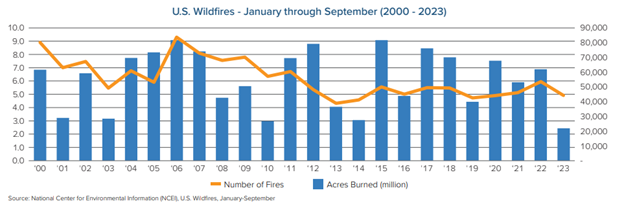

With record-breaking wildfires making headlines in recent years, it may be surprising to learn that U.S. wildfire frequency and severity for in 2023 are on track to be the lowest in the past two decades. In fact, the trend has been generally downward since 2000, according to a recently published Triple-I Issues Brief.

Despite catastrophic losses in Washington State, Hawaii, Louisiana, and elsewhere, California – a state often considered synonymous with wildfire – is in the midst of its second mild fire season in a row. This may be due to drought-breaking rains and snows, but Texas is experiencing fewer wildfires than in 2022, despite worsening drought conditions. About 37 percent of the continental U.S. remains under some form of drought, according to the U.S. Drought Monitor.

At the same time, Swiss Re reports that wildfire’s share of insured natural catastrophe losses has doubled over the past 30 years. How can those trends be reconciled? At least part of the answer resides in population trends – specifically, growing numbers of people choosing to live in the wildland-urban interface (WUI), the zone between unoccupied and developed land, where structures and human activity intermingle with vegetative fuels.

Mitigation is necessary – but not sufficient

The improvements in frequency and severity are likely due to investments in mitigation. State and local authorities have invested heavily to mitigate the human causes of wildfire. In addition, the federal Infrastructure and Jobs Act of 2021 included billions to support wildfire-risk reduction, homeowner investment in mitigation, and improved responsiveness to fires. More recently, the Biden Administration announced $185 million for wildfire mitigation and resilience as part of the Investing in America Agenda, which should help continue the declines in frequency and severity.

But with more people living in the WUI – nearly 99 million, or one third of the U.S. population, according to the U.S. Fire Administration – more than 46 million homes with an estimated value of $1.3 trillion are at risk.

According to the 2022 Annual Report of Wildfires produced by the National Interagency Fire Center (NIFC), 68,988 wildfires were reported and 7.5 million acres burned in 2022. Of these fires, 89 percent were caused by human activity and burned 55 acres per fire. By contrast, the 11 percent of fires caused by lightning resulted in an average of 563 acres burned, 10 times more than human-caused fires.

This difference may shed light on why the number of fires has been decreasing more dramatically than acres burned. Further, population shifts into the WUI are increasing the proximity of property to places prone to fire, helping to explain the rise in wildfire’s increased percentage of insured losses.

CSAA Insurance Group – a AAA insurer – is spurring innovation in the insurance industry through several initiatives tackling the dangers of climate risk.

“We’ve been on a journey to reduce our environmental footprint for a long time,” said Debbie Brackeen, Chief Strategy & Innovation Officer with CSAA, in a recent executive exchange with Triple-I CEO Sean Kevelighan. “We are seeking to reduce our carbon footprint by 50 percent by 2025. We view this work as aligned with our mission: to help our members prepare for and recover from climate risk.”

CSAA has taken several steps to help achieve its goals, including:

Leading the first-ever Innovation Challenge on climate resilience with IDEO and Aon, along with several other sponsors;

Working on the California Innovation Fund in partnership with Blue Forest, a $50 million fund that CSAA contributed half that capital, focused on forest restoration and reducing fuel in a smart and sustainable way; and

Supporting the Wildfire Interdisciplinary Research Center at San Jose State University, which conducts work around predictive modeling, among other endeavors.

While this may seem like a new development, Kevelighan noted that insurers have long worked toward these goals.

