Tariffs and threats of tariffs have been roiling financial markets since January. Property and casualty insurers are no less concerned, as the cost of repairing and replacing damaged property is a driver of claim costs and, ultimately, policyholder premiums.

Triple-I Chief Economist and Data Scientist Dr. Michel Léonard recently sat down to explain the implications of tariffs and trade barriers for insurers and what economic considerations concern industry decisionmakers.

While property and casualty insurers write many kinds of coverage, the lines Léonard primarily discussed were homeowners and personal and commercial auto – “lines that have a physical emphasis on repair, rebuild, and replace.”

Lumber from Canada; cars, trucks, and parts from Canada and Mexico; and garments, furnishings, and technology from Asia all come into play when considering the prospective impacts of tariffs on replacement costs, Léonard said.

“When we’re focusing specifically on China,” he said, “we’re looking primarily at farm equipment and alternative-energy components.”

Uncertainty around tariffs – particularly in recent weeks, as tariffs on Mexico and Canada have been imposed and “paused” – makes analysis even more difficult.

“Much depends on how much clarity there is, how much communication from the policymakers, from the administration and from the legislature,” Léonard said. It’s also important to remember that impacts can last well beyond their implementation and withdrawal.

During the first Trump Administration, tariffs on soft commodities, beef, grain, and so forth had impacts for several years afterwards.

“Those tariffs were fairly short lived,” Léonard said, “but for two to three years afterward farmers were uncomfortable investing in equipment at the same pace, and that reduced farmowners’ insurance growth.”

Regardless of how the current discussions around tariffs play out, the Trump Administration has signaled a decided shift in policy toward greater protectionism. As a result, Léonard said, “We should expect a repositioning in our understanding of our replacement costs and underlying growth forecast for the next 12 months, at a minimum.”

He projects a period of “most likely 24 to 36 months” in which growth will be slower and inflation – including replacement costs for the P&C industry – will be higher.

Florida’s legislative reforms to address claim fraud and legal system abuse are stabilizing the state’s property/casualty insurance market, according to the latest Triple-I Issues Brief.

Claims-related litigation has significantly declined over the past two years, and premium averages are nearly flat, with several insurers requesting rate decreases from the state’s insurance regulator. In addition, the brief says, the number of insurers writing business in the state has rebounded after a multi-year exodus. This competition from the private market has allowed policyholders to leave Citizens Property Insurance Corp. – the state-run insurer of last resort – to obtain coverage at previously unavailable rates from a much healthier private market.

According to the state’s Office of Insurance Regulation (OIR), Florida in 2022 accounted for nearly 71 percent of the nation’s homeowners claim-related litigation, despite representing only 15 percent of homeowners insurance claims. The same year – before Hurricane Ian made landfall in Florida – six insurers in the state declared insolvency, primarily due to economic pressures from legal system abuse. Based on insured losses, Ian became the second-most costly U.S. hurricane on record, due in large part to extraordinary litigation costs for disputed claims.

The Legislature responded to the growing crisis by passing several pieces of insurance reform that, among other things, eliminated one-way attorney fees and assignment of benefits (AOB) for property insurance claims and prohibited misleading legal service ads and the misuse of consumer health information for legal services.

Premium rate growth slowing

The impact of the 2022 and 2023 reforms can be seen in premium rate changes, particularly with respect to homeowners insurance. Homeowners rates in Florida grew at a much slower rate in 2024, even as rate growth remained strong nationally. Growth in personal auto insurance premium rates in Florida has slowed since the repeal of AOB and one-way attorney fees, but the trend also is consistent with nationwide experience.

“There are a lot of factors involved in insurance rates, and Florida’s property and auto markets are challenging,” Florida Governor Ron DeSantis said in February, “but…data suggests that, in 2024, Florida had the lowest average homeowners’ premium increases in the nation, and the overall market has stabilized, with 11 new companies having entered the market over the past two years.”

Among the top 10 national insurers writing homeowners insurance in Florida, 60 percent have expanded their business over the past year, and 40 percent of all insurers operating in the state filed for rate decreases in 2024, according to Florida Insurance Commissioner Michael Yaworksy.

The cost of reinsurance also continues to decrease for Florida carriers.

“In 2024, most companies paid less for reinsurance than they did in 2023,” according to the OIR website. “The average risk-adjusted cost for 2024 was -0.7 percent, a large reduction from last year’s change of 27 percent increase from the prior year.”

Reinsurance costs are factored into premium rates, so this is another reason Florida now has the lowest average rate filings in the United States in 2024, according to S&P Global Marketplace.

