I wrapped up my first-ever Climate Week NYC last week at ClimateTech Connect. After their two-day April event in Washington, D.C., I could hardly miss this special half-day update when it was so close to home.

Fifty-plus attendees crammed a room near Grand Central Station, and I immediately spotted familiar faces and had the opportunity to meet with a mix of industry veterans and relative newbies spanning all insurance disciplines, from underwriting and claims to the cutting edge of modeling and artificial intelligence. Top insurance thought leaders and influencers were there to speak on climate-related issues of pressing interest to my industry and everyone it serves. The panel themes and the panelist themselves made it clear from the start that a blog post was not going to do the event justice.

The first panel – Pioneers Shaping the Future of Climate Resilience – was moderated by Francis Bouchard, managing director for climate at Marsh McLennan, whose bona fides include senior positions with Zurich Insurance and the Reinsurance Association of America. Francis moderated a no-holds-barred panel of young insurance leaders: Angela Grant at Palomar, Michael Gulla of Adaptive Insurance, and Valkyrie Holmes of Faura. The energy and expertise of these panelists left me feeling that the industry – in the face of myriad challenges – is being put into good hands.

The next discussion was moderated by Jerry Theodorou, a director at the R Street Institute whose professional background includes roles at Conning, AIG, and Chubb. It featured Dan Kaniewski, managing director and U.S. public sector lead for Marsh McLennan and a former FEMA deputy administrator, and Raghuveer Vinukollu, head of climate insights and advisory for Munich Re. The depth and timeliness of these three experts’ insights made for an engaging and thought-provoking session.

The third panel was both engaging and accessible – a bit surprising to me, given that it consisted entirely of PhDs. Steve Weinstein, CEO of Mangrove Property Insurance led a discussion among Joanna Syroka of Fermat Capital Management, Catherine Ansell of JPMorgan Chase, and M. Cameron Rencurrel at Mercury Insurance on not only “Why Science Needs to Be in the Boardroom,” but HOW young scientists can find their way there and decide IF that’s where they want to be.

Between these panels were presentations from representatives of several insurtechs who shared their data-driven solutions focused on understanding and addressing climate-related panels. All this in a period of about three hours (not including the networking reception afterward). Despite all the information shared, the event did not feel at all rushed.

If you weren’t able to make it and are feeling a bit left out, don’t fret! ClimateTech Connect 2026 will be held in Washington, D.C., on April 8 and 9, 2026.

Economic shifts, geopolitical uncertainties, cybersecurity trends, and mounting climate perils have created an increasingly severe and interconnected risk crisis, according to participants in a members-only Triple-I webinar.

In an environment constrained, for instance, by frequent natural disasters and rising replacement costs, risks no longer develop in isolation. They collide with and compound each other. Their combined impact exceeds the sum of individual risks’ effects. Such interdependence complicates identifying, let alone mitigating, the forces underpinning a specific risk.

“Under this new system that’s emerging, risk can propagate very rapidly through a host of otherwise disconnected networks,” TradeSecure president and cofounder Scott Jones told webinar host Michel Léonard, Triple-I’s Chief Economist and Data Scientist. “This new reality fundamentally challenges the core principles that insurance has relied on for centuries.”

Jones emphasized the growing unpredictability of risk on a global scale, particularly as nations impose export controls, sanctions, investment restrictions, and tariffs for purposes like economic competition. Companies with global footprints may struggle to ascertain these interwoven, sometimes competing regulations, creating compliance concerns and potentially exacerbating supply-chain disruptions.

With the frequency and severity of U.S. cyber claims on the rise, cyberattacks also carry substantial transnational implications. Sophisticated ransomware encounters can exploit businesses of all sizes, propelling privacy liability claims and related third-party litigation.

TradeSecure vice president and cofounder Michael Beck explained how the almost universal accessibility of malware – harnessed by criminal syndicates, activist groups, or even lone hackers – presents “a new class of systemic non-physical disruption” that could undermine “the entire system’s liquidity and stability.”

“A coordinated non-state cyberattack wouldn’t just steal money – it could stop the flow of money, causing many transaction failures and possibly triggering a wave of claims far beyond what traditional cyber policies are designed to handle,” Beck said.

Though insurers as well as business owners and consumers consider cyber incidents a chief risk concern, personal cyber take-up rates remain low, with the broader cyber insurance market facing its third consecutive year of declining rates. Misunderstandings surrounding cyber risk and benefits of coverage fuel this discrepancy, revealing a gap between agent perceptions of product value and that of their customers.

Analysis based on granular, cutting-edge data is essential to staying ahead in our rapidly shifting risk landscape. During Triple-I’s Joint Industry Forum in Chicago, two “Risk Take” presenters dove deep into the innovative data initiatives they engaged in to help turn these challenges into new opportunities for insurers.

Balancing consumer needs

With natural catastrophe frequency and supply chain uncertainty on the rise, so are home maintenance costs. Estimated to exceed $10,000 annually in 2024 – at a 5.9 percent year-over-year increase – home maintenance further weighs against the mounting costs of premium rates and property taxes across the U.S., leading many homeowners to forgo investing in at-home risk mitigation like smart home telematics.

