The Institutes’ Pete Miller and Francis Bouchard of Marsh McLennan discuss how AI is transforming property/casualty insurance as the industry attacks theclimate crisis.

“Climate” is not a popular word in Washington, D.C., today, so it would take a certain audacity to hold an event whose title prominently includes it in the heart of the U.S. Capitol.

For two days, expert panels at the Ronald Reagan Building and International Trade Center discussed climate-related risks – from flood, wind, and wildfire to extreme heat and cold – and the role of technology in mitigating and building resilience against them. Given the human and financial costs associated with climate risks, it was appropriate to see the property/casualty insurance industry strongly represented.

Peter Miller, CEO of The Institutes, was on hand to talk about the transformative power of AI for insurers, and Triple-I President and CEO Sean Kevelighan discussed – among other things – the collaborative work his organization and its insurance industry members are doing in partnership with governments, non-profits, and others to promote investment in climate resilience. Triple-I is an affiliate of the Institutes.

Sean Kevelighan of Triple-I and Denise Garth, Majesco’s chief strategy officer, discuss how to ensure equitable coverage against climate events.

You can get an idea of the scope and depth of these panels by looking at the agenda, which included titles like:

Building Climate-Resilient Futures: Innovations in Insurance, Finance, and Real Estate;

Fire, Flood, and Wind: Harnessing the Power of Advanced Data-Driven Technology for Climate Resilience;

The Role of Technology and Innovation to Advance Climate Resilience Across our Cities, States and Communities;

Pioneers of Parametric: Navigating Risks with Parametric Insurance Innovations;

Climate in the Crosshairs: How Reinsurers and Investors are Redefining Risk; and

Safeguarding Tomorrow: The Regulator’s Role in Climate Resilience.

As expected, the panels and “fireside chats” went deep into the role of technology; but the importance of partnership, collaboration, and investment across stakeholder groups was a dominant theme for all participants. Coming as the Trump Administration takes such steps as eliminating FEMA’s Building Resilient Infrastructure and Communities (BRIC) program; slashing budgets of federal entities like the National Oceanographic and Atmospheric Administration (NOAA) and the National Weather Service (NWS); and revoking FEMA funding for communities still recovering from last year’s devastation from Hurricane Helene, these discussions were, to say the least, timely.

Helge Joergensen, co-founder and CEO of 7Analytics, talks about using granular data to assess and address flood risk.

In addition to the panels, the event featured a series of “Shark Tank”-style presentations by Insurtechs that got to pitch their products and services to the audience of approximately 500 attendees. A Triple-I member – Norway-based 7Analytics, a provider of granular flood and landslide data – won the competition.

Earth Day 2025 is a good time to recognize organizations that are working hard and investing in climate-risk mitigation and resilience – and to recommit to these efforts for the coming years. What better place to do so than walking distance from both the White House and the Capitol?

The Trump Administration’s unwinding of the Building Resilient Infrastructure and Communities (BRIC) program and cancellation of all BRIC applications from fiscal years 2020-2023 reinforce the need for collaboration among state and local government and private-sector stakeholders in climate resilience investment.

Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters. FEMA announced on April 4 that it is ending BRIC .

Chad Berginnis, executive director of the Association of State Floodplain Managers (ASFPM), called the decision “beyond reckless.”

“Although ASFPM has had some qualms about how FEMA’s BRIC program was implemented, it was still a cornerstone of our nation’s hazard mitigation strategy, and the agency has worked to make improvements each year,” Berginnis said. “Eliminating it entirely — mid-award cycle, no less — defies common sense.”

While the FEMA press release called BRIC a “wasteful, politicized grant program,” Berginnis said investments in hazard mitigation programs “are the opposite of ‘wasteful.’ “ He pointed to a study by the National Institute of Building Sciences (NIBS) that showed flood hazard mitigation investments return up to $8 in benefits for every $1 spent.

“At this very moment, when states like Arkansas, Kentucky, and Tennessee are grappling with major flooding, the Administration’s decision to walk away from BRIC is hard to understand,” Berginnis said.

Heading into hurricane season

Especially hard hit will be catastrophe-prone Florida. Nearly $300 million in federal aid meant to help protect communities from flooding, hurricanes, and other natural disasters has been frozen since President Trump took office in January, according to an article in Government Technology.

The loss of BRIC funding leaves dozens of Florida projects in limbo, from a plan to raise roads in St. Augustine to a $150 million effort to strengthen canals in South Florida. According to Government Technology, the agency most impacted is the South Florida Water Management District, responsible for maintaining water quality, controlling the water supply, ecosystem restoration and flood control in a 16-county area that runs from Orlando south to the Keys.

“The district received only $6 million of its $150 million grant before the program was canceled,” the article said. “The money was intended to help build three structures on canals and basins in North Miami -Dade and Broward counties to improve flood mitigation.”

Florida’s Division of Emergency Management must return $36.9 million in BRIC money that was earmarked for management costs and technical assistance. Jacksonville will lose $24.9 million targeted to raise roads and make improvements to a water reclamation facility.

FEMA announced the decision to end BRIC the day after Colorado State University’s (CSU) Department of Atmospheric Science released a forecast projecting an above-average Atlantic hurricane season for 2025. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach CSU research team forecasts 17 named storms, nine hurricanes – four of them “major” (Category 3, 4, or 5). A typical season has 14 named storms, seven hurricanes – three of them major.

Nationwide impacts

More than $280 million in federal funding for flood protection and climate resilience projects across New York City — “including critical upgrades in Central Harlem, East Elmhurst, and the South Street Seaport” – is now at risk, according to an article in AMNY. The cuts affect over $325 million in pending projects statewide and another $56 million of projects where work has already begun.

