By Jeff Dunsavage, Senior Research Analyst, Triple-I

Florida Gov. Ron DeSantis announced last week that state regulators have secured nearly $1 billion in premium refunds for Progressive auto insurance policyholders in the state, due to cost savings achieved through litigation reform.

DeSantis, who signed sweeping tort reform legislation bills into law in 2022 and 2023, said the refunds are a direct result of declining litigation expenses in Florida’s auto insurance market.

“Florida was really considered a litigation hellhole by a lot of folks,” DeSantis said. “That contributed to consumers having to bear more costs with respect to auto insurance.”

He pledged Insurance Commissioner Mike Yaworksy is negotiating with other major auto carriers for similar reimbursements to their customers.

Mark Friedlander, Triple-I’s director of communications, told Spectrum News Florida that reduced lawsuit expenses has enabled auto insurers to lower average costs and, in some cases, return premium to customers.

“When you take that out of the equation — all of those abusive lawsuits — this brings down the expenses, and that in turn gets passed along to the consumer,” Friedlander said. “The consumer wins with legal system reform.”

Increased legislative involvement in regulating homeowners’ insurance pricing and rates – as recently called for by some officials in Illinois – would hurt insurance affordability in the state, rather than helping consumers as intended, Triple-I says in its latest Issues Brief.

Rising premiums are a national issue. They reflect a combination of costly climate-related weather events, demographic trends, and rising material and labor costs to repair and replace damaged or destroyed property. Average insured catastrophe losses have been increasing for decades, fueled in part by natural disasters and population shifts into high-risk areas. More recently, these and other losses to which the property/casualty insurance industry is vulnerable were exacerbated by inflation related to the pandemic and Russia’s invasion of Ukraine. Tariffs and changes in U.S. economic policies have since put even more upward pressure on costs.

These increasing costs – if not addressed – threaten to erode the policyholder surplus insurers are required to keep on hand to pay claims. If surplus falls below a certain level, insurers have no choice but to increase premium rates or adjust their willingness to assume risks in certain areas.

To avoid this, many insurers have filed with state regulators for rate increases – requests that often meet with resistance from consumer advocacy groups and legislators. Illinois would not be the first state to try to ease consumers’ pain by constraining insurers’ ability to accurately set coverage prices to reflect increasing levels of risk and costs.

Practicality, not politics

Such efforts, while perhaps politically popular, confuse one symptom (higher premiums) of a growing risk crisis with its underlying cause (increasing losses and rising costs). Using the blunt instrument of legislation to address the complexities and sensitivities of underwriting and pricing would tend to disrupt the market and further hurt insurance affordability – and, in some areas, availability.

Rather than target insurers with misguided legislation, the brief says, states would be wiser to work with the industry to improve their risk profiles by investing in mitigation and resilience. The brief describes the causes of higher premium rates nationally and in Illinois and how other states have successfully collaborated to address those causes and reduce upward pressure on – and eventually bring down –premium rates.

“Triple-I welcomes the opportunity to collaborate with state policymakers to develop constructive approaches to risk mitigation and resilience that will benefit communities and consumers,” the brief says.

By William Nibbelin, Senior Research Actuary, Triple-I

Motor vehicle tort cases in federal and state courts generated $42.8 billion in “excess value” from 2014 to 2023, according to new analysis by Triple-I.

“Excess value” may sound like a good thing, but it’s not. It represents an additional cost of motor vehicle civil litigation – above and beyond what it would have been if prior trends in court filings had continued. From 1995 to 2007, filings declined, and from 2007 to 2014 they were flat.

The report illustrates the impact of litigation inflation on insurance premiums for all drivers. It also underscores the challenges related to accurately quantifying and comparing state-by-state experience.

Lawsuits push premium up

As Triple-I has previously reported, litigation trends are a major force driving up auto insurance premiums. As claims costs rise – whether due to rising repair costs, litigation, or other factors – premiums must increase to ensure that insurers have enough policyholder surplus to pay future, higher claims.

