Average U.S. homeowners insurance premiums have increased at a rate that has outpaced household income from 2001 to 2021, according to a new report by the Insurance Research Council (IRC). In 2021 – the latest year for which data is available – homeowners spent an average of 1.99 percent of their income on homeowners insurance, up from 1.54 percent in 2001.

Affordability varies widely from state to state, and affordability rankings have fluctuated over time. In 2021, Utah was the most affordable state and Florida was the least affordable. Kansas, New York, and Washington, D.C., have demonstrated improvements from 2015 to 2021, and California, Montana, and Wyoming saw the greatest deterioration during the same period. Florida and Louisiana have consistently been the least-affordable states in the nation.

The analysis by IRC – like Triple-I, an affiliate of The Institutes – looks at homeowners insurance affordability at national and state levels and examines underlying cost drivers by state. It does not address affordability for specific demographic or geographic risk profiles. The report found that frequency and severity of natural disasters, economic conditions, rising construction costs, and litigation all significantly contributed to rising homeowners insurance costs.

“An understanding of what drives the cost of insurance is essential for consumers navigating the current insurance market,” said Dale Porfilio, FCAS, MAAA, IRC president and chief insurance officer for Triple-I. “Efforts to promote homeowner awareness and adoption of protective measures, strengthen state and local building codes, and encourage community resilience programs can all improve insurance affordability.”

Legislative reforms put in place in 2022 and early 2023 to address legal system abuse and assignment-of-benefits claim fraud in Florida are beginning to help the state’s property/casualty insurance market recover from its crisis of recent years, according to a new Triple-I Issues Brief.

Claims-related litigation is down, the “depopulation” of the state’s insurer of last resort continues apace, and underwriting profitability – while still in negative territory – has improved significantly. Insurers also benefited from a relatively mild 2023 Atlantic hurricane season and a meaningful increase in investment income, posting a net profit for the first time in seven years.

But it’s important to remember that the crisis wasn’t created overnight and that it will take time for the reforms and other developments to be reflected in policyholder premiums. Homeowners should not expect their rates to decline in 2024, despite the improved industry performance, although some regional insurers have filed for small decreases.

“Rates may moderate some compared to prior years,” said Mark Friedlander, Triple-I director of corporate communications, “but rising replacement costs – combined with expected higher reinsurance costs for the June 1 renewals – are going to continue to drive average premiums upward in 2024.”

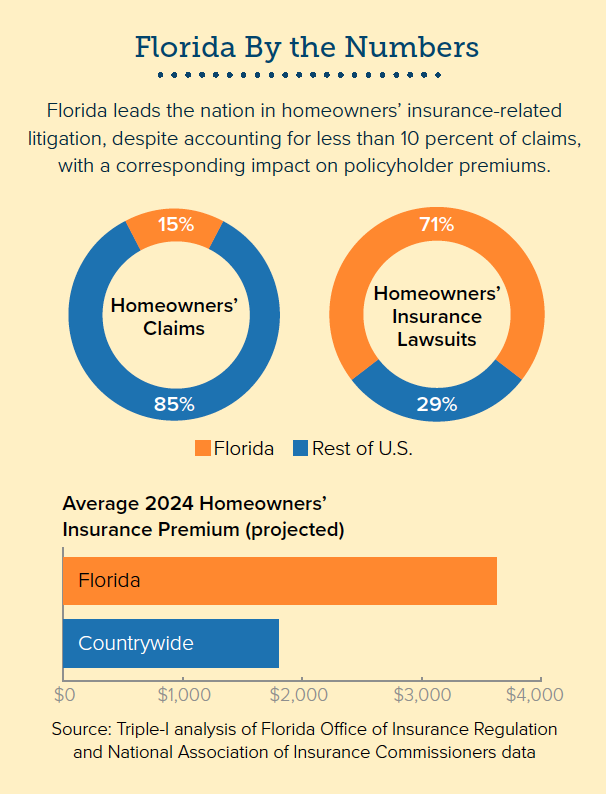

One factor keeping upward pressure on rates is fraud and legal system abuse. With only 15 percent of U.S. homeowners insurance claims, the state accounts for nearly 71 percent of the nation’s homeowners claim-related litigation, according to Florida’s Office of Insurance Regulation.