“Across the providers we’ve talked to, adoption of telematics falls somewhere between the single digits,” said presenter James Bilodeau, CEO and founder of PreFix Inc. “The reason is simple: the value proposition of what we would like homeowners to do isn’t important enough compared to what homeowners actually need.”

For Bilodeau, the solution is also simple: combine advanced technology with routine preventative maintenance. By providing personalized, year-round home repair, Bilodeau’s Texas-based firm aims to mitigate losses while gathering unique primary data on the properties they service. Insurers can use this data to develop telematics technology and more accurately price the associated risks.

Such data collection “creates a flywheel in which we help our partners delight their customers with exceptional service and hit directly at affordability issues, both with home maintenance and in premium reduction,” Bilodeau said.

After a successful pilot program, USAA expanded its partnership with the company to offer discounted maintenance services to members who sign up for PreFix. Noting that the company is pursuing partnerships with other major insurers, Bilodeau highlighted that industry collaboration is crucial to not only facilitate more refined coverage but to lower the cost of entry to enhancing resilience.

Emerging public safety risks

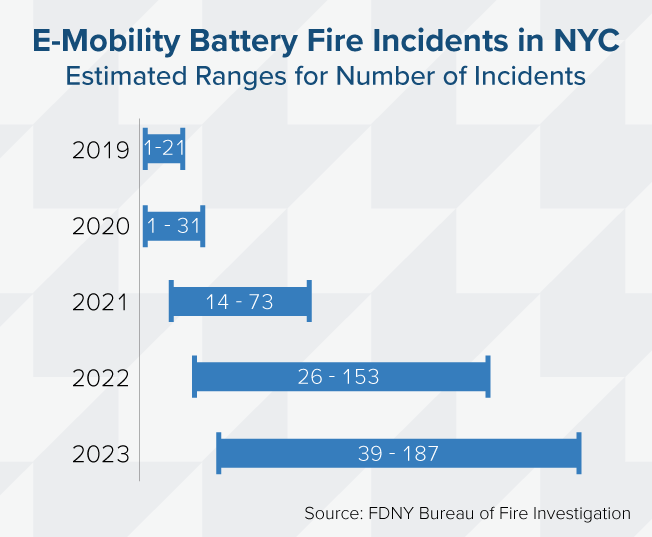

An eightfold increase in New York City fire incidents between 2019 and 2023 correlates strongly with the growing popularity of e-mobility devices, according to a joint report by UL Standards & Engagement (ULSE) and Oxford Economics that is based in part on Triple-I data.

Presenting on the report, ULSE Director of Insights Sayon Deb explained how lithium-ion battery fires linked to e-bikes and scooters became a mainstream risk for COVID-era urban environments, due in part to the booming online food and grocery delivery market.

“Nearly $519 million worth of damages were caused in just four years from structural property damage, injuries, and loss of life,” Deb said, pointing out that this figure does not account for “the additional cost of communal fear, in terms of fires happening across the hallway from you, and also the loss in economic opportunities and the community toll that it takes as we respond to these fires.”

Inadequate public safety awareness, paired with the easy availability of uncertified devices, helped fuel the crisis. Beyond overusing or incorrectly charging the devices, e-mobility users often left them in dangerous locations, with “66 percent of those who charge at home charging their devices near their exit,” Deb explained – effectively “blocking your exit from your home in the event of a fire.”

E-mobility regulations vary wildly by state. Though New York City regulations passed in 2023 show progress, ULSE recommends more proactive public outreach, safety standard enforcement, and incident reporting to better track e-mobility risk data.

“The better the data we collect, the better we can understand where, how, and why these battery fires occur, so that we can prevent future fires from happening,” Deb concluded.

Identifying key risk trends amid an increasingly complex risk landscape was a dominant theme throughout Triple-I’s 2025 Joint Industry Forum – particularly during the panel spotlighting some of the insurance industry’s C-suite leaders.

Moderated by CNBC correspondent Contessa Brewer, the panel consisted of:

J. Powell Brown, president and CEO of Brown & Brown Inc.;

John J. Marchioni, chairman, president, and CEO of Selective Insurance Group;

Susan Rivera, CEO of Tokio Marine HCC (TMHCC); and

Rohit Verma, president and CEO of Crawford & Co.

Their discussion provided insight into how insurers can transform these uncertainties into opportunities for business development and for cultivating deeper connections with consumers.

Recouping policyholder trust

Given the volatility of the current risk environment – exacerbated by various ongoing geopolitical conflicts and the rising frequency and severity of natural catastrophes – it is more imperative than ever to reaffirm the intrinsic human element of insurance, the panelists agreed.

“That’s one of the most underappreciated aspects of our industry,” Marchioni said. “We make communities safer and put people’s lives and businesses back together after an unexpected loss. Being the calming force when you have unsettling events like this happen around the world is a big part of what we do.”

Yet prevailing public perception continues to indicate otherwise, even as insurers report repeated losses or nominal profits compared to other industries.

“The insurance industry may be the only industry where record profits are a problem,” CNBC’s Brewer added, because consumers tend to “not care whether it’s coming from your investments, or whether it’s coming from your underwriting business or your reinsurance. They just hear that you’re making record profits.”