“We’ve seen the ESG movement take a hold in the past few years, but it’s been in the DNA of the Triple-I and the insurance industry generally for a long time,” Kevelighan said. “More than half the battle is recognizing that the risk is increasing, while identifying solutions.”

Still, with the increasing consequences associated with climate risk, more work needs to be done.

“There were billion-dollar wildfire losses at CSAA in my first two years in the industry,” Brackeen said. “I wondered if this was normal. It ignited in me that, whatever we do in innovation, it will have to do with wildfire risk. However, what concerns me the most is that risks are becoming uninsurable. This is from the cumulative effects of several different types of losses, including convective storms.”

“We have to seek different types of innovative partnerships to address these issues,” Brackeen concluded. “In this fight for our industry, there are no competitors. We have to be on the same side of the table.”

By Jeff Dunsavage, Senior Research Analyst, Triple-I

I’m pleased and proud to have been part of Triple-I’s Town Hall — “Attacking the Risk Crisis” — in Washington, D.C. In an intimate setting at the Mayflower Hotel on November 30, 120-plus attendees got to hear from experts representing insurance, government, academia, nonprofits, and other stakeholder groups on climate risk, what’s being done to address it, and what remains to be done.

Triple-I’s first-ever Town Hall was designed as a logical step in its multi-disciplinary, action-oriented effort to change behavior to drive resilience. Capping a year in which headlines about “insurance crises” in several states garnered major media attention, Triple-I and its members and partners recognized the need for clarification.

“What we’re seeing is not an ‘insurance crisis’,” Triple-I CEO Sean Kevelighan told the standing-room-only audience. “We’re in the midst of a risk crisis. Rising insurance premium rates and availability difficulties are not the cause but a symptom of this crisis.”

Whisker Labs CEO Bob Marshall discusses innovation with moderator Jennifer Kyung, Vice President and Chief Underwriter at USAA.

While the insurance industry has a critical role to play and is uniquely well equipped to lead the attack, simply transferring risk is not enough. A recurring theme at the Town Hall was the need to shift from a focus on assessing and repairing damage to one of predicting and preventing losses.

Three moderated discussions – examining the nature of climate risk and its costs; highlighting the need of strategic innovation in mitigating those risks and building resilience; and exploring the role and impact of government policy – gave panelists the opportunity to share their insights with a diverse audience focused on collaborative action.

The agenda was:

Climate Risk Is Spiraling: What Can Be Done?

Moderator: David Wessel, Senior Fellow and Director at the Brookings Institution and former Economics Editor for The Wall Street Journal.

Panelists:

Dr. Philip Klotzbach, Colorado State University, researcher and Triple-I non-resident scholar.

Dan Kaniewski, Managing Director, Public Sector at Marsh McLennan, Former FEMA Deputy Administrator.

Jacqueline Higgins, Head, North America & Senior Vice President, Public Sector Solutions, Swiss Re

Jim Boccher, Chief Development Officer, ServiceMaster.

Jeff Huebner, Chief Risk Officer, CSAA.

Innovation, High- and Low-Tech: How Insurers Are Driving Solutions

Moderator: Jennifer Kyung, VP, Chief Underwriter, USAA.

Panelists:

Partha Srinivasa, EVP, CIO, Erie Insurance.

Sam Krishnamurthy, CTO, Digital Solutions, Crawford.

Bob Marshall, CEO, Whisker Labs.

Stephen DiCenso, Principal,Milliman.

Charlie Sidoti, Executive Director, InnSure.

Outdated Regs to Legal System Abuse: It Will Take Villages to Fix This

Parr Schoolman, SVP and Chief Risk Officer, Allstate.

Tim Judge, SVP, Head Modeler, Chief Climate Officer, Fannie Mae.

Dan Coates, Deputy Director, DRS, Federal Housing Finance Agency.

Fred Karlinsky, Co-Chair of Greenberg Traurig’s Global Insurance Regulatory & Transactions Practice Group.

