Tariffs and threats of tariffs have been roiling financial markets since January. Property and casualty insurers are no less concerned, as the cost of repairing and replacing damaged property is a driver of claim costs and, ultimately, policyholder premiums.

Triple-I Chief Economist and Data Scientist Dr. Michel Léonard recently sat down to explain the implications of tariffs and trade barriers for insurers and what economic considerations concern industry decisionmakers.

While property and casualty insurers write many kinds of coverage, the lines Léonard primarily discussed were homeowners and personal and commercial auto – “lines that have a physical emphasis on repair, rebuild, and replace.”

Lumber from Canada; cars, trucks, and parts from Canada and Mexico; and garments, furnishings, and technology from Asia all come into play when considering the prospective impacts of tariffs on replacement costs, Léonard said.

“When we’re focusing specifically on China,” he said, “we’re looking primarily at farm equipment and alternative-energy components.”

Uncertainty around tariffs – particularly in recent weeks, as tariffs on Mexico and Canada have been imposed and “paused” – makes analysis even more difficult.

“Much depends on how much clarity there is, how much communication from the policymakers, from the administration and from the legislature,” Léonard said. It’s also important to remember that impacts can last well beyond their implementation and withdrawal.

During the first Trump Administration, tariffs on soft commodities, beef, grain, and so forth had impacts for several years afterwards.

“Those tariffs were fairly short lived,” Léonard said, “but for two to three years afterward farmers were uncomfortable investing in equipment at the same pace, and that reduced farmowners’ insurance growth.”

Regardless of how the current discussions around tariffs play out, the Trump Administration has signaled a decided shift in policy toward greater protectionism. As a result, Léonard said, “We should expect a repositioning in our understanding of our replacement costs and underlying growth forecast for the next 12 months, at a minimum.”

He projects a period of “most likely 24 to 36 months” in which growth will be slower and inflation – including replacement costs for the P&C industry – will be higher.

Florida’s legislative reforms to address claim fraud and legal system abuse are stabilizing the state’s property/casualty insurance market, according to the latest Triple-I Issues Brief.

Claims-related litigation has significantly declined over the past two years, and premium averages are nearly flat, with several insurers requesting rate decreases from the state’s insurance regulator. In addition, the brief says, the number of insurers writing business in the state has rebounded after a multi-year exodus. This competition from the private market has allowed policyholders to leave Citizens Property Insurance Corp. – the state-run insurer of last resort – to obtain coverage at previously unavailable rates from a much healthier private market.

According to the state’s Office of Insurance Regulation (OIR), Florida in 2022 accounted for nearly 71 percent of the nation’s homeowners claim-related litigation, despite representing only 15 percent of homeowners insurance claims. The same year – before Hurricane Ian made landfall in Florida – six insurers in the state declared insolvency, primarily due to economic pressures from legal system abuse. Based on insured losses, Ian became the second-most costly U.S. hurricane on record, due in large part to extraordinary litigation costs for disputed claims.

The Legislature responded to the growing crisis by passing several pieces of insurance reform that, among other things, eliminated one-way attorney fees and assignment of benefits (AOB) for property insurance claims and prohibited misleading legal service ads and the misuse of consumer health information for legal services.

Premium rate growth slowing

The impact of the 2022 and 2023 reforms can be seen in premium rate changes, particularly with respect to homeowners insurance. Homeowners rates in Florida grew at a much slower rate in 2024, even as rate growth remained strong nationally. Growth in personal auto insurance premium rates in Florida has slowed since the repeal of AOB and one-way attorney fees, but the trend also is consistent with nationwide experience.

“There are a lot of factors involved in insurance rates, and Florida’s property and auto markets are challenging,” Florida Governor Ron DeSantis said in February, “but…data suggests that, in 2024, Florida had the lowest average homeowners’ premium increases in the nation, and the overall market has stabilized, with 11 new companies having entered the market over the past two years.”

Among the top 10 national insurers writing homeowners insurance in Florida, 60 percent have expanded their business over the past year, and 40 percent of all insurers operating in the state filed for rate decreases in 2024, according to Florida Insurance Commissioner Michael Yaworksy.

The cost of reinsurance also continues to decrease for Florida carriers.

“In 2024, most companies paid less for reinsurance than they did in 2023,” according to the OIR website. “The average risk-adjusted cost for 2024 was -0.7 percent, a large reduction from last year’s change of 27 percent increase from the prior year.”

Reinsurance costs are factored into premium rates, so this is another reason Florida now has the lowest average rate filings in the United States in 2024, according to S&P Global Marketplace.