Brown noted that consumer mistrust derives, in part, from “a very active plaintiffs’ bar,” which the American Tort Reform Association estimates spent over $2.5 billion for nearly 27 million ads across the United States last year. He further discussed how, though the average homeowners’ insurance premium rate in Florida will increase this year, his home state has enjoyed far more stable rates after tort reforms eased litigation costs on insurers.

Previous research by the Insurance Research Council (IRC) – like Triple-I, an affiliate of the Institutes – showed that most consumers perceive the link between attorney advertising and higher insurance costs. Crawford’s Verma, however, emphasized that this awareness does not necessarily translate into consumers understanding their own agency.

“It’s easier for homeowners to understand how the weather impacts potential losses and the fact that weather patterns have changed,” Verma said. “But when it comes to [legal system abuse], I don’t think that connection is as well understood.”

Reflecting on a record high in nuclear verdicts last year, Rivera suggested insurers must reconfigure how they communicate legal system abuse to consumers.

“Where are those hospital professional liability verdicts going to go?” he said. “They’re going to go back into the cost of health care at the end of the day.”

Leading the AI charge

Maintaining consumer centricity while implementing or experimenting with technological innovations – especially generative AI – was a unifying objective for all the panelists.

“We look at AI as an enabler,” Brown said, “so we can put teammates in a position to spend more time with customers, which is the most important thing.”

For Tokio Marine’s Rivera, AI “ultimately helps all of our insureds” by boosting operational efficiency while reducing operational costs, as well as facilitating more proactive risk management than ever before. A growing percentage of insurance executives appear to agree, as generative AI models continue to expedite data processing across the insurance value chain, reshaping underwriting, pricing, claims, and customer service.

Such efficiency, paired with the potential for improved decision-making, is crucial “in our dramatically changing environment,” Marchioni stressed.

“We have thousands of claims every day,” he said. “Thinking about lawsuit abuse as a backdrop – a claims adjuster, every day, has to make decisions regarding, ‘Do I settle this claim based on injuries or venue? What’s the value of the injury and of the claim? Who’s the plaintiffs’ attorney?’ These tools give more refined information so your knowledge workers can make better, more timely decisions.”

Generative AI fails, however, when base datasets are insufficient, outdated, or inaccurate, Brown pointed out. Training AI models uncritically can lead to outputs containing false and/or nonsensical information, commonly known as “hallucinations”.

At their current capacity, at least, AI models cannot draw the kinds of salient conclusions that adjustors and underwriters can, meaning AI could “change the way we work, but it’s not going to replace the jobs,” Verma said.

Though they do not currently exist in the United States at the federal level, AI regulations have already been introduced in some states, following a comprehensive AI Act enacted last year in Europe. With more legislation on the horizon, insurers must help lead these conversations to ensure that AI regulations suit the complex needs of insurance, without hindering the industry’s commitments to equity and security.

A 2024 report by Triple-I and SAS, a global leader in data and AI, centers the insurance industry’s role in guiding conversations around ethical AI implementation on a global, multi-sector scale, given insurers’ unique expertise in analyzing and preserving data integrity.

Insurance industry executives and thought leaders gathered yesterday for Triple-I’s Joint Industry Forum (JIF) in Chicago to discuss the trends, economics, geopolitics, and policy influencing the market today, as well as ways to navigate these complexities while focusing on making their products affordable and available for consumers.

Triple-I CEO Sean Kevelighan in his opening remarks, noted that effective risk management depends on collaboration across stakeholder groups, as interconnected perils “present a community problem, not just an industry problem.”

JIF keynote speaker Louisiana Insurance Commissioner Tim Temple said facilitating community resilience planning is a top priority for the National Association of Insurance Commissioners (NAIC). The NAIC’s 2025 initiative – “Securing Tomorrow: Advancing State-Based Regulation” – aims to improve disaster mitigation and recovery by consolidating “the collective expertise of experienced state regulators from across the country, who can share real-time insights and proven strategies,” Temple said.

Among the initiative’s goals is aggregating more data from insurers to better understand challenges to affordability and availability on state levels, which the NAIC can then translate into actionable policy proposals. Such data calls, Temple said, help regulators, legislators, and policyholders focus on improving the cost drivers of insurance rates.

Louisiana has consistently been among the least affordable states for homeowners and auto insurance, according to the Insurance Research Council (IRC), in part because of its reputation for being plaintiff-friendly in civil litigation. Significant tort legislation has been approved in the state, but resistance to reform remains a challenge.

Getting to the roots of high premiums

After a recent data call in his home state, Temple told the JIF audience, “For the first time in Louisiana, we’re not talking about only premiums. We’re talking about why premiums are where they are.”

A critical lack of transparency surrounding cost drivers persists, however. Temple criticized the National Flood Insurance Program’s Risk Rating 2.0 reforms for not publicly disclosing more information “for individuals and communities to identify and address factors driving up their premiums,” such as “whether increased rates take into account levee systems, pump stations, and other things designed to help mitigate against floods.”

Conversely, government programs like Strengthen Alabama Homes – and the numerous programs it inspired, including in Louisiana – have demonstrated success in communicating the benefits of resilience investments for consumers and policymakers.

“We’re seeing major positive results after just a few short years,” Temple said, noting that, since early 2024, over 5,000 homeowners not chosen for Louisiana’s grant program still decided to invest in the same hazard mitigation, as they may still qualify for the corresponding state-mandated insurance discounts.

