Even as California moves to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing, the state’s risk profile continues to evolve in ways that underscore the importance of risk-based insurance pricing and investment in mitigation and resilience.

Triple-I’s latest “State of the Risk” Issues Brief discusses this changing risk environment and the impact of Proposition 103 – a three-decades-old measure that has made it hard for insurers to profitably write coverage in the state. In a dynamically evolving risk environment that includes earthquakes, drought, wildfire, landslides, and — in recent years, due to “atmospheric rivers” — damaging floods, Proposition 103 has prevented insurers from using the most current data and advanced modeling technologies. Instead, it has required them to price coverage based on historical data alone.

It also has restricted accurate underwriting and pricing by not allowing insurers to incorporate the cost of reinsurance into their pricing. Insurers use reinsurance to maximize their capacity to write coverage, and reinsurance rates have been rising for many of the same reasons as primary insurance rates. If insurers can’t reflect reinsurance costs in their pricing – particularly in catastrophe-prone areas – they must pay for these costs from policyholder surplus, reduce their market share in the state, or do both.

Proposition 103 also has impeded premium rate changes by allowing consumer advocacy groups to intervene in the rate-approval process. This makes it hard to respond quickly to changing market conditions, resulting in approval delays and rates that don’t accurately reflect current (let alone future) risk. It also drives up legal and administrative costs.

This has led, in some cases, to insurers deciding to limit or reduce their business in the state. With fewer private insurance options available, more Californians are resorting to the state’s FAIR Plan, which offers less coverage for a higher premium.

This isn’t a tenable situation.

In September 2023, California Insurance Commissioner Ricardo Lara announced a Sustainable Insurance Strategy for the state that includes allowing insurers to use forward-looking risk models that prioritize wildfire safety and mitigation and include reinsurance costs into their premium pricing. In exchange, insurers must cover homeowners in wildfire-prone parts of the state at 85 percent of their statewide coverage.

Issues around property insurance affordability are not confined to California. They’ve been a long time in the making, and they won’t be resolved overnight.

“Any sustainable solutions will have to rest on actuarially sound underwriting and pricing principles,” the Triple-I brief says. “Unfortunately, too often, the public discourse frames the risk crisis as an `insurance crisis’ – conflating cause with effect. Legislators, spurred by calls from their constituents for lower insurance premiums, often propose measures that would tend to worsen the problem because these proposals generally fail to reflect the importance of accurately valuing risk when pricing coverage.”

California’s Proposition 103 and the federal flood insurance program prior to its Risk Rating 2.0 reforms are just two examples, according to Triple-I.

Communities, businesses, and government at all levels to invest in mitigating flood risk and in improving resilience.

It’s important to amplify this message, especially in light of a recent proposal by Rep. Adam Schiff that would, among other things, disband NFIP and require property/casualty insurers to provide “all-risk policies” based on coverage thresholds and rating factors dictated by a board in which the insurance industry is only nominally represented. Last year’s budget uncertainty – in which a potential government shutdown was threatened – left open the very real possibility of funding for NFIP expiring if Congress failed to reach a deal.

“Federal policies and programs, including NFIP, are essential,” said Daniel Kaniewski, managing director, public sector, for Marsh McLennan in his testimony. “But all disasters are local, and so too are resilience investment decisions.”

Before joining Marsh McLennan, Kaniewski was the second-ranking official at FEMA, where he was the agency’s first deputy administrator for resilience.

“To increase the resilience of communities against the pervasive risk of flooding,” Kaniewski testified, “we believe that risk transfer— including from the NFIP, private flood insurance, reinsurance, and parametric insurance — should be paired with risk reduction.”

In this regard, Kaniewski emphasized NFIP’s Community Rating System (CRS), which encourages and rewards community floodplain management practices that exceed the NFIP’s minimum requirements. He cited Tulsa, Okla., as one of two U.S. communities to have achieved the highest CRS rating (the other is Roseville, Calif.), making residents eligible for the program’s greatest flood insurance discount of 45 percent.

Even without achieving the maximum rating, citizens save on flood insurance when their communities invest in resilience. For example, Miami-Dade County, Fla., recently became the latest jurisdiction in the hurricane- and flood-prone state to benefit from CRS program. The county’s new Class 3 rating will result in an estimated $12 million savings annually by giving qualifying residents and business owners in unincorporated parts of the county a 35 percent discount on flood insurance premiums.