There are early signs that recent legislative reforms are beginning to bear fruit. In 2023, Florida’s defense and cost-containment expense (DCCE) ratio – a key measure of the impact of litigation – fell to 3.1, from 8.4 in 2022, according to S&P Global.

But the catastrophe-prone state faces a number of natural challenges, from a projected “extremely active” 2024 hurricane season to wildfires, flooding, and severe convective storms.

“Hurricanes get the most media attention,” Friedlander said, “but severe convective storms inflict comparable losses. And it only takes one bad hurricane season to wipe out the benefits of one or more mild years.”

Insurers paid $1.12 billion in dog-related injury claims in 2023, according to research by Triple-I and State Farm.

The total number of dog-bite and related claims was 19,062 in 2023 – an increase of more than 8 percent from 2022 and a rise of 110 percent over the past 10 years.

However, the average cost per claim decreased from $64,555 in 2022 to $58,545 in 2023. California, Florida, and Texas had the most claims.

“Education and training for owners and pets is key to keeping everyone safe and healthy,” said Janet Ruiz, director of strategic communications at Triple-I.

“As the largest property insurer in the country, State Farm is committed to educating people about pet-owner responsibility and how to safely interact with dogs,” added Heather Paul, media relations specialist at State Farm. “It is important to recognize that any dog, including ones that are in the home, can bite or cause injury.”

During Dog Bite Prevention Week (April 7 – 13), a coalition of veterinarians, animal behavior experts, and insurance representatives urge people to understand the risks dog bites pose to people and other pets and the steps required to prevent bites from happening.

“Dogs are not just pets; they are beloved members of our households, providing joy, companionship, and comfort in our lives,” said Dr. Rena Carlson, president of the American Veterinary Medical Association (AVMA). “Together, we can nurture the bonds we share with our dogs and ensure the safety of our families and communities.”

Tips to prevent dog bites

All dogs – even well-trained, gentle dogs – can bite when provoked, especially when eating, sleeping, or caring for puppies. Therefore, it is essential to keep both children and dogs safe by preventing bites wherever possible. The National Dog Bite Prevention Week Coalition provides the following tips:

Make sure your pet is healthy. Not all illnesses and injuries are obvious, and dogs are more likely to bite if they are sick or in pain. If you haven’t seen a veterinarian in a while, schedule an appointment for a checkup to discuss your dog’s physical and behavioral health.

Prioritize proper socialization: Socialization involves gently introducing your dog to a range of settings, people, and other animals, and ensuring these experiences are positive. Whether it’s quietly observing the bustle of a park, meeting new people in a controlled manner, or getting used to the sights and sounds of your neighborhood, each positive experience builds confidence. Remember, socialization is a lifelong journey, not just a puppy phase.

Take it slow. If your dog has been mainly interacting with your family since you brought them home, don’t rush out into crowded areas or dog parks. Try to expose your dogs to new situations slowly and for short periods of time, arrange for low-stress interactions, and look for behaviors that indicate your dog is comfortable and happy to remain in the situation.

Understand your dog’s needs and educate yourself in positive training techniques. Recognize your dog’s body language and advocate for them in all situations. This will give your dog much needed skills and help you navigate any challenges you might encounter.

Be responsible about approaching other people’s pets. Ask permission from the owner before approaching a dog and look for signs that the dog wants to interact with you. Sometimes dogs want to be left alone, and we need to recognize and respect that.

Make sure that you are walking your dog on a leash and recognize changes in your dog’s body language indicating they may not be comfortable.

Always monitor your dog’s activity, even when they are in the backyard at your own house, because they can be startled by something, get out of the yard and possibly injure someone or be injured themselves.

Join the discussion on Facebook Live April 11

To assist in these efforts, members of the National Dog Bite Prevention Week Coalition—which includes the AVMA, State Farm®, Triple I, and Victoria Stilwell Positively—will be hosting a Facebook Live event on Thursday, April 11, at 1 p.m. Eastern Time.

The event, moderated by certified animal behavior consultant and broadcaster Steve Dale, will discuss training tips to help prevent bites, how to safely socialize your dog after a period of isolation, and how to recognize the warning signs that a dog may bite. In addition, the coalition will be releasing the latest dog-related injury claims data. The panelists will also be answering questions submitted by the public during the event.

