapples with retirements and the challenge of attracting talent, forward-thinking insurers are finding success by combining traditional mentorship with cutting-edge technology, according to Triple-I’s latest Executive Exchange.

The “Ascend” Approach to Talent Development

David Corry, who heads Casualty for Argo Group, told Triple-I CEO Sean Kevelighan that the company’s “Ascend with Argo” program offers a blueprint for effective talent recruitment and retention. Rather than hoping young professionals will stumble into insurance careers, Argo actively partners with brokers to create meaningful experiences for early-career workers.

By offering shadow days, continuing education, and direct access to industry leaders, programs like Ascend make insurance careers tangible and appealing.

“Last month, we hosted a dozen young career brokers in our New York City office,” Corry said. “They spent a day with our underwriters and heard from senior leadership—giving them real exposure to how carrier operations work from the inside.”

Technology as a Talent Magnet

Cutting-edge technology – including generative AI – is transforming how insurers operate, as well as helping them attract tech-savvy talent who might otherwise overlook the industry. This creates what Corry calls “two-way learning,” with experienced professionals teaching industry fundamentals while younger workers contribute innovation skills. It’s a win-win that makes insurance careers more attractive to digitally minded professionals.

What ties these efforts together is authentic leadership focused on people rather than personal advancement.

“A strong leader is someone who’s in it for the people they work with, not for themselves,” Corry emphasizes.

The insurance industry’s talent challenge is real, but companies are addressing it by combining innovative programs, mentorship, and technology adoption – demonstrating that insurance careers offer both stability and cutting-edge opportunities for the next generation of professionals.

By Sayon Deb, Director of Insights, UL Standards & Engagement

In just five years, lithium-ion battery fires linked to e-mobility devices have evolved from a fringe risk into a mainstream safety and liability crisis – particularly in dense urban areas, like New York City, where adoption of these devices has outpaced regulatory safeguards.

In addition to the obvious public safety threat, e-mobility battery related fires represent a significant and expanding liability exposure for insurers, property managers, and city agencies. Our latest report – developed in collaboration with Oxford Economics – sets out to answer a more fundamental question: What is this crisis truly costing the city?

The answer, conservatively estimated, is up to $519 million in combined human and economic loss between 2019 and 2023. This figure includes fatalities, injuries, and structural property damage

Why Now? Why New York?

The dramatic rise in fire incidents – an estimated eightfold increase from 21 in 2019 to as many as 187 incidents in 2023 – correlates strongly with the influx of low-cost, uncertified e-bikes and scooters. New York City’s unique combination of traffic congestion, delivery-based gig work, and dense multi-family housing has made it a case study in how quickly innovation can outstrip risk management.

Data from the Fire Department of New York, the Consumer Product Safety Commission, and UL Solutions’ Lithium-Ion Battery Fire Incident Database formed the foundation of our modeling. This helped us generate incident estimates of fatalities, injuries, and structural properties damages.

Oxford Economics translated these incident reports into cost estimates using a rigorous, conservative methodology by applying federal valuation metrics for loss of life and injury. Fatality costs were calculated using the U.S. Department of Transportation’s Value of a Statistical Life, set at $13.2 million per life as of 2023. Non-fatal injury costs were derived as severity-weighted fractions of that value, ranging from minor injury to critical injury, in accordance with DOT and Office of Management and Budget economic guidance.

Our analysis then integrated structural fire cost benchmarks from both Triple-I and the National Fire Protection Association. Triple-I’s data was particularly important in defining the upper-bound estimates for property loss. Claims data on the average insurance payout for residential fire damage provided a grounded, actuarial counterweight to NFPA’s generalized national averages.

This dual-source approach allowed us to capture a more realistic range of likely losses across different housing types, from NYCHA public units to private homes.

A growing blind spot for insurers

From a risk-modeling standpoint, e-mobility fire incidents don’t map easily to conventional insurance categories. Many e-mobility users, particularly gig economy workers, rely on leased, used, or modified e-bikes and e-scooters to meet delivery demands. Some of these devices are powered by third-party or uncertified batteries or, in some instances, contain second-hand components. This creates a messy risk environment in which it’s hard to know who owns what, how it has been maintained, or how it’s being used. Moreover, fires resulting from these devices often fall outside the scope of standard product warranties or manufacturer responsibility. This makes it difficult to determine who’s responsible when something goes wrong.

For insurers, this presents a growing blind spot. Traditional assumptions around property and contents coverage did not include high-risk devices charged in hallways or shared living spaces or for ignition sources that are not part of conventional product recall channels.

A $300 imported battery with no certification can trigger a six-figure claim, and those risks are becoming more common.

