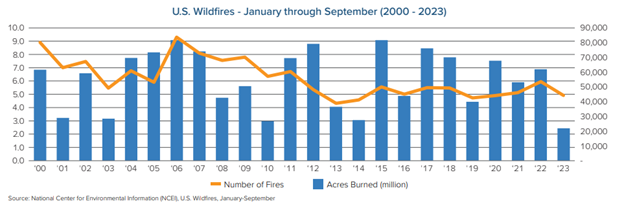

With record-breaking wildfires making headlines in recent years, it may be surprising to learn that U.S. wildfire frequency and severity for in 2023 are on track to be the lowest in the past two decades. In fact, the trend has been generally downward since 2000, according to a recently published Triple-I Issues Brief.

Despite catastrophic losses in Washington State, Hawaii, Louisiana, and elsewhere, California – a state often considered synonymous with wildfire – is in the midst of its second mild fire season in a row. This may be due to drought-breaking rains and snows, but Texas is experiencing fewer wildfires than in 2022, despite worsening drought conditions. About 37 percent of the continental U.S. remains under some form of drought, according to the U.S. Drought Monitor.

At the same time, Swiss Re reports that wildfire’s share of insured natural catastrophe losses has doubled over the past 30 years. How can those trends be reconciled? At least part of the answer resides in population trends – specifically, growing numbers of people choosing to live in the wildland-urban interface (WUI), the zone between unoccupied and developed land, where structures and human activity intermingle with vegetative fuels.

Mitigation is necessary – but not sufficient

The improvements in frequency and severity are likely due to investments in mitigation. State and local authorities have invested heavily to mitigate the human causes of wildfire. In addition, the federal Infrastructure and Jobs Act of 2021 included billions to support wildfire-risk reduction, homeowner investment in mitigation, and improved responsiveness to fires. More recently, the Biden Administration announced $185 million for wildfire mitigation and resilience as part of the Investing in America Agenda, which should help continue the declines in frequency and severity.

But with more people living in the WUI – nearly 99 million, or one third of the U.S. population, according to the U.S. Fire Administration – more than 46 million homes with an estimated value of $1.3 trillion are at risk.

According to the 2022 Annual Report of Wildfires produced by the National Interagency Fire Center (NIFC), 68,988 wildfires were reported and 7.5 million acres burned in 2022. Of these fires, 89 percent were caused by human activity and burned 55 acres per fire. By contrast, the 11 percent of fires caused by lightning resulted in an average of 563 acres burned, 10 times more than human-caused fires.

This difference may shed light on why the number of fires has been decreasing more dramatically than acres burned. Further, population shifts into the WUI are increasing the proximity of property to places prone to fire, helping to explain the rise in wildfire’s increased percentage of insured losses.

CSAA Insurance Group – a AAA insurer – is spurring innovation in the insurance industry through several initiatives tackling the dangers of climate risk.

“We’ve been on a journey to reduce our environmental footprint for a long time,” said Debbie Brackeen, Chief Strategy & Innovation Officer with CSAA, in a recent executive exchange with Triple-I CEO Sean Kevelighan. “We are seeking to reduce our carbon footprint by 50 percent by 2025. We view this work as aligned with our mission: to help our members prepare for and recover from climate risk.”

CSAA has taken several steps to help achieve its goals, including:

Leading the first-ever Innovation Challenge on climate resilience with IDEO and Aon, along with several other sponsors;

Working on the California Innovation Fund in partnership with Blue Forest, a $50 million fund that CSAA contributed half that capital, focused on forest restoration and reducing fuel in a smart and sustainable way; and

Supporting the Wildfire Interdisciplinary Research Center at San Jose State University, which conducts work around predictive modeling, among other endeavors.

While this may seem like a new development, Kevelighan noted that insurers have long worked toward these goals.

“We’ve seen the ESG movement take a hold in the past few years, but it’s been in the DNA of the Triple-I and the insurance industry generally for a long time,” Kevelighan said. “More than half the battle is recognizing that the risk is increasing, while identifying solutions.”

Still, with the increasing consequences associated with climate risk, more work needs to be done.