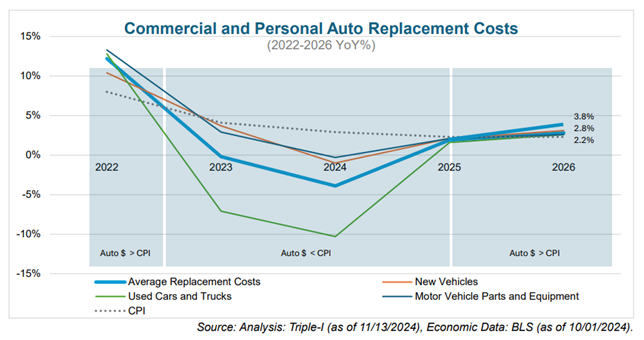

Triple-I expects the pace of increase in average property/casualty insurance replacement costs to exceed increases in the consumer price index in 2025 and beyond as auto replacement costs rise for the first time since 2022 and CPI continues to decline.

Triple-I’s replacement cost index for personal and commercial auto tracks changes in the price of vehicles, parts, and equipment that make up the replacement costs facing insurance carriers providing collision insurance for both personal and commercial motor vehicles. These costs – which have increased by as much as 30 percent over the past five years – are expected to increase by 2.8 percent in 2025.

The index combines replacement costs data for motor vehicles by age and for parts and equipment from the CPI for All Urban Consumers. These cost drivers were chosen from a wider selection of U.S. government sources, including the Bureau of Labor Statistics, Bureau of Economic Analysis, Federal Reserve, Census Bureau, and the Departments of Labor, Transportation, and Energy.

“While we expect the economic drivers of P/C insurance performance to continue improving 2025, performance will be constrained by replacement cost increases, rising natural catastrophe losses, and geopolitical uncertainty,” said Triple-I Chief Economist Dr. Michel Léonard.

By William Nibbelin, Senior Research Actuary, Triple-I

The U.S. Property & Casualty insurance market is expected to continue its trajectory of improving underwriting results in 2024 into 2025 and 2026, according to the latest projections by actuaries at Triple-I and Milliman. The latest report – Insurance Economics and Underwriting Projections: A Forward View – was released during Triple-I’s January 16 members-only webinar.

Year-over-year gains in net written premium increases and quarter-over-quarter loss ratios are primarily due to better-than-expected Q3 performance in personal auto.

The 2024 underlying economic growth for P&C ended slightly below U.S. GDP growth at 2.3 percent versus 2.5 percent year over year. A further economic milestone occurred in 2024, with the number of people employed in the U.S. insurance industry surpassing three million.

Michel Léonard, Ph.D., CBE, chief economist and data scientist at Triple-I, noted P&C underlying economic growth is expected to remain above overall GDP growth in 2025 (2.3 percent versus 2.1 percent) and 2026 (2.6 percent versus 2.0 percent) as lower interest rates continue to revive real estate and contribute to higher volume for homeowners’ insurance and commercial property.

“This is an improvement on our 2025 P&C underlying growth expectations from second half of 2024,” Léonard said. “The pace of increase in P&C replacement costs is expected to overtake overall inflation in 2025 (3.3 percent versus 2.5 percent). This aligns with our earlier expectations from the second half of last year.”

Personal vs. commercial lines performance

The 2024 net combined ratio for the P&C industry is projected to be 99.5, a year-over-year improvement of 2.2 points, with a net written premium (NWP) growth rate of 9.5 percent. Combined ratio is a standard measure of underwriting profitability, in which a result below 100 represents a profit and one above 100 represents a loss. Personal lines 2024 net combined ratio estimates improved by nearly 1 point, while the commercial lines 2024 estimates worsened by 1.2 points.

Dale Porfilio, FCAS, MAAA, Triple-I’s chief insurance officer, expanded upon the dichotomy of commercial and personal lines results.

“Commercial lines continue to have better underwriting results than personal lines, but the gap is closing,” Porfilio said. “The impact from natural catastrophes such as Hurricane Helene in Q3 2024 and Hurricane Milton in Q4 2024 significantly impacted commercial property. The substantial rate increases necessary to offset inflationary pressures on losses have driven the improved results in personal auto and homeowners.”

Personal auto and homeowners are each projected to have improved 6.1 points over 2023, with a 2024 net combined ratio of 98.8 and 104.8, respectively. NWP growth rate for personal lines is expected to surpass commercial lines by 9 points in 2024, with personal auto leading at 14.0 percent, the second highest in over 15 years.