Panelists and participants alike appreciated the compact, action-focused, conversational nature of the single-afternoon event, as well as the opportunity to discuss areas in which their diverse industry- or sector-specific priorities and efforts overlapped.

If you weren’t able to join us in Washington, don’t worry. In his closing remarks, Kevelighan announced plans to take the program on the road with a local and regional focus, so stay tuned. You can contact us if you’re interested in participating in future Town Halls or other Triple-I events. You also can join the “Attacking the Risk Crisis” LinkedIn Group to be part of the ongoing conversation.

By Kelley Collins, Director of Business Development and Communications, Lightning Protection Institute

Our lives are filled with risk assessment and mitigation. From grabbing an umbrella for a rainy day to stocking up on supplies for an impending natural disaster, we assess and measure the potential risks before an event occurs to be prepared and protect ourselves from unwanted consequences.

For many, however, assessing and mitigating lighting risk isn’t necessarily top of mind. We know lightning is going to strike – more than 31 million cloud-to-ground strikes occur annually. But being personally affected seems so unlikely that people may think preparation isn’t necessary or even possible. Understanding how to mitigate risks associated with lightning is essential to individuals and property owners.

Lightning strikes about 100 times every second. Incorporate assessment of lightning risk into our daily lives.

Impact of Lightning: Homes, Businesses, Critical Facilities

About 6,000 times a minute, there is a lightning strike that contains an electrical discharge hotter than the sun. One strike can cause immense damage that goes beyond fire. The damage to the electrical infrastructure and the electronics connected to that infrastructure can be destroyed – bringing communication, security and productivity to a halt.

Convective storms – which are associated with thunder, lightning, and other weather changes – caused $38 billion in insured losses in the first half of 2023.

“Assessing your risk to lightning before a storm enables homeowners and business owners to predict and mitigate their risks to losses due to a lightning strike,” said Triple-I CEO Sean Kevelighan.

If any of the following structures are hit by lightning, there are consequences beyond the repairs from a fire. When there are surges and/or damages to the electrical system, here are just a few consequences that impact time, money, and – in the worst cases – can cost lives:

Homes: Costly repairs and equipment replacement (TVs, washer/dryer, computers);

Businesses: Emails and communication stopped, production downtime and loss of revenue; and

Critical Facilities: Inability to meet the emergencies of individuals or the community.

Lightning protection systems are scientifically proven to mitigate these risks. When properly installed, a lightning protection system makes a building resilient to the damage of lightning strike. These systems protect the structure, the electrical system, and the humans within the building.

Lightning risk assessment

From homeowners to design/build experts, learning how to measure and mitigate the risks of lightning is vital to the prevention of lightning damage. For personal safety, assess the current and future weather conditions; if you see lightning, get indoors. For protecting homes, buildings, and structures, there are a few ways to conduct an assessment to determine the risks of lightning. If the assessment determines that there are perceived risks of lightning, lightning protection systems can be installed to mitigate those risks.

Key assessment factors

The NFPA 780 standard for lightning protection is one option that offers a simple and complex approach to assessments. At the advanced level, an assessment involves a complex equation with several variables (ie., Nd= Ngx Aex C1 x10-6). At the very least, consider the key assessment factors within three general areas of a structure:

External criteria

Structure, design, and use

Internal activity

External Criteria

When you first walk up to a building or structure, scan the surroundings and conduct a visual inspection. This involves identifying potential lightning strike paths, such as tall trees, antennas, or nearby structures. Evaluate the building’s height and design. Now, assess how that structure compares to other buildings or objects near it.

Is it the tallest building?

Is it situated on a hill or by itself?

If you are designing a new building, assess how that building will be incorporated into these surroundings to ensure proper consideration for making that building more sustainable to a lightning strike.

What is the propensity for lightning strikes in that city, county, or state? Different regions have varying levels of lightning activity, and this information is crucial in determining the necessary level of protection. Lightning frequency data can be obtained from local weather services or scientific experts, such as Vaisala, who collect data on lightning activity.