Insurance affordability in Georgia is dwindling as claim frequency and insurer costs soar, according to the latest issue brief from Insurance Information Institute (Triple-I), Trends and Insights: Georgia Insurance Affordability.

Given the state’s below-average income vs. above-average insurance expenditures, Georgia ranks 42nd on the list of affordable states forhomeowners insurance and 47th (plummeting from the 2006 high of 27th) forpersonal auto affordability, according to reports by the Insurance Research Council. This brief provides an overview of how several factors, including skyrocketing costs from litigation, pose risks to coverage affordability, availability, and other potential economic outcomes for Georgia residents. Tort reform is discussed as a legislative solution to the challenge of legal system abuse – excessive policyholder or plaintiff attorney practices that increase costs and time to settle insurance claims.

The Georgia insurance market grapples with multiple risk factors

From 1980–2024, Georgia was impacted by134 confirmed weather/climate disaster events in which losses exceeded $1 billion each. At least 38 of those events happened in the last five years, with 14 in 2023. Homeowners in Georgia’s most climate-risk-vulnerable counties, such as the coastal and most southern parts of the state, can face double-digit premium hikes or nonrenewals. Also, data indicates the rate of underinsured motorists in Georgia is twice as high as the national average, and the rate of uninsured motorists is 25 percent higher. Injury claim severity in the state is slightly higher than in the rest of the country.

Data indicates that litigation costs have become a pervasive concern for risk management.

Rising claim frequency and litigation costs put coverage affordability and availability at risk. For example, the IRC findings across personal auto lines show a dual trend in Georgia of increased claims and litigation. Property damage liability claims per 100 insured vehicles are 15 percent higher, and relative body injury claims frequency is 60 percent higher. According to IRC, the rate for private passenger litigation in Georgia is nearly three times that in the median state.

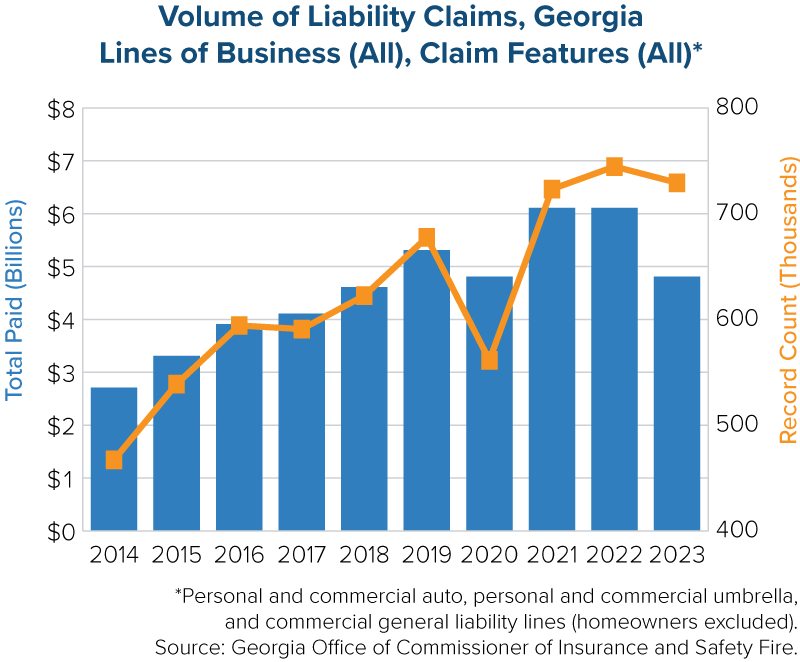

The Georgia Office of Commissioner of Insurance and Safety Fire (“OCI”) reviewed all lines across personal and commercial auto, personal and commercial umbrella, and commercial general liability (homeowners liability was excluded). The five-year average count for liability claims increased 24.9 percent (2014 – 2018 at 583,756 vs. 2019-2023 at 729,191). A rising percentage of claims with payment are full-limit claims, and the OCI analysis indicates litigation is driving that increase. While costs rose for both litigated and non-litigated claims, the number of claims with legal involvement dominated paid indemnity for most lines of business, and litigated claims comprised a growing portion of the total paid indemnity.

Attorneys appear to have revved up their mining for lawsuits in Georgia. Law firms spent $160 million on advertising in Georgia, according to preliminary data from the American Tort Reform Association (ATRA). Outdoor ads for lawsuits increased by 119 percent in GA during that time. It might not be a surprise then to see that the Georgia OCI report shows legal (attorney involved) claims dominated Personal Auto claims for Bodily Injury, comprising 62 percent of claims and 86 percent of total indemnity paid for closed claims in Accident Year 2023. A review of losses of $1 million or more by accident year that have closed during the 2014 to 2023 period shows that each accident year cohort surpasses the count from the previous accident years.