Senate Majority Leader Chuck Schumer and Gov. Kathy Hochul warned that the move jeopardizes public safety as climate-driven disasters become more frequent and severe.

“In the last few years, New Yorkers have faced hurricanes, tornadoes, blizzards, wildfires, and even an earthquake – and FEMA assistance has been critical to help us rebuild,” Hochul said. “Cutting funding for communities across New York is short-sighted and a massive risk to public safety.”

According to the National Association of Counties, cancellation of BRIC funding has several implications for counties, including paused or canceled projects, budget and planning adjustments, and reduced capacity for long-term risk reduction.

North Dakota, for example, has 10 projects that were authorized for federal funding. Those dollars will now be rescinded. Impacted projects include $7.1 million for a water intake project in Washburn; $7.8 million for a regional wastewater treatment project in Lincoln; and $1.9 million for a wastewater lagoon project in Fessenden.

“This is devastating for our community,” said Tammy Roehrich, emergency manager for Wells County. “Two million dollars to a little community of 450 people is huge.”

The cancellation of BRIC roughly coincides with FEMA’s decision to deny North Carolina’s request to continue matching 100 percent of the state’s spending on Hurricane Helene recovery.

“The need in western North Carolina remains immense — people need debris removed, homes rebuilt, and roads restored,” said Gov. Josh Stein. “Six months later, the people of western North Carolina are working hard to get back on their feet; they need FEMA to help them get the job done.”

Resilience key to insurance availability

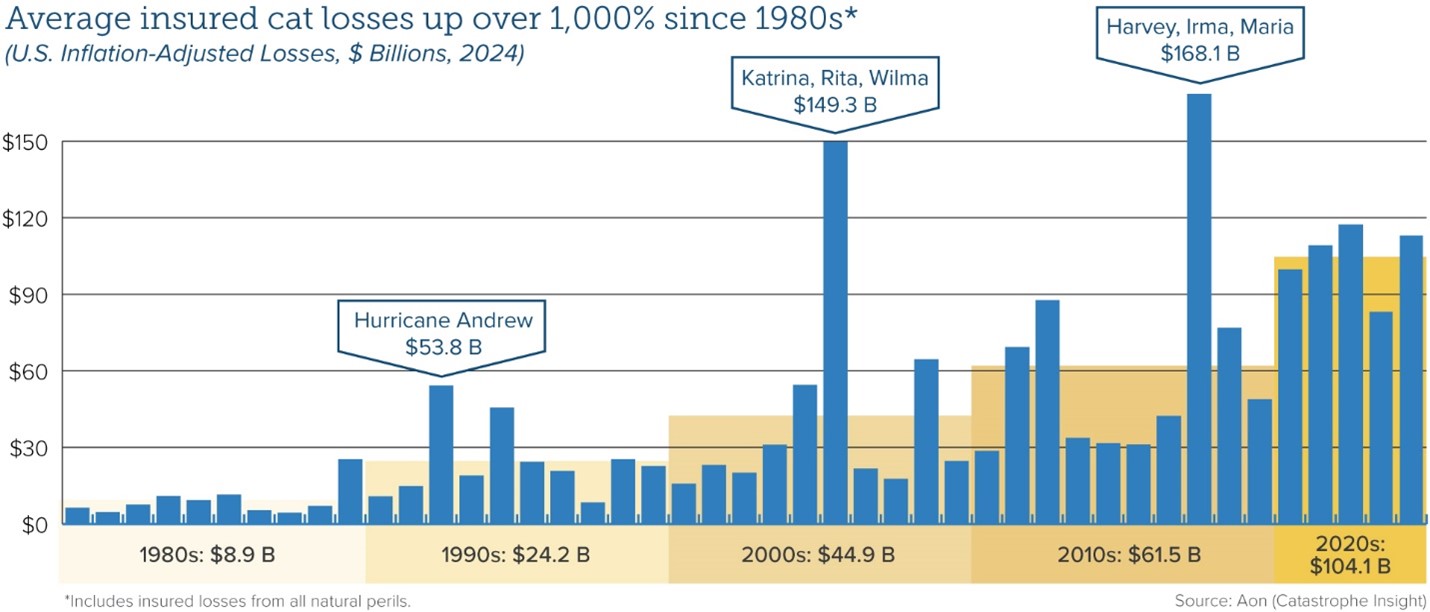

Average insured catastrophe losses have been on the rise for decades, reflecting a combination of climate-related factors and demographic trends as more people have moved into harm’s way.

“Investing in the resilience of homes, businesses, and communities is the most proactive strategy to reducing the damage caused by climate,” said Triple-I Chief Insurance Officer Dale Porfilio. “Defunding federal resilience grants will slow the essential investments being made by communities across the U.S.”

Flood is a particularly pressing problem, as 90 percent of natural disasters involve flooding, according to the National Flood Insurance Program (NFIP). The devastation wrought by Hurricane Helene in 2024 across a 500-mile swath of the U.S. Southeast – including Florida, Georgia, the Carolinas, Virginia, and Tennessee – highlighted the growing vulnerability of inland areas to flooding from both tropical and severe convective storms, as well as the scale of the flood-protection gap in non-coastal areas.

Coastal flooding in the U.S. now occurs three times more frequently than 30 years ago, and this acceleration shows no signs of slowing, according to recent research. By 2050, flood frequency is projected to increase tenfold compared to current levels, driven by rising sea levels that push tides and storm surges higher and further inland.