Colorado State University hurricane researchers predict an “extremely active” Atlantic hurricane season in their initial 2024 forecast. The team cites record-warm tropical and eastern subtropical Atlantic sea surface temperatures as a primary factor for their prediction of 11 hurricanes this year.

Led by senior research scientist and Triple-I non-resident scholar Phil Klotzbach, Ph.D, the CSU Tropical Meteorology Project forecasts 23 named storms, 11 hurricanes, and five major hurricanes during the 2024 season, which starts on June 1 and continues through Nov. 30. A typical Atlantic season has 14 named storms, seven hurricanes, and three major hurricanes.

The 2023 season produced 20 named storms and seven hurricanes. Three reached “major hurricane” intensity. Major hurricanes are defined as those with wind speeds reaching Category 3, 4 or 5 on the Saffir-Simpson Hurricane Wind Scale.

“We anticipate a well above-average probability for major hurricanes making landfall along the continental United States coastline and in the Caribbean this season,” Klotzbach said. “Current El Niño conditions are likely to transition to La Niña conditions this summer/fall, leading to hurricane-favorable wind-shear conditions. Sea surface temperatures in the eastern and central Atlantic are currently at record-warm levels and are anticipated to remain well above average for the upcoming hurricane season. A warmer-than-normal tropical Atlantic provides a more conducive dynamic and thermodynamic environment for hurricane formation and intensification.”

One hurricane and two tropical storms made continental U.S. landfalls last year. Category 3 Hurricane Idalia struck Florida’s Big Bend region near Keaton Beach on Aug. 30 with wind speeds of 115 mph. It was the third hurricane, and second major hurricane, to make a Florida landfall over the past two seasons. Idalia caused storm surge inundation of 7 to 12 feet and widespread flooding in Florida and throughout the Southeast.

“The widespread damage incurred from Idalia last year highlighted the importance of being financially protected from catastrophic losses – and that includes having adequate levels of property insurance and flood coverage,” said Triple-I CEO Sean Kevelighan. “Beyond Florida, we saw significant impacts from Idalia in southern Georgia and the Carolinas. All it takes is one storm to make it an active season for you and your family, so it is time to prepare as the 2024 Atlantic hurricane season’s start nears.”

With this forecast in mind, now is ideal time for homeowners and business owners to review their policies with an insurance professional to ensure they have the right amount and types of coverage. That includes exploring whether they need flood coverage, which is not part of a standard homeowners, condo, renters or business insurance policy.

Homeowners also can make their residences more resilient to windstorms and torrential rain by installing roof tie-downs and a good drainage system. Installation of a wind-rated garage door and storm shutters also boost a home’s resilience to a hurricane’s damaging winds and may generate savings on a homeowner’s insurance premium.

Private-passenger vehicles damaged or destroyed by either wind or flooding are covered under the optional comprehensive portion of an auto insurance policy.

Even as the Smokehouse Creek Fire – the largest wildfire ever to burn across Texas – was declared “nearly contained” this week, the Texas A&M Service warned that conditions are such that the remaining blazes could spread and even more might break out.

“Today, the fire environment will support the potential for multiple, high impact, large wildfires that are highly resistant to control” in the Texas Panhandle, the service said.

This year’s historic Texas fires – like the state’s 2021 anomalous winter storms, California’s recent flooding after years of drought, and a surge in insured losses due to severe convective storms across the United States – underscore the variability of climate-related perils and the need for insurers to be able to adapt their underwriting and pricing to reflect this dynamic environment. It also highlights the importance of using advanced data capabilities to help risk managers better understand the sources and behaviors of these events in order to predict and prevent losses.

For example, Whisker Labs – a company whose advanced sensor network helps monitor home fire perils, as well as tracking faults in the U.S. power grid – recorded about 50 such faults in Texas ahead of the Smokehouse Creek fires.

Bob Marshall, Whisker Labs founder and chief executive, told the Wall Street Journal that evidence suggests Xcel Energy’s equipment was not durable enough to withstand the kind of extreme weather the nation and world increasingly face. Xcel – a major utility with operations in Texas and other states — has acknowledged that its power lines and equipment “appear to have been involved in an ignition of the Smokehouse Creek fire.”