Recently introduced state tort reform legislation may help to stabilize insurance costs.

Analysts estimate that litigation costs Georgia residents $880 million annually, or an average of $1,415 per resident. Sean Kevelighan, Triple-I CEO, says “understanding how these trends drive up costs and identifying policy levers for tort reform legislation can ultimately bring positive outcomes for Georgia’s economy and its consumers and business owners.”

As part of our commitment to educating stakeholders, Triple-I has launched a multi-faceted campaign to raise awareness of the mounting costs oflegal system abuse in Georgia and other states. We invite you to view thevideo statement by our CEO Sean Kevelighan, interviews capturing the opinions of consumers about legal system abuse, and read the full issue brief, Trends and Insights: Georgia Insurance Affordability.

Reforms put in place in 2024 are a positive move toward repairing Louisiana’s insurance market, which has long suffered from excessive claims litigation and attorney involvement that drive up costs and, ultimately, premium rates.

But more work is needed, Triple-I says in its latest Issues Brief.

Research by the Insurance Research Council (IRC) – like Triple-I, an affiliate of The Institutes – shows Louisiana to be among the least affordable states for both personal auto and homeowners insurance.

In 2022, the average annual personal auto premium expenditure per vehicle in Louisiana was $1,588, which is nearly 40 percent above the national average and nearly double that of the lowest-cost Southern state of North Carolina ($840), IRC said. Louisianans also pay significantly more for homeowners coverage than the rest of the nation, with an average annual expenditure of $2,178, representing 3.81 percent of the median household income in the state – 54 percent above the national average.

Louisiana’s low average personal income relative to the rest of the nation contributes to its personal auto insurance affordability challenges, which are exacerbated by its litigation environment.

Louisiana Insurance Commissioner Tim Temple has championed a series of legislative changes that he has said will encourage insurers to return to Louisiana, especially in hurricane-prone areas.

“There are fewer companies willing to write property insurance in Louisiana, and that’s a lot of what our legislation is designed to do,” Temple said. “To help promote Louisiana and change the marketplace so that companies feel like they are going to be treated fairly.”

In June 2024, Gov. Landry signed into law S.B. 355, which puts limitations on third-party litigation funding – a practice in which investors, with no stake in claims apart from potentially lucrative settlements, fund lawsuits aimed at entities perceived as having deep pockets. Third-party litigation funding drives up claims costs and delays settlements, which end up being passed along to consumers in the form of higher premiums.

This progress was undermined when Landry vetoed H.B. 423, which would have reformed the state’s “collateral source doctrine” that allows civil juries to have access to the “sticker price” of medical bills and the amount actually paid by the insurance company.

“In addition to creating more transparency and helping lower insurance rates, this bill would have brought more fairness and balance to our civil justice system,” said Lana Venable, director of Louisiana Lawsuit Abuse Watch in a statement regarding the veto. “Lawsuit abuse does not discriminate – everyone pays the price when the resulting costs are passed down to all of us.”

Continued reforms in 2025 will be necessary to help prevent legal system abuse and promote a more competitive insurance market that leads to greater affordability for consumers, Triple-I says in its brief.

Maintaining human centricity in an increasingly digitized world was a focus of discussion for many participants at Triple-I’s 2024 Joint Industry Forum (JIF) – particularly during the “Fireside Chat,” featuring Katherine Horowitz, executive vice president and head of business units for The Institutes, and Casey Kempton, president of personal lines at Nationwide.

As generative AI and other technological innovations help streamline the insurance value chain, such processes must continue to align with the human needs intrinsic to insurance, Kempton stressed.

“Insurance is a human business,” Kempton said. “The moment of a claim – of whatever tragedy or inconvenience that has happened – is a human moment. Theres’s emotion involved in that. I don’t expect any robot or machine to take on that experience end-to-end and be able to deliver what folks need in that moment, which is comfort and assurance.”

Rather, new technology presents opportunities to facilitate more proactive and individualized risk management than ever before, while also enabling employees to do what this industry does best: engaging with other people.

Role of telematics

Usage-based insurance, for instance, allows insurers to tailor auto rates based on the policyholder’s driving behavior, tracked by telematics. By providing feedback to encourage safer driving habits, telematics has been found to lower risk and reduce auto premiums, empowering consumers to recognize their direct influence on their insurance rates, Kempton said.