Policyholder surplus is not a nice-to-have extra. It is the money state regulators require insurers to maintain so they will be able to keep their promises to pay policyholders. In addition, credit rating agencies expect insurers to keep even larger surpluses than the states mandate to enable the insurers to borrow at more favorable interest rates when needed.

Interestingly, motor vehicle tort settlement amounts appear to have decreased on average between 2014 and 2023. While actual settlement amounts are not reported, the “amount in controversy” – legalese for the amount demanded by the plaintiff – serves as a proxy for filings disposed as settlements. The average amount in controversy decreased from $748,000 in the first of the three decades under consideration to $674,000 in the third.

However, the increased volume of cases during the period drove the overall excess value to $984.6 million at the federal level alone.

State courts present a challenge

The report estimates that state courts handled approximately 5.0 million motor vehicle tort cases from 2014 to 2023, generating an excess value of $41.8 billion – dwarfing the federal court impact. This analysis, however, is challenged by the state-by-state variety of definitions and criteria for data collection.

“Because states maintain different definitions and criteria for data collection, most state civil case data is either unavailable or incomplete,” the report says.

The report concludes that its findings align with previous research by Triple-I and the Casualty Actuarial Society, which quantified increasing inflation on auto liability insurance at $118.9 billion for 2014-2023, representing both litigation and economic inflation.

“As we continue to analyze the evolving landscape of motor vehicle litigation, it’s clear that a deeper, data-driven understanding of both national and state trends is crucial,” said Patrick Schmid, Triple-I’s chief insurance officer. “Only with more transparent and comprehensive data can we craft effective solutions that benefit both policyholders and the broader insurance market. Future research should focus on bridging the gaps in state-level information and exploring the causal factors behind rising litigation and its impacts.”

Improved loss ratios, strong premium growth, and lower retention rates characterized the U.S. auto insurance industry in 2024, according to LexisNexis® Risk Solutions’ 2025 U.S Auto Insurance Trends Report.

The report shows that, “while a number of insurers returned to profitability as the market softened,” the market was characterized by “record levels of policy shopping and switching, attorney representation, claims severity, and rising driving violations.”

Rate increases over the past two years helped U.S. insurers address profitability issues, the report said. Premium rate increases are beginning to ease, rising 10 percent in 2024, compared with a 15 percent hike in 2023, as market conditions soften. Insurer profitability is improving, with direct written premiums growing 13.6 percent, to $359 billion, and incurred loss ratios stabilizing, enabling some carriers to pursue growth strategies and file for rate decreases.

LexisNexis Risk Solutions also notes that tariffs may factor into how insurers consider rate in 2025. While the market wouldn’t expect the magnitude of activity seen between 2022 through 2024, tariffs, if they stick, could set off a ripple effect of moderate rate increases with implications across the industry.

Other trends identified in the report include:

Bodily injury claims severity jumped 9.2 percent, and property damage severity climbed 2.5 percent, year over year. In contrast, collision severity fell 2.5 percent for the same period.

All driving violations increased 17percent and driving violation rates across the United States surpassed 2019 levels.

Policy shopping reached an all-time high, with more than 45 percent of policies in force shopped at least once by year-end.

The report also noted that electric vehicle (EV) transitions are introducing new risks, as drivers moving from internal combustion engine vehicles to EVs experienced a 14 percet rise in claim frequency.

“Auto insurers continue to navigate a dynamic market,” said Jeff Batiste, senior vice president and general manager, U.S. auto and home insurance, LexisNexis Risk Solutions. “The combination of the market softening and a return to profitability presents a potential new chapter for the industry as insurers encounter a consumer base that is more willing than ever to shop for deals.”

Record levels of auto policy switching translated to 2024’s new policy growth rate of 17.7 percent year over year. It also added momentum to the ongoing customer retention decline across the industry.

Since 2021, retention has decreased five percentage points, to 78 percent, resulting in a 22 percent increase in policy churn, the report says.

“Historically, dropping even one percentage point is significant,” it says. “However, against a backdrop of heightened levels of shopping and switching activity, insurers may want to focus on their retention strategies, especially when long-tenured customers are hitting the market.”