Last year, 17 other Florida jurisdictions achieved Class 3 ratings. In Cutler Bay – a town on Miami’s southern flank with about 45,000 residents – the average premium dropped by $338. Citywide, that represented a savings of $2.3 million.

Unfortunately, only 1,500 communities nationwide participate in CRS, underscoring the importance of awareness-building, education, and collaboration.

Kaniewski also highlighted the opportunity presented by community-based catastrophe insurance (CBCI), which uses parametric insurance to provide coverage to local government entities that wish to cover a group of properties. Such programs enhance financial resilience by simultaneously providing affordable coverage and creating incentives for risk reduction.

“Our recent CBCI pilot in New York City was developed in partnership with the City of New York and several nonprofit and insurance industry partners and funded by the National Science Foundation,” Kaniewski said. “It provides a level of financial protection for low-to-moderate-income households that previously lacked flood insurance.”

Kaniewski called on other industries – such as finance and real estate – to encourage flood resilience investments, along with the insurance industry and all levels of government. He cited the recent roadmap for resilience incentives issued by the National Institute of Building Sciences (NIBS) – funded by Fannie Mae and co-authored by representatives of a cross-section of “co-beneficiary industries” – that focused on residential structures prone to flooding. Triple-I subject-matter experts were co-authors on the NIBS project.

Sen. Tim Scott of South Carolina, committee co-chair – along with Sen. Sherrod Brown of Ohio – spoke from the perspective of a former insurance professional who has sold flood insurance about his state’s recent investment in mitigation.

“In 2023, the state’s budget included significant funding for mitigation efforts that would reduce flood damage from future storms,” Scott said.“Backing up that investment, the South Carolina Office of Resilience released a nationally praised Statewide Risk Reduction Plan, identifying the communities most vulnerable to floods and targeting mitigation resources to protect those residents. These are local solutions to local challenges – and they will make a huge difference in the lives of South Carolinians.”

While solutions that work in South Carolina might not work in other states, Scott said, “I’m confident that similar, locally based solutions and approaches could make a huge difference.”

Sen. Katie Britt of Alabama invited Kaniewski to elaborate on her state’s Strengthen Alabama Homes program, which provides grants and insurance discounts to homeowners who make qualifying retrofits to their houses. Britt cited research that found the program had “directly resulted in lower insurance premiums and higher home resale values.”

Kaniewski spoke in detail about Alabama’s efforts, including Strengthen Alabama Homes – which, he pointed out, is now being emulated by other states, including hurricane- and flood-prone Louisiana. He also cited by name the author of the research Britt referenced – Dr. Lars Powell, executive director of the Alabama Center for Insurance Information and Research at the University of Alabama and a Triple-I Non-resident Scholar – for producing “the first study that I’ve seen that gives empirical data — real evidence that mitigation pays.”

Steve Patterson, mayor of Athens, Ohio, described a range of nature-based solutions his city has taken – from rerouting the Hocking River, which runs through the middle of the city, to removing invasive plants and restoring native trees along the bank.

“That’s been very effective in reducing flooding in different neighborhoods throughout the city,” Patterson said. “There are a lot of things cities and villages can do.”

The work done by Athens – like green infrastructure work by the Milwaukee Metropolitan Sewerage District in Wisconsin and municipal entities – offers opportunities to reduce flood risk while improving quality of life for citizens. But, as Patterson points out, not all municipalities have the financial capacity to engage in such projects.

That is where the engagement of co-beneficiaries of resilience investment as partners becomes so crucial.

Severe convective storm losses drove adverse results in 2023 underwriting profitability for the property/casualty industry, according to the latest projections by actuaries at the Triple-I and Milliman.

The quarterly report, Insurance Economics and Underwriting Projections: A Forward View, which was presented on January 30, at a members-only webinar, found that the overall combined ratio is forecast to be 103.9, with commercial lines at 97.7, outperforming personal lines at 109.9. Combined ratio is a standard measure of underwriting profitability, in which a result below 100 represents a profit and one above 100 represents a loss.

Hard markets continue with 2023 net written premium growth forecast at 9.0 percent.

Dale Porfilio, FCAS, MAAA, Chief Insurance Officer at Triple-I, discussed the overall P&C industry underwriting projections.

“The bad news is that the 2023 Q3 incurred loss ratio for homeowners, commercial auto, and commercial multi-peril exceeded our expectations, as 2023 Q3 incurred loss ratios were above historical averages.” Porfilio said.

Porfilio elaborated on the industry’s bleak homeowners financial results, stating that, “For 2023, the net combined ratio is forecast at 112.3, the worst since 2011.”