Similarly, advanced smart devices – such as those developed by Whisker Labs (Ting) and Ondo InsurTech (LeakBot) – continuously detect conditions that could lead to damage within a home and notify homeowners before losses occur. The success of these devices has spurred numerous insurance carriers, including Nationwide, to pay for and distribute them to customers.

“Supporting the delivery of these technologies to our customers is critical,” Kempton explained, as is “making the cost of entry accessible.”

Words matter

Kempton noted that mitigative insurance solutions further serve to alleviate widespread public distrust in the industry, which has become “sullied” under misconceptions of insurance as merely a commodity.

Industry language fixated on costs, rather than consumer needs, is partly to blame.

“In insurance, we talk about ‘mitigating loss,’” Kempton said. “That’s how it feels from our perspective – we see claims as losses – but let’s turn that into, ‘how can [insurers] better engender peace of mind and protection for consumers?’”

Louisiana Insurance Commissioner Tim Temple later echoed this sentiment during a panel on legal system abuse, discussing how “billboard attorney” advertising has appropriated the consumer confidence once placed in insurance carriers.

“I remember when insurance companies advertised dependability and stability,” Temple explained. “Now it’s lizards, birds, and jingles… And then you see the attorneys, and they talk about how you’re going to be safe and secure with their service. That’s [the insurance company’s] job.”

Fueled by such advertising, excessive claims-related litigation has cost residents of Louisiana and other states across the country thousands of dollars in “tort taxes” every year, contributing to rising premium rates as insurers struggle to predict and mitigate protracted claims disputes. Lack of transparency around third-party litigation funding (TPLF), in which investors fund lawsuits in exchange for a percentage of any settlement, exacerbates this financial strain.

“If we can avoid these additional expenses and the severity attached to nuclear verdicts, it benefits all consumers,” Kempton said. Recent reforms in Florida – once the poster child for legal system abuse – indicate as much.

But reform necessarily hinges on collaboration between all stakeholders, which is unattainable without resolving “the consumer mindset we’ve inadvertently created around what the value of insurance is,” Kempton said. Updated legal regulations are equally important to ending legal system abuse as reasserting the key values of insurers – to protect and care for policyholders.

While the perception of overall severe weather risks varies significantly by region, 65 percent of the participants nationwide believed their home is at risk from thunderstorms, according to the new report,Catastrophic Weather Events and Mitigation: Survey of Homeowners by the Insurance Research Council (IRC), a division of The Institutes.

Overall, this and other key report findings revolve around the value of proactive measures for effective preparedness and mitigation strategies to address the increasing risks posed by severe weather events and the need for collaboration between homeowners, insurers, and governments to enhance resilience against natural disasters. The report highlights how interactions with contractors, public adjusters, and attorney involvement can significantly impact recovery timelines, claims frequency, and insurance costs.

The online survey of over 1,500 respondents investigates U.S. public opinions and homeowners’ experiences with severe weather, offering insights on U.S. regional perceptions of future risks, preparedness levels, attitudes toward mitigation strategies, post-storm solicitations by contractors and service providers, and homeowners; opinions on the roles of insurance and government in managing severe weather-related risks.

Disaster anticipation and preparedness

Eighty percent of the responding homeowners expressed confidence in their preparedness for severe weather events. Homeowners participating in the survey who experienced severe weather events in the past five years were significantly more likely to believe that a similar event would occur within the next five years.

Only 30 percent are aware of premium savings for implementing mitigation measures. However, Eighty-three percent of participants said they would consider implementing catastrophe preparedness and mitigation measures if it meant receiving savings on their insurance premiums, but most of those required premium savings large enough to offset the costs of these measures. Seventy percent revealed they would be willing to pay higher premiums for better protection against future severe weather events. Overall, 80 percent agreed that the government should provide emergency assistance.

Weather Experiences

Nearly half of the participants reported damage to their homes after a severe weather event. About 34 percent said they filed an insurance claim after experiencing damage to their homes, and 45 percent said they hired a contractor. Sixty-four percent of respondents reported receiving solicitation from contractors after a severe weather event. Also, 68 percent of participants who filed claims said they used Assignment of Benefits (AOB) to authorize the repair company to bill the insurance carrier. Fifty-four percent reported hiring public adjusters to handle repairs and insurance claims.