“As natural disasters become more frequent and severe, state regulators will continue to drive forward common-sense policies that protect consumers and ensure that insurance remains available and reliable for at-risk communities,” Temple concluded. Developing the database required for such policies is a necessary first step.

Keep an eye on the Triple-I Blog for further JIF coverage.

By Sayon Deb, Director of Insights, UL Standards & Engagement

In just five years, lithium-ion battery fires linked to e-mobility devices have evolved from a fringe risk into a mainstream safety and liability crisis – particularly in dense urban areas, like New York City, where adoption of these devices has outpaced regulatory safeguards.

In addition to the obvious public safety threat, e-mobility battery related fires represent a significant and expanding liability exposure for insurers, property managers, and city agencies. Our latest report – developed in collaboration with Oxford Economics – sets out to answer a more fundamental question: What is this crisis truly costing the city?

The answer, conservatively estimated, is up to $519 million in combined human and economic loss between 2019 and 2023. This figure includes fatalities, injuries, and structural property damage

Why Now? Why New York?

The dramatic rise in fire incidents – an estimated eightfold increase from 21 in 2019 to as many as 187 incidents in 2023 – correlates strongly with the influx of low-cost, uncertified e-bikes and scooters. New York City’s unique combination of traffic congestion, delivery-based gig work, and dense multi-family housing has made it a case study in how quickly innovation can outstrip risk management.

Data from the Fire Department of New York, the Consumer Product Safety Commission, and UL Solutions’ Lithium-Ion Battery Fire Incident Database formed the foundation of our modeling. This helped us generate incident estimates of fatalities, injuries, and structural properties damages.

Oxford Economics translated these incident reports into cost estimates using a rigorous, conservative methodology by applying federal valuation metrics for loss of life and injury. Fatality costs were calculated using the U.S. Department of Transportation’s Value of a Statistical Life, set at $13.2 million per life as of 2023. Non-fatal injury costs were derived as severity-weighted fractions of that value, ranging from minor injury to critical injury, in accordance with DOT and Office of Management and Budget economic guidance.

Our analysis then integrated structural fire cost benchmarks from both Triple-I and the National Fire Protection Association. Triple-I’s data was particularly important in defining the upper-bound estimates for property loss. Claims data on the average insurance payout for residential fire damage provided a grounded, actuarial counterweight to NFPA’s generalized national averages.

This dual-source approach allowed us to capture a more realistic range of likely losses across different housing types, from NYCHA public units to private homes.

A growing blind spot for insurers

From a risk-modeling standpoint, e-mobility fire incidents don’t map easily to conventional insurance categories. Many e-mobility users, particularly gig economy workers, rely on leased, used, or modified e-bikes and e-scooters to meet delivery demands. Some of these devices are powered by third-party or uncertified batteries or, in some instances, contain second-hand components. This creates a messy risk environment in which it’s hard to know who owns what, how it has been maintained, or how it’s being used. Moreover, fires resulting from these devices often fall outside the scope of standard product warranties or manufacturer responsibility. This makes it difficult to determine who’s responsible when something goes wrong.

For insurers, this presents a growing blind spot. Traditional assumptions around property and contents coverage did not include high-risk devices charged in hallways or shared living spaces or for ignition sources that are not part of conventional product recall channels.

A $300 imported battery with no certification can trigger a six-figure claim, and those risks are becoming more common.

The Path Forward

Regulatory momentum is improving. New York City’s Local Law 39, signed in 2023, bans the sale and lease of uncertified e-mobility devices. In July 2024, New York Governor Hochul enacted additional statewide measures to support battery safety and user education. Federal legislation aimed at establishing nationwide safety requirements for lithium-ion batteries used in e-bikes and e-scooters is making its way through Congress. While these are positive steps, enforcement and awareness remain uneven, leaving significant gaps in consumer protection and risk mitigation.

From our perspective at ULSE, a multi-pronged strategy is essential:

Better enforcement of safety standards for batteries and chargers.

More robust public education on safe charging practices.

Trade-in and swap programs that encourage delivery workers to discard unsafe batteries.

Underwriting models that consider device certification, consumer behavior, and building type.

Improved incident reporting frameworks that enable cities and insurers to collect better data and therefore better track risk exposure.

With better data, smarter standards, and more coordinated public-private action, the future of e-mobility will thrive with safety at its center.

Mr. Deb will be among the risk and insurance industry thought leaders speaking at Triple-I’s Joint Industry Forum (JIF) in Chicago on June 18, 2025. It’s not too late to register to attend this insight-driven event.

The Institutes’ Pete Miller and Francis Bouchard of Marsh McLennan discuss how AI is transforming property/casualty insurance as the industry attacks theclimate crisis.

“Climate” is not a popular word in Washington, D.C., today, so it would take a certain audacity to hold an event whose title prominently includes it in the heart of the U.S. Capitol.

For two days, expert panels at the Ronald Reagan Building and International Trade Center discussed climate-related risks – from flood, wind, and wildfire to extreme heat and cold – and the role of technology in mitigating and building resilience against them. Given the human and financial costs associated with climate risks, it was appropriate to see the property/casualty insurance industry strongly represented.