“We know from many recent wildfires that the consequences of poor grid resilience can be catastrophic,” said Marshall, noting that his company’s sensor network recorded similar malfunctions in Maui before last year’s deadly blaze that ripped across the town of Lahaina.

Role of government

Government has a critical role to play in addressing the risk crisis. Modernizing building and land-use codes; revising statutes that facilitate fraud and legal system abuse that drive up claim costs; investing in infrastructure to reduce costly damage related to storms – these and other avenues exist for state and federal government to aid disaster mitigation and resilience.

Too often, however, the public discussion frames the current situation as an “insurance crisis” – confusing cause with effect. Legislators, spurred by calls from their constituents for lower premiums, often propose measures that would tend to worsen the problem because they fail to reflect the importance of accurately valuing risk when pricing coverage.

The federal “reinsurance” proposal put forth in January by U.S. Rep. Adam Schiff of California is a case in point. If enacted, it would dismantle the National Flood Insurance Program (NFIP) and create a “catastrophic property loss reinsurance program” that, among other things, would set coverage thresholds and dictate rating factors based on input from a board in which the insurance industry is only nominally represented.

U.S. Rep. Maxine Waters (also of California) has proposed a Wildfire Insurance Coverage Study Act to research issues around insurance availability and affordability in wildfire-prone communities. During House Financial Services Committee deliberations, Waters compared current challenges in these communities to conditions related to flood risk that led to the establishment of NFIP in 1968. She said there is a precedent for the federal government to step in when there is a “private market failure.”

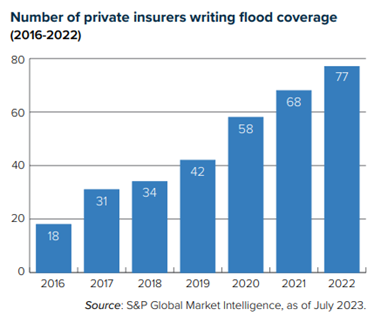

However, flood risk in 1968 and wildfire risk in 2024 could not be more different. Before FEMA established the NFIP, private insurers were generally unwilling to underwrite flood risk because the peril was considered too unpredictable. The rise of sophisticated computer modeling has since given private insurers much greater confidence covering flood (see chart).

In California, some insurers have begun rethinking their appetite for writing homeowners insurance – not because wildfire losses make properties in the state uninsurable but because policy and regulatory decisions made over 30 years ago have made it hard to write the coverage profitably. Specifically, Proposition 103 and its regulatory implementation have blocked the use of modeling to inform underwriting and pricing and restricted insurers’ ability to incorporate reinsurance costs into their premium pricing.

California’s Insurance Commissioner Ricardo Lara last year announced a Sustainable Insurance Strategy for the state that includes allowing insurers to use forward-looking risk models that prioritize wildfire safety and mitigation and include reinsurance costs into their pricing. It is reasonable to expect that Lara’s modernization plan will lead to insurers increasing their business in the state.

It’s understandable that California legislators are eager to act on climate risk, given their long history with drought, fire, landslides and more recent experience with flooding due to “atmospheric rivers.” But it’s important that any such measures be well thought out and not exacerbate existing problems.

Partners in resilience

Insurers have been addressing climate-related risks for decades, using advanced data and analytical tools to inform underwriting and pricing to ensure sufficient funds exist to pay claims. They also have a natural stake in predicting and preventing losses, rather than just continuing to assess and pay for mounting claims.

As such, they are ideal partners for businesses, communities, governments, and nonprofits – anyone with a stake in climate risk and resilience. Triple-I is engaged in numerous projects aimed at uniting diverse parties in this effort. If you represent an organization that is working to address the risk crisis and your efforts would benefit from involvement with the insurance industry, we’d love to hear from you. Please contact us with a brief description of your work and how the insurance industry might help.

Even as California moves to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing, the state’s risk profile continues to evolve in ways that underscore the importance of risk-based insurance pricing and investment in mitigation and resilience.

Triple-I’s latest “State of the Risk” Issues Brief discusses this changing risk environment and the impact of Proposition 103 – a three-decades-old measure that has made it hard for insurers to profitably write coverage in the state. In a dynamically evolving risk environment that includes earthquakes, drought, wildfire, landslides, and — in recent years, due to “atmospheric rivers” — damaging floods, Proposition 103 has prevented insurers from using the most current data and advanced modeling technologies. Instead, it has required them to price coverage based on historical data alone.