For context, each year, there are about100,000 thunderstorms in the U.S., about 10% of which reach severe levels, according to the National Oceanic and Atmospheric Administration (NOAA). Storms are classified as severe “when containing one or more of the following: hail one inch or greater, winds gusting more than 50 knots (57.5 mph), or a tornado.” Data analysis from Munich Re indicates that by just thefirst six months of 2024, severe thunderstorms in the U.S. caused $45 billion in losses, $34 billion of which were insured, making 2024 the fourth-costliest thunderstorm year on record.

Between 1980 and 2024 (as of November 1), the U.S. experienced 400 weather and climate disasters, with overall damage costs for each reaching or exceeding $1 billion. The cumulative cost for these 400 events exceeds $2.78 trillion. The yearly average for events during this period is 8.5, with the annual average for 2019–2023 being 20.4. However, the U.S. experienced 28 events in 2023 and 27 events in 2024costing at least 1 billion dollars each.

Stakeholder Takeaways

While climate risk plays a significant role in the number and severity of extreme weather events that cause insurance industry losses, Triple-I has kept an eye on the impact of the unpredictable confluence of attorney fee mechanisms, assignment of benefits (AOB), and other practices that can amplify claim costs. For example, involving third parties has the propensity to introduce the risk of claim inflation and may compound issues for the policyholder.

When property owners are compelled to share their claim value (typically 30 – 40 percent to attorneys and 10 – 30 percent to public adjusters), this, in turn, may impact the final amount they feel necessary to settle a claim. Previous IRC research suggests thatattorney involvement can increase claims costs and the time needed to resolve them (again, even while reducing value for claimants). Additionally, after a severe weather event, some exploitative actors can aggressively leverage assignment of benefits (AOBs) agreements to bill or even sue the insurer without further input from the policyholder. Policyholders lose the ability to work through and settle the claim efficiently.

Triple-I and key insurance industry stakeholders define legal system abuse as policyholder or plaintiff attorney practices that increase costs and time to settle insurance claims, including situations when a disputed claim could have been fairly resolved without judicial intervention. Without measures such as regulatory intervention and increased policyholder awareness, coverage affordability and availability are at risk. Insurers, policyholders, and policymakers can take actionable steps to address the legal system’s impact on the cost of insurance. Triple-Iremains committed to advancing the conversation and exploring actionable strategies with all stakeholders.

Natural catastrophe perils’ rising frequency and severity may be impossible to fully abate, but Nationwide Property & Casualty Insurance Co. President and CEO Mark Berven believes modern building codes could dramatically reduce their costly destructiveness.

In a recent article for PropertyCasualty360, Berven wrote that inconsistent building codes create alarming safety disparities from state to state and that improved codes are essential to reducing risk and post-disaster recovery costs.

“Extreme weather events like heat waves, large storms, landslides and more are becoming more frequent and intense,” Berven writes. “The U.S. has already experienced at least 24 confirmed weather disaster events through October with losses exceeding $1 billion each.”

“Building Codes Save” — a landmark report by the Federal Emergency Management Agency (FEMA) –found that universal enforcement of modern building codes could prevent more than $600 billion in disaster losses by 2060. In states where stricter codes have been implemented, the report says, billion-dollar savings already have been realized.

Virginia and Florida, for example, have long-modeled robust building code systems, leading both to consistently top code adoption rankings – especially after the latter saved an estimated $1 billion to $3 billion in averted damages during Hurricane Ian through its modern Florida Building Code.

By contrast, fewer than one-third of hazard-prone jurisdictions have adopted modernized building codes, and some states – such as Delaware and Alabama – lack mandatory statewide building code systems entirely.

Perceived cost an obstacle

Barriers to adoption include the perceived expenses of enforcement. Conforming existing structures to the same standards as new buildings can be costly, as can rebuilding communities in non-hazardous areas. Navigating these concerns in tandem with an ongoing affordable housing shortage will require a coordinated effort on local, state, and federal levels.

But as the annual average of billion-dollar disasters in the U.S. trends upward, improving building codes must take precedence for policymakers at every level of government, Berven explained, adding that the research organization Insurance Institute for Business & Home Safety (IBHS) has already provided a versatile and relatively affordable outline for safer construction standards.

Known collectively as the FORTIFIED method, such standards reinforce the durability of homes against severe weather, involving, for example, anchoring roofs to wall framing using stronger nails. The FORTIFIED method is, at present, completely voluntary, though the insurance industry-funded Strengthen Alabama Homes incentivizes homeowners to retrofit their houses along these guidelines via thousand-dollar grants. Completed retrofits reduce post-disaster claims and qualify grantees for substantial insurance premium discounts, prompting flood-prone Louisiana to replicate the program.