In addition to the movement of more people and property into harm’s way, climate-related risks are exacerbated by inflation (which drives up the cost of repairing and replacing damaged property); legal system abuse, (which delays claim settlements and drives up insurance premium rates); and antiquated regulations (like California’s Proposition 103) that discourage insurers from writing business in the states subject to them.

Thanks to the engagement and collaboration of a range of stakeholders, some of these factors in some states are being addressed. Others – for example, improved building and zoning codes that could help reduce losses and improve insurance affordability – have met persistent local resistance.

As frequently reported on this blog, the property/casualty insurance industry has been working hard with governments, communities, businesses, and others to address the causes of high costs and the insurance affordability and availability challenges that flow from them. Triple-I, its members, and partners are involved in several of these efforts, which we’ll be reporting on here as they progress.

Even as California moves to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing, the state’s risk profile continues to evolve in ways that impede progress, according to the most recent Triple-I Issues Brief.

Like many states, California has suffered greatly from climate-related natural catastrophe losses. Like some disaster-prone states, it also has experienced a decline in insurers’ appetite for covering its property/casualty risks.

But much of California’s problem is driven by regulators’ application of Proposition 103 – a decades-old measure that constrains insurers’ ability to profitably write business in the state. As applied, Proposition 103 has:

Kept insurers from pricing catastrophe risk prospectively using models, requiring them to price based on historical data alone;

Barred insurers from incorporating reinsurance costs into pricing; and

Allowed consumer advocacy groups to intervene in the rate-approval process, making it hard for insurers to respond quickly to changing market conditions and driving up administration costs.

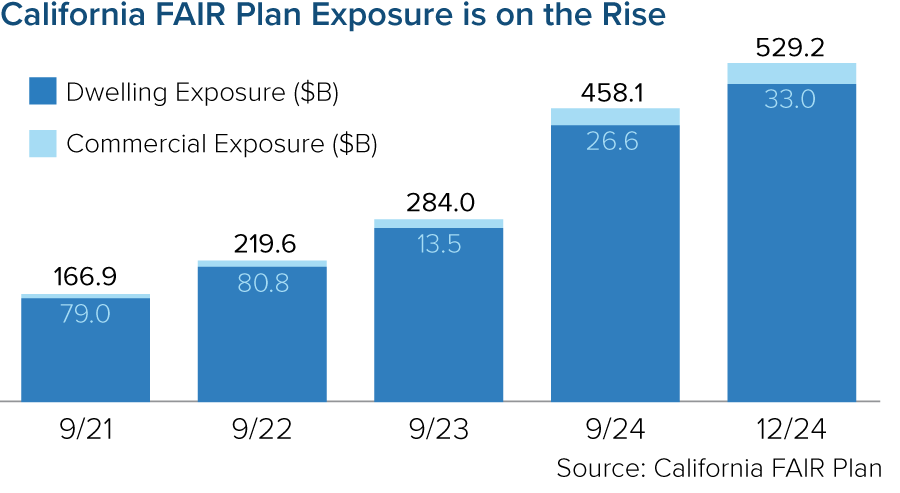

As insurers have adjusted their risk appetite to reflect these constraints, more property owners have been pushed into the California FAIR plan – the state’s property insurer of last resort. As of December 2024, the FAIR plan’s exposure was $529 billion – a 15 percent increase since September 2024 (the prior fiscal year end) and a 217 percent increase since fiscal year end 2021. In 2025, that exposure will increase further as FAIR begins offering higher commercial coverage for larger homeowners, condominium associations, homebuilders and other businesses.

Insurance Commissioner Ricardo Lara has implemented a Sustainable Insurance Strategy to alleviate these pressures. The strategy has generated positive impacts, but it continues to meet resistance from legislators and consumer groups. And, regardless of what regulators or legislators do, California homeowners’ insurance premiums will need to rise.

The Triple-I brief points out that – despite the Golden State’s many challenges – its homeowners actually enjoy below-average home and auto insurance rates as a percentage of median income. Insurance availability ultimately depends on insurers being able to charge rates that adequately reflect the full impact of increasing climate risk in the state. In a disaster-prone state like California, these artificially low premium rates are not sustainable.

“Higher rates and reduced regulatory restrictions will allow more carriers to expand their underwriting appetite, relieving the availability crisis and reliance on the FAIR plan,” said Triple-I Chief Insurance Officer Dale Porfilio.

With events like January’s devastating fires, frequent “atmospheric rivers” that bring floods and mudslides, and the ever-present threat of earthquakes – alongside the many more mundane perils California shares with its 49 sister states – premium rates that adequately reflect the full impact of these risks are essential to continued availability of private insurance.

U.S. property claims volume rose 36 percent in 2024, propelled by a 113 percent increase in catastrophe claims, according to a recent Verisk Analytics report.

While evolving climate risks fueled claim frequency, uncertain inflation trends and unchecked legal system abuse will likely further strain insurer costs and time to settle these claims, posing risks to coverage affordability and availability.

Abnormally active Atlantic hurricane season

In a “dramatic shift” from previous loss patterns, late-season hurricane activity – rather than winter storms – dictated fourth-quarter claims operations last year, Verisk reported. Hurricane-related claims comprised nearly 9 percent of total claims volume, at a staggering 1,100 percent increase from the third quarter of 2023. Flood and wind claims both also jumped by 200 percent in volume.

“This shift in risk patterns demands new approaches to risk assessment and resource planning, particularly in the Southeast, where costs increased at six times the national rate following hurricane activity,” Verisk stated. Notably, Hurricane Milton generated roughly 187,000 claims totaling $2.68 billion in replacement costs across the Southeast, with 8 percent of claims still outstanding as of the report’s release.