Peter Miller, CEO of The Institutes, was on hand to talk about the transformative power of AI for insurers, and Triple-I President and CEO Sean Kevelighan discussed – among other things – the collaborative work his organization and its insurance industry members are doing in partnership with governments, non-profits, and others to promote investment in climate resilience. Triple-I is an affiliate of the Institutes.

Sean Kevelighan of Triple-I and Denise Garth, Majesco’s chief strategy officer, discuss how to ensure equitable coverage against climate events.

You can get an idea of the scope and depth of these panels by looking at the agenda, which included titles like:

Building Climate-Resilient Futures: Innovations in Insurance, Finance, and Real Estate;

Fire, Flood, and Wind: Harnessing the Power of Advanced Data-Driven Technology for Climate Resilience;

The Role of Technology and Innovation to Advance Climate Resilience Across our Cities, States and Communities;

Pioneers of Parametric: Navigating Risks with Parametric Insurance Innovations;

Climate in the Crosshairs: How Reinsurers and Investors are Redefining Risk; and

Safeguarding Tomorrow: The Regulator’s Role in Climate Resilience.

As expected, the panels and “fireside chats” went deep into the role of technology; but the importance of partnership, collaboration, and investment across stakeholder groups was a dominant theme for all participants. Coming as the Trump Administration takes such steps as eliminating FEMA’s Building Resilient Infrastructure and Communities (BRIC) program; slashing budgets of federal entities like the National Oceanographic and Atmospheric Administration (NOAA) and the National Weather Service (NWS); and revoking FEMA funding for communities still recovering from last year’s devastation from Hurricane Helene, these discussions were, to say the least, timely.

Helge Joergensen, co-founder and CEO of 7Analytics, talks about using granular data to assess and address flood risk.

In addition to the panels, the event featured a series of “Shark Tank”-style presentations by Insurtechs that got to pitch their products and services to the audience of approximately 500 attendees. A Triple-I member – Norway-based 7Analytics, a provider of granular flood and landslide data – won the competition.

Earth Day 2025 is a good time to recognize organizations that are working hard and investing in climate-risk mitigation and resilience – and to recommit to these efforts for the coming years. What better place to do so than walking distance from both the White House and the Capitol?

With nearly half of all homes in the United States at risk of “severe or extreme” damage from events like flooding, high winds, and wildfire, the perfect storm of climate risk and legal system abuse creates obstacles for homeowners. It also threatens a more financially vulnerable segment of the housing market, as increased premiums and waning coverage for affordable housing providers can put millions of renters at risk of becoming rent-burdened (paying more than 30 percent of gross monthly income in gross monthly rent) or unhoused.

In June of this year, about two dozen real estate, housing, and nonprofit organizations — self-describing as a “broad coalition of housing providers and lenders” — wrote a letter to Congress and the Biden administration urging them to address the issue of property insurance affordability. Although the coalition declared its intent to represent all stakeholders in the housing market, it called attention to special concerns of affordable housing providers and renters.

The letter referenced anOctober 2023 survey and report commissioned by the National Leased Housing Association (NLHA) and supported by other affordable housing organizations. The survey involved more than 400 housing providers that operate 2.7 million rental units — 1.7 million of which are federally subsidized. Findings mentioned in the letter and report about the affordable housing market include:

– Rate increases of 25 percent or more in the most recent renewal period for one in every three policies for affordable housing providers.

– Over 93 percent of housing providers said they plan to mitigate cost increases, with three most commonly cited tactics: increasing insurance deductibles (67 percent), decreasing operating expenses (64 percent), and increasing rent (58 percent).

– Respondents cited limited markets and capacity as the cause for most premium increases, followed by claims history/loss and renter population.

According to the U.S. Department of Housing and Urban Development (HUD) guidelines, affordable housing is generally defined as housing for which the occupant is paying no more than 30 percent of gross income for housing costs. These units are often regulated under various regional and nationwide programs, which typically offer some form of government subsidy to the property owners – usually either through tax credits, government-backed financing, or direct payments. Rising insurance premiums for affordable housing properties have come at a particularly challenging time for both renters and affordable housing property owners, a large share of which are non-profit organizations.

Census Data indicates that in total renters comprise around 36 percent, or about 44.2 million of the 122.8 million Census captured households. The number of rent-burdened households nationwide has hit an all-time high. The latest rental housing market figures, taken from a report issued by the Joint Center For Housing Studies Of Harvard University, counts 22.4 million rent burdened households in this category, amplifying the dire need for more affordable units. That report also reveals the proportion of “cost-burdened renters rose to 50 percent, up 3.2 percentage points from 2019.”

Additionally, homelessness increased 12 percent in 2023. More than 650,000 people were unhoused at some point last year — the highest number recorded since data collection began in 2007. AWall Street Journal analysis reveals the most recent counts for 2024 are already up 10 percent, putting the total number of unhoused persons on track to exceed last year’s amount.

Meanwhile, the affordable housing stock is aging and the cost of debt to acquire or build multifamily properties has risen, too. As interest rates have been high in recent years, developers must offer investors greater returns than treasury notes. The problem is complex, but the outcomes can be brutally straightforward.