Porfilio added that the 2023 net written premium growth rate of 12.4 percent is the highest in over 10 years, reflecting rate increases to offset inflationary loss costs.

“We expect personal auto and homeowners lines to improve in 2024 and 2025, but to remain unprofitable,” Porfilio added.

Jason B. Kurtz, FCAS, MAAA, a Principal and Consulting Actuary at Milliman – a premier global consulting and actuarial firm – said commercial property and workers compensation continue to be profitable, while commercial multi-peril and commercial auto remain troubled.

“Looking at commercial auto, underwriting losses continue, with a projected 2023 net combined ratio of 110.2, the highest since 2017,” said Kurtz. “For 2023 Q3, the incurred loss ratio was the highest in over 15 years, while the 2023 Net Written Premium growth rate of 6 percent is noticeably lower than the prior two years.”

Turning to workers compensation, Kurtz noted that “the 2023 net combined ratio of 88.7 is in line with the five-year average of approximately 89. With anticipated net written premium growth of 2 percent per year from 2023 through 2025, growth will be modest, but the net combined ratio is expected to remain favorable for our forecast horizon.”

Michel Léonard, Ph.D., CBE, Chief Economist and Data Scientist at Triple-I, discussed key macroeconomic trends impacting the property/casualty industry results including inflation, interest rates, and overall economic underlying growth.

“Real (inflation-adjusted) gross domestic product in the third quarter of 2023 accelerated to 4.9 percent, but economists still expect year-over-year growth of 2.1 percent,” said Léonard, noting that for GDP, “revised Q3 numbers did not disappoint, but all eyes remain on Q4.”

Léonard said inflation as measured by the consumer price index (CPI) continues to slow down to 3.1 percent as of November, but CPI, less food and energy prices, is still up 4.0 percent year over year.

“Year-over-year, P&C underlying growth grew 1.3 percent in 2023 and is forecasted by Triple-I to grow 2.6 percent in 2024,” said Léonard. “This is below U.S. GDP growth in 2023 and slightly above U.S. GDP growth in 2024. Year-over-year P&C replacement costs increased by 1.1 percent in 2023 and are forecasted to increase by 2.0 percent in 2024.”

Donna Glenn, FCAS, MAAA, Chief Actuary at the National Council on Compensation Insurance (NCCI), identified rate adequacy and medical inflation as two of the workers compensation line’s top concerns.

“We’ve seen loss costs decline for 10 consecutive years,” Glenn said. She credits a “strong labor market and overall economy” resulting in “payroll increases outpacing loss cost declines.”

Glenn added that the “NCCI continues to analyze the data with healthy skepticism to identify changes in trends.”

Legislation proposed by U.S. Rep. Adam Schiff (D-Calif.) to create a federal “catastrophe reinsurance program” raises several concerns that warrant scrutiny and discussion – starting with the question: Does what’s being proposed even qualify as insurance?

If enacted into law, the bill would establish a “catastrophic property loss reinsurance program…to provide reinsurance for qualifying primary insurance companies.” To qualify, insurers would have to offer:

An all-perils property insurance policy for residential and commercial property, and

A loss-prevention partnership with the policyholder to encourage investments and activities that reduce insured and economic losses from a catastrophe peril.

The proposed program would phase in coverage requirements peril by peril over several years and discontinue FEMA’s National Flood Insurance Program (NFIP). It would set coverage thresholds and dictate rating factors based on input from a board in which the insurance industry is only nominally represented.

And nowhere in the 22-page proposal do any of the following words or phrases appear:

“Actuarial soundness”;

“Risk-based pricing”;

“Reserves”; or

“Policyholder surplus”.

Actuarially sound risk-based pricing and the need to maintain adequate reserves and policyholder surplus to ensure financial strength and claims-paying ability are the bedrock of any insurance program worthy of the name – not technical fine print to be worked out down the road while existing mechanisms are being dismantled and market forces distorted through government involvement.

Insurance is a complicated discipline, and prior federal attempts at providing coverage have struggled to balance their goal of increasing availability and reducing premiums against the need to base underwriting and pricing on actuarially sound principles to ensure sufficient reserves for paying claims.