Another above-average hurricane season is projected for 2025 in the Atlantic basin, according to a forecast by Colorado State University’s (CSU) Department of Atmospheric Science. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach, the CSU research team forecasts 17 named storms, including nine hurricanes – four of them “major” – during the 2025 season, which begins June 1 and continues through Nov. 30. A typical Atlantic season has 14 named storms, seven hurricanes, three of them major. Major hurricanes are defined as those with wind speeds reaching Category 3, 4, or 5 on the Saffir-Simpson Hurricane Wind Scale.

Water, hail, and wind events in the Great Plains and Pacific Northwest also contributed to unexpected claim volumes, Verisk added. In contrast, wind-related claims fell in the Northeast compared to the fourth quarter of 2023.

Such regional variations highlight “the importance of granular, location-specific analysis for accurate risk assessment,” Verisk stated.

Contributing economic factors

Labor and material costs continued to rise year over year, with commercial reconstruction costs seeing a more pronounced increase of 5.5 percent compared to residential’s 4.5 percent, Verisk reported. The firm projected moderate reconstruction cost increases within both sectors during the first half of 2025.

Looming U.S. tariffs, however, may complicate this trajectory. Inflationary pressures related to the Trump Administration’s tariffs could further disrupt supply chains still recovering from natural catastrophes and the COVID-19 pandemic. Any such disruptions would compound replacement costs for U.S. auto and homeowners insurers as material costs – such as lumber, a major import from Canada – become even more expensive.

Excessive litigation trends

Similarly, excessive claims litigation – which prolongs claims disputes while driving up claim costs – plagues several of the states Verisk identified as experiencing increased claim volumes. For instance, though hurricane activity helps explain higher claim frequency in Georgia, the Peach State also is home to a personal auto claim litigation rate more than twice that of the median state, with a relative bodily injury claim frequency 60 percent higher than the U.S. average.

Verisk’s preliminary Q4 data reveals a 7 percent decrease in average claims severity compared to the same period in 2023 – a figure the firm expects to rise as more complex claims reach completion. But costly and protracted claims litigation, paired with ongoing tariff uncertainty, could magnify this figure even beyond their projections.

Undoubtedly, both will challenge insurers’ capacity to reliably predict loss trends and set fair and accurate premium rates for the foreseeable future, underscoring Verisk’s point that “staying ahead of these evolving patterns is essential in building more resilient operations in the future.”

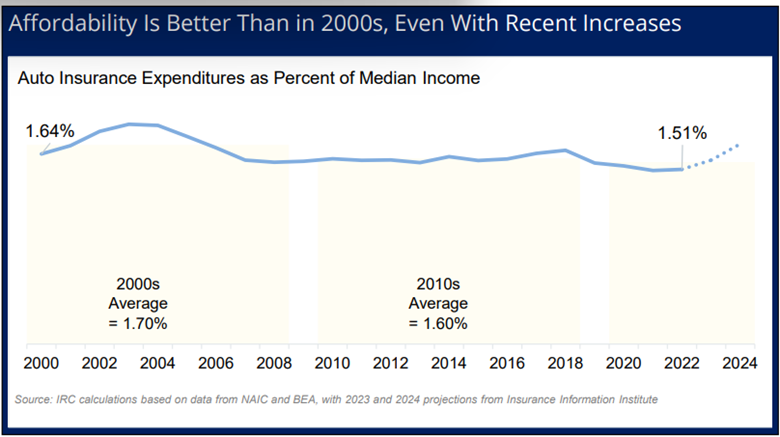

You read that right. As a percentage of median household income, personal auto insurance premiums nationally were more affordable in 2022 (the most recent data available) than they have been since the beginning of this century.

And even the premium increases of the past two years are only expected to bring affordability back into the 2000 range, according to the Insurance Research Council (IRC).

A new IRC report – Auto Insurance Affordability: Countrywide Trends and State Comparisons – looks at the average auto insurance expenditure as a percent of median income. The measure ranges from a low of 0.93 percent in North Dakota (the most affordable state for auto insurance) to a high of 2.67 percent in Louisiana (the least affordable).

The pain is real

This is not to downplay the pain being experienced by consumers – particularly those in areas where premium rates have been rising while household income has been flat to lower. It’s just to provide perspective as to the diverse factors that come into play when discussing insurance affordability.

Between 2000 and 2022, median household income grew somewhat faster than auto insurance expenditures, causing the affordability index to decline from 1.64 percent in 2000 to 1.51 percent in 2022. In other words, auto insurance was somewhat more affordable in 2022 than in 2000.

“With the recent increases in insurance costs, affordability is projected to deteriorate in 2023 and 2024,” said Dale Porfilio, FCAS, MAAA, president of the IRC and chief insurance officer at Triple-I. “The affordability index is projected to increase to approximately 1.6 percent in 2023 and 1.7 percent in 2024, a significant increase from the low in 2021 but still below the peak of 1.9 percent in 2003.”

In other words, we’ve been here before; and, if risks and costs can be contained, so can premium growth in the long term.

Cost factors vary by state

Auto insurance affordability is largely determined by the key underlying cost drivers in each state. They include:

Accident frequency

Repair costs

Claim severity

Tendency to file injury claims

Injury claim severity

Expense index

Uninsured and underinsured motorists

Claim litigation.

These factors vary widely by state, and the IRC report looks at the profiles of each state to arrive at its affordability index.

Reducing risk and costs is key

Porfilio noted that “while state-level data cannot directly address affordability issues among traditionally underserved populations, collaborative efforts to reduce these key cost drivers can improve affordability for all consumers.”