Higher insurance premiums on rented properties increase costs, which, in turn, get passed on to renters. Market-rate landlords can usually raise rents to cover the increasing costs of capital and insurance premiums. However, affordable housing providers are locked into rents set by the government. These amounts are tied to regional incomes, which can be depressed by wage stagnation. Thus, renters who rely on affordable housing can experience the impact of rising premiums in the form of decreased services and lapsed maintenance (as housing providers dip into other parts of the operating budget to make up the shortfall) or a decrease in the number of units on the market as housing providers extract units or leave the market.

In July of this year,HUD convened a meeting with various stakeholders to discuss policies and opportunities to address this and related challenges while managing potential risks to the long-term viability of affordable housing. HUD has modified its insurance requirements for apartment buildings with government-backed mortgages, now allowing owners to set their deductible for wind and storm events as high as $475,000, up from $250,000. This tactic may reduce premiums but can also raise out-of-pocket costs after a storm or severe climate event. Another approach in progress is the revision of HUD’s methodology for calculating the Operating Cost Adjustment Factors (OCAF),parameters for annual percentile increases in rent, for eligible multifamily properties to better account for increasing insurance costs.

Triple-I is committed to advancing conversations with business leaders, government regulators, and other stakeholders to attack the risk crisis and chart a path forward. To join the discussion, register for JIF 2024. Follow our blog to learn more about trends in insurance affordability and availability across the property and casualty market.