Actuarially sound risk-based pricing and the need to maintain adequate reserves and policyholder surplus…are the bedrock of any insurance program worthy of the name – not technical fine print to be worked out down the road…

Sean Kevelighan, CEO, Triple-I

Learn from history

NFIP is a strong case in point. Created in 1968 to protect property owners for a peril that most private insurers were reluctant to cover, NFIP’s “one-size-fits-all” approach to underwriting and pricing has led to the program now owing more than $20 billion to the U.S. Treasury because it lacked the reserves to fully pay claims after major events like Hurricane Katrina and Superstorm Sandy. It also often led to lower-risk property owners unfairly subsidizing coverage for higher-risk properties.

Having thus learned the importance of risk-based pricing, NFIP has changed its underwriting and pricing methodology. The new approach – Risk Rating 2.0, announced in 2019 and fully implemented as of April 1, 2023 – more equitably distributes premiums based on home value and individual properties’ flood risk. As a result, premiums of previously subsidized policyholders – particularly in coastal areas with higher values – have risen, leading to outcries from many higher-risk owners who have seen their subsidies reduced.

In addition to leading to fairer pricing, Risk Rating 2.0 – by reducing market distortions – increases incentives for private insurers to get involved. For a long time, private insurers considered flood an untouchable peril, but improved data modeling and analytical tools have increased their comfort writing this business. As the charts below show, private insurers have been playing a steadily increasing role in recent years, covering a larger percentage of a growing risk pool.

Over time, this trend should lead to greater availability and affordability of flood insurance coverage.

Rather than incorporating the lessons generated by NFIP’s experience with a single peril, Rep. Schiff’s proposal would discontinue the reformed flood insurance program while adding a new layer of complexity to coverage across all perils and casting into question the future of various state insurance programs and residual market mechanisms currently in place.

Time-tested principles

Any attempt by the federal government to address insurance availability and affordability concerns must be made with an understanding of how insurance works – from pricing and underwriting to reserving and claim settlement. For example, the Schiff bill proposes piloting an all-perils policy with a term of five years. There are good reasons for property/casualty policies to be written with a one-year term. Specifically, the conditions that affect claims costs can change quickly, and insurers – as referenced above – must set aside sufficient reserves to be able to pay all legitimate claims. If they cannot revisit pricing annually, the financial results could be disastrous.

“Who would have thought in 2019 that replacement costs would increase 55 percent within three years?” asked Dale Porfilio, Triple-I’s chief insurance officer. Supply-chain disruptions related to the COVID-19 pandemic and Russia’s invasion of Ukraine contributed to just such a replacement-cost spike. “Requiring five-year terms for policies would have led to a massive drain on policyholder surplus.”

Policyholder surplus is the financial cushion representing the difference between an insurer’s assets and its liabilities.

In announcing his proposed legislation, Rep. Schiff said it is intended to “insulate consumers from unrestrained cost increases by offering insurers a transparent, fairly priced public reinsurance alternative for the worst climate-driven catastrophes.”

This language ignores the fact that, under state-by-state regulation, premium rate increases are anything but “unrestrained” and ratemaking is based on actuarially sound principles that are transparent and fair. Property/casualty insurance already is one of the most heavily regulated industries in the United States.

Consumers deserve real solutions

Policyholders have legitimate concerns about affordability and, in some cases, availability of insurance. These concerns can create pressure for political leaders at both the state and federal levels to advance measures that are perceived as promising to help. Unfortunately, many recent proposals begin by mischaracterizing current trends as an “insurance crisis,” as opposed to what they really represent: A risk crisis.

Insurance premium rates tend to move in line with the frequency and severity of the perils they cover. They also are affected by factors like fraud and litigation abuse; climate, population, and development trends; and global economics and geopolitics. That is why insurers hire actuaries and data scientists and employ cutting-edge modeling technology to ensure that insurance pricing is actuarially sound, fair, and compliant with regulatory requirements in all states in which they do business.

That is how insurers keep lower-risk policyholders from unfairly subsidizing higher-risk ones.

But history has shown that direct government involvement in the underwriting and pricing of insurance products tends not to end well. Any plan that would attempt to micromanage insurers’ coverage of all perils through a lens that ignores time-tested, actuarially sound risk-based pricing principles raises a host of red flags that must be discussed and addressed before such a plan is allowed to become law.

By Jeff Dunsavage, Senior Research Analyst, Triple-I

I’m pleased and proud to have been part of Triple-I’s Town Hall — “Attacking the Risk Crisis” — in Washington, D.C. In an intimate setting at the Mayflower Hotel on November 30, 120-plus attendees got to hear from experts representing insurance, government, academia, nonprofits, and other stakeholder groups on climate risk, what’s being done to address it, and what remains to be done.