Jason B. Kurtz, FCAS, MAAA, a principal and consulting actuary at Milliman – a premier global consulting and actuarial firm – elaborated on profitability concerns within commercial lines.

“Commercial auto continues to remain unprofitable,” he said. “The 2024 direct incurred loss ratio through Q3 is only marginally improved relative to 2023 and is the second highest in over 15 years.”

Hurricane Milton is projected to be the worst catastrophic event for commercial property since Hurricane Ian in 2022 Q3, driving higher-than-expected losses and subsequently increasing the commercial property projected 2024 net combined ratio up 3.3 points to 91.2, which is also 3.3 points worse than 2023. During the webinar, commercial property forecasts were also shared for the fire and allied and inland marine sub-lines.

Continued worsening in general liability

General liability’s projected 2024 net combined ratio of 103.7 is 3.6 points worse than actual 2023 experience. Kurtz said the line has seen significantly worsening, with each quarterly loss ratio in 2024 worse than 2023 year over year.

“The 2024 direct incurred loss ratio through Q3 is the highest in over 15 years,” Kurtz said. “As a result, we have increased our expectations for 2025 and 2026 net written premium growth, as the industry responds to the worsening 2024 performance.”

Continuing the discussion on general liability, Emma Stewart, FIA, chief actuary at Lloyds added that U.S. general liability has experienced material deterioration in loss ratios and a slowing down of claims development.

“A large driver of this has been the post-underwriting emergence of heightened social inflation, or more specifically, legal system abuse and nuclear verdicts,” Stewart said. “If these trends continue to increase, reserves on this class can be expected to deteriorate further.”

Workers comp loss-cost preview

Ending with workers compensation, Donna Glenn, FCAS, MAAA, chief actuary at the National Council on Compensation Insurance, provided a preview of this year’s average loss-cost changes and discussed the long-term financial health of the workers compensation system.

“The 2025 average loss cost decrease of 6 percent is moderate, which will inevitably have implications on the overall net written premium change,” Glenn said. She added that the –6 percent average loss cost level change in 2025 is notably different than the -9 percent average seen in 2024, the largest average decrease since before the pandemic.

“Payroll for 2025 will develop throughout the year resulting from both wage and employment levels. Therefore, overall premium will become clearer as the year progresses,” she said.

California’s Department of Insurance last week posted long-awaited rules that remove obstacles to profitably underwriting coverage in the wildfire-prone state. Among other things, the new rules eliminate outdated restrictions on use of catastrophe models in setting premium rates.

The measure also extends language related to catastrophe modeling to “nature-based flood risk reduction.” In the original text, “the only examples provided of the kinds of risk mitigation measures that would have to be considered in this context involved wildfire. However, because the proposed regulations also permit catastrophe modeling with respect to flood lines, it was appropriate to add language to this subdivision relating to flood mitigation.”

The relevant language applies “generally to catastrophe modeling used for purposes of projecting annual loss,” according to documents provided by the state Department of Insurance.

Benefits for policyholders

As a result, the department said in a press release, “Homeowners and businesses will see greater availability, market stability, and recognition for wildfire safety through use of catastrophe modeling.”

For the past 30 years, California regulations – specifically, Proposition 103 – have required insurance companies to apply a catastrophe factor to insurance rates based on historical wildfire losses. In a dynamically changing risk environment, historical data alone is not sufficient for determining fair, accurate insurance premiums. According to Cal Fire, five of the largest wildfires in the state’s history have occurred since 2017.

The state’s evolving risk profile, combined with the underwriting and pricing constraints imposed by Proposition 103, has led to rising premium rates and, in some cases, insurers deciding to limit or reduce their business in the state.

With fewer private insurance options available, more Californians have been resorting to the state’s FAIR Plan, which offers less coverage for a higher premium. This isn’t a tenable situation.

“Put simply, increasing the number of policyholders in the FAIR Plan threatens the solvency of insurance companies in the voluntary market,” California Insurance Commissioner Ricardo Lara explained to the State Assembly Committee on Insurance. “If the FAIR Plan experiences a massive loss and cannot pay its claims, by law, insurance companies are on the hook for the unpaid FAIR Plan losses…. This uncertainty is driving insurance companies to further limit coverage to at-risk Californians.”

“Including the use of catastrophe modeling in the rate making process will help stabilize the California insurance market,” said Janet Ruiz, Triple-I’s California-based director of strategic communication. “Homeowners in California will be able to better understand their individual risk and take steps to strengthen their homes.”