Continued replacement-cost inflation is likely to maintain upward pressure on premium rates. Tariffs could exacerbate that trend, as well as hurting household income in areas dependent on industries likely to be affected by them.

At the same time, some states are working hard to ameliorate other factors hurting affordability. Florida, for example, was the second least affordable state for auto insurance in 2022; however, the state has made recent progress to reduce legal system abuse, a major contributor to claims costs in the Sunshine State. In 2022 and 2023, Florida passed several key reforms that have led to significant decreases in lawsuits. As a result, insurers have been writing more business in the state after a multi-year exodus. This increased competition puts downward pressure on rates, which should be reflected in the IRC’s next affordability study.

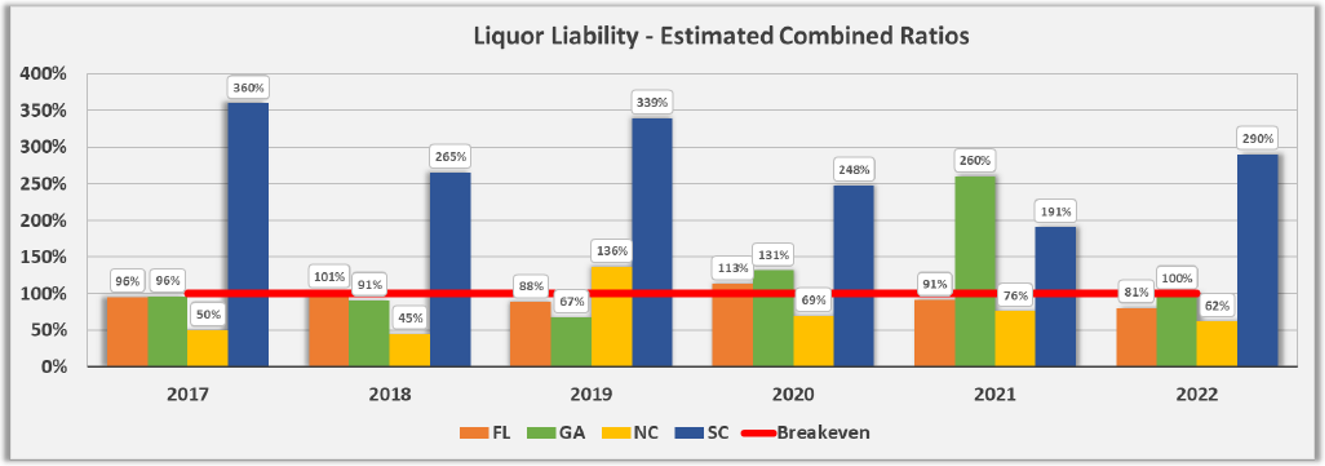

South Carolina’s liquor liability insurance market is in crisis, with insurers losing an average of $1.77 for every $1.00 of premium earned since 2017, while claim frequencies significantly outpace neighboring states, according to a recent study by the state’s Department of Insurance.

The comprehensive analysis, initiated following a 2019 request by the South Carolina Senate Judiciary Committee, reveals a deeply troubled marketplace where insurers are losing money.

“The data seem to confirm the anecdotal assertions, made by both insurance companies and small businesses, of a very troubled and challenged marketplace,” the report stated.

Current Market Landscape

The liquor liability insurance market in South Carolina has maintained a relatively stable number of participants in recent years. Since 2019, the number of insurance groups operating in this sector has held steady at around 48 participants. This consistency in market players suggests a mature, albeit challenging, insurance environment.

Despite the overall stability in participant numbers, the market is characterized by the dominance of three major insurance groups.

Premium Trends

While the number of market participants has remained relatively constant, earned premiums have experienced remarkable growth over a five-year period. From 2017 to 2022, earned premiums in the South Carolina liquor liability insurance market more than doubled to $17.0 million from $7.6 million.

This dramatic surge in premiums can be attributed to various factors, but rising insurance rates play a crucial role, the report noted.

Profitability Crisis in South Carolina

Since 2017, liquor liability insurers have lost about $1.77 for every $1.00 of premium earned over the six years observed. In the best performing of those six years (2018), the industry lost roughly $0.91 per $1.00 of premiums earned, while losing about $2.60 per $1.00 of premiums earned in the worst performing year, 2022.

“Combined ratios for the industry make it clear that this sub-line of insurance is being written at massive underwriting losses,” the report’s authors stated.

Source: South Carolina Department of Insurance

The severity of South Carolina’s liquor liability insurance crisis becomes even more apparent when compared to their neighboring states, where these same insurers have realized a net profit over time, the report noted.

Over the same 2017-2022 period analyzed, for example, North Carolina’s estimated liquor liability combined ratio ranged between 45% and 76%. In 2022, when South Carolina’s estimated combined ratio hit 290%, North Carolina’s stood at 62%.

Claims Severity and Frequency

The liquor liability insurance market in South Carolina also has experienced significant fluctuations in claim severity over recent years. In 2022, the average incurred claim per $1 million of earned premium reached $281,071, a substantial increase from $121,761 the previous year. This figure, however, falls within a broader historical context of volatility. The state witnessed its highest average claim of $338,244 in 2017, followed by a dramatic drop to $121,761 in 2021.

Despite these fluctuations, recent data suggests that South Carolina’s claim severity is aligning more closely with neighboring states in recent years, according to the report.

While severity trends show signs of alignment with regional norms, claim frequency in South Carolina presents a more pressing challenge.