Triple-I’s first-ever Town Hall was designed as a logical step in its multi-disciplinary, action-oriented effort to change behavior to drive resilience. Capping a year in which headlines about “insurance crises” in several states garnered major media attention, Triple-I and its members and partners recognized the need for clarification.

“What we’re seeing is not an ‘insurance crisis’,” Triple-I CEO Sean Kevelighan told the standing-room-only audience. “We’re in the midst of a risk crisis. Rising insurance premium rates and availability difficulties are not the cause but a symptom of this crisis.”

Whisker Labs CEO Bob Marshall discusses innovation with moderator Jennifer Kyung, Vice President and Chief Underwriter at USAA.

While the insurance industry has a critical role to play and is uniquely well equipped to lead the attack, simply transferring risk is not enough. A recurring theme at the Town Hall was the need to shift from a focus on assessing and repairing damage to one of predicting and preventing losses.

Three moderated discussions – examining the nature of climate risk and its costs; highlighting the need of strategic innovation in mitigating those risks and building resilience; and exploring the role and impact of government policy – gave panelists the opportunity to share their insights with a diverse audience focused on collaborative action.

The agenda was:

Climate Risk Is Spiraling: What Can Be Done?

Moderator: David Wessel, Senior Fellow and Director at the Brookings Institution and former Economics Editor for The Wall Street Journal.

Panelists:

Dr. Philip Klotzbach, Colorado State University, researcher and Triple-I non-resident scholar.

Dan Kaniewski, Managing Director, Public Sector at Marsh McLennan, Former FEMA Deputy Administrator.

Jacqueline Higgins, Head, North America & Senior Vice President, Public Sector Solutions, Swiss Re

Jim Boccher, Chief Development Officer, ServiceMaster.

Jeff Huebner, Chief Risk Officer, CSAA.

Innovation, High- and Low-Tech: How Insurers Are Driving Solutions

Moderator: Jennifer Kyung, VP, Chief Underwriter, USAA.

Panelists:

Partha Srinivasa, EVP, CIO, Erie Insurance.

Sam Krishnamurthy, CTO, Digital Solutions, Crawford.

Bob Marshall, CEO, Whisker Labs.

Stephen DiCenso, Principal,Milliman.

Charlie Sidoti, Executive Director, InnSure.

Outdated Regs to Legal System Abuse: It Will Take Villages to Fix This

Parr Schoolman, SVP and Chief Risk Officer, Allstate.

Tim Judge, SVP, Head Modeler, Chief Climate Officer, Fannie Mae.

Dan Coates, Deputy Director, DRS, Federal Housing Finance Agency.

Fred Karlinsky, Co-Chair of Greenberg Traurig’s Global Insurance Regulatory & Transactions Practice Group.

Panelists and participants alike appreciated the compact, action-focused, conversational nature of the single-afternoon event, as well as the opportunity to discuss areas in which their diverse industry- or sector-specific priorities and efforts overlapped.

If you weren’t able to join us in Washington, don’t worry. In his closing remarks, Kevelighan announced plans to take the program on the road with a local and regional focus, so stay tuned. You can contact us if you’re interested in participating in future Town Halls or other Triple-I events. You also can join the “Attacking the Risk Crisis” LinkedIn Group to be part of the ongoing conversation.

The cost of homeowners insurance outpaced inflation from 2000 to 2020, according to new research by the Insurance Research Council (IRC) – like Triple-I, an affiliate of The Institutes. During that period, IRC found the coverage to be most affordable in Utah and least affordable in Louisiana.

The IRC research brief, Homeowners Insurance Affordability: Countrywide Trends and State Comparisons, reports that the average homeowners insurance expenditure across the United States was $1,311 in 2020, while the median household income was $68,010 for the same year. The data excluded flood and earthquake insurance, neither of which is included in a standard homeowners policy.

Median household income was sourced from the U.S. Census Bureau, and average homeowners insurance expenditures data came from the National Association of Insurance Commissions (NAIC). Because the most recent NAIC data is from 2020, the affordability index does not reflect the inflation surge related to the COVID-19 pandemic and the war in Ukraine.

In Utah – the most affordable state – households spent only 0.92 percent of their income on homeowners insurance. Oregon, Wisconsin, Washington, and New Hampshire rounded out the states with the lowest expenditure-to-income ratios.

Catastrophes played a major role in states where homeowners insurance was least affordable. Louisiana topped the list, at 3.84 percent of income in 2020. The other least affordable states were Florida, Oklahoma, Mississippi, and Alabama.