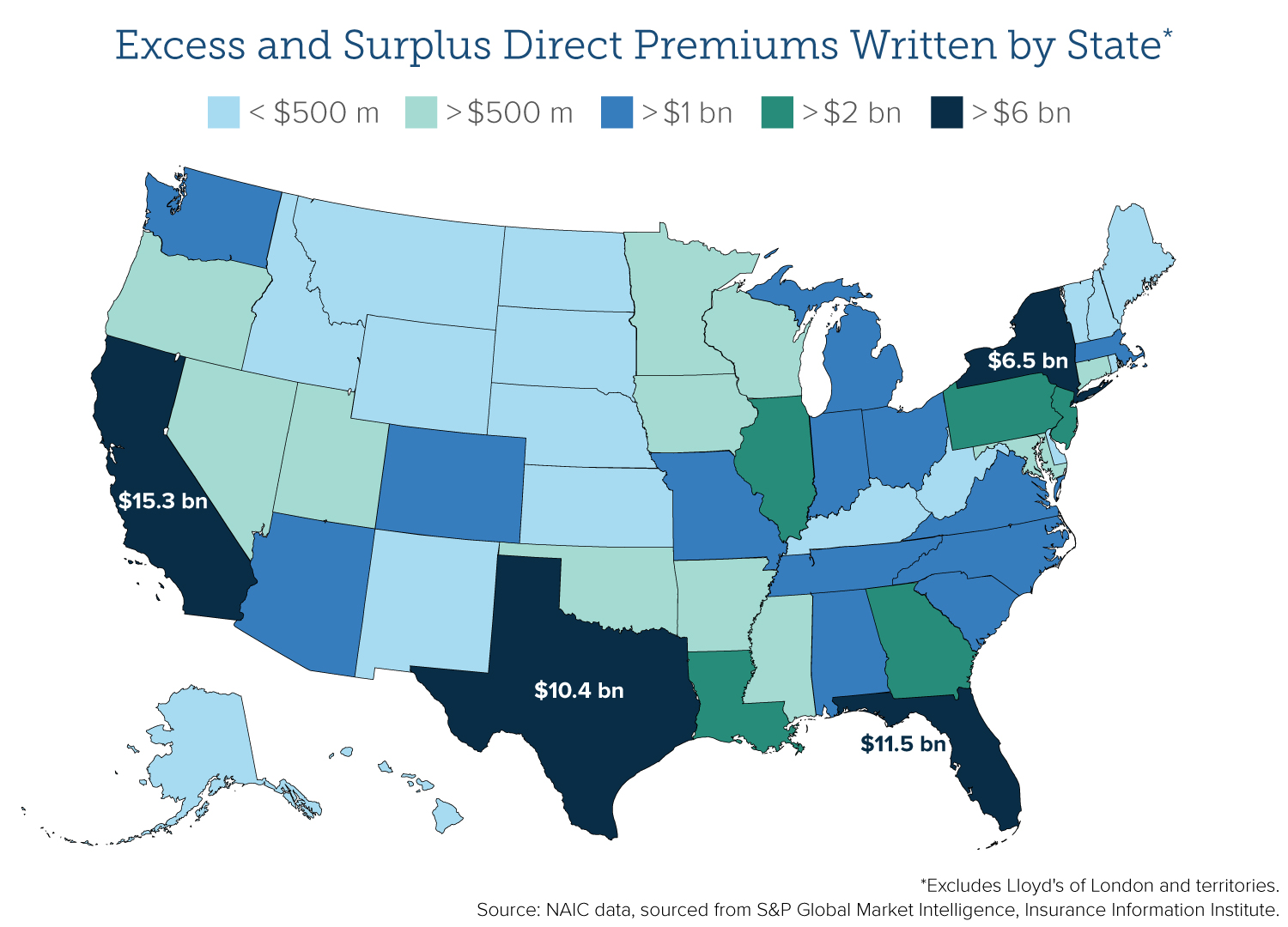

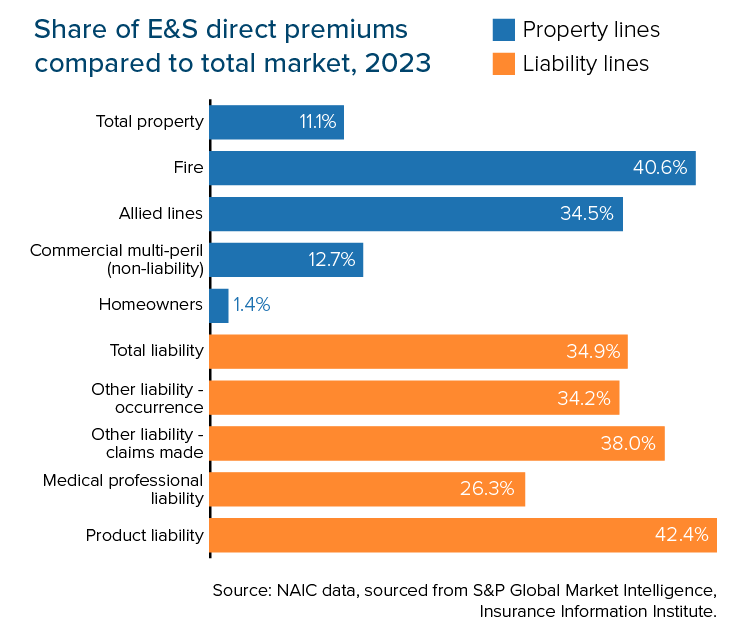

The Excess and Surplus (E&S) market has grown for five consecutive years by double-digit percentage rates. While expansion appears to have slowed, ample growth likely to continue if major trends persist, according to Triple-I’s latest issue brief, Excess and Surplus: State of the Risk.

As reported byS&P Global Intelligence, total premiums for 2023 reached $86.47 billion, up from $75.51 billion in 2022. The growth rate for direct premiums in 2023 climbed to 14.5 percent, down from the peak year-over-year (YoY) increase of 32.3 percent in 2021 and 20.1 percent in 2022. The share of U.S. total direct premiums written (DPW) for P/C in 2023 grew to 9.2 percent, up from 5.2 percent in 2013.

The brief summarizes how these outcomes are driven by the niche segment’s capacity to take advantage of coverage gaps in the admitted market and quickly pivot to new product development in the face of emerging or novel risks. Analysis and takeaways, based on data from US-based carriers, highlight dynamics that may support continued market expansion:

The rising frequency of climate disasters and catastrophes that overwhelm the admitted market

The increasing number and amount of outsized verdicts (awards over $10 million)

The sustainability of amenable regulatory frameworks

Outlook for the reinsurance segment

These factors can also converge to enhance or aggravate conditions.

For example, some states, such as Florida and California, are dealing with significant obstacles to P/C affordability and availability in the admitted market posed by catastrophe and climate risk while also experiencing large respective shares of outsized verdict activity. Also, 13 of the 15 largest U.S. E&S underwriters for commercial auto liability experienced a YoY increase in 2023 direct premiums written. In contrast, eight of the largest 15 underwriters of commercial auto physical damage coverage experienced a decline. Given 2023 research from the Insurance Information Institute showing how inflationary factors from legal costs amplify claim payouts for commercial auto liability, it appears that E&S is flourishing off the struggles of the admitted market.

At the state level, the top three states based on E&S property premiums as portion of the total property market were Louisiana (22.7 percent), Florida (21.1 percent), and South Carolina (19.4 percent) in 2023. The states experiencing the highest growth rates in E&S share of property premiums were South Carolina (9.0 percent), California (8.8 percent), and Louisiana (8.3 percent).

Since the publication of Triple-I’s brief, AM Best released its2024 Market Segment Report on U.S. Surplus Lines. One of the key updates: after factoring in numbers from regulated alien insurers and Lloyd’s syndicates, the E&S market exceeded the $100 billion premium ceiling for the first time, climbing past $115 billion. The share size in the P/C market has more than tripled, from 3.6 percent total P/C DPW in 2000 to 11.9 percent in 2023. Findings also indicate that DPW is concentrated heavily within the top 25 E&S carriers (ranked by DPW), with about 68% of the total E&S market DPW coming from this group.

The E&S market typically provides coverage across three areas:

Nonstandard risks: potential liabilities that have unconventional underwriting characteristics

Unique risks: admitted carriers don’t offer a filed policy form or rate, or there is limited loss history information available

Capacity risks: the customer to be insured seeks a higher level of coverage than most insurers are willing to provide

Thus, E&S carriers offer coverage for hard-to-place risks, stepping in where admitted carriers are unwilling or unable to tread. It makes sense that the policies typically come with higher premiums, which can boost DPW.

However, the value proposition for E&S policyholders hinges on the lack of coverage in the admitted market and the insurer’s financial stability – especially since state guaranty funds don’t cover E&S policies. Therefore, minimum capitalization requirements tend to higher for E&S than for admitted carriers. Ratings from A&M Best over the past several years indicate that most surplus insurers stand secure. Robust underwriting and strong reinsurance capital positions will play a role in the market’s capacity for continued expansion.

To learn more, read our issue brief and follow our blog for the latest insights.