Florida’s top five auto insurance groups are cutting personal auto rates by a statewide average of 6.5 percent due to legislative reforms that addressed legal system abuse and assignment of benefits (AOB) claim fraud, the Florida Office of Insurance Regulation (OIR) announced this week.

“Citizens of the Sunshine State are now clearly seeing the benefits of a more stable and affordable insurance marketplace,” Triple-I CEO Sean Kevelighan said.

State leaders credit the reforms for driving down both average rates and loss ratios, with Florida now reporting the lowest personal auto liability loss ratio in the United States, OIR said. Improved underwriting results and reduced litigation are helping insurers lower premiums, while increased consumer shopping is boosting competition and affordability across the state’s auto insurance market.

Resistance to reforms persists

Despite the measurable benefits to consumers, these reforms are under attack in the state legislature. HB 947 and HB 837 would undo much of this progress.

“The continued reduction in auto insurance rates is yet another sign that Florida’s reforms are working,” said Florida Gov. Ron DeSantis. “We will protect our reforms from those who seek to undo them and continue to fight for Floridians.”

Other states, including Georgia and Louisiana, are following Florida’s lead.

Premium relief for Florida drivers comes on top of significant improvements in the state’s property insurance market, where many consumers are securing better rates for their home insurance due to legislative reform and a competitive market with more than a dozen new carriers, Triple-I Director of Corporate Communications Mark Friedlander told BestWire.

“For many years, unscrupulous glass vendors preyed upon Florida drivers at car washes, gas stations, and shopping center parking lots with promises of gift cards in exchange for signing over their glass repair,” Friedlander said. “When insurers rejected these highly inflated claims, frivolous lawsuits followed.”

Recent efforts to curb federal spending – particularly massive proposed cuts to several major federal science agencies and numerous FEMA grant programs – drew concern from panelists at Triple-I’s Joint Industry Forum in Chicago.

Slated to lose around half of their original budgets, organizations like the National Oceanic and Atmospheric Administration (NOAA) and the National Science Foundation (NSF) provide insurers with much of the research data needed to model climate risks, at no cost to insurers nor the broader public. Abolishing this research, which also enables daily weather and natural disaster forecasting, will increase underwriting costs and those associated with various other industries, including transportation, agriculture, and energy.

“Federal science agencies probably facilitate more economic activity in the country than any other federal agency,” said Frank Nutter, president of the Reinsurance Association of America (RAA). “Fully funding and restaffing those agencies is pretty critical.”

A host of cancelled FEMA mitigation programs have left dozens of catastrophe-prone communities without aid – including projects that were approved before the cuts. Ending the Building Resilient Infrastructure and Communities (BRIC) program, for instance, rescinded approximately $882 million in climate resilience funding — “money we could have spent on mitigation, so we don’t have to spend so much after a disaster,” said Neil Alldredge, president and CEO of the National Association of Mutual Insurance Companies (NAMIC).

Nutter added that “weighing against safety, teacher salaries – all the kinds of things that communities grapple with,” most former grantees lack the resources for “risk reduction or municipal projects and infrastructure” without federal investment.

Population growth in high-risk areas exacerbates the issue, Alldredge said.

“If you look at a map of this country and the population changes from 1980 to today, we have moved the entire population to all the wrong places,” he explained. Building properties capable of withstanding these weather patterns – let alone insuring them – has launched the industry into “a new era of risk.”

While the panelists agreed that opportunities to improve FEMA operations exist, they questioned President Trump’s consideration to disband it entirely by shifting to a state-based relief system.

David Sampson, president and CEO of the American Property Casualty Insurance Association (APCIA), noted that “the very nature of a natural disaster means that it overwhelms the local entity’s ability to respond,” rendering any state-based solution “unworkable.”

“I think we as an industry know where the low-hanging fruit for reforms are,” Sampson continued, because “we interact with FEMA on the ground after disasters.”

State-level legislative momentum

Though the Trump administration’s current plans do not bode well for the future of disaster resilience, insurers celebrated many state legislative wins this year regarding tort reform, notably in Georgia and Louisiana.

“Even at the federal level, there is a growing sense of awareness of the negative impact that an out-of-control tort system is taking on the economy and the American consumer,” Sampson said, highlighting a new bill that would impose taxes on third-party litigation funding.