Some of these higher costs are due to insurers facing obstacles related to fraud, excessive claims, and legal system abuse after catastrophic events. These cost drivers have led to less affordable coverage nationwide.

Additionally, certain areas are undergoing crises of both affordability and availability, as some insurers respond by reducing coverage or withdrawing from specific markets. The research brief notes that examining trends in cost drivers can reveal opportunities for improving both affordability and availability for all consumers.

Want to know more about the risk crisis and how insurers are working to address it? Check out Triple-I’s upcoming Town Hall, “Attacking the Risk Crisis,” which will be held Nov. 30 in Washington, D.C.

Severe convective storm losses—the highest in decades—significantly affected the 2023 net combined ratio for the property/casualty industry, according to the latest underwriting projections by Triple-I and Milliman actuaries.

The 2023 net combined ratio is now forecast to be 103.8, with hard markets continuing the net written premium growth, forecast at 8.3 percent. Combined ratio is a standard measure of underwriting profitability, in which a result below 100 represents a profit and one above 100 represents a loss.

The quarterly report, Insurance Economics and Underwriting Objections: A Forward View, was presented on November 2 at a members only briefing moderated by Triple-I CEO Sean Kevelighan. Members can access the briefing replay by contacting members@iii.org for instructions.

Dale Porfilio, FCAS, MAAA, Chief Insurance Officer of Triple-I, discussed the overall P&C industry underwriting projections.

“We forecast personal lines to improve each year from 2023 through 2025, but still lag behind strong underwriting profitability in commercial lines,” he said. He also noted that the improvements are expected to result in “the overall P&C industry returning to a small underwriting profit in 2025.”

On personal auto, Porfilio forecast premium growth of 11.0 percent in 2023 as rate increases start to exceed loss trends, allowing the 2023 net combined ratio to improve incrementally to 110.5 from 112.2 in 2022.

“Costlier replacement parts and low inventories are contributing to current and future loss pressures,” Porfilio said, adding, “unless replacement cost begins to decrease materially—which is not currently forecast—we project personal auto to remain at an underwriting loss through 2025.”

Looking at commercial property, the 2023 net combined ratio is forecast at 91.6, nearly identical to 2022.

“Hard market conditions continue into 2023, most notably in catastrophe-prone regions,” said Jason Kurtz, a principal and consulting actuary at Milliman—an independent risk-management, benefits, and technology firm said. “We expect premium growth to moderate through 2025.”

Kurtz also discussed commercial auto, predicting that underwriting losses will continue, with first-half 2023 direct incurred loss ratios at the highest in at least 15 years.

“There will be a continued need for rate to improve the combined ratio results,” Kurtz said, adding, “We are forecasting the 2023 combined ratio at 106.7 percent, 2024 at 103.4 percent and 2025 at 102.7 percent.”

Michel Léonard, PhD, CBE, Chief Economist and Data Scientist at Triple-I, discussed key macroeconomic trends impacting the property/casualty industry results including inflation, increasing interest rates and overall economic underlying growth.

“P&C growth has improved in 2023, growing 1.3 percent versus 2.1 percent for overall GDP. While many hurdles could derail such improvements, P&C underlying economic growth is currently positioned to increase faster than overall GDP by 2.6 percent versus 1.7 percent in 2024 and by 4.5 percent versus 2.0 percent in 2025,” Léonard explained.

Léonard noted that top risk scenarios for 2024 include geopolitics, weaking employment, and GDP contraction. “The Fed may also keep increasing rates into 2025, pushing down home and auto insurance underlying economic growth.”

Donna Glenn, Chief Actuary at the National Council on Compensation Insurance (NCCI), also shared preliminary numbers for 2023 on workers compensation premium, payroll, and underwriting profitability. She noted that premium increased 11 percent in 2022, returning to near the pre-pandemic levels of 2019. Glenn also indicated that the 2023 combined ratio should be very similar to 2022, resulting in a full decade of workers comp calendar-year combined ratios under 100 percent.

“All in all, the results for the first half of 2023 are remarkably stable,” she said. “I want to be clear—we continue to be vigilant in monitoring results and trends.”

Want to know more about the risk crisis and how insurers are working to address it? Check out Triple-I’s upcoming Town Hall, “Attacking the Risk Crisis,” which will be held Nov. 30 in Washington, D.C.

