By Lewis Nibbelin, Contributing Writer, Triple-I

U.S. property claims volume rose 36 percent in 2024, propelled by a 113 percent increase in catastrophe claims, according to a recent Verisk Analytics report.

While evolving climate risks fueled claim frequency, uncertain inflation trends and unchecked legal system abuse will likely further strain insurer costs and time to settle these claims, posing risks to coverage affordability and availability.

Abnormally active Atlantic hurricane season

In a “dramatic shift” from previous loss patterns, late-season hurricane activity – rather than winter storms – dictated fourth-quarter claims operations last year, Verisk reported. Hurricane-related claims comprised nearly 9 percent of total claims volume, at a staggering 1,100 percent increase from the third quarter of 2023. Flood and wind claims both also jumped by 200 percent in volume.

“This shift in risk patterns demands new approaches to risk assessment and resource planning, particularly in the Southeast, where costs increased at six times the national rate following hurricane activity,” Verisk stated. Notably, Hurricane Milton generated roughly 187,000 claims totaling $2.68 billion in replacement costs across the Southeast, with 8 percent of claims still outstanding as of the report’s release.

Another above-average hurricane season is projected for 2025 in the Atlantic basin, according to a forecast by Colorado State University’s (CSU) Department of Atmospheric Science. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach, the CSU research team forecasts 17 named storms, including nine hurricanes – four of them “major” – during the 2025 season, which begins June 1 and continues through Nov. 30. A typical Atlantic season has 14 named storms, seven hurricanes, three of them major. Major hurricanes are defined as those with wind speeds reaching Category 3, 4, or 5 on the Saffir-Simpson Hurricane Wind Scale.

Water, hail, and wind events in the Great Plains and Pacific Northwest also contributed to unexpected claim volumes, Verisk added. In contrast, wind-related claims fell in the Northeast compared to the fourth quarter of 2023.

Such regional variations highlight “the importance of granular, location-specific analysis for accurate risk assessment,” Verisk stated.

Contributing economic factors

Labor and material costs continued to rise year over year, with commercial reconstruction costs seeing a more pronounced increase of 5.5 percent compared to residential’s 4.5 percent, Verisk reported. The firm projected moderate reconstruction cost increases within both sectors during the first half of 2025.

Looming U.S. tariffs, however, may complicate this trajectory. Inflationary pressures related to the Trump Administration’s tariffs could further disrupt supply chains still recovering from natural catastrophes and the COVID-19 pandemic. Any such disruptions would compound replacement costs for U.S. auto and homeowners insurers as material costs – such as lumber, a major import from Canada – become even more expensive.

Excessive litigation trends

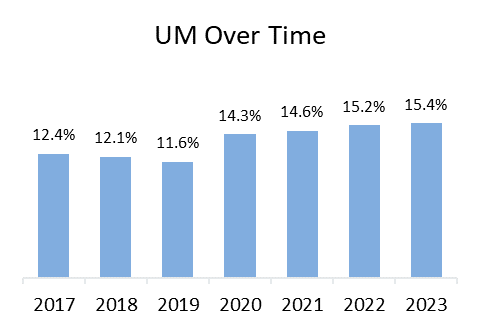

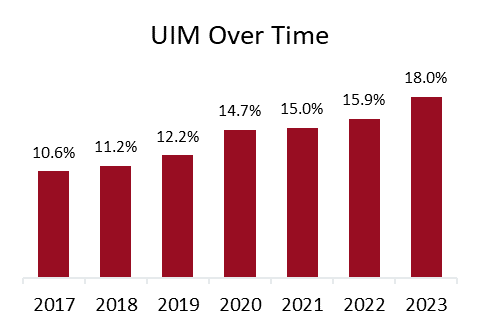

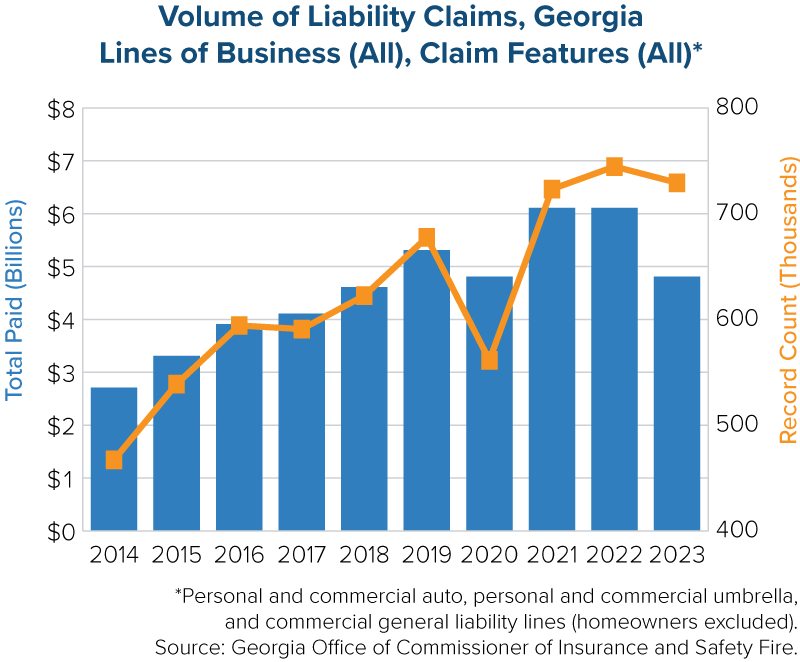

Similarly, excessive claims litigation – which prolongs claims disputes while driving up claim costs – plagues several of the states Verisk identified as experiencing increased claim volumes. For instance, though hurricane activity helps explain higher claim frequency in Georgia, the Peach State also is home to a personal auto claim litigation rate more than twice that of the median state, with a relative bodily injury claim frequency 60 percent higher than the U.S. average.

Verisk’s preliminary Q4 data reveals a 7 percent decrease in average claims severity compared to the same period in 2023 – a figure the firm expects to rise as more complex claims reach completion. But costly and protracted claims litigation, paired with ongoing tariff uncertainty, could magnify this figure even beyond their projections.

Undoubtedly, both will challenge insurers’ capacity to reliably predict loss trends and set fair and accurate premium rates for the foreseeable future, underscoring Verisk’s point that “staying ahead of these evolving patterns is essential in building more resilient operations in the future.”

Learn More:

Tenfold Frequency Rise for Coastal Flooding Projected by 2050

How Tariffs Affect P&C Insurance Prospects

What Florida’s Misguided Investigation Means for Georgia Tort Reform

Florida Bills Would Reverse Progress on Costly Legal System Abuse

Florida Reforms Bear Fruit as Premium Rates Stabilize

Georgia Targets Legal System Abuse

Severe Convective Storm Risks Reshape U.S. Property Insurance Market

New Triple-I Issue Brief Puts the Spotlight on Georgia’s Insurance Affordability Crisis

P/C Replacement Costs Seen Outpacing CPI in 2025

California Insurance Market at a Critical Juncture

Florida’s Progress in Legal Reform: A Model for 2025

Louisiana Reforms: Progress, But More Is Needed to Stem Legal System Abuse

Data Fuels the Assault on Climate-Related Risk

California Finalizes Updated Modeling Rules, Clarifies Applicability Beyond Wildfire

U.S. Consumers See Link Between Attorney Involvement in Claims and Higher Auto Insurance Costs