The new measure also requires major insurers to increase the writing of comprehensive policies in wildfire-distressed areas equivalent to no less than 85 percent of their statewide market share. Smaller and regional insurance companies must also increase their writing.

Requirements for insurers

It also requires catastrophe models used by insurers to account for mitigation efforts by homeowners, businesses, and communities – something not currently possible under existing outdated regulations today.

Moves like this by state governments – combined with increased availability of more comprehensive and granular data tools to inform underwriting and mitigation investment – will go a long way toward improving resilience and reducing losses.

The efficacy of collaboration and investment by “co-beneficiaries” in resilience initiatives was a dominant theme throughout Triple-I’s 2024 Joint Industry Forum – particularly in the final panel, which celebrated leaders behind recent real-world impacts of such investments.

Moderated by Dan Kaniewski, Marsh McLennan (MMC) managing director for public sector, the panelists discussed how their multi-industry backgrounds inform their innovative mindsets, as well as their knowledge on the profound ripple effects of targeted resilience planning.

The panel included:

Jonathan Gonzalez, co-founder and CEO of Raincoat;

Bob Marshall, co-founder and CEO of Whisker Labs;

Dawn Miller, chief commercial officer of Lloyd’s and CEO of Lloyd’s Americas; and

Lars Powell, director of the Alabama Center for Insurance Information and Research (ACIIR) at the University of Alabama and a Triple-I Non-Resident Scholar.

Productive partnership

Kaniewski – who spent most of his career in emergency management, previously serving as the second-ranking official at the Federal Emergency Management Agency (FEMA) and the agency’s first deputy administrator for resilience – kicked off the panel by raising the question “how do we define success?”

He characterized success as “putting theory into practice” and “having elected officials taking steps to reduce risk and transfer some of this risk from federal, state, or local taxpayers.”

But, as participants in earlier panels and this one made clear, government efforts can only go so far without private-sector collaboration.

“It doesn’t matter who makes that investment, whether it’s the homeowner, the business owner, or the government,” Kaniewski explained. “The reality is we all benefit from that one investment. If we can acknowledge that we benefit from those investments, we should do our best to incentivize them.”

Kaniewski and Raincoat’s Gonzalez were both integral in the development of community-based catastrophe insurance (CBCI), developed in the wake of Superstorm Sandy in 2012.

“A lot of the neighborhoods that experienced flooding due to Sandy didn’t have access to insurance prior to the flooding – and then, post flooding, the government really had to step up to figure out how to keep those families in those houses,” Gonzalez said.

In collaboration with the city, a nonprofit called the Center for NYC Neighborhoods developed the concept of buying parametric insurance on behalf of these communities, with any payouts going toward helping families stay in their homes after disasters. Unlike traditional indemnity insurance, a parametric policy pays out if certain agreed-upon conditions are met – for example, a specific wind speed or earthquake magnitude in a particular area – regardless of damage. Parametric insurance eliminates the need for time-consuming claim adjustment. Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders.

In this case, Kaniewski said, success was reflected in the fact that the pilot program received sufficient funding not only for renewal but expansion, bringing needed protection to even more vulnerable communities.

Powell reinforced this sentiment in explaining ACIIR’s research on the FORTIFIED method, a set of voluntary construction standards created by the Insurance Institute for Business and Home Safety (IBHS) for durability against severe weather. The insurance industry-funded Strengthen Alabama Homes program issues grants and substantial insurance premium discounts to homeowners to retrofit their houses along these guidelines, prompting multiple states to replicate the program.

Such homes in Alabama sustained 54 to 76 percent reduced loss frequency from Hurricane Sally compared to standard homes, Powell reported, and an estimated 65 to 73 percent could have been saved in claims if standard homes were FORTIFIED.

Incentivizing contractors to learn FORTIFIED standards was especially critical, Powell explained, because they further advertised these skills and expanded the presence of FORTIFIED homes beyond the grant program.

“A lot of companies have said for several years, ‘we don’t know if we’re comfortable writing these…we haven’t seen it on the ground,’” Powell said. “Well, now we’ve seen it on the ground. We need to have houses that don’t burn down or blow over. We know how to do it, it’s not that expensive.”

Addressing concerns to drive adoption

Miller described how Lloyd’s Lab works to ease that discomfort by creating a space for businesses to nurture and integrate novel insights and products without fear. With mentor support, companies are encouraged to test new ideas while free from the usual degree of financial and/or intellectual property risks attached to innovation investments.

“It’s about having an avenue out to try,” Miller said. “Having that courage, as we continue to work together, to try to understand what’s working, what’s not, and being brave to say, ‘this isn’t working, but we can course correct.’”

