By William Nibbelin, Senior Research Actuary, Triple-I

The U.S. personal auto insurance industry saw a significant turnaround in 2024, achieving its best underwriting result since the pandemic began, according to Triple-I’s latest Issues Brief.

In fact, with a net combined ratio of 95.3, personal auto insurance has outperformed the broader property and casualty (P/C) insurance industry in terms of underwriting profitability for 10 out of the last 20 years. A combined ratio under 100 indicates an underwriting profit. One above 100 indicates a loss.

This positive shift comes after a period in which personal auto premiums experienced fluctuations. While the overall P/C industry outpaced personal auto in premium growth from 2018 to 2022, personal auto saw a strong rebound in 2023 and 2024, with double-digit premium growth rates of 14.4 percent and 12.8 percent, respectively. This surge in premiums follows a notable decline in 2020, the first since 2009, largely due to reduced driving during the initial phase of the COVID-19 pandemic. Since then, vehicle miles driven have returned to pre-pandemic levels.

A major factor influencing auto insurance premiums has been the significant rise in replacement costs for vehicles and parts after the pandemic. Insurers adjusted rates in response to these increased costs. The changes in consumer prices for new and used vehicles, as well as parts and repairs, have shown a strong correlation with average insurance rate adjustments over the past decade:

- New Vehicles: 88 percent correlation;

- Motor Vehicle Parts & Equipment: 74 percent correlation;

- Used Vehicles: 79 percent correlation; and

- Motor Vehicle Maintenance & Repair: 78 percent correlation.

Looking at losses, the direct incurred loss ratio for personal auto improved considerably by 21.7 points from late 2022 to the end of 2024. However, this improvement wasn’t uniform across all types of claims. Auto physical damage claims saw more improvement than auto liability claims, creating the largest disparity between the two in over a decade of 15.7 points.

Loss trends in personal auto are shaped by how often claims occur (frequency) and the average cost of each claim (severity). For personal auto liability, while the number of claims has stayed below pre-pandemic levels, the average cost per claim has continued to rise year after year with a cumulative increase from 2019 to 2024 of 54.2 points.

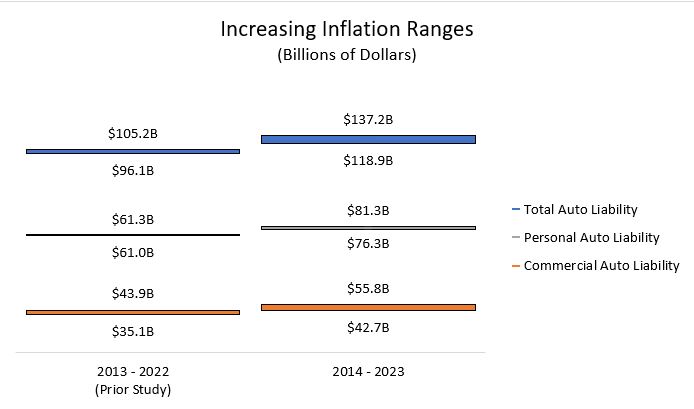

One of the significant challenges contributing to the increasing severity in personal auto liability is what’s known as legal system abuse. This includes a rise in lawsuits, larger jury awards, and more attorney involvement in claims. This phenomenon, intertwined with broader inflation, has driven up auto liability losses and related expenses by a range of $76.3 billion to $81.3 billion from 2014 to 2023 according to the latest Triple-I | Casualty Actuarial Society study.

Another important factor impacting the auto insurance market is the state regulatory environment. A recent report by the Insurance Research Council on Rate Regulation in Personal Auto Insurance indicated that the process for insurers to get rate changes approved has become more complex across the country between 2010 and 2023. This has led to longer approval times and a higher incidence of insurers receiving less than their requested rate increases. These trends can ultimately affect the availability of competitive auto insurance policies for consumers.

Learn More:

Even With Recent Rises, Auto Insurance Is More Affordable Than During Most of Century to Date

New IRC Report: Personal Auto Insurance State Regulation Systems