The Path Forward

Regulatory momentum is improving. New York City’s Local Law 39, signed in 2023, bans the sale and lease of uncertified e-mobility devices. In July 2024, New York Governor Hochul enacted additional statewide measures to support battery safety and user education. Federal legislation aimed at establishing nationwide safety requirements for lithium-ion batteries used in e-bikes and e-scooters is making its way through Congress. While these are positive steps, enforcement and awareness remain uneven, leaving significant gaps in consumer protection and risk mitigation.

From our perspective at ULSE, a multi-pronged strategy is essential:

Better enforcement of safety standards for batteries and chargers.

More robust public education on safe charging practices.

Trade-in and swap programs that encourage delivery workers to discard unsafe batteries.

Underwriting models that consider device certification, consumer behavior, and building type.

Improved incident reporting frameworks that enable cities and insurers to collect better data and therefore better track risk exposure.

With better data, smarter standards, and more coordinated public-private action, the future of e-mobility will thrive with safety at its center.

Mr. Deb will be among the risk and insurance industry thought leaders speaking at Triple-I’s Joint Industry Forum (JIF) in Chicago on June 18, 2025. It’s not too late to register to attend this insight-driven event.

As high-severity natural catastrophes – wildfires, floods, hurricanes, and others – become more frequent and more people move into riskier locales, insurance affordability and availability have become a challenge in many states.

Insurers underwrite and price coverage based on the risks they’re assuming, and rising premiums in these states have pushed more homeowners into residual market mechanisms, such as state-backed insurance pools or agencies. Reliance on these funds – which often provide more limited coverage at higher costs – is not sustainable in the long term.

To ensure market stability and continued insurance availability and affordability, insurers must leverage more granular and dynamic risk models that account for real-time environmental conditions, mitigation measures, and property-specific characteristics. A new paper by Triple-I and Guidewire – a provider of software solutions to the insurance industry – uses case studies from three California areas with very different geographic and demographic characteristics to show how such tools can be used to identify properties with attractive risk properties, despite their location in wildfire-prone areas.

California’s risk profile

In addition to its particular risk characteristics, California’s insurance challenge is exacerbated by a 1988 measure – Proposition 103 – that has constrained insurers’ ability to profitably insure property in the state. In a dynamically evolving risk environment that includes earthquakes, drought, wildfire, landslides, and damaging floods, regulatory interpretation of Proposition 103 has made it hard for some insurers to offer coverage in the state.

In some cases, this has led to insurers limiting or reducing their business in the state. With fewer private insurance options available, more Californians are resorting to the state’s FAIR Plan, which offers less coverage for a higher premium. For many, this “insurer of last resort” has become the insurer of first resort. This isn’t a tenable situation for the state or its policyholders. California’s insurance availability/affordability challenges will require a multi-pronged approach, and underlying every component is the need for granular, high-quality, reliable data.

Modeling based on granular data

Guidewire’s analysis, based on its HazardHub Wildfire Score, has shown that wildfire mitigation and home hardening can reduce wildfire damage by as much as 70 percent. But identifying less risky lots in such areas is no easy task.

“Every property being assessed for wildfire risk is unique,” the report says. “Therefore, it’s important to subject as many relevant variables as possible to analysis. For example, proximity of structures to fuel is important – but, to be more predictive, it helps to know more: What kind of fuel? Is there potential for a wind-driven event? Is the property on a hill? If so, is it north-facing?”

Guidewire’s model includes standard variables, such as slope, aspect, wildfire history, wind, and the amount of nearby vegetation. It also includes differentiators like vegetation type and fire-suppression success rate.

“The traditional approach to wildfire risk assessment has left many Californians without access to affordable property insurance coverage,” said Triple-I Chief Insurance Officer Dale Porfilio. “Our research shows that with more detailed, property-level analysis, insurers can confidently offer coverage in areas previously deemed too risky.”

Important moves by California

California has taken steps to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing – most notably, the state’s Sustainable Insurance Strategy, an ambitious plan released by Insurance Commissioner Ricardo Lara in 2023 plan aimed at safeguarding the health of the insurance market while ensuring long-term sustainability. A key component of the plan is a requirement that insurers writing homeowners coverage in the state write no less than 85 percent of their statewide market share in areas identified by the commissioner as “under-marketed.”

Tightly focused, data-driven analysis using tools like the HazardHub Wildfire Score, can go a long way toward helping insurers meet those requirements by identifying less risky parcels in undermarketed areas.

“The Triple-I analysis highlights how next-generation tools and data can uncover lower-risk properties – even in high-risk areas – empowering insurers to expand coverage confidently and responsibly,” said Leo Tenenblat, Senior Vice President and General Manager, Data and Analytics at Guidewire.