Whisker Labs’ Marshall noted that numerous insurance carriers have taken a chance on his company’s front-line disaster mitigation devices, Ting, by paying for and distributing them to their customers.

Ting plug-in sensors detect conditions that could lead to electrical fires through continuous monitoring of a home’s electrical system. Statistically preventing more than 80 percent of electrical fires, communities benefit – not only by preventing individual home fires but also by providing data about the electrical grid and potentially heading off grid-initiated wildfires.

“There are so many applications for the data,” Marshall said, but “to have a true impact on society…we have to prove that we’re preventing more losses than the cost, and we have to do that in partnership with insurance carriers.”

Everyone wins if everyone plays

Cultivating innovative solutions is pivotal to enhancing resilience, the panelists agreed – but driving them forward requires more than just the insurance industry’s support.

He pointed to a project last year – funded by Fannie Mae and developed by the National Institute of Building Science (NIBS) – that culminated in a roadmap for resilience investment incentives, focusing on urban flooding.

The co-authors of the project, including Triple-I subject-matter experts, represented a cross-section of “co-beneficiary” groups, such as the insurance, finance, and real estate industries and all levels of government, Kaniewski said.

Implementation of the roadmap requires participation from communities and multiple co-beneficiaries. Triple-I and NIBS are exploring such collaborations with potential co-beneficiaries in several areas of the United States.

Natural catastrophe perils’ rising frequency and severity may be impossible to fully abate, but Nationwide Property & Casualty Insurance Co. President and CEO Mark Berven believes modern building codes could dramatically reduce their costly destructiveness.

In a recent article for PropertyCasualty360, Berven wrote that inconsistent building codes create alarming safety disparities from state to state and that improved codes are essential to reducing risk and post-disaster recovery costs.

“Extreme weather events like heat waves, large storms, landslides and more are becoming more frequent and intense,” Berven writes. “The U.S. has already experienced at least 24 confirmed weather disaster events through October with losses exceeding $1 billion each.”

“Building Codes Save” — a landmark report by the Federal Emergency Management Agency (FEMA) –found that universal enforcement of modern building codes could prevent more than $600 billion in disaster losses by 2060. In states where stricter codes have been implemented, the report says, billion-dollar savings already have been realized.

Virginia and Florida, for example, have long-modeled robust building code systems, leading both to consistently top code adoption rankings – especially after the latter saved an estimated $1 billion to $3 billion in averted damages during Hurricane Ian through its modern Florida Building Code.

By contrast, fewer than one-third of hazard-prone jurisdictions have adopted modernized building codes, and some states – such as Delaware and Alabama – lack mandatory statewide building code systems entirely.

Perceived cost an obstacle

Barriers to adoption include the perceived expenses of enforcement. Conforming existing structures to the same standards as new buildings can be costly, as can rebuilding communities in non-hazardous areas. Navigating these concerns in tandem with an ongoing affordable housing shortage will require a coordinated effort on local, state, and federal levels.

But as the annual average of billion-dollar disasters in the U.S. trends upward, improving building codes must take precedence for policymakers at every level of government, Berven explained, adding that the research organization Insurance Institute for Business & Home Safety (IBHS) has already provided a versatile and relatively affordable outline for safer construction standards.

Known collectively as the FORTIFIED method, such standards reinforce the durability of homes against severe weather, involving, for example, anchoring roofs to wall framing using stronger nails. The FORTIFIED method is, at present, completely voluntary, though the insurance industry-funded Strengthen Alabama Homes incentivizes homeowners to retrofit their houses along these guidelines via thousand-dollar grants. Completed retrofits reduce post-disaster claims and qualify grantees for substantial insurance premium discounts, prompting flood-prone Louisiana to replicate the program.

Given the programs’ demonstrated success, “updating our building codes to align with proven frameworks like IBHS’s FORTIFIED standards is not just an option — it’s a necessity,” Berven wrote. “The time for action is now, and the cost of inaction is far too high.”

Many consumers are unaware of the current absence and potential benefits of building code regulations, he continued, emphasizing an industry need for greater public outreach. Building codes play an indispensable role in enhancing resilience against evolving climate and weather risks, but any “revolution” in their regulation cannot advance without the collaboration of all relevant stakeholders.

From “social inflation” to “tort reform” to, simply, “fraud,” settling upon uniform terminology to describe litigation trends that drive up costs – including insurance premiums – for all Americans is a primary challenge to addressing them, according to participants at Triple-I’s 2024 Joint Industry Forum.