Structure Design and Use

Evaluate the materials and use of the building.

What are the building materials: Glass, wood, brick, etc.?

Does the design impact the propensity for a lightning strike: Taller points or roof attachments?

What is the use of the building:

Does it contain hazardous or flammable objects?

Does it store valuable and/or historical objects?

Does it perform critical services?

Internal Activity

Identify people and activity on the inside of the structure.

Are there many people inside this structure?

What’s the likely panic level if a building evacuation is necessary?

Can the people move quickly? For instance: In a nursing home or hospital, all occupants cannot quickly exit a building that was hit by lightning. In a large high-rise with large groups of occupants, a speedy exit may not be possible.

What is the building’s function? Identify the services that are being conducted in that building. If lightning hits the structure you are assessing, what happens to the people and services inside? Here are some key structures to protect in high-risk areas:

Data centers

Distribution centers

Schools and churches

Public works facilities

Critical facilities, such as fire, police, hospitals, emergency operation centers

Assessment leads to mitigation and protection. Having a general understanding of a lightning risk assessment enables all of us to make better choices. Individuals and homeowners can protect themselves and their homes. Design/build experts and facility managers can make choices to ensure their buildings are more resilient, sustainable, and safer with lightning protection systems.

Proper steps for a formal assessment and installation

If your general assessment leads you to question the structure’s vulnerability, the NFPA 780 guidelines specify that the formal assessment process should be carried out by qualified professionals who are knowledgeable about lightning protection systems. These professionals may include lightning protection system designers, engineers, or certified installers who have undergone specific training and have a comprehensive understanding of the guidelines.

By following the lightning assessment process outlined by NFPA 780, property owners can ensure that their lightning protection systems are properly designed, installed, and maintained. Proper installation protects structures from the devastating effects of lightning strikes and promotes the safety of individuals inside.

Nature-based solutions, green jobs, and resilient infrastructure are at the core of Liberty Mutual Foundation’s approach to helping marginalized communities that are most vulnerable to climate-related perils.

“We believe investing philanthropically in communities to help them mitigate and adapt to the impact of climate change is a natural extension that we do as a property-casualty insurer and an area where we can offer a lot of expertise,” Foundation President Melissa MacDonnell told Triple-I CEO Sean Kevelighan in a recent Triple-I Executive Exchange.

MacDonnell described the foundation’s three-pronged approach to community giving, which consists of:

Nature-based solutions, such as increasing access to locally grown food and green space to protect communities from sea-level rise or flooding;

Green jobs that provide training and skill development in the green economy for low-income and underrepresented youth and young adults; and

Resilient infrastructure for low-income neighborhoods and communities of color.

The foundation also supports existing partners in advancing their climate resiliency goals.

“Any organization in our philanthropic portfolio is eligible for these grants, so they can step back and consider how climate is impacting them,” MacDonnell said. “This includes homelessness shelters and job programs. This is our way of acknowledging that climate affects all of us.”

Kevelighan noted that this holistic approach is particularly important for residents of vulnerable communities.

“We’ve been talking at Triple-I about the role everyone plays in climate,” he said. “It’s encouraging that you’re bringing risk management into communities – particularly those that can’t provide themselves enough resources.”

Kevelighan and MacDonnell discussed how other insurers can become more involved in helping vulnerable communities.

“Insurers should carve out the time to listen to the communities” MacDonnell said. “Partnering with communities and public officials is also important. We are at an incredible moment in time where federal funding is available for climate projects” as a result of measures like the Community Disaster Resilience Zones Act of 2022, which aims to build disaster resilience by identifying disadvantaged communities that are most at risk to natural disasters and providing funding for projects that mitigate those risks.