Florida also successfully resisted challenges to its 2023 and 2024 reforms, which have already helped stabilize the state’s insurance rates and attracted new insurers after a multi-year exodus. Charles Symington, president and CEO of the Independent Insurance Agents & Brokers of America, pointed out that industry advocacy is crucial to tort reform survival.

“Once you get these beneficial pieces of legislation passed,” he said, “we have to fight the fight in every legislative session.”

Symington then contrasted Florida’s recovering market with California’s enduringly hostile regulatory environment, propelled by the 1988 measure Proposition 103.

Insurance Commissioner Ricardo Lara has implemented a Sustainable Insurance Strategy to mitigate the effects of Prop 103 – such as by authorizing insurers to use catastrophe modeling if they agree to offer coverage in wildfire-prone areas – but the strategy has garnered criticism from legislators and consumer groups.

“California doesn’t have the assessment ability like Florida does,” agreed moderator Fred Karlinsky, shareholder and global chair of Greenberg Traurig, LLP. “California is three decades behind.”

As insurers adjust their risk appetite to reflect these constraints, more property owners have been pushed into California’s FAIR Plan – the state’s property insurer of last resort.

“Our members are having to cobble together coverage,” said Joel Wood, president and CEO of the Council of Insurance Agents & Brokers (CIAB), who noted that the FAIR plan’s policyholder count has more than doubled since 2020.

Natural disasters like January’s devastating wildfires underscore California’s need for premium rates that adequately reflect the full impact of these risks, which is essential to the continued availability of private insurance in the state.

“When you have the right leadership in place – the governor, the state legislature – and you have the industry being effective in our advocacy, then we can improve these difficult marketplaces,” Symington concluded.

Insurance industry executives and thought leaders gathered yesterday for Triple-I’s Joint Industry Forum (JIF) in Chicago to discuss the trends, economics, geopolitics, and policy influencing the market today, as well as ways to navigate these complexities while focusing on making their products affordable and available for consumers.

Triple-I CEO Sean Kevelighan in his opening remarks, noted that effective risk management depends on collaboration across stakeholder groups, as interconnected perils “present a community problem, not just an industry problem.”

JIF keynote speaker Louisiana Insurance Commissioner Tim Temple said facilitating community resilience planning is a top priority for the National Association of Insurance Commissioners (NAIC). The NAIC’s 2025 initiative – “Securing Tomorrow: Advancing State-Based Regulation” – aims to improve disaster mitigation and recovery by consolidating “the collective expertise of experienced state regulators from across the country, who can share real-time insights and proven strategies,” Temple said.

Among the initiative’s goals is aggregating more data from insurers to better understand challenges to affordability and availability on state levels, which the NAIC can then translate into actionable policy proposals. Such data calls, Temple said, help regulators, legislators, and policyholders focus on improving the cost drivers of insurance rates.

Louisiana has consistently been among the least affordable states for homeowners and auto insurance, according to the Insurance Research Council (IRC), in part because of its reputation for being plaintiff-friendly in civil litigation. Significant tort legislation has been approved in the state, but resistance to reform remains a challenge.

Getting to the roots of high premiums

After a recent data call in his home state, Temple told the JIF audience, “For the first time in Louisiana, we’re not talking about only premiums. We’re talking about why premiums are where they are.”

A critical lack of transparency surrounding cost drivers persists, however. Temple criticized the National Flood Insurance Program’s Risk Rating 2.0 reforms for not publicly disclosing more information “for individuals and communities to identify and address factors driving up their premiums,” such as “whether increased rates take into account levee systems, pump stations, and other things designed to help mitigate against floods.”

Conversely, government programs like Strengthen Alabama Homes – and the numerous programs it inspired, including in Louisiana – have demonstrated success in communicating the benefits of resilience investments for consumers and policymakers.

“We’re seeing major positive results after just a few short years,” Temple said, noting that, since early 2024, over 5,000 homeowners not chosen for Louisiana’s grant program still decided to invest in the same hazard mitigation, as they may still qualify for the corresponding state-mandated insurance discounts.