It also has restricted accurate underwriting and pricing by not allowing insurers to incorporate the cost of reinsurance into their pricing. Insurers use reinsurance to maximize their capacity to write coverage, and reinsurance rates have been rising for many of the same reasons as primary insurance rates. If insurers can’t reflect reinsurance costs in their pricing – particularly in catastrophe-prone areas – they must pay for these costs from policyholder surplus, reduce their market share in the state, or do both.

Proposition 103 also has impeded premium rate changes by allowing consumer advocacy groups to intervene in the rate-approval process. This makes it hard to respond quickly to changing market conditions, resulting in approval delays and rates that don’t accurately reflect current (let alone future) risk. It also drives up legal and administrative costs.

This has led, in some cases, to insurers deciding to limit or reduce their business in the state. With fewer private insurance options available, more Californians are resorting to the state’s FAIR Plan, which offers less coverage for a higher premium.

This isn’t a tenable situation.

In September 2023, California Insurance Commissioner Ricardo Lara announced a Sustainable Insurance Strategy for the state that includes allowing insurers to use forward-looking risk models that prioritize wildfire safety and mitigation and include reinsurance costs into their premium pricing. In exchange, insurers must cover homeowners in wildfire-prone parts of the state at 85 percent of their statewide coverage.

Issues around property insurance affordability are not confined to California. They’ve been a long time in the making, and they won’t be resolved overnight.

“Any sustainable solutions will have to rest on actuarially sound underwriting and pricing principles,” the Triple-I brief says. “Unfortunately, too often, the public discourse frames the risk crisis as an `insurance crisis’ – conflating cause with effect. Legislators, spurred by calls from their constituents for lower insurance premiums, often propose measures that would tend to worsen the problem because these proposals generally fail to reflect the importance of accurately valuing risk when pricing coverage.”

California’s Proposition 103 and the federal flood insurance program prior to its Risk Rating 2.0 reforms are just two examples, according to Triple-I.

The increasing frequency and severity of claims costs beyond insurer expectations continue to threaten insurance coverage and affordability. Triple-I’s latest Issue Brief, Legal System Abuse – State of the Risk describes how trends in claims litigation can drive social inflation, leading to higher insurance premiums for policyholders and losses for insurers.

Key Takeaways

Insured losses continue to exceed expectations and surpass inflation, notably impacting coverage affordability and availability in Florida and Louisiana.

In promoting the term “legal system abuse”, Triple-I seeks to capture how litigation and related systemic trends amplify social inflation.

Progress has been made toward increased awareness about the risks of third-party litigation funding (TPLF), but more work is needed.

What we mean when we talk about legal system abuse

Legal system abuse occurs when policyholders, plaintiff attorneys, or other third parties use fraudulent or unnecessary tactics in pursuing an insurance claim payout, increasing the time and cost of settling insurance claims. These actions can include illegal maneuvers, such as claims inflation and frivolous or outright fraudulent claims. Unscrupulous contractors, for example, seek to profit from Assignment of Benefits (AOBs) by overstating repair costs and then filing lawsuits against the insurer – sometimes even without the homeowner’s knowledge. Filing a lawsuit to reap an outsized payout when it’s evident the claims process will likely provide a fair, reasonable, and timely claim settlement can also be considered legal system abuse.

The latest brief provides a round-up of several studies Triple-I and other organizations conducted on elements of these litigation trends. The report, “Impact of Increasing Inflation on Personal and Commercial Auto Liability Insurance,” describes the $96 billion to $105 billion increase in combined claim payouts for U.S. personal and commercial auto insurer liability. The Insurance Research Council highlighted the dire lack of affordability for personal auto and homeowners insurance coverage in Louisiana, along with the state’s exceptionally high claim litigation rates.

Readers will also find an update on the discussion of legal industry trends associated with increased claims litigation. The lack of transparency around TPLF arrangements and the fear of outside influence on cases are attracting the attention of legislators at the state and federal levels. The brief also describes how some law firms may use TPLF resources to encourage large windfall-seeking lawsuits instead of speedy and fair claims litigation. Research findings suggest that consumers have become aware of how ubiquitous attorney ads can influence the frequency of lawsuits, increasing claims costs.