“There were billion-dollar wildfire losses at CSAA in my first two years in the industry,” Brackeen said. “I wondered if this was normal. It ignited in me that, whatever we do in innovation, it will have to do with wildfire risk. However, what concerns me the most is that risks are becoming uninsurable. This is from the cumulative effects of several different types of losses, including convective storms.”

“We have to seek different types of innovative partnerships to address these issues,” Brackeen concluded. “In this fight for our industry, there are no competitors. We have to be on the same side of the table.”

Of the findings in Triple-I’s recent report on consumer perceptions of weather risk, the Weather Channel’s experts were most struck by the fact that 60 percent of homeowners said they’d taken no steps to prepare – so, they asked Triple-I Chief Insurance Officer Dale Porfilio for his perspective.

Ultimately, Porfilio said, it comes down to perceptions.

“Two thirds of the people surveyed said they don’t expect to be affected by weather risk in the next five years,” Porfilio told the Weather Channel. “If you don’t think you’re going to be impacted, why would you prepare with a home evacuation plan or a home inventory?”

Of course, anyone who is exposed to weather is exposed to weather-related risk, and it’s essential for homeowners to understand and address the most relevant risks in order to protect their investments and their families.

Porfilio also addressed a question regarding availability of flood insurance, explaining that coverage is generally available through the Federal Emergency Management Agency’s National Flood Insurance Program, as well as a growing number of private insurers, but “might be perceived as too expensive.”

It is possible, however, that some insurers might not be willing to offer coverage in areas that have been hit repeatedly by flood.

Awareness and preparation are key. The Triple-I survey, published in coordination with global reinsurer Munich Re, found that, among the 22 percent of respondents who reported understanding their level of flood risk, 78 percent said they had purchased flood insurance. The report, Homeowners Perception of Weather Risks, provides insights into trends, behavior and how experiencing a weather event impacts consumer perceptions of future events.

By Loretta L. Worters, Vice President, Media Relations, Triple-I

Fire historically has been the main risk associated with the peril of lightning strikes. But as urban density increases and society’s dependence on electrical and electronic devices rises, lightning damage can be far more significant than the average home or business owners realizes.

According to a Triple-I analysis of State Farm data compiled to coincide with Lightning Safety Awareness Week (June 18-24), $952 million in lightning-caused U.S. homeowners insurance claims were paid out in 2022 to more than 62,000 policyholders. There was good news in the data, including:

The total value of lightning-caused U.S. homeowners insurance claims fell more than 27 percent in 2022 ($952 million) from 2021 ($1.3 billion).

The number of lightning-caused U.S. homeowners insurance claims only slightly increased, by 2.2 percent between 2021 and 2022 from 60,851 to 62,189, with numbers from the top 10 claims states contributing to about half of the total.

The average cost per lightning-caused claim decreased 29 percent, from $21,578 in 2021 to $15,280 in 2022.

“Insurers are moving toward predicting and preventing losses by advocating for resilience in coordination with the real-time application of technology,” said Triple-I CEO Sean Kevelighan. “Lightning Safety Awareness Week highlights the dangers lightning poses to life and property and how insurers and policyholders are reducing these risks.”

Homes aren’t the only structures at risk from lighting damage. In a recent interview with Kevelighan, Tim Harger – executive director of the Lightning Protection Institute – said an East Coast furniture manufacturer was subjected to “just over a million dollars in damage” when it was struck.

“Yes, there was the typical fire that caused structural damage, but what was impacted on the ‘inside’ was even more costly,” he said. “They had damaged inventory, production downtime, and loss of revenue during the repairs.”

Investment in a lightning protection system could have saved this business owner – and his insurer – the million dollars lost and prevented the business interruption.

“When it comes to protecting homes, businesses or critical facilities in communities, we know that a properly installed lighting protection system is scientifically proven to mitigate the damage from a lightning strike,” Harger said.

While cities have lightning issues, so do parts of the country where lightning-ignited wildfires are significant. According to the Congressional Research Service, most wildfires are human-caused (89 percent of the average number of wildfires from 2018 to 2022). However, wildfires caused by lightning tend to be slightly larger and to burn more acreage (53 percent of the average acreage burned from 2018 to 2022) than human-caused fires.