Given the programs’ demonstrated success, “updating our building codes to align with proven frameworks like IBHS’s FORTIFIED standards is not just an option — it’s a necessity,” Berven wrote. “The time for action is now, and the cost of inaction is far too high.”

Many consumers are unaware of the current absence and potential benefits of building code regulations, he continued, emphasizing an industry need for greater public outreach. Building codes play an indispensable role in enhancing resilience against evolving climate and weather risks, but any “revolution” in their regulation cannot advance without the collaboration of all relevant stakeholders.

The need for collective action to address the property/casualty risk crisis was a recurring theme throughout Triple-I’s Joint Industry Forum in Miami – particularly during the panel on climate risk and resilience. The discussion focused heavily on what’s currently being done to address this evolving area of peril.

The panel, moderated by Veronika Torarp – a partner in PwC Strategy’s insurance practice – consisted of subject-matter experts representing a cross section of natural perils, from hurricanes and floods to wildfires and severe convective storms. They were:

Dr. Philip Klotzbach, research scientist in the Department of Atmospheric Science at Colorado State University;

Matthew McHatten, president and CEO at MMG Insurance and chairman of Triple-I’s Executive Leadership Committee;

Emily Swift, sustainable business framework senior manager at American Family Insurance; and

Heather Kanzlemar, consulting actuary at Milliman.

Part of the reason for this need to build coalitions is the diverse and overlapping causes of climate-related events and the related losses. Torarp cited a PwC study that projects the global protection gap in 2025 at $1.9 trillion, though she acknowledged that number may turn out to be “an understatement”.

Warmer, wetter, riskier

Running through the discussions of the various perils was the dynamic nature of evolving threats and the protection gap. Examples included increased inland flooding, such as the devastation caused in the rural southeast by Hurricane Helene, and damage inflicted by surprisingly intense tornadoes spun off by Hurricane Milton.

Dr. Klotzbach discussed the “very busy” 2024 Atlantic Hurricane season with its surprising impact on Asheville, N.C., and surrounding communities from Helene.

“It’s important to understand that the inland flooding threat is extremely problematic,” he said.

MMG’s McHatten emphasized the complexity of addressing flood risk, given the environmental forces driving it.

“Warmer planet, warmer ocean, more precipitation, more wind,” he said, “as well as this dynamic of atmospheric rivers and what happens to them as they start to hit higher elevations.” He pointed out how such conditions – which led to cataclysmic rains in Ashville as well as in MMG’s home state of Maine and the mountains of Vermont – are exacerbated by population trends.

“People live near water because that’s where economy and commerce was,” he said. “The ability to adapt to dynamic conditions that are changing rapidly is super-difficult. We can’t just say, ‘Raise every house six feet’ that’s near a body of water.”

Hope amid the perils

American Family’s Emily Swift discussed the state of severe convective storm risk, which she said is tending to migrate from its historic domain of the U.S. Midwest toward the Southeast.

“As we’re seeing the impact of hurricanes move further west and severe convective storms move further east, that means a lot more risk exposure to our customers who are living in those regions,” she said. “However, I think there’s a lot of hope.”

Swift talked about emerging partnerships between the insurance industry and academia — particularly work being done through Industry-University Cooperative Research Centers (IUCRC) funded by the National Science Foundation (NSF) to better understand severe convective storms and develop innovative ways of addressing the risks they pose.

“I’m optimistic that, although we don’t know quite the direction where severe convective storms are heading, we at least have diversified our risks to better manage them” – thanks, in part, to the learnings derived from these partnerships, Swift said.

Kanzlemar reinforced Swift’s optimistic tone in discussing Milliman’s work around wildfire risk. In the midst of a growing insurance availability and affordability crisis in fire-prone states – particularly California – Milliman is partnering with the Insurance Institute for Building and Home Safety (IBHS) and and stakeholders in its Wildfire Prepared Home program to gather data to help inform insurance underwriting, as well as mitigation and prevention at the community level.

“Most insurers have data on type of structure, what the roof material is, the number of stories,” Kanzlemar said, “but a lot of the granular data around eave enclosures, ember-resistant vents, that data is typically not available, and almost no insurers had that data at a community level to account for adjacent risk.”

That’s the bad news, she said, but “the good news is in the kinds of solutions we’re working toward. Most insurers were willing to consider a contributory data model like a comprehensive loss-underwriting exchange for [wildland-urban interface (WUI)] data as long as there’s sufficient participation and reciprocity. That’s an effort that we’re calling the ‘WUI Data Commons’. ”

All the panelists agreed that such collaborative, data-driven approaches that respect consumer needs and interests at the community level were going to be key to solving natural catastrophe risk in our rapidly changing future.