“As we’re trying to raise awareness of this problem with consumers, ‘social inflation’ doesn’t work,” said discussion moderator and Triple-I’s Chief Insurance Officer Dale Porfilio. Though Triple-I previously favored “social inflation,” consumer testing was done that suggested a better name was needed. “That’s when we landed on ‘legal system abuse.’”

“The name absolutely matters,” said Viji Rangaswami, senior vice president and chief public affairs officer for Liberty Mutual. “When you talk to a legislator, whether that’s in Kansas or in Washington, D.C., and you say the words, ‘social inflation,’ they don’t know what you’re talking about. But when you say the words ‘legal system abuse,’ you see the lightbulb go off.”

Louisiana Insurance Commissioner Tim Temple – a self-described “unicorn” among insurance regulators, given his decades-long background in the industry as an agent, broker, and company president – even renamed programs to address “legal system abuse” when he assumed office in January. This shift exemplifies Temple’s commitment to using his experience to shape a regulatory and statutory environment that enhances the attractiveness of Louisiana’s insurance market.

“We’re getting more buy-in now, people understand it,” Temple said. “That’s part of transparency – talking about what it truly is.”

Clear communication is key

Opaque, ill-defined language empowers predatory “billboard attorneys” to define these terms themselves, contributing to pervasive policyholder distrust, said Jeff Sauls, Farmers Insurance head of legislative affairs.

“There’s this perception of the insurance industry amongst the public – and plaintiffs’ attorneys help portray this – as a high-margin business,” he said, when, in reality, “we compete with grocery stores for who can make less money in an average year.”

Attorney advertising – estimated to total over $2.4 billion across the U.S. last year – has commandeered the messaging once associated with insurers, noted Temple, who encouraged the industry to “take back that high ground” of providing “dependability and stability during the worst days of people’s lives” without overuse of brand mascots or jingles.

“We have to remind the public why we exist,” Rangaswami added. “We want to pay claims as expeditiously as possible…. We’re on the side of the consumer, whereas the plaintiffs’ attorney is often on their own side or the investor’s side.”

Third-party litigation funding

With her reference to “investors,” Rangaswami took aim at a little-known, rapidly growing practice called third-party litigation funding (TPLF), in which investors with no stake beyond potential profit step in to fund lawsuits against corporate entities perceived as having deep pockets. As of last year, such investors retained an estimated $15.2 billion in assets for U.S. litigation alone.

Only a handful of states require mandatory disclosure of TPLF, which enables hedge funds and other foreign funders to compound and profit from protracted and even fraudulent U.S. court cases. Secrecy surrounding TPLF prevents insurers and regulators from identifying, let alone mitigating, the risks of increased costs and time to resolve claims disputes.

Preventing adversaries to the U.S. from exploiting TPLF to influence settlement outcomes and access sensitive defense information is another concern.

“We’re looking at TPLF as potentially exacerbating national security risk,” said Jerry Theodorou, policy director for finance, insurance, and trade at the R Street Institute. “Most people don’t know what TPLF is and the way it can insidiously impact the economy, our businesses, our jobs.”

Everyone is affected

Legal system abuse costs the highly litigious states Louisiana and Georgia over 175,000 jobs combined and thousand-dollar “tort taxes” for each resident per year, earning both states recurring spots on the American Tort Reform Foundation’s list of “Judicial Hellholes.” They also rank among the least affordable places for auto and homeowners’ insurance by the Insurance Research Council – an affiliate of The Institutes, like Triple-I.

Louisiana recently enacted a law enforcing some oversight over TPLF, Temple noted, as well as repealed a unique “three-year rule” that impeded actuarially-sound underwriting. But as the state’s bodily injury claims climb well over the national average, more reform is needed to return insurance profitability to the state.

“One thing I would look to is importing some of the good things Florida has done,” Theodorou suggested, explaining that reform curtailing contingency and one-way attorneys’ fees “have brought down the number of lawsuits against insurance companies by 24 percent” for the second consecutive three-quarter period. “Notice of intention to sue is also down by double digits. It’s working, so let’s learn from that.”

Considering the fact that the former “poster child” for legal system abuse generated over 70 percent of all homeowners insurance litigation nationally in 2022 – despite accounting for only about 15 percent of total homeowners claims – Florida’s reduced premium growth and nine new property insurers this year reveal the likely efficacy of such reforms in other states.

Education and coalition building

But such reform requires advocacy, which requires consumer education and coalition building across diverse stakeholder groups, Rangaswami pointed out.

Fixing “an economy-wide problem,” she explained, requires an “economy-wide coalition.”