Florida, Georgia, Texas and California Lead Lightning Losses

Not surprisingly, Florida – the state with the most thunderstorms — remained the top state for number of lightning claims in 2022, with 5,504, followed by Georgia, with 4,474. However, California had the highest average cost per claim, at $36,319, followed by Texas, with $25,286.

Damage caused by lightning, such as fire, is covered by standard homeowners insurance policies. Some homeowners policies provide coverage for power surges that are the direct result of a lightning strike.

The 2023 Atlantic hurricane season officially started June 1 and is forecast to be a busy one, which is why homeowners need to prepare. Yet many lack even the most basic preventative measures, unaware of the risks they face, according to a new survey by Triple-I, in coordination with Munich Re.

The new report, Homeowners Perception of Weather Risks,provides insights into trends, behavior and how experiencing a weather event impacts consumer perceptions of future events.

In the first half of 2023, Triple-I, in coordination with Munich Re, asked homeowners across the United States about their experiences with weather-related risks. Among the key findings:

Twenty-five percent of respondents don’t expect to be impacted by weather risks in the future.

Thirty-two percent report that they have been impacted by weather in the last five years.

Two primary ways to prepare for weather risk includes creating a home inventory and an evacuation plan in case of emergency. Yet only 47 percent of respondents have a home inventory and slightly more (52 percent) have an evacuation plan.

Thunderstorms are reported as the chief weather concern, at 54 percent nationally. This includes flooding and tornados and varies by geographic region. The Midwest leads the area of highest reported thunderstorm risk, at 75 percent, and the West region reports the lowest proportion of concern, at 33 percent.

The survey suggests awareness and education around flood risk are the greatest opportunity for getting homeowners to take the necessary steps to protect their property. For example, among the 22 percent of respondents who reported understanding their flood risk, 78 percent said they had purchased flood insurance.

The cost of claims per insured home in the United States has increased at a rate outpacing inflation over the past 20 years, according the Insurance Research Council (IRC) — like Triple-I, an affiliate of The Institutes.

A new IRC study, Trends in Homeowners Insurance Claims: 2001–2021, attributes this to a combination of natural catastrophes, human-made disasters, rising home-repair costs, and ongoing population migration into disaster-prone areas.

Insurers also continue to wrestle with insurance fraud and claim abuse following disastrous events. These trends have cut into profits and led several major insurers to reduce their capacity in some U.S. states or leave the homeowners market entirely.

Other findings include:

Countrywide average loss costs (average claim payment per insured home) increased throughout the past two decades and rose nine percent in 2021.

Claim severity is increasing, while frequency is declining—in part because of widespread adoption of higher policyholder deductibles, including percentage deductibles for specified perils, and premium surcharge programs designed to reduce the number of lower-cost claims.

Catastrophe losses play an increasing role because of natural disaster trends and the methods used to define and categorize catastrophe claims.

Average loss costs for claims vary widely by state. States with the highest loss costs are Louisiana and Mississippi; states with the lowest are Hawaii and Maine.

States with the highest claim frequency over the period include Louisiana, Mississippi, and Oklahoma. States with the highest severity include California, Alaska, and Florida.

“During the two decades of the study period, the U.S. homeowners market has experienced a surge in volatility, mainly driven by a barrage of disasters, such as hurricanes Katrina, Ike, Michael, Rita, Sandy and Wilma and California fires,” said Dale Porfilio, IRC president and chief insurance officer for Triple-I.

Porfilio also noted that another challenge facing the homeowners insurance market is the continued threat of insurance fraud and claim abuse, especially after natural disasters.

“Industry and government organizations have increased efforts to inform consumers about potential scams, to investigate and prosecute the perpetrators, and to enact legislative changes to make systems less vulnerable to abuse,” Porfilio added.

The Louisiana property insurance market has been deteriorating since the state was hit by a record level of hurricane activity during the 2020/2021 seasons, Triple-I says in a new Issues Brief on the state’s insurance crisis. Twelve insurers that write homeowners coverage in Louisiana were declared insolvent between July 2021 and February 2023.