From “social inflation” to “tort reform” to, simply, “fraud,” settling upon uniform terminology to describe litigation trends that drive up costs – including insurance premiums – for all Americans is a primary challenge to addressing them, according to participants at Triple-I’s 2024 Joint Industry Forum.

“As we’re trying to raise awareness of this problem with consumers, ‘social inflation’ doesn’t work,” said discussion moderator and Triple-I’s Chief Insurance Officer Dale Porfilio. Though Triple-I previously favored “social inflation,” consumer testing was done that suggested a better name was needed. “That’s when we landed on ‘legal system abuse.’”

“The name absolutely matters,” said Viji Rangaswami, senior vice president and chief public affairs officer for Liberty Mutual. “When you talk to a legislator, whether that’s in Kansas or in Washington, D.C., and you say the words, ‘social inflation,’ they don’t know what you’re talking about. But when you say the words ‘legal system abuse,’ you see the lightbulb go off.”

Louisiana Insurance Commissioner Tim Temple – a self-described “unicorn” among insurance regulators, given his decades-long background in the industry as an agent, broker, and company president – even renamed programs to address “legal system abuse” when he assumed office in January. This shift exemplifies Temple’s commitment to using his experience to shape a regulatory and statutory environment that enhances the attractiveness of Louisiana’s insurance market.

“We’re getting more buy-in now, people understand it,” Temple said. “That’s part of transparency – talking about what it truly is.”

Clear communication is key

Opaque, ill-defined language empowers predatory “billboard attorneys” to define these terms themselves, contributing to pervasive policyholder distrust, said Jeff Sauls, Farmers Insurance head of legislative affairs.

“There’s this perception of the insurance industry amongst the public – and plaintiffs’ attorneys help portray this – as a high-margin business,” he said, when, in reality, “we compete with grocery stores for who can make less money in an average year.”

Attorney advertising – estimated to total over $2.4 billion across the U.S. last year – has commandeered the messaging once associated with insurers, noted Temple, who encouraged the industry to “take back that high ground” of providing “dependability and stability during the worst days of people’s lives” without overuse of brand mascots or jingles.

“We have to remind the public why we exist,” Rangaswami added. “We want to pay claims as expeditiously as possible…. We’re on the side of the consumer, whereas the plaintiffs’ attorney is often on their own side or the investor’s side.”

Third-party litigation funding

With her reference to “investors,” Rangaswami took aim at a little-known, rapidly growing practice called third-party litigation funding (TPLF), in which investors with no stake beyond potential profit step in to fund lawsuits against corporate entities perceived as having deep pockets. As of last year, such investors retained an estimated $15.2 billion in assets for U.S. litigation alone.

Only a handful of states require mandatory disclosure of TPLF, which enables hedge funds and other foreign funders to compound and profit from protracted and even fraudulent U.S. court cases. Secrecy surrounding TPLF prevents insurers and regulators from identifying, let alone mitigating, the risks of increased costs and time to resolve claims disputes.

Preventing adversaries to the U.S. from exploiting TPLF to influence settlement outcomes and access sensitive defense information is another concern.

“We’re looking at TPLF as potentially exacerbating national security risk,” said Jerry Theodorou, policy director for finance, insurance, and trade at the R Street Institute. “Most people don’t know what TPLF is and the way it can insidiously impact the economy, our businesses, our jobs.”

Everyone is affected

Legal system abuse costs the highly litigious states Louisiana and Georgia over 175,000 jobs combined and thousand-dollar “tort taxes” for each resident per year, earning both states recurring spots on the American Tort Reform Foundation’s list of “Judicial Hellholes.” They also rank among the least affordable places for auto and homeowners’ insurance by the Insurance Research Council – an affiliate of The Institutes, like Triple-I.

Louisiana recently enacted a law enforcing some oversight over TPLF, Temple noted, as well as repealed a unique “three-year rule” that impeded actuarially-sound underwriting. But as the state’s bodily injury claims climb well over the national average, more reform is needed to return insurance profitability to the state.

“One thing I would look to is importing some of the good things Florida has done,” Theodorou suggested, explaining that reform curtailing contingency and one-way attorneys’ fees “have brought down the number of lawsuits against insurance companies by 24 percent” for the second consecutive three-quarter period. “Notice of intention to sue is also down by double digits. It’s working, so let’s learn from that.”