The end goal is not a “tilted playing field,” Sauls emphasized. “We’re trying to get to a place where we are all on level footing, without being exploited by plaintiffs’ attorneys.”

Legal system abuse “is going to be a pressure point for the industry moving forward,” stressed Fred Karlinsky, shareholder and global chair of Greenberg Traurig, LLP. “No state is immune from what we’ve seen in Florida.”

Karlinsky emphasized that spreading normalization of “nuclear” (over $10 million) and an emergent class of “thermonuclear” (over $100 million) verdicts will stall reform in newly targeted states.

Rangaswami pointed out that not all the news has been bad.

“We had some great wins in 2024,” she said, citing Florida’s improved insurance market and legislation introduced at both the federal and state levels as movement in a promising direction. “But we have to keep this momentum up.”

Triple-I’s Joint Industry Forum this week in Miami brought together subject-matter experts from across insurance, academia, government, and the nonprofit space to discuss climate resilience, legal system abuse, and – most important – what is being done and must continue to be done to ensure insurance availability and affordability during this period of evolving perils and policy challenges.

The insight-rich and engaging panels and “Risk Takes” will be generating Triple-I blog content for weeks to come. The following is a brief wrap-up.

While our times are “riskier than ever,” Triple-I CEO Sean Kevelighan pointed out that the U.S. property/casualty insurance industry “is well poised to manage these risks.” At the same time, he and many participants noted that collaboration and coalition building are critical for long-term success.

With respect to climate resilience, such collaboration is already taking place. Veronika Torarp, a partner in PwC Strategy’s insurance practice and moderator of the Climate Resilience panel, discussed the multi-industry coalition PwC is developing with Triple-I and other partners. Marsh McLennan’s managing director for public sector Dan Kaniewski – who moderated the Success Stories panel – discussed a project funded last year by Fannie Mae and managed by the National Institute of Building Sciences (NIBS) that culminated in a roadmap to incentivize investment in urban flood resilience across “co-beneficiary” groups.. Triple-I played an integral role in the NIBS project, which is currently seeking communities and partners for implementation of the roadmap.

In the area of legal system abuse, there was much conversation around the benefits to Florida of recent reforms in terms of making the Sunshine State more attractive to insurers again by discouraging excessive and fraudulent litigation. Legal system abuse is a multi-headed monster that drives up costs for everyone – from home and car owners to businesses and taxpayers – and, although progress has been made to fight it in Florida and elsewhere, it is expanding as quickly as those states are able to advance in tamping it down. Triple-I’s Dale Porfilio moderated a lively panel on the topic that included Louisiana Insurance Commissioner Tim Temple; Farmers Insurance head of legislative affairs Jeff Sauls; Viji Rangaswami, senior vice president and chief public affairs officer for Liberty Mutual; and Jerry Theodorou, policy director for finance, insurance, and trade at the R Street Institute.

Peter Miller, president and CEO of The Institutes, moderated the Innovation panel, which included Denise Garth, chief strategy officer at Majesco; Paul O’Connor, vice president of operational excellence at ServiceMaster; Kenneth Tolson, global president for digital solutions at Crawford & Co.; and Reggie Townsend, vice president and head of the data ethics practice at SAS. These subject-matter experts discussed how generative AI and other technologies are transforming insurance strategy and operations and increasing opportunities to improve and advance this most human-centered industry.

All four panels – as well as the Risk Takes and the “Fireside Chat” featuring Kate Horowitz, executive vice president of The Institutes, and Casey Kempton, president of personal lines for Nationwide Insurance – will be reported on in greater detail in subsequent posts.

By William Nibbelin, Senior Research Actuary, Triple-I

Insurance is priced to reflect the underlying risk of every policy. When more claims are filed and the average amount paid of those claims increases, insurance becomes more expensive. A measure of underwriting profitability for insurance carriers is the combined ratio calculated as losses and expense divided by earned premium plus operating expenses divided by written premium. A combined ratio over 100 represents an underwriting loss. When expected losses increase, an insurance carrier must increase premiums by raising rates to maintain a combined ratio under 100.

Commercial auto insurance has recorded a net combined ratio over 100 nine times out of 10 between 2014 and 2023, and, according to the latest forecasting report by Triple-I and Milliman, continues to worsen in 2024. According to the Triple-I Issues Brief, personal auto insurance has had a net combined ratio over 100 for the past three years, with a 2023 net written premium (NWP) growth of 14.3 percent, which was the highest in over 15 years.