“As natural disasters become more frequent and severe, state regulators will continue to drive forward common-sense policies that protect consumers and ensure that insurance remains available and reliable for at-risk communities,” Temple concluded. Developing the database required for such policies is a necessary first step.

Keep an eye on the Triple-I Blog for further JIF coverage.

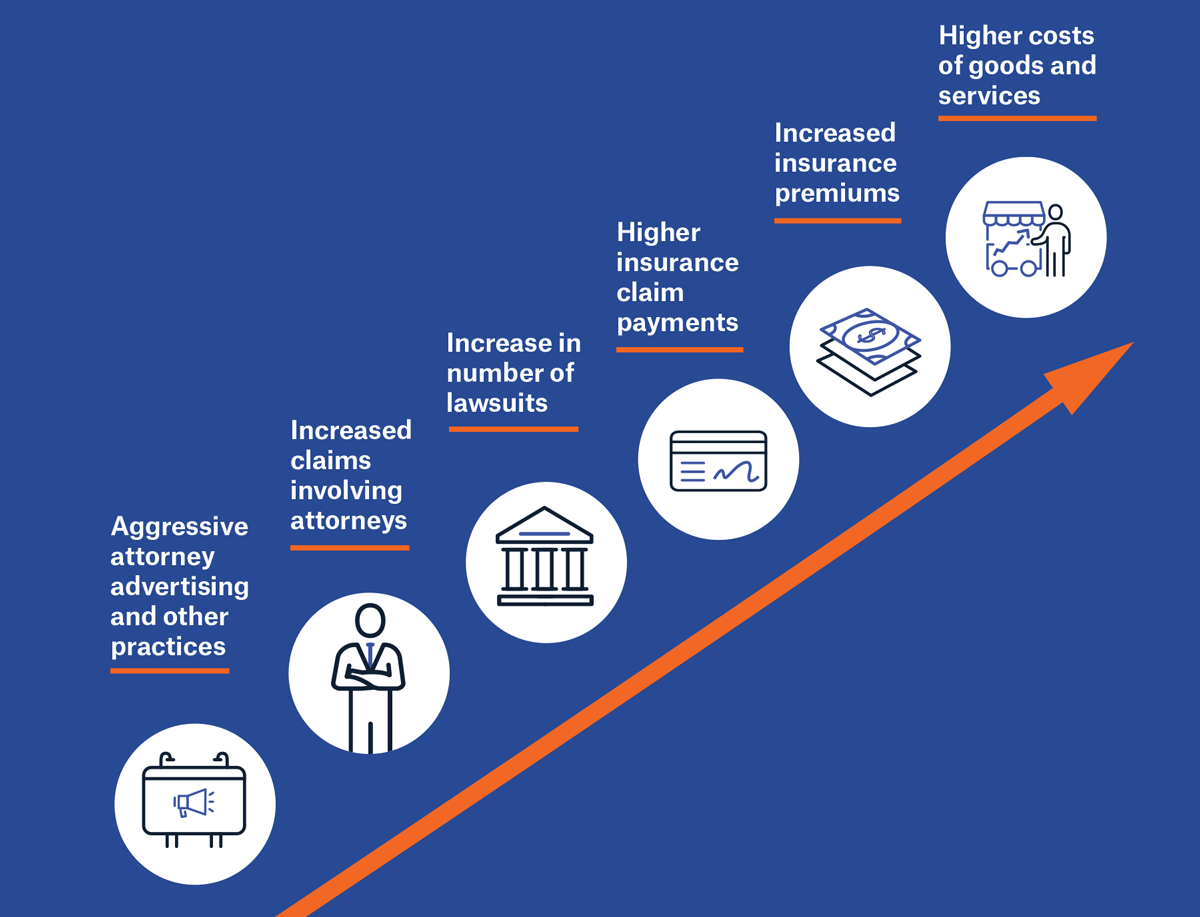

Practices that foster unnecessary or drawn-out litigation are among several hard-to-measure forces that can shift loss ratios for insurers and disrupt forecasts, making cost management more challenging. Ultimately, the resulting cost increase is passed on to consumers, which adversely impacts the affordability and availability of coverage. The Insurance Information Institute (Triple-I) and Munich Re US published a new resource to help consumers understand how legal system abuse is fueling higher claim costs, driving up premiums, and reducing the efficiency of our civil justice system.