Ten states – Louisiana, Florida, Idaho, Kentucky, Mississippi, Montana, North Dakota, South Carolina, Texas, and Virginia – as well as additional plaintiffs, are suing the Federal Emergency Management Agency (FEMA) over its new methodology for pricing flood insurance, Risk Rating 2.0. On Sept. 14, a federal hearing lasted six hours as the plaintiffs sought a preliminary injunction to halt the new pricing regime while the lawsuit plays out.

Many residents of these states are understandably upset about seeing their flood insurance premium rates rise under the new approach. There may not be much comfort for them in knowing that the current system is much fairer than the previous one, in which higher-risk homeowners subsidized those with lower risks. Similarly, policyholders who have had their premium rates reduced under Risk Rating 2.0 are unlikely to take to the streets in celebration.

These homeowners aren’t alone in seeing insurance rates rise – or even having to struggle to obtain insurance. And these difficulties aren’t confined to holders of flood insurance policies. Florida and California are two states in which insurers have been forced to rethink their risk appetite – due in part to rising natural catastrophe losses and in part to regulatory and litigation environments that make it increasingly difficult for insurers to profitably write coverage.

Even before the COVID-19 pandemic and Russia’s invasion of Ukraine – and the supply-chain and inflationary pressures they created – the property/casualty insurance market was hardening as insurers adjusted their pricing and their risk appetites to keep pace with conditions that were driving losses up and eroding underwriting profitability – topics Triple-I has written about extensively (see a partial list below).

“Rising insurance rates are not the problem,” says Dale Porfilio, chief insurance officer at Triple-I. “They are a symptom of rising losses related to a range of factors, from climate and population trends to post-pandemic driving behaviors and surging cybercrime to antiquated policies, outdated building codes, fraud, and legal system abuse.”

In short, we are not experiencing an “insurance crisis,” as many media outlets tend to describe the current state of the market; we are experiencing a risk crisis. And even as the states referenced above push back against much-needed flood insurance reform, legislators in several states have been pushing measures that would restrict insurers’ ability to price coverage accurately and fairly – rather than addressing the underlying perils and forces aggravating them.

Triple-I, its members, and a range of partners are working to educate stakeholders and decisionmakers and promote pre-emptive risk mitigation and investment in resilience. We are using our position as thought leaders and our unique non-lobbying role in the insurance industry to reach across sector boundaries and drive constructive action. You will be hearing more about these efforts over the next few months.

The success of these efforts will require a collective understanding among stakeholders and decisionmakers that for insurance to be available and affordable frequency and severity of risk must be measurably reduced. This will require highly focused, integrated projects and programs – many of them at the community level – in which all stakeholders (co-beneficiaries of these efforts) will share responsibility.

Want to know more about the risk crisis and how insurers are working to address it? Check out Triple-I’s upcoming Town Hall, “Attacking the Risk Crisis,” which will be held Nov. 30 in Washington, D.C.

Even as the 2023 Atlantic hurricane season proves to be more intense than originally predicted, federal funding for the National Flood Insurance Program (NFIP) is threatened by a potential government shutdown. Funding for NFIP will expire after September 30 if lawmakers don’t reach a deal.

Claims on existing policies would still get paid if NFIP isn’t reauthorized. But the program would be unable to issue new policies and would face other funding constraints. If it can’t issue new policies, thousands of real estate transactions requiring flood coverage could be derailed.

Insured losses from hurricanes have risen over just the past 15 years. When adjusted for inflation, nine of the 10 costliest hurricanes in U.S. history have struck since 2005. This is due in large part to the fact that more people have been moving into harm’s way since the 1940s, and Census Bureau data show that homes being built are bigger and more expensive than before. Bigger homes filled with more valuables means bigger claims when a flood occurs – a situation exacerbated by continuing replacement cost inflation.

Flooding isn’t just a problem for East and Gulf Coast communities. Inland flooding also is on the rise. In August 2021, Hurricane Ida brought heavy flooding to the Louisiana coast before delivering so much water to the northeast that Philadelphia and New York City saw flooded subway stations days after the storm passed. Floods in Eastern Kentucky in 2022 further underscored the need for more comprehensive planning on how to deal with these disasters and reduce the nationwide flood protection gap. California and the Pacific Northwest have been hit in recent years by drenching “atmospheric rivers” and, most recently, Hurricane Hilary, which slammed Southern California and neighboring Nevada, where it turned the Burning Man festival in the state’s northern desert into a dangerous mess of foot-deep mud and limited supplies.