Economic turbulence, political unrest, climate catastrophes, and the aftermath of a global pandemic are just a few of the forces demanding that everyone – homeowners, consumers, businesses, and policymakers, as well as risk-management professionals – take responsibility for understanding and reducing the perils facing all of us, Triple-I CEO Sean Kevelighan said in a recent episode of the Predict & Prevent podcast.

Triple-I CEO Sean Kevelighan

“We’re simply living more and more in harm’s way,” Kevelighan told Peter Miller, president and CEO of The Institutes and host of the podcast, which explores how innovators are combating some of the biggest risk challenges facing society by working to eliminate losses before they occur. “We’re a riskier society in terms of our behavior, and this is placing pressure on the traditional risk-transfer tool that is insurance.”

“Even before we got into COVID, severity in catastrophes, both natural and manmade, had been increasing,” Kevelighan said. The two CEOs discussed this growth in severity and what it means for insurers and the policyholders they protect.

“There’s little doubt that predict and prevent is urgently needed,” Miller said. “But the big question remains how? How can we put these principles and practices into action?”

Among other things, Kevelighan talked about the role of telematics and the Internet of Things in helping policyholders anticipate losses and mitigate them in advance by making investments or changing their behaviors. Automobile telematics, for example, shouldn’t simply be about getting discounted insurance premiums.

“It should be about helping people become safer drivers,” Kevelighan said.

Predicting and preventing costly losses has to involve collective responsibility by all parties. It’s no longer enough to simply buy an insurance policy and rest comfortably in the knowledge that, if something bad happens, you’ll get a payout. A change in mindset is required.

As Kevelighan put it, “Nobody wins from a loss.”

The Predict & Prevent podcast can be found on Apple Podcasts, Spotify, Google Podcasts, and Stitcher. Other recent episodes include:

Of the findings in Triple-I’s recent report on consumer perceptions of weather risk, the Weather Channel’s experts were most struck by the fact that 60 percent of homeowners said they’d taken no steps to prepare – so, they asked Triple-I Chief Insurance Officer Dale Porfilio for his perspective.

Ultimately, Porfilio said, it comes down to perceptions.

“Two thirds of the people surveyed said they don’t expect to be affected by weather risk in the next five years,” Porfilio told the Weather Channel. “If you don’t think you’re going to be impacted, why would you prepare with a home evacuation plan or a home inventory?”

Of course, anyone who is exposed to weather is exposed to weather-related risk, and it’s essential for homeowners to understand and address the most relevant risks in order to protect their investments and their families.

Porfilio also addressed a question regarding availability of flood insurance, explaining that coverage is generally available through the Federal Emergency Management Agency’s National Flood Insurance Program, as well as a growing number of private insurers, but “might be perceived as too expensive.”

It is possible, however, that some insurers might not be willing to offer coverage in areas that have been hit repeatedly by flood.

Awareness and preparation are key. The Triple-I survey, published in coordination with global reinsurer Munich Re, found that, among the 22 percent of respondents who reported understanding their level of flood risk, 78 percent said they had purchased flood insurance. The report, Homeowners Perception of Weather Risks, provides insights into trends, behavior and how experiencing a weather event impacts consumer perceptions of future events.

Of all the challenges facing property casualty insurers today – from growing catastrophe losses to social inflation – Church Mutual president Alan Ogilvie sees the “war for talent” as one of the most pressing.

“For us, the old adage is very true. Our best assets walk in the door in the morning, at the end of the day they leave, and you just hope and pray they come back,” Ogilvie said in a recent Executive Exchange conversation with Triple-I CEO Sean Kevelighan.

Ogilvie called talent acquisition and retention “our number one challenge.”

“We like to think we bring something a little bit unique to our employees, and that’s a sense of mission,” he said.

He pointed to Church Mutual’s status as 126-year-old mutual company – the largest writer of insurance for religious institutions, which has expanded to include coverage for health, educational, and nonprofit organizations – and said, “It’s pretty easy to get up in the morning when you’re protecting organizations that you know are doing tremendous things in our communities.”