“While similarities exist between the situations in these two hurricane-prone states, the underlying causes of their insurance woes are different in important ways,” said Mark Friedlander, Triple-I’s director of corporate communications. “Florida’s problems are largely rooted in decades of litigation abuse and fraud, whereas Louisiana’s troubles have had more to do with insurers being undercapitalized and not having enough reinsurance to withstand the claims incurred during the record-setting hurricane seasons of 2020 and 2021.”

Insurers have paid out more than $23 billion in insured losses from over 800,000 claims filed from the two years of heavy hurricane activity. The largest property loss events were Hurricane Laura (2020) and Hurricane Ida (2021). The growing volume of losses also drove a dozen insurers to voluntarily withdraw from the market and more than 50 to stop writing new business in hurricane-prone parishes.

This is not to say legal system abuse is absent as a factor in the Louisiana’s crisis – quite the opposite, as highlighted by Insurance Commissioner Jim Donelon’s cease-and-desist order, issued in February, against a Houston-based law firm. According to Donelon, the firm filed more than 1,500 hurricane claim lawsuits in Louisiana over the span of three months last year.

“The size and scope of McClenny, Moseley & Associates’ illegal insurance scheme is like nothing I’ve seen before,” Donelon said. “It’s rare for the department to issue regulatory actions against entities we don’t regulate, but in this case, the order is necessary to protect policyholders from the firm’s fraudulent insurance activity.”

McClenny Moseley has since been suspended from practice in Louisiana’s Western District federal court over its work on Hurricane Laura insurance cases.

A regular on the American Tort Reform Foundation’s “Judicial Hellholes” list, Louisiana’s “onerous bad faith laws contribute significantly to inflated claims payments and awards,” according to a joint paper published by the American Property Casualty Insurance Association (APCIA), the Reinsurance Association of America (RAA), and the Association of Bermuda Insurers and Reinsurers (ABIR).

“Insurers who fail to pay claims or make a written offer to settle within 30 days of proof of loss may face penalties of up to 50 percent of the amount due, even for purely technical violations,” the paper notes. “To avoid incurring these massive penalties, which are meted out pursuant to highly subjective standards of conduct, insurers sometimes feel compelled to pay more than the actual value of claims as the lesser of two evils.”

As a result of these converging contributors, Louisiana Citizens Property Insurance Corp. – the state-run insurer of last resort – has grown from 35,000 to 128,000 policyholders over the past two years, according to the Louisiana Department of Insurance.

Florida Gov. Ron DeSantis’s proposed insurance fraud and legal system abuse reforms, announced this week for consideration during the legislative session that begins in March, would build on measures approved in the closing weeks of 2022 and go a long way toward fixing the state’s insurance crisis.

Legislation passed during the 2022 special session eliminated one-way attorney fees and assignment of benefits (AOB) arrangements for property insurance claims. Gov. DeSantis’s proposal would go further, eliminating these mechanisms and “attorney fee multipliers” for all lines of insurance.

“For decades, Florida has been considered a judicial hellhole due to excessive litigation and a legal system that benefitted the lawyers more than people who are injured,” DeSantis said in his announcement. “We are now working on legal reform that is more in line with the rest of the country and that will bring more businesses and jobs to Florida.”

Before the 2022 reforms, state law required insurers to pay the fees of homeowners insurance policyholders who successfully sued over claims, while shielding policyholders from paying insurers’ attorney fees when the policyholders lose. The legislation also eliminated AOBs – agreements in which property owners sign over their claims to contractors, who then work with insurers.

AOBs are a standard practice in insurance, but in Florida this consumer-friendly convenience has long served as a magnet for fraud. The state’s legal environment – including some of the most generous attorney-fee mechanisms in the country – has encouraged vendors and their attorneys to solicit unwarranted AOBs from tens of thousands of Floridians, conduct unnecessary or unnecessarily expensive work, then sue insurers that deny or dispute the claims.

As a result, Florida accounts for nearly 80 percent of the nation’s homeowners’ insurance lawsuits, but only 9 percent of claims, according to the state’s Office of Insurance Regulation.

Eliminating these two mechanisms for property claims addresses much of the insurance fraud in the state. Eliminating them for all lines would be a promising sign that the state is truly committed to addressing the root causes of the crisis.