From 2019 to 2022, South Carolina’s claim frequency (number of incurred claims per $1 million of earned premium) has outpaced that observed in the other states considerably. The claims frequency rate was nine in 2022, 13 in 2021, 10 in 2020 and 12 in 2019. During that same period, none of its neighboring states — Florida, Georgia and North Carolina — reported a claims frequency rate higher than five.

Reforms put in place in 2024 are a positive move toward repairing Louisiana’s insurance market, which has long suffered from excessive claims litigation and attorney involvement that drive up costs and, ultimately, premium rates.

But more work is needed, Triple-I says in its latest Issues Brief.

Research by the Insurance Research Council (IRC) – like Triple-I, an affiliate of The Institutes – shows Louisiana to be among the least affordable states for both personal auto and homeowners insurance.

In 2022, the average annual personal auto premium expenditure per vehicle in Louisiana was $1,588, which is nearly 40 percent above the national average and nearly double that of the lowest-cost Southern state of North Carolina ($840), IRC said. Louisianans also pay significantly more for homeowners coverage than the rest of the nation, with an average annual expenditure of $2,178, representing 3.81 percent of the median household income in the state – 54 percent above the national average.

Louisiana’s low average personal income relative to the rest of the nation contributes to its personal auto insurance affordability challenges, which are exacerbated by its litigation environment.

Louisiana Insurance Commissioner Tim Temple has championed a series of legislative changes that he has said will encourage insurers to return to Louisiana, especially in hurricane-prone areas.

“There are fewer companies willing to write property insurance in Louisiana, and that’s a lot of what our legislation is designed to do,” Temple said. “To help promote Louisiana and change the marketplace so that companies feel like they are going to be treated fairly.”

In June 2024, Gov. Landry signed into law S.B. 355, which puts limitations on third-party litigation funding – a practice in which investors, with no stake in claims apart from potentially lucrative settlements, fund lawsuits aimed at entities perceived as having deep pockets. Third-party litigation funding drives up claims costs and delays settlements, which end up being passed along to consumers in the form of higher premiums.

This progress was undermined when Landry vetoed H.B. 423, which would have reformed the state’s “collateral source doctrine” that allows civil juries to have access to the “sticker price” of medical bills and the amount actually paid by the insurance company.

“In addition to creating more transparency and helping lower insurance rates, this bill would have brought more fairness and balance to our civil justice system,” said Lana Venable, director of Louisiana Lawsuit Abuse Watch in a statement regarding the veto. “Lawsuit abuse does not discriminate – everyone pays the price when the resulting costs are passed down to all of us.”

Continued reforms in 2025 will be necessary to help prevent legal system abuse and promote a more competitive insurance market that leads to greater affordability for consumers, Triple-I says in its brief.

By William Nibbelin, Senior Research Actuary, Triple-I

The U.S. Property & Casualty insurance market is expected to continue its trajectory of improving underwriting results in 2024 into 2025 and 2026, according to the latest projections by actuaries at Triple-I and Milliman. The latest report – Insurance Economics and Underwriting Projections: A Forward View – was released during Triple-I’s January 16 members-only webinar.

Year-over-year gains in net written premium increases and quarter-over-quarter loss ratios are primarily due to better-than-expected Q3 performance in personal auto.

The 2024 underlying economic growth for P&C ended slightly below U.S. GDP growth at 2.3 percent versus 2.5 percent year over year. A further economic milestone occurred in 2024, with the number of people employed in the U.S. insurance industry surpassing three million.

Michel Léonard, Ph.D., CBE, chief economist and data scientist at Triple-I, noted P&C underlying economic growth is expected to remain above overall GDP growth in 2025 (2.3 percent versus 2.1 percent) and 2026 (2.6 percent versus 2.0 percent) as lower interest rates continue to revive real estate and contribute to higher volume for homeowners’ insurance and commercial property.

“This is an improvement on our 2025 P&C underlying growth expectations from second half of 2024,” Léonard said. “The pace of increase in P&C replacement costs is expected to overtake overall inflation in 2025 (3.3 percent versus 2.5 percent). This aligns with our earlier expectations from the second half of last year.”

Personal vs. commercial lines performance

The 2024 net combined ratio for the P&C industry is projected to be 99.5, a year-over-year improvement of 2.2 points, with a net written premium (NWP) growth rate of 9.5 percent. Combined ratio is a standard measure of underwriting profitability, in which a result below 100 represents a profit and one above 100 represents a loss. Personal lines 2024 net combined ratio estimates improved by nearly 1 point, while the commercial lines 2024 estimates worsened by 1.2 points.

Dale Porfilio, FCAS, MAAA, Triple-I’s chief insurance officer, expanded upon the dichotomy of commercial and personal lines results.

“Commercial lines continue to have better underwriting results than personal lines, but the gap is closing,” Porfilio said. “The impact from natural catastrophes such as Hurricane Helene in Q3 2024 and Hurricane Milton in Q4 2024 significantly impacted commercial property. The substantial rate increases necessary to offset inflationary pressures on losses have driven the improved results in personal auto and homeowners.”

Personal auto and homeowners are each projected to have improved 6.1 points over 2023, with a 2024 net combined ratio of 98.8 and 104.8, respectively. NWP growth rate for personal lines is expected to surpass commercial lines by 9 points in 2024, with personal auto leading at 14.0 percent, the second highest in over 15 years.

Jason B. Kurtz, FCAS, MAAA, a principal and consulting actuary at Milliman – a premier global consulting and actuarial firm – elaborated on profitability concerns within commercial lines.

“Commercial auto continues to remain unprofitable,” he said. “The 2024 direct incurred loss ratio through Q3 is only marginally improved relative to 2023 and is the second highest in over 15 years.”