Florida: a case study in the consequences of excessive litigation

While several states, such as California, Colorado, and Louisiana, are experiencing a drastic rise in the cost of homeowners’ insurance, this brief discusses Florida. Property insurance premiums there rank the highest in the nation. Several insurers facing insurmountable losses have stopped writing new policies or left the state in the last few years. In some areas, residents are leaving, too, because of skyrocketing premiums.

Excessive claims litigation isn’t a new issue for insurers, but it can work with other elements to shift loss ratios and disrupt forecasts, rendering cost management more challenging. In Florida, factors such as the rise in home values and frequency of extreme weather events play a significant role, along with the challenges homeowners face in the aftermath: soaring construction costs, supply chain bottlenecks, and new building codes. However, Florida also leads the nation in litigating property claims. While 15 percent of all homeowners claims in the nation originate in the state, Floridians file 71 percent of homeowners insurance lawsuits.

In Florida and elsewhere, increasing time to settle a claim puts a financial strain on insurers, which is passed on to policyholders in the form of higher premiums. Legal system abuse activities are difficult (if not impossible) to forecast and mitigate, hampering insurers’ ability to remain in the market. Therefore, legal system abuse could be one of the biggest underlying drivers of social inflation. Without preventive measures, such as policy intervention and increased policyholder awareness, coverage affordability and availability is at risk.

Triple-I remains committed to advancing the conversation and exploring actionable strategies with all stakeholders. Learn more about legal system abuse and its components, such as third-party litigation funding by following our blog and checking out our social inflation knowledge hub.

Homes with more modern roofs were able to avoid significant damage from Hurricane Ian, compared with those with older roofs, according to a recent study by the Federal Emergency Management Agency (FEMA).

Of the 200 homes surveyed, 90 percent with roofs installed before 2015 had roof damage, as opposed to 28 percent for those installed after 2015, when Florida imposed new ordinances regarding how roofs are attached to houses and how waterproof they need to be. Indeed, when Hurricane Ian made landfall at Cayo Costa, a barrier island in Lee County, Fla., on Sept. 28, 2022, it damaged 52,514 homes and other structures in the area, causing an estimated $55 billion in insured losses in 2024 dollars.

Some of this damage, according to the data, could have been mitigated by updated roofs.

History tells the same story

After the devastation of Hurricane Andrew in 1992, Florida took the initiative to develop innovative plans to prevent hurricane damage. These changes further came into effect in 2002, with a new focus on roofing. However, there were inconsistencies in the quality of the roofing.

“The 1970s-era homes performed better than some of the post-2002 new building code homes because of the sealed roof deck,” Leslie Chapman-Henderson, president of the Federal Alliance for Safe Homes, told The Miami Herald. “It was a nominal cost (to reinforce the roof) and a simple thing to do, but it made a huge difference.”

Now, with a renewed focus on metal sheet roofs—which bear the brunt of storms more resiliently than asphalt shingle roofs—FEMA’s data could drastically change the way in which homes are built, and how insurers are responding to fraudulent claims.

Insurance scams set progress back

Insurers are forced to raise the price of coverage in hurricane-prone areas in Florida because of a rash of schemes to deliberately damage roofs to qualify them for insurance claims, a persisting trend.

“Fraud drives insurance rates up and harms all Florida policyholders,” Citizens Property Insurance CEO Tim Cerio said. Still, implementing the changes suggested by the FEMA study may help alleviate some of the concerns posed by insurers—and help homeowners.

“When you’re looking at a home and evaluating its ability to survive a hurricane, the health of the roof is the first question to ask,” said Chapman-Henderson. “It not only increases your performance in the hurricane itself, but in the current environment it can help save you money on your insurance.”

According to a recent Chubb survey of 800 high-net-worth individuals in the United States and Canada, 92 percent are concerned about the size of a verdict against them if they were a defendant in a liability case – yet only 36 percent have excess liability insurance.

When it comes to liability, Chubb says respondents are most worried about auto accidents, allegations of assault or harassment, and someone working in their home getting hurt. Damage awards are rising dramatically for a number of reasons, according to Laila Brabander, head of North American personal lines claims for Chubb.