Florida’s insurance crisis didn’t happen overnight, and it will take years for the impacts of fraud and legal system abuse to be wrung out of the system. Policyholders won’t see premium benefits any time soon. Job 1 is to “stop the bleeding” as insurers fail, leave the state, or stop writing critical personal lines coverages like auto and homeowners.

Triple-I has published a new Issues Brief about the crisis and the state’s efforts to repair it.

Legislation being considered in Illinois underscores the need for legislators and other policymakers to become better educated about the importance of risk-based pricing and how it works.

The Motor Vehicle Insurance Fairness Act would bar insurers from considering nondriving factors, such as credit scores, when setting premium rates. The prohibitions include factors that actuaries have demonstrated correlate strongly with the likelihood of a driver eventually submitting a claim, as well as ones insurers already are prohibited from using.

This suggests a lack of understanding about risk-based pricing that is not isolated to Illinois legislators – indeed, similar proposals are submitted from time to time at state and federal levels.

Confusion is understandable

Risk-based pricing means offering different prices for the same coverage, based on risk factors specific to the insured person or property. If policies were not priced this way, lower-risk drivers would subsidize riskier ones. Charging higher premiums to higher-risk policyholders helps insurers underwrite a wider range of coverages, improving both availability and affordability of insurance.

The concept becomes complicated when actuarially sound rating factors intersect with other attributes in ways that can be perceived as unfairly discriminatory. For example, concerns are raised about the use of credit-based insurance scores, geography, home ownership, and motor vehicle records in setting home and car insurance premium rates. Critics say this can lead to “proxy discrimination,” with people of color in urban neighborhoods being charged more than their suburban neighbors for the same coverage.

Confusion is understandable, given the complex models used to assess and price risk. To navigate this complexity, insurers hire actuaries and data scientists to quantify and differentiate among a range of risk variables while avoiding unfair discrimination.

Appropriate protections are in place

It’s important to remember that insurers don’t make money by notinsuring people. They are in the business of pricing, underwriting, and assuming risk.

Because of the critical role insurers play in facilitating commerce and protecting the lives and property of individuals, insurance is one of the most heavily regulated industries on the planet. To ensure that sufficient funds are available to pay claims, regulators require insurers to maintain a cushion called policyholder surplus.

Credit rating agencies, such as Standard & Poor’s and A.M. Best, expect insurers to have surpluses exceeding what regulators require to keep their financial strength ratings. A strong financial strength rating enables insurers to borrow money at favorable rates – further promoting insurance availability and affordability.

On top of these constraints, state regulators have the authority to limit the rates insurers can charge within their jurisdictions.

No profit, no insurers — no insurers, no coverage

Like any other business, insurers must make a reasonable profit to remain solvent. Because they can’t just move money around as more lightly regulated industries can, the only way to generate underwriting profits is through rigorous pricing and expense and loss controls. Insurers don’t want to overcharge and send consumers shopping for a better price, or undercharge and experience losses that erode their ability to pay claims.

In this context, it’s important to note that personal auto and homeowners insurance premium rates have remained relatively flat as inflation and replacement costs have soared through the pandemic and supply-chain issues related to Russia’s invasion of Ukraine (see chart below).

During this period, writers of these coverages have struggled to turn an underwriting profit. Personal auto has been a primary driver of the overall industry’s weak underwriting results. Dale Porfilio, Triple-I’s chief insurance officer, recently said the 2022 net combined ratio for personal auto insurance is forecast at 111.8, 10.4 points worse than 2021 and 19.3 points worse than 2020. Combined ratio represents the difference between claims and expenses paid and premiums collected by insurers. A combined ratio below 100 represents an underwriting profit, and one above 100 represents a loss.

Even as inflation moderates, loss trends in both of these lines – associated with increased accident frequency and severity in auto and extreme-weather trends in homeowners and auto – will require premium rates to rise. The question is: Will the cost fall evenly across all policyholders, or will rates more accurately reflect policyholders’ risk characteristics?

Protected classes

The United States recognizes “protected classes” – groups who share common characteristics and for whom federal or state laws prohibit discrimination based on those traits. Race, religion, and national origin are most commonly meant when describing protected classes in the context of insurance rating, and insurers generally do not collect information on these “big three” classes. Any discrimination based on these attributes would have to arise from using data that might serve as proxies for protected classes.