Hurricane Milton is projected to be the worst catastrophic event for commercial property since Hurricane Ian in 2022 Q3, driving higher-than-expected losses and subsequently increasing the commercial property projected 2024 net combined ratio up 3.3 points to 91.2, which is also 3.3 points worse than 2023. During the webinar, commercial property forecasts were also shared for the fire and allied and inland marine sub-lines.

Continued worsening in general liability

General liability’s projected 2024 net combined ratio of 103.7 is 3.6 points worse than actual 2023 experience. Kurtz said the line has seen significantly worsening, with each quarterly loss ratio in 2024 worse than 2023 year over year.

“The 2024 direct incurred loss ratio through Q3 is the highest in over 15 years,” Kurtz said. “As a result, we have increased our expectations for 2025 and 2026 net written premium growth, as the industry responds to the worsening 2024 performance.”

Continuing the discussion on general liability, Emma Stewart, FIA, chief actuary at Lloyds added that U.S. general liability has experienced material deterioration in loss ratios and a slowing down of claims development.

“A large driver of this has been the post-underwriting emergence of heightened social inflation, or more specifically, legal system abuse and nuclear verdicts,” Stewart said. “If these trends continue to increase, reserves on this class can be expected to deteriorate further.”

Workers comp loss-cost preview

Ending with workers compensation, Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance, provided a preview of this year’s average loss-cost changes and discussed the long-term financial health of the workers compensation system.

“The 2025 average loss cost decrease of 6 percent is moderate, which will inevitably have implications on the overall net written premium change,” Glenn said. She added that the –6 percent average loss cost level change in 2025 is notably different than the -9 percent average seen in 2024, the largest average decrease since before the pandemic.

“Payroll for 2025 will develop throughout the year resulting from both wage and employment levels. Therefore, overall premium will become clearer as the year progresses,” she said.

While rising premiums have been the primary driver for commercial property insurance growth for years, a 25-quarter rate increase streak broke in early 2024. Strong risk-adjusted capitalization and adequate liquidity may sustain the stable outlook, notwithstanding formidable risks, according to Triple-I’s latest insurance brief Commercial Property: Trends and Insights.

The brief focuses on several core trends shaping opportunities and threats to the commercial property insurance segment:

Mounting climate and natural catastrophe risks

Increasing capacity in the reinsurance market

Lurking undervaluation risk

Rise of AI and technology in risk mitigation

According to a recent McKinsey report, data involving global figures for 25 primary commercial lines carriers indicate a combined ratio of 91 percent for 2023, down from a high of 102 in 2020 but holding steady from the prior year. Commercial property comprised $254 billion (or 26 percent) of premiums across these carriers.

Before 2024, the overall U.S. P&C commercial market experienced hard market conditions going back to 2018, according to NAIC data and analysis. Double-digit rate increases were the norm, particularly for properties in high-risk regions or with poor loss histories. A Marsh McLennan report shows that in Q4 2023, rate increases averaged 11 percent for more considerable commercial property risks and even higher for accounts with loss history challenges or catastrophic exposure. Carriers have delivered steady quarterly increases since 2017 “to offset pressures from catastrophes and economic and social inflation.” Capacity constraints, driven by increased reinsurance costs, compounded this hardening, creating challenges for insurers and policyholders.

However, commercial insurers benefited from underwriting margins that outperformed the long-term average despite slowing year-over-year growth in direct premiums written, according to the 2024 S&P Global Market Intelligence U.S. Property and Casualty Industry Performance Rankings report. The top 50 of the 100 evaluated carriers was dominated by commercial line providers, with insurers focusing primarily on commercial property lines capturing three of the top 10 spots. In comparison, only two personal lines carriers ranked in the top 50.

AM Best, which maintains that insured losses in recent years have been driven primarily by secondary perils such as severe convective storms, issued its “Market Segment Outlook: US Commercial Lines” report. The analysts predict a stable market segment outlook for the U.S. commercial lines insurance sector in 2025. The company expects the commercial lines segment “will remain profitable in the aggregate and will be resilient in the face of near- and longer-term challenges.” However, relatively high claims costs, the multi-year impact of social inflation, and geopolitical risks may pose threats. The latest AM Best reportfocused solely on the commercial property segment (dated March 2024) advises that the Excess and Surplus (E&S) market has absorbed some of the higher risks. Still, overall secondary perils continue to be a significant “offsetting factor” for commercial property.

The damage of weather events and natural catastrophes tend to make big headlines (and rightly so), but the overall risk for commercial property isn’t limited to the destruction wrought by each disaster. It also extends to the interactions between the event outcomes and human systems. Specifically, these events can strain regional economic systems, such as decreasing the availability of rebuilding materials and labor while simultaneously amplifying demand for these same inputs. In turn, property replacement costs can soar.

Reinsurance

In 2023, major changes in reinsurance policy structures and price increases compelled insurers to decrease limits and absorb higher retentions. The policy restructurings also meant primary insurers had to retain more losses from increased secondary perils, such as floods, wildfires, and severe convective storms, that they could not cede to the reinsurance market. The insurers’ retention of loss may have allowed the incubation of increased capacity in the reinsurance market, improving late in 2023 and into early 2024.

By mid-year 2024 renewals, reinsurance appetite had grown with easing in some loss-free areas and, as applicable, underwriting scrutiny held firm in others areas. Analysts observed “flat to down mid-to high-single digits” reinsurance risk-adjusted rates for global property catastrophes. A Marsh McLennan report noted modest growth in investment and capital due to increased market capacity and underwriting interest from carriers. Late 2024 catastrophic events and any similar activities in the coming year will likely remain a primary drivers for reinsurance costs, along with the increasing cost of capital, financial market volatility, and economic inflation.