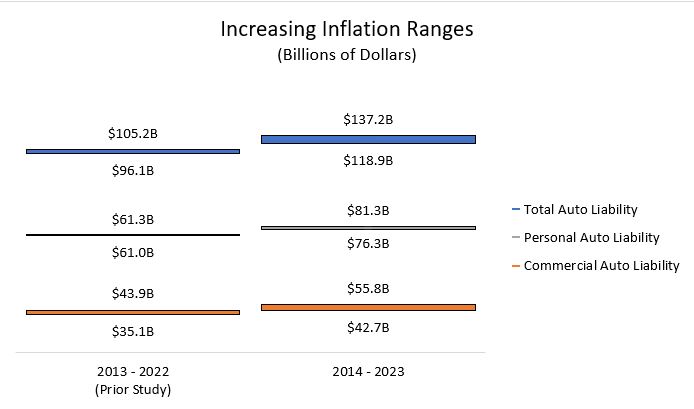

From 2014 through 2023 economic and social inflation added $118.9 billion to $137.2 billion in auto liability losses and defense and cost containment (DCC) expenses. This represents 9.9 percent to 11.5 percent of the $1.2 trillion in net losses and DCC for the period and an increase of 24 percent to 31 percent from the previous analysis on years 2013 through 2022.

A new study – “Increasing Inflation on Auto Liability Insurance – Impact as of Year-end 2023” – is the fourth installment of research on the impact of economic and social inflation on insurer costs and claim payouts. Compared to the prior study, Commercial Auto Liability loss and DCC is 20.7 percent to 27.0 percent ($43 billion to $56 billion) higher due to increasing inflation. Personal auto liability loss and DCC is 7.7 percent to 8.2 percent ($76 billion to $81 billion) higher from increasing inflation.

Key Takeaways

The compound annual impact of increasing inflation ranges from 2.2 percent to 2.9 percent for commercial auto liability, which is higher than the personal auto liability estimate of 0.7 percent. However, the impact of increasing inflation from a dollar perspective is much higher for personal auto liability compared to commercial auto liability. This is due, in part, to the underlying size of the line of business.

Frequency of auto liability claims per $100 million GDP for 2023 is unchanged for commercial auto liability and lower for personal auto liability compared to 2020, when frequency dropped at the onset of the COVID-19 pandemic for both lines.

Severity of auto liability claims continues to increase year over year and has increased more than 70 percent from 2014 to 2023 for both lines.

Researchers Jim Lynch, FCAS, MAAA, Dave Moore, FCAS, MAAA, LLC, Dale Porfilio, FCAS, MAAA, Triple-I’s chief insurance officer, and William Nibbelin, Triple-I’s senior research actuary used a similar methodology as prior studies. Loss development patterns were used to identify inflation for selected property/casualty lines in excess of inflation in the overall economy. The new study extends the model with annual statement data through year-end 2023.

Commercial Auto Liability

The prior study indicated claim severity (size of losses) had risen 72 percent overall from 2013 to 2022, with the median annual increase at 6.3 percent. The new study indicates an additional annual increase of 6.6 percent from 2022 to 2023. The report compares the compound annual growth rate of 6.6 percent from 2014 through 2023 to the compound annual increase in the consumer price index (CPI) of 2.8 percent during this same time. With a flat frequency trend combined with an increasing severity trend in recent years for commercial auto liability, this comparison calls out the higher inflation faced by insurers beyond just general inflation trends.

Personal Auto Liability

While replacement costs remain flat to negative providing relief to personal auto physical damage, personal auto liability represents approximately 60 percent of the overall personal auto line. Similar to commercial auto liability – but slightly lower – claim severity for personal auto liability has increased at a compound annual rate of 6.3 percent from 2014 through 2023. However, unlike commercial auto liability, the frequency for personal auto liability has declined slightly in 2022 and 2023, with 85 claims per $100 million GDP in 2023 compared to 90 in 2022 and 100 in 2021.

Limitation of industry data

The report relies on industry data as reported by insurers to the National Association of Insurance Carriers (NAIC) and made available through different reporting suppliers, such as S&P Global Market Intelligence. As such, different individual inflationary elements – whether economic, social, or otherwise – cannot be determined using the underlying actuarial methodologies.

However, like prior studies the bulk of increasing inflation before 2020 is attributed to social inflation, while social inflation and economic inflation dominate increasing inflation together beginning in 2020.

Triple-I continues to foster a research-based conversation around social inflation as part of legal system abuse. For an overview of the topic and other helpful resources about its potential impact on insurers, policyholders, and the economy, check out our knowledge hub.