A study by the Alabama Department of Insurance, in collaboration with the University of Alabama Center for Insurance Information and Research, shows that widespread adoption of IBHS FORTIFIED construction standards could dramatically reduce insurance claims from hurricanes, while also encouraging property/casualty insurers to maintain coverage in high-risk areas.

Homes built or retrofitted to FORTIFIED standards from the Insurance Institute for Business & Home Safety were found to have suffered far less property damage and a lower volume of insurance claims from Hurricane Sally — which made landfall in Gulf Shores, Alabama, as a Category 2 storm in September 2020 — than non-FORTIFIED properties.

“The results show mitigation works and that we can build things that are resilient to climate change,” said the author of the study, Triple-I non-resident scholar Lars Powell.

A collective effort

Alabama’s proactive approach – which includes mandatory insurance discounts and a state-backed grant program for resilient construction – offers a model for risk mitigation and protecting homeowners from catastrophic winds of tropical cyclones.

“Alabama was an early adopter of FORTIFIED designations for wind loss mitigation,” the report says. “In 2025, there are more than 53,000 FORTIFIED houses in the state,” out of approximately 80,000 nationwide.

The state grants and insurance discounts have been a big motivator for homeowners to make the investment. Lawmakers in other hurricane-prone states, such as Louisiana, are looking to Alabama’s strategy as they seek solutions for predicting and preventing losses from increasing natural disaster risks.

Tornado activity in 2025 has surged, with more than 1,000 reported tornadoes as of May 28 and outbreaks spreading across nearly every state east of the Rockies this season, according to according to the NOAA Storm Prediction Center.

Researchers have highlighted a shift in both the timing and geography of tornadoes, raising new safety concerns for communities outside the traditional Tornado Alley states. The widening prevalence of tornado activity has some experts suggesting that the name “Tornado Alley” be retired.

The 1,010 tornadoesreported is almost 40 percent higher than the 15-year average of 727 tornadoes for the same period. Mississippi leads with 97 tornado reports, followed by Illinois (93), Missouri (89), and Texas (87), according to AccuWeather.

Severe convective storms – which include tornadoes – are among the most common, most damaging natural catastrophes in the United States. The result of warm, moist air rising from the earth, they manifest in various ways, depending on atmospheric conditions – from drenching thunderstorms with lightning, to tornadoes, hail, or destructive straight-line winds.

In 2024, according to Gallagher Re, the economic cost solely from weather and climate events was approximately $402 billion ($151 billion insured). At least 41 percent of insured losses ($64 billion) resulted from severe convective storms.

So far this year, Gallagher said, the United States has recorded at least eight separate billion-dollar insured loss events from SCS activity so far in 2025. This compares to 13 such events by the end of May in 2024, 11 in 2023, six in both 2022 and 2021, and 12 in 2020.

In addition to tornadoes, Gallagher said, large hail – measuring two inches or more in diameter – was a major factor in driving losses.

Two lawsuits filed in Los Angeles claim major California insurers colluded illegally to impede coverage in wildfire-prone areas, forcing homeowners into the state’s last-resort FAIR Plan. Accusing carriers of violating antitrust and unfair competition laws, the two suits exemplify an ongoing disconnect between public and insurer perceptions of insurance market dynamics, exacerbated by legislators’ resistance to accommodating the state’s evolving risk profile.

An untenable situation

Both suits claim the insurers conspired to “suddenly and simultaneously” drop existing policies and cease writing new ones in high-risk communities, deliberately pushing consumers into the FAIR Plan. Left underinsured by the FAIR Plan, the plaintiffs argue they were wrongfully denied “coverage that they were ready, willing, and able to purchase to ensure that they could recover after a disaster,” Michael J. Bidart, who represents homeowners in one of the cases, said in a statement.

Established in response to the 1965 Watts Rebellion, the California FAIR Plan provides an insurance option for homeowners unable to purchase from the traditional market. Though FAIR Plans offer less coverage for a higher premium, they cover properties where insurance protection would otherwise not exist. California law requires licensed property insurers to contribute to the FAIR Plan insurance pool to conduct any business within the state, meaning they share the risks associated with those properties.