A Consumer Guide: How Legal System Abuse Impacts You explains, using accessible language and engaging graphics, how elements of legal system abuse – including third-party litigation financing, persuasive jury anchoring, and the deluge of attorney advertising – can distort outcomes and siphon value away from injured parties, policyholders, and the economy.

“Legal system abuse has driven up litigation expenses and costs, impacting businesses and consumers across the United States,” said Joshua Hackett, Head of Casualty at Munich Re US. “If left unchecked, these rising costs will continue to increase insurance premiums and limit coverage options.”

The consumer guide outlines legal trends and quantifies the impact of legal system abuse beyond rising premiums.

• $6,664 in added annual costs for the average American family of four

• 4.8 million U.S. jobs lost due to excessive litigation

• $160 billion in tort-related costs borne by small businesses annually

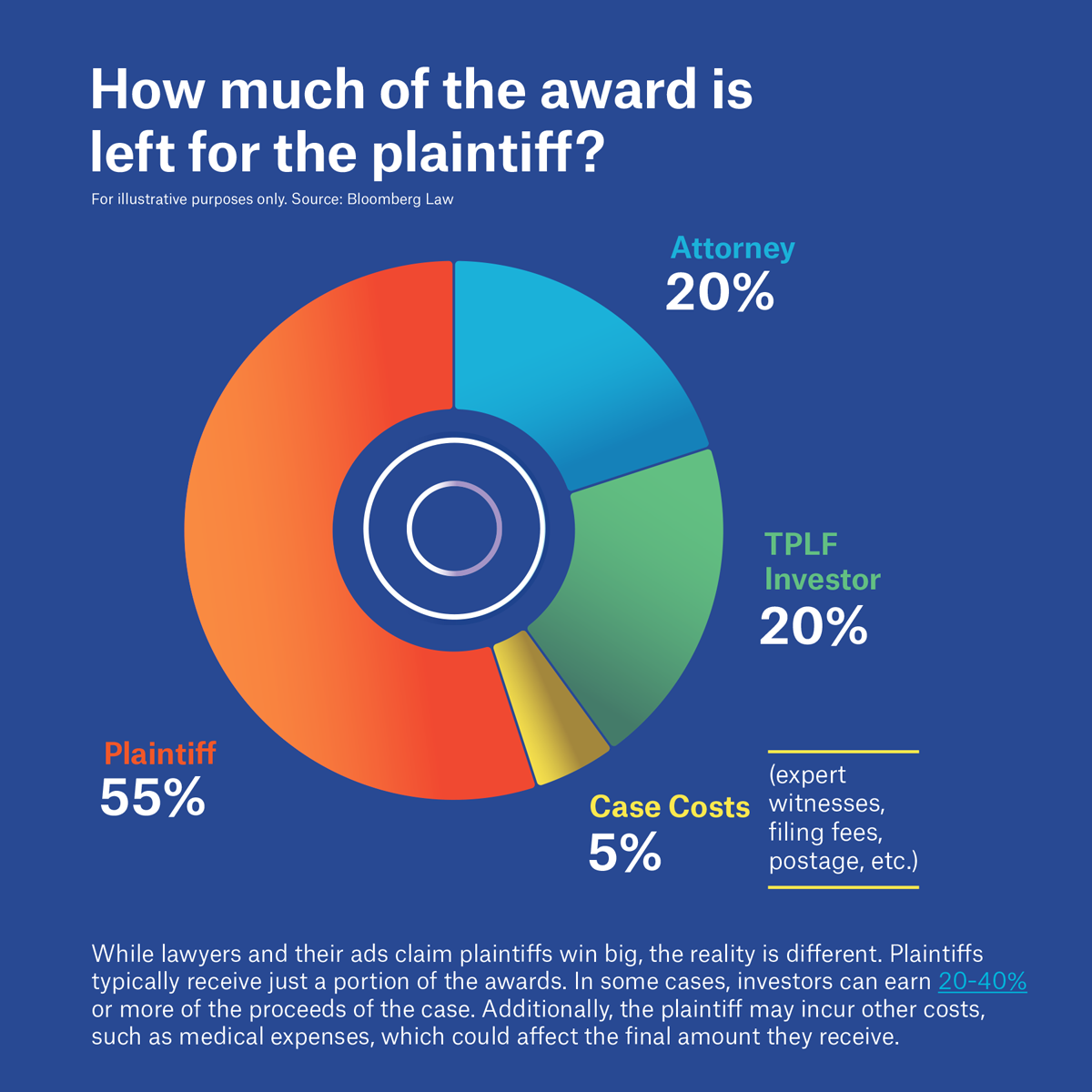

Who Benefits from Large Settlements?

The narrative of legal system abuse can be muddled by news of large, high-profile settlements, which can imply plaintiffs are winning big. In reality, injured parties typically end up with only a fraction of their awarded damages after fees, obligations to third-party litigation funders, and inflated expenses are taken into account.

According to a recent report from Duane Morris Class Action Review, a defense attorney interest group, $42 billion in class action settlements was reached last year, the third-highest value the group has tallied over the past twenty years. That figure included ten settlements of at least $1 billion. Products Liability Class Actions reaped by far the largest amount for a practice area, at $23.40 billion. Annual numbers for overall settlements reported in 2023 and 2022 were $51.4 billion and $60 billion, respectively.

However, the bulk of these settlements do not ultimately benefit the injured parties. Attorneys can charge contingency fees ranging from 33 to 40 percent for their labor, plus expenses incurred through litigation, such as court costs and expert witness fees. Additionally, the process for injured parties to claim and receive their share of the settlement can be complex and drawn out, and, often, it is not worth the small share amounts dispersed to most claimants in the long run. A 2019 Federal Trade Commission study estimates the median claims rate for consumer class action settlements was 9 percent and that the weighted mean — weighted by the size of the class — was only 4 percent.