“Economic damages historically were based on factors such as the extent of an injury and resultant medical expenses or past and future loss of income,” she said. “But we are seeing a rise in non-economic damages, such as pain and suffering and post-traumatic stress disorder, that overshadow actual economic losses.”

Brabander described a case in which a client at a yoga studio fell onto the person next to her and was sued by the injured party for pain and suffering.

“The same plaintiffs’ tactics to encourage large verdicts in commercial trucking, auto liability, product liability and medical malpractice suits are now being utilized to push for larger jury awards against our high-net-worth clients,” Brabander said.

Another factor driving up the cost of settlements is the third-party litigation funding, in which firms provide funding to plaintiffs and their lawyers in exchange for a percentage of the settlement. These private-equity firms began in the commercial space and are now funding lawsuits against individuals and their insurers.

High-net-worth people also are deeply concerned about the threats posed to their homes by extreme weather and climate-related events. Much of this concern may be due to increased development in coastal areas vulnerable to tropical storms and flooding and in the wildland-urban interface – areas in which development places property into proximity with fire-prone wilderness (see links below).

Chubb’s findings are based on a survey of 800 wealthy individuals in the United States (650 respondents) and Canada (150 respondents). Respondents had investable assets of at least $500,000, with the majority reporting assets of $1.5 million to $50 million and 12 percent reporting assets of more than $50 million.

Louisiana continues to be the least affordable state for personal auto and homeowners insurance, according to a new report by the Insurance Research Council (IRC).

The average annual expenditure for auto insurance in Louisiana was $1,495 In 2020, more than 40 percent above the national average, the report finds. These costs account for 2.93 percent of the median household income in the state, rendering it the least affordable.

Louisianans also pay significantly more for homeowners coverage compared to the national average, with an average annual expenditure of $1,965. These are among the highest rates in the country, representing 3.84 percent of the median household income in the state – 55 percent above the national average.

“The state has faced multiple major weather events, with extensive litigation following each natural disaster,” the report finds. “Rising auto-repair and construction costs, as well as the state’s relatively low household income, have compounded these issues.”

Personal auto cost drivers include:

Accident frequency: The number of property damage liability claims per 100 insured vehicles in Louisiana is 16 percent higher than the countrywide average.

Injury claim relative frequency: Louisianians show a greater propensity to file injury claims once an accident has occurred, with a relative claim frequency almost twice the national average.

Medical utilization: Louisiana auto claimants are more likely than those in other states to receive diagnostic procedures, such as magnetic resonance imaging (MRI).

Attorney involvement: Louisiana claimants are more likely than those in other states to hire attorneys. Attorney involvement has been associated with higher claim costs and longer settlement times.

Claim litigation: The rate of litigation in personal auto claims in Louisiana is more than twice the national average. This rate is the second-highest in the country, surpassed only by Florida.

Homeowners cost drivers include:

Claim frequency, catastrophe claims: The number of catastrophe claims paid for every 100 homes insured for the entire year in Louisiana is almost six times higher than the national average.

Claim severity, catastrophe claims: In the hurricane-prone region, Louisianians are second only to Floridians in the amount paid for the average homeowners insurance claim. Louisiana is 12 percent higher than the national average.

Natural-hazard risk, weather: Louisiana’s exposure to building damage from weather hazards is second only to Florida’s and is dramatically higher than other states.

Claim litigation: Claims in Louisiana were 12 times more likely to involve litigation, compared with states other than Florida.

These issues have led to the insolvency of several carriers and the departure of key insurance providers from the market. Many remaining insurers have chosen to limit coverage and raise premiums.

Louisiana has tried to address these coverage gaps through incentive programs for private carriers and a greater reliance on the state-run insurer Louisiana Citizens Property Insurance Corporation, the last-resort insurance. However, Louisiana Citizens Property Insurance Corporation can be expensive, making it unaffordable for many and especially for the state’s most vulnerable residents.

These hardships have also influenced a population decline in Louisiana, as individuals and businesses are uprooting and seeking improved affordability elsewhere. Louisiana’s population declined by almost 1 percent in 2022, accounting for nearly 39,000 people, according to a new Census estimate.