Algorithms and machine learning hold great promise for ensuring equitable pricing, but research shows these tools can amplify implicit biases.

The insurance industry has been responsive to such concerns. For example, recent Colorado legislation requires insurers to show that their use of external data and complex algorithms does not discriminate against protected classes, and the American Academy of Actuaries has offered extensive guidance to the state’s insurance commissioner on implementation. The Casualty Actuarial Society also recently published a series of papers (see links at end of post) on the topic.

Correlation matters

Certain demographic factors have been shown to correlate with increased risk of submitting a claim. Gender and age correlate strongly with crash involvement, as the National Highway Traffic Safety Administration (NHTSA) data illustrated at right shows.

Likewise, National Association of Insurance Commissioners (NAIC) data below clearly shows higher credit scores correlate strongly with lower crash claims.

Similar correlations can be shown for other rating factors. It’s important to remember that no single factor is determinative – many are used to assess a policyholder’s risk level.

Consumers “get it” – when it’s explained to them

A recent study by the Insurance Research Council (IRC) found consumer skepticism about the connection between credit history and future insurance claims appears to decline when the predictive power of credit-based insurance scores is explained to them. Through an online survey with more than 7,000 respondents, IRC found that:

Nearly all believe it is important to maintain good credit history, and most believe it would be “very” or “somewhat” easy to improve their credit score;

Consumers see the link between credit history and future bill paying but are less confident about the link between credit history and future insurance claims.

After reading that many studies have demonstrated its predictive power, most agree with using credit-based insurance scores to rate insurance, especially for drivers with good credit who could benefit.

If consumers “get it” when you share the data with them, perhaps policymakers and legislators can, too.

Consumer skepticism about the connection between credit history and future insurance claims appears to decline when the predictive power of credit-based insurance scores is explained to them, a recent study by the Insurance Research Council (IRC) suggests.

This is just one of the IRC’s encouraging findings. Others include:

Consumers are generally knowledgeable about credit, credit histories, and credit scores.

Nearly all believe it’s important to maintain good credit history, and most believe it would be easy to improve their credit score.

Among nearly all demographic groups, paying for auto insurance is not considered a burden for most households.

Concerns have been raised about the use of credit-based scores and certain other metrics in setting home and car insurance premium rates. Critics say it can lead to “proxy discrimination,” with people of color – who are more likely to have less-than-stellar credit histories – sometimes being charged more than their neighbors for the same coverage.

Confusion around insurance rating is understandable, given the complex models used to assess and price risk, and insurers are well aware of the history of unfair discrimination in financial services. To navigate this complexity, they hire teams of actuaries and data scientists to quantify and differentiate among a range of risk variables while avoiding unfair discrimination.

As the chart below shows, insurance claims tend to decline as credit scores improve. The fact that race frequently correlates with lower credit scores highlights societal problems that must be addressed through public policy, including financial literacy education. If anything, apparent racial disparities in insurance availability or affordability related to credit quality lend force to arguments for policy change.

In a study published last year, nearly half of respondents said financial literacy education would have helped them manage their money better through the pandemic. The study, which surveyed 1,047 U.S. adults, found that 21 percent felt insurance was the subject they understood least.

While the IRC study found non-Hispanic Black respondents were more likely than other groups to say their credit scores were below average and that it was important to improve their scores and would be easy to do so, they also were less likely to believe credit is a reliable indicator of paying bills or filing claims. Similarly, they were less likely to say it was okay to use credit history in lending, renting, or insurance settings.

All ethnic and racial groups, however, agreed that a person who has maintained good credit should benefit in the form of lower insurance rates.

“Many studies have shown that credit-based insurance scores are predictive of claims behavior,” the IRC report says, adding that recent studies using driving data from telematics devices “show a link between specific driving behaviors, such as hard braking, and variations in credit-based insurance scores.”

Any rating factor that can predict losses and claims helps insurers fairly price insurance by charging individual drivers rates that closely align with their risk. In the absence of these factors, less risky drivers would pay higher rates to subsidize the insurance of more risky drivers.