Considering the fact that the former “poster child” for legal system abuse generated over 70 percent of all homeowners insurance litigation nationally in 2022 – despite accounting for only about 15 percent of total homeowners claims – Florida’s reduced premium growth and nine new property insurers this year reveal the likely efficacy of such reforms in other states.

Education and coalition building

But such reform requires advocacy, which requires consumer education and coalition building across diverse stakeholder groups, Rangaswami pointed out.

Fixing “an economy-wide problem,” she explained, requires an “economy-wide coalition.”

The end goal is not a “tilted playing field,” Sauls emphasized. “We’re trying to get to a place where we are all on level footing, without being exploited by plaintiffs’ attorneys.”

Legal system abuse “is going to be a pressure point for the industry moving forward,” stressed Fred Karlinsky, shareholder and global chair of Greenberg Traurig, LLP. “No state is immune from what we’ve seen in Florida.”

Karlinsky emphasized that spreading normalization of “nuclear” (over $10 million) and an emergent class of “thermonuclear” (over $100 million) verdicts will stall reform in newly targeted states.

Rangaswami pointed out that not all the news has been bad.

“We had some great wins in 2024,” she said, citing Florida’s improved insurance market and legislation introduced at both the federal and state levels as movement in a promising direction. “But we have to keep this momentum up.”

Babcock Ranch – a small community in southwestern Florida dubbed “The Hometown of Tomorrow” – made headlines for sheltering thousands of evacuees and never losing power during Hurricane Milton, which devastated numerous neighboring cities and left more than three million people without power.

Hunters Point, a subdivision on Florida’s Gulf Coast, remained similarly unscathed during both Hurricanes Helene and Milton. Though the development is only two years old, it’s already been through four major hurricanes. Its homes were designed with an elevation high enough to avoid severe flooding and materials that make them as sturdy as possible in high winds. When the power goes out, each home turns to its own solar panels and battery system.

For residents of both communities, this news comes as no surprise; their flood-resistant infrastructure and solar panel power systems have helped them survive several storms and hurricanes with only minor damages, demonstrating the utility of disaster resilience planning.

Such planning is expensive to implement. Homes in either community can run for over a million dollars. But, as the combined costs of Hurricanes Helene and Milton rise to the tens of billions, it’s hard to overstate the long-term benefits. Every dollar invested in disaster resilience could save 13 in property damage, remediation, and economic impact costs, suggesting risk mitigation and recovery strategies will become even more essential as natural catastrophe severity increases.

Incentivizing investment

The National Flood Insurance Program (NFIP) Community Rating System (CRS) – a voluntary program that rewards homeowners with reduced premiums when their communities invest in floodplain management practices that exceed NFIP minimum standards – aims to encourage resilience. Class 1 is the program’s highest rating, qualifying residents for a 45 percent reduction in their premiums. Of the nearly 23,000 participating NFIP communities, only 1,500 participate in the CRS. Of those 1,500, only two – Tulsa, Okla., and Roseville, Calif. – have achieved the highest rating.

High ratings are difficult to secure and maintain. Homeowners in Lee County, which borders Babcock Ranch, nearly lost their discounts earlier this year due to improper post-Hurricane Ian monitoring and documentation within flood hazard areas.

Discounts in lower-rated jurisdictions, however, still equate to large premium reductions. Miami-Dade County, Fla., for instance, earned a Class 3 rating after extensive stormwater infrastructure upgrades, saving the community an estimated $12 million annually. Residents sustained minimized flooding from Hurricane Milton under these improvements, further justifying their cost.

Local mitigation efforts offer targeted resilience solutions and resources to alleviate community risks. The insurance industry-funded Strengthen Alabama Homes provides homeowners grants to retrofit their houses along voluntary standards for constructing buildings resistant to severe weather. Completed retrofits reduce post-disaster claims and qualify grantees for substantial insurance premium discounts, prompting flood-prone Louisiana to replicate the program.

Other nature-based planning exploits local flora as a source of natural hazard protection. Previous studies support conserving natural wetlands and mangroves to impede the rate and flow of flooding, leading many communities – including Babcock Ranch, which is 90 percent wetlands – to invest in green infrastructure. Reforestation and wetland restoration projects undertaken by the Milwaukee Metropolitan Sewerage District (MMSD) also promise to store or capture millions of gallons of storm and flood water, enabling risk management alongside improved quality of life for citizens.

Most resilience projects are impossible to fund or operate without stakeholder partnerships and advanced data and analytics. Insurers, who have long assessed and measured catastrophe risk utilizing cutting-edge data tools, are uniquely positioned to confront these evolving risks and present a framework for successful preemptive mitigation.