To learn more about Triple-I’s take on these and other commercial property insurance trends, read the issue brief and follow our blog.

The efficacy of collaboration and investment by “co-beneficiaries” in resilience initiatives was a dominant theme throughout Triple-I’s 2024 Joint Industry Forum – particularly in the final panel, which celebrated leaders behind recent real-world impacts of such investments.

Moderated by Dan Kaniewski, Marsh McLennan (MMC) managing director for public sector, the panelists discussed how their multi-industry backgrounds inform their innovative mindsets, as well as their knowledge on the profound ripple effects of targeted resilience planning.

The panel included:

Jonathan Gonzalez, co-founder and CEO of Raincoat;

Bob Marshall, co-founder and CEO of Whisker Labs;

Dawn Miller, chief commercial officer of Lloyd’s and CEO of Lloyd’s Americas; and

Lars Powell, director of the Alabama Center for Insurance Information and Research (ACIIR) at the University of Alabama and a Triple-I Non-Resident Scholar.

Productive partnership

Kaniewski – who spent most of his career in emergency management, previously serving as the second-ranking official at the Federal Emergency Management Agency (FEMA) and the agency’s first deputy administrator for resilience – kicked off the panel by raising the question “how do we define success?”

He characterized success as “putting theory into practice” and “having elected officials taking steps to reduce risk and transfer some of this risk from federal, state, or local taxpayers.”

But, as participants in earlier panels and this one made clear, government efforts can only go so far without private-sector collaboration.

“It doesn’t matter who makes that investment, whether it’s the homeowner, the business owner, or the government,” Kaniewski explained. “The reality is we all benefit from that one investment. If we can acknowledge that we benefit from those investments, we should do our best to incentivize them.”

Kaniewski and Raincoat’s Gonzalez were both integral in the development of community-based catastrophe insurance (CBCI), developed in the wake of Superstorm Sandy in 2012.

“A lot of the neighborhoods that experienced flooding due to Sandy didn’t have access to insurance prior to the flooding – and then, post flooding, the government really had to step up to figure out how to keep those families in those houses,” Gonzalez said.

In collaboration with the city, a nonprofit called the Center for NYC Neighborhoods developed the concept of buying parametric insurance on behalf of these communities, with any payouts going toward helping families stay in their homes after disasters. Unlike traditional indemnity insurance, a parametric policy pays out if certain agreed-upon conditions are met – for example, a specific wind speed or earthquake magnitude in a particular area – regardless of damage. Parametric insurance eliminates the need for time-consuming claim adjustment. Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders.

In this case, Kaniewski said, success was reflected in the fact that the pilot program received sufficient funding not only for renewal but expansion, bringing needed protection to even more vulnerable communities.

Powell reinforced this sentiment in explaining ACIIR’s research on the FORTIFIED method, a set of voluntary construction standards created by the Insurance Institute for Business and Home Safety (IBHS) for durability against severe weather. The insurance industry-funded Strengthen Alabama Homes program issues grants and substantial insurance premium discounts to homeowners to retrofit their houses along these guidelines, prompting multiple states to replicate the program.

Such homes in Alabama sustained 54 to 76 percent reduced loss frequency from Hurricane Sally compared to standard homes, Powell reported, and an estimated 65 to 73 percent could have been saved in claims if standard homes were FORTIFIED.

Incentivizing contractors to learn FORTIFIED standards was especially critical, Powell explained, because they further advertised these skills and expanded the presence of FORTIFIED homes beyond the grant program.

“A lot of companies have said for several years, ‘we don’t know if we’re comfortable writing these…we haven’t seen it on the ground,’” Powell said. “Well, now we’ve seen it on the ground. We need to have houses that don’t burn down or blow over. We know how to do it, it’s not that expensive.”

Addressing concerns to drive adoption

Miller described how Lloyd’s Lab works to ease that discomfort by creating a space for businesses to nurture and integrate novel insights and products without fear. With mentor support, companies are encouraged to test new ideas while free from the usual degree of financial and/or intellectual property risks attached to innovation investments.

“It’s about having an avenue out to try,” Miller said. “Having that courage, as we continue to work together, to try to understand what’s working, what’s not, and being brave to say, ‘this isn’t working, but we can course correct.’”

Whisker Labs’ Marshall noted that numerous insurance carriers have taken a chance on his company’s front-line disaster mitigation devices, Ting, by paying for and distributing them to their customers.

Ting plug-in sensors detect conditions that could lead to electrical fires through continuous monitoring of a home’s electrical system. Statistically preventing more than 80 percent of electrical fires, communities benefit – not only by preventing individual home fires but also by providing data about the electrical grid and potentially heading off grid-initiated wildfires.

“There are so many applications for the data,” Marshall said, but “to have a true impact on society…we have to prove that we’re preventing more losses than the cost, and we have to do that in partnership with insurance carriers.”

Everyone wins if everyone plays

Cultivating innovative solutions is pivotal to enhancing resilience, the panelists agreed – but driving them forward requires more than just the insurance industry’s support.

He pointed to a project last year – funded by Fannie Mae and developed by the National Institute of Building Science (NIBS) – that culminated in a roadmap for resilience investment incentives, focusing on urban flooding.

The co-authors of the project, including Triple-I subject-matter experts, represented a cross-section of “co-beneficiary” groups, such as the insurance, finance, and real estate industries and all levels of government, Kaniewski said.

Implementation of the roadmap requires participation from communities and multiple co-beneficiaries. Triple-I and NIBS are exploring such collaborations with potential co-beneficiaries in several areas of the United States.