Ogilvie is committed to busting the myth that insurance is a boring business. Among the features of insurance he emphasizes to people early in their careers is the focus on technology and addressing the challenges of climate risk. Catastrophe management – viewed through the lens of artificial intelligence and predictive analytics – has become a cutting-edge discipline.

This, combined with the fact that many insurance professionals are expected to be retiring over the next decade, “creates an incredible amount of opportunity,” Ogilvie said.

The 2023 Atlantic hurricane season officially started June 1 and is forecast to be a busy one, which is why homeowners need to prepare. Yet many lack even the most basic preventative measures, unaware of the risks they face, according to a new survey by Triple-I, in coordination with Munich Re.

The new report, Homeowners Perception of Weather Risks,provides insights into trends, behavior and how experiencing a weather event impacts consumer perceptions of future events.

In the first half of 2023, Triple-I, in coordination with Munich Re, asked homeowners across the United States about their experiences with weather-related risks. Among the key findings:

Twenty-five percent of respondents don’t expect to be impacted by weather risks in the future.

Thirty-two percent report that they have been impacted by weather in the last five years.

Two primary ways to prepare for weather risk includes creating a home inventory and an evacuation plan in case of emergency. Yet only 47 percent of respondents have a home inventory and slightly more (52 percent) have an evacuation plan.

Thunderstorms are reported as the chief weather concern, at 54 percent nationally. This includes flooding and tornados and varies by geographic region. The Midwest leads the area of highest reported thunderstorm risk, at 75 percent, and the West region reports the lowest proportion of concern, at 33 percent.

The survey suggests awareness and education around flood risk are the greatest opportunity for getting homeowners to take the necessary steps to protect their property. For example, among the 22 percent of respondents who reported understanding their flood risk, 78 percent said they had purchased flood insurance.

Lightning is a more complex peril than it is often given credit for being, according to Tim Harger, executive director of the Lightning Protection Institute (LPI). In a recent interview with Triple-I CEO Sean Kevelighan, Harger discussed the importance of preparing for and preventing damage from this risk, which is second only to flooding when it comes to costly weather events.

People typically think about fire damage when they think about lightning. But Harger said, “Beyond the fire is the destruction of electrical wires and infrastructure that supports everything we do to communicate and to conduct business.”

If lighting strikes any of these structures, he said, “Activity is stopped.”

Harger cited the case of an East Coast furniture manufacturer that was struck.

“That one lightning strike cost them just over a million dollars in damage,” he said. “Yes, there was the typical fire that caused structural damage, but what was impacted on the ‘inside’ was even more costly. They had damaged inventory, production downtime, and loss of revenue during the repairs.”

Investment in a lightning protection system could have saved this business owner – and his insurer – the million dollars lost and prevented business interruption. Nearly $1 billion in lightning claims was paid out in 2018 to almost 78,000 policy holders, according to LPI.

“Lightning strikes about a 100 times every second,” Harger said. “When installed properly, lightning protection systems are scientifically proven to mitigate the risks of a lightning strike.”

A lightning protection system consists of six parts:

Strike termination device,

Conductors,

Grounding,

Surge protection,

Potential equalization, and

Inspection.

Architects and engineers play an important role in specifying and designing these systems, and installation is completed by certified lightning protection contractors. When properly installed lightning is intercepted by the strike termination device and energy is routed through the conductors and into the grounding system, preventing impact to the structure or electrical infrastructure.

“Businesses already install fire alarms and sprinkler systems to mitigate greater risks of fires,” Harger said. “Lightning protection systems prevent a lightning strike from causing any damage. So the investment in a lightning protection system prevents personal injury and the costly impact of even one strike.”

Several insurers offer premium discounts for policyholders who invest in lightning protection systems. LPI invites insurance providers who are interested in sharing their customer incentives to contact them at lpi@lightning.org.