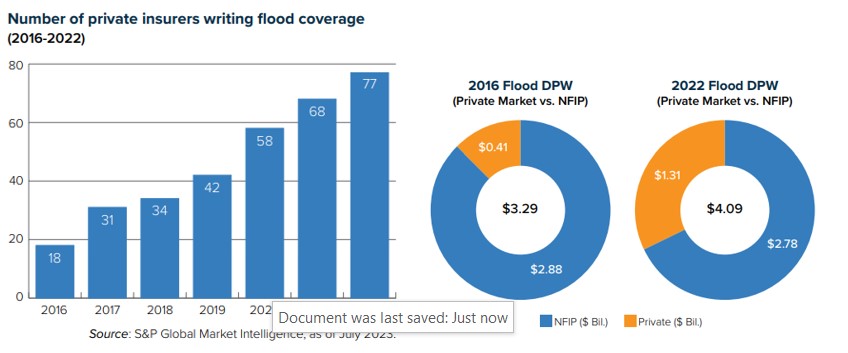

Flood insurance is provided by NFIP and a small but growing number of private insurers, who have become increasingly comfortable writing the coverage since the advent of sophisticated modeling and analytical tools. Between 2016 and 2022, the total flood market grew 24 percent – from $3.29 billion in direct premiums written (DPW) to $4.09 billion – with 77 private companies writing 32.1 percent of the business.

Flood risk was long considered untouchable by private insurers, which is a large part of the reason the federally run NFIP exists. While private participation in the flood market is growing, NFIP remains a critical source of protection for this growing and underinsured peril.

Want to know more about the risk crisis and how insurers are working to address it? Check out Triple-I’s upcoming Town Hall, “Attacking the Risk Crisis,” which will be held Nov. 30 in Washington, D.C.

Poor personal lines performance will keep the U.S. property/casualty insurance industry’s underwriting profitability constrained for at least the next two years, Triple-I’s chief insurance officer told attendees at a members only webinar today.

“We forecast net combined ratios to incrementally improve each year from 2023 to 2025,” said Dale Porfilio, FCAS, MAAA, “with the industry returning to a small underwriting profit in 2025.”

The industry’s combined ratio – a standard measure of underwriting profitability, in which a result below 100 represents a profit and one above 100 represents a loss – is expected to end 2023 at 102.2, almost matching the 2022 result of 102.4.

“Catastrophe losses in the first half of 2023 were the highest in over two decades, slightly higher than the record set in first half of 2021,” Porfilio said. Triple-I predicted net written premium growth for 2023 at 7.9 percent.

Michel Léonard, PhD, CBE, Triple-I’s chief economist and data scientist, discussed key macroeconomic trends impacting the P&C industry results including inflation, rising interest rates, and overall P&C underlying growth.

“U.S. CPI will likely stay in the mid-to-upper 3 percent range through the end of the year,” Léonard said, noting that underlying growth for private passenger auto has resumed its pre-pandemic trend. “Increases in replacement costs continue to decelerate and have now returned to pre-COVID trends as supply-chain backlogs and labor disruptions ended.”

Léonard added that U.S. GDP “will likely decrease on a quarterly basis in the second half of the year compared to the first half, but still avoiding a technical recession in 2023.”

For homeowners, Porfilio noted that the 2023 net combined ratio forecast of 104.8 is nearly identical to 2022 actual. He said homeowners incurred the majority of the first half of 2023 elevated catastrophes.

“A cumulative replacement cost increase of 55 percent from 2019-2022 contributes to our forecast of underwriting losses through 2025,” Porfilio added. “Premium growth in 2023-2025 is forecast to be elevated primarily due to rate increases.”

On the commercial side, Jason B. Kurtz, FCAS, MAAA, a principal and consulting actuary at Milliman, said commercial lines experienced underwriting gains in 2022.

“Commercial auto, however, was one commercial line that did not perform well in 2022,” he said. “For commercial auto, 2022 saw a return to underwriting losses, as the industry logged a 105.4 net combined ratio, the highest since 2019.”

“Workers compensation is the brightest spot among all major P&C product lines, with strong underwriting profitability forecast to continue through 2025,” Kurtz added. “Premium growth is expected to be modest, however, with approximately 3 percent growth each year.”

Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance, highlighted key factors that influenced the 2022 workers compensation results.

“Overall frequency continues its long-term negative trend as workplaces continue to get safer,” Glenn said. “Medical severity has remained moderate despite rising inflation, and wages and employment are above pre-pandemic levels. While severity was notably higher in 2022, it’s been moderate over the last few years. Together, these system dynamics result in a healthy and strong workers compensation system.”