“While billboard attorneys use exploitative advertisements promising big dollar settlements, the truth is consumers and business owners can be left with less money, sometimes substantially less, if third-party litigation financiers are involved,” said Triple-I CEO Sean Kevelighan.

The consumer guide reinforces what many risk and claims professionals are observing in the market.

Longer case durations

Higher settlements and awards

Diminishing predictability in the legal environment

This erosion of predictability poses underwriting challenges and affects the affordability and availability of coverage, particularly in casualty and liability lines.

Legal system abuse can be mitigated by supporting public awareness and robust tort reform policy.

Triple-I and Munich Re US are encouraging the industry to advocate for:

Disclosure requirements for litigation financing

Reforms to reduce medical billing abuse

More oversight of attorney advertising practices

The guide serves as an educational tool that insurers, brokers, and industry partners can share with clients and stakeholders to explain the link between premium increases, other rising costs, and potential legal exposure.

By William Nibbelin, Senior Research Actuary, Triple-I

The U.S. personal auto insurance industry saw a significant turnaround in 2024, achieving its best underwriting result since the pandemic began, according to Triple-I’s latest Issues Brief.

In fact, with a net combined ratio of 95.3, personal auto insurance has outperformed the broader property and casualty (P/C) insurance industry in terms of underwriting profitability for 10 out of the last 20 years. A combined ratio under 100 indicates an underwriting profit. One above 100 indicates a loss.

This positive shift comes after a period in which personal auto premiums experienced fluctuations. While the overall P/C industry outpaced personal auto in premium growth from 2018 to 2022, personal auto saw a strong rebound in 2023 and 2024, with double-digit premium growth rates of 14.4 percent and 12.8 percent, respectively. This surge in premiums follows a notable decline in 2020, the first since 2009, largely due to reduced driving during the initial phase of the COVID-19 pandemic. Since then, vehicle miles driven have returned to pre-pandemic levels.