The increasing frequency and severity of claims costs beyond insurer expectations continue to threaten insurance coverage and affordability. Triple-I’s latest Issue Brief, Legal System Abuse – State of the Risk describes how trends in claims litigation can drive social inflation, leading to higher insurance premiums for policyholders and losses for insurers.

Key Takeaways

Insured losses continue to exceed expectations and surpass inflation, notably impacting coverage affordability and availability in Florida and Louisiana.

In promoting the term “legal system abuse”, Triple-I seeks to capture how litigation and related systemic trends amplify social inflation.

Progress has been made toward increased awareness about the risks of third-party litigation funding (TPLF), but more work is needed.

What we mean when we talk about legal system abuse

Legal system abuse occurs when policyholders, plaintiff attorneys, or other third parties use fraudulent or unnecessary tactics in pursuing an insurance claim payout, increasing the time and cost of settling insurance claims. These actions can include illegal maneuvers, such as claims inflation and frivolous or outright fraudulent claims. Unscrupulous contractors, for example, seek to profit from Assignment of Benefits (AOBs) by overstating repair costs and then filing lawsuits against the insurer – sometimes even without the homeowner’s knowledge. Filing a lawsuit to reap an outsized payout when it’s evident the claims process will likely provide a fair, reasonable, and timely claim settlement can also be considered legal system abuse.

The latest brief provides a round-up of several studies Triple-I and other organizations conducted on elements of these litigation trends. The report, “Impact of Increasing Inflation on Personal and Commercial Auto Liability Insurance,” describes the $96 billion to $105 billion increase in combined claim payouts for U.S. personal and commercial auto insurer liability. The Insurance Research Council highlighted the dire lack of affordability for personal auto and homeowners insurance coverage in Louisiana, along with the state’s exceptionally high claim litigation rates.

Readers will also find an update on the discussion of legal industry trends associated with increased claims litigation. The lack of transparency around TPLF arrangements and the fear of outside influence on cases are attracting the attention of legislators at the state and federal levels. The brief also describes how some law firms may use TPLF resources to encourage large windfall-seeking lawsuits instead of speedy and fair claims litigation. Research findings suggest that consumers have become aware of how ubiquitous attorney ads can influence the frequency of lawsuits, increasing claims costs.

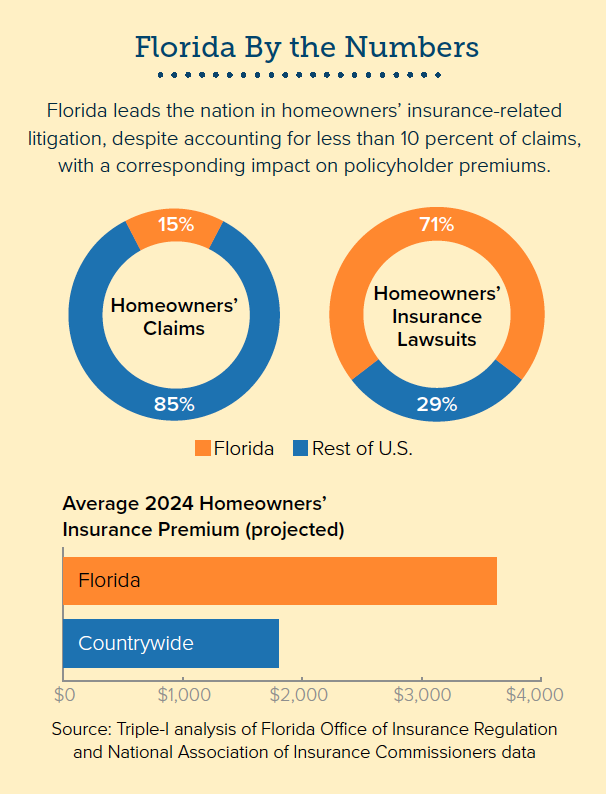

Florida: a case study in the consequences of excessive litigation

While several states, such as California, Colorado, and Louisiana, are experiencing a drastic rise in the cost of homeowners’ insurance, this brief discusses Florida. Property insurance premiums there rank the highest in the nation. Several insurers facing insurmountable losses have stopped writing new policies or left the state in the last few years. In some areas, residents are leaving, too, because of skyrocketing premiums.

Excessive claims litigation isn’t a new issue for insurers, but it can work with other elements to shift loss ratios and disrupt forecasts, rendering cost management more challenging. In Florida, factors such as the rise in home values and frequency of extreme weather events play a significant role, along with the challenges homeowners face in the aftermath: soaring construction costs, supply chain bottlenecks, and new building codes. However, Florida also leads the nation in litigating property claims. While 15 percent of all homeowners claims in the nation originate in the state, Floridians file 71 percent of homeowners insurance lawsuits.

In Florida and elsewhere, increasing time to settle a claim puts a financial strain on insurers, which is passed on to policyholders in the form of higher premiums. Legal system abuse activities are difficult (if not impossible) to forecast and mitigate, hampering insurers’ ability to remain in the market. Therefore, legal system abuse could be one of the biggest underlying drivers of social inflation. Without preventive measures, such as policy intervention and increased policyholder awareness, coverage affordability and availability is at risk.

Triple-I remains committed to advancing the conversation and exploring actionable strategies with all stakeholders. Learn more about legal system abuse and its components, such as third-party litigation funding by following our blog and checking out our social inflation knowledge hub.