A major factor influencing auto insurance premiums has been the significant rise in replacement costs for vehicles and parts after the pandemic. Insurers adjusted rates in response to these increased costs. The changes in consumer prices for new and used vehicles, as well as parts and repairs, have shown a strong correlation with average insurance rate adjustments over the past decade:

New Vehicles: 88 percent correlation;

Motor Vehicle Parts & Equipment: 74 percent correlation;

Used Vehicles: 79 percent correlation; and

Motor Vehicle Maintenance & Repair: 78 percent correlation.

Looking at losses, the direct incurred loss ratio for personal auto improved considerably by 21.7 points from late 2022 to the end of 2024. However, this improvement wasn’t uniform across all types of claims. Auto physical damage claims saw more improvement than auto liability claims, creating the largest disparity between the two in over a decade of 15.7 points.

Loss trends in personal auto are shaped by how often claims occur (frequency) and the average cost of each claim (severity). For personal auto liability, while the number of claims has stayed below pre-pandemic levels, the average cost per claim has continued to rise year after year with a cumulative increase from 2019 to 2024 of 54.2 points.

One of the significant challenges contributing to the increasing severity in personal auto liability is what’s known as legal system abuse. This includes a rise in lawsuits, larger jury awards, and more attorney involvement in claims. This phenomenon, intertwined with broader inflation, has driven up auto liability losses and related expenses by a range of $76.3 billion to $81.3 billion from 2014 to 2023 according to the latest Triple-I | Casualty Actuarial Society study.

Another important factor impacting the auto insurance market is the state regulatory environment. A recent report by the Insurance Research Council on Rate Regulation in Personal Auto Insurance indicated that the process for insurers to get rate changes approved has become more complex across the country between 2010 and 2023. This has led to longer approval times and a higher incidence of insurers receiving less than their requested rate increases. These trends can ultimately affect the availability of competitive auto insurance policies for consumers.

Rising natural disaster costs, increased home repair expenses, and legal system challenges have made homeowners’ insurance significantly less affordable across the United States over the past two decades, according to new research from the Insurance Research Council. The trend shows no signs of slowing.

The financial burden of protecting one’s home has grown substantially. With homeowners insurance expenditures growing much faster than incomes over the past two decades, American households now dedicate an increasing share of their income to insurance premiums.

In 2001, homeowners typically spent about 1.19 percent of their household income on insurance coverage. This figure climbed to 2.09 percent – a 75 percent increase – by 2022, the most recent available year’s data.

Projections of average premiums from the Insurance Information Institute suggest the trend will continue escalating, with estimates indicating households could spend 2.4 percent of their income on homeowners’ insurance by 2024 – the highest level recorded in more than two decades.

Wide variation by state

Utah emerged as the most affordable state in 2022, where residents spent only 1.00 percent of their income on homeowners’ insurance. Other states offering relative affordability included Oregon (1.09 percent), Alaska (1.23 percent), and Maryland (1.27 percent).

Louisiana ranked as the least affordable, with households dedicating 4.22 percent of their income to homeowners’ insurance. Disaster-prone states dominated the least-affordable rankings, with Florida (3.99 percent), Mississippi (3.87 percent), and Oklahoma (3.45 percent), following the Pelican State.

Multiple Cost Pressures

The affordability crisis stems from interconnected factors that have intensified pressure on insurance markets, according to IRC. Increased natural catastrophe risk represents a primary driver, with weather-related events becoming more frequent and severe.

Rising home construction and repair costs have compounded the challenge. Supply-chain disruptions have inflated material prices and extended project timelines, directly impacting claim settlements. When homes require repairs or replacement, insurers face significantly higher costs than in previous years, necessitating premium adjustments to maintain financial stability.

Population migration patterns have exacerbated risk concentrations, with more Americans moving to areas susceptible to natural disasters, the report noted. Coastal regions prone to hurricanes, wildfire-vulnerable areas, and tornado-prone territories have seen increased development, creating larger pools of exposed properties that insurers must protect.

Litigation has added another layer of complexity. Insurance companies report challenges with fraud, excessive claims, and legal system abuse following catastrophic events. The expense index – measuring what insurers spend to process, investigate, and litigate claims as a percentage of incurred losses – varies significantly across states, with litigation rates affecting overall costs.