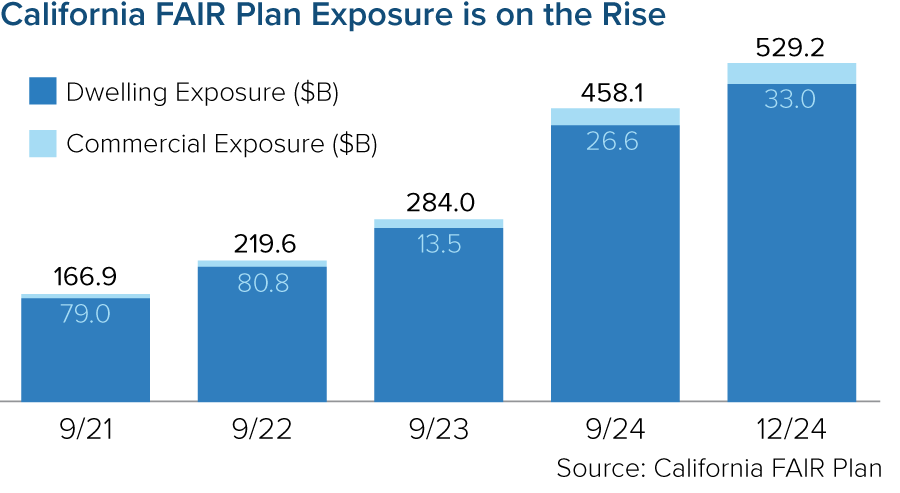

Intended as a temporary solution until homeowners can secure policies elsewhere, the FAIR Plan has become overwhelmed in recent years as more insurers pull back from the market. As of December 2024, the FAIR plan’s exposure was $529 billion – a 15 percent increase since September 2024 (the prior fiscal year end) and a 217 percent increase since fiscal year end 2021. In 2025, that exposure will increase further as FAIR begins offering higher commercial coverage for farmers, homebuilders, and other business owners.

With a policyholder count that has more than doubled since 2020, the FAIR Plan faces an estimated $4 billion total loss from the January fires alone.

Out of touch regulations

Homeowners are understandably frustrated with dwindling coverage availability, which currently afflicts many other disaster-prone states. Supply-chain and inflationary pressures, which could intensify under oncoming U.S. tariff policies, help fuel the crisis. But California’s problems stem largely from an antiquated regulatory measure that severely constrains insurers’ ability to manage and price risk effectively.

Despite a global rise in natural catastrophe frequency and severity, regulators have applied the 1988 measure, Proposition 103, in ways that bar insurers from using advanced modeling technologies to price prospectively, requiring them to price based only on historical data. It also blocks insurers from incorporating reinsurance costs into their prices, forcing them to pay for these costs from policyholder surplus and/or reduce their presence in the state.

Insurers must adjust their risk appetite to reflect these constraints, as they cannot profitably underwrite otherwise. Underwriting profitability is essential to maintain policyholder surplus. Regulators require insurers to maintain policyholder surplus at levels that ensure that every policyholder is adequately protected.

Restricting insurers’ use of prospective data, however, inhibits risk-based pricing and weakens policyholder surplus, facilitating policy nonrenewals and, in serious cases, insolvencies.

Insurance Commissioner Ricardo Lara implemented a Sustainable Insurance Strategy to mitigate these trends, including a new measure that authorizes insurers to use catastrophe modeling if they agree to offer coverage in wildfire-prone areas. The strategy has garnered criticism from legislators and consumer groups, one of whom is suing Lara and the California Department of Insurance over a 2024 policy aimed at expediting insurance market recovery after an extreme disaster.

“Insurers are committed to helping Californians recover and rebuild from the devastating Southern California wildfires,” Denni Ritter, the American Property Casualty Insurance Association’s department vice president for state government relations, said in a statement about the suit. “Insurers have already paid tens of billions in claims and contributed more than $500 million to support the FAIR Plan’s solvency – even though they do not collect premiums from FAIR Plan policyholders.”

A call for collective action

Litigation prolongs – it does not alleviate – California’s risk crisis. Government has a crucial role to play in addressing it, from adopting smarter land-use planning regulations to investing in long-term resilience solutions.

For instance, Dixon Trail, a San Diego County subdivision dubbed the country’s first “wildfire resilient neighborhood,” models the Insurance Institute for Business & Home Safety (IBHS) standards for wildfire preparedness, but not at a cost attainable to most communities, and few local governments incentivize them. Launched by state legislature in 2019, the California Wildfire Mitigation Program is on track to retrofit some 2,000 houses along these guidelines, with the goal of solving how to fortify homes more quickly and inexpensively. Funded primarily by FEMA’s Hazard Mitigation Assistance Grant program, the pilot has thus far avoided the same cuts befalling FEMA’s sister programs under the Trump Administration.

Regardless of what legislators do, California homeowners’ insurance premiums will need to rise. The state’s current home and auto rates are below average as a percentage of median household income, reflecting a combination of the increased climate risk and of the regulatory limitations preventing insurers from setting actuarially sound rates. Insurance availability will not improve if these rates persist.

To quote Gabriel Sanchez, spokesperson for the state’s Department of Insurance: “Californians deserve a system that works – one where decisions are made openly, rates reflect real risk, and no one is left without options.” Insurers do not wield absolute control over that system, and neither do legislators, regulators, consumer advocates, or any other singular group. Confronting the root causes of these issues – i.e., the risks – rather than the symptoms is the only path towards systemic change.

Wildfire risk is strongly conditioned by geographic considerations that vary widely among and within states. The latest Triple-I Issues Brief shows how that fact played out in 2024 and early this year and discusses the importance of granular local data for underwriting and pricing insurance in wildfire-prone areas, as well as for much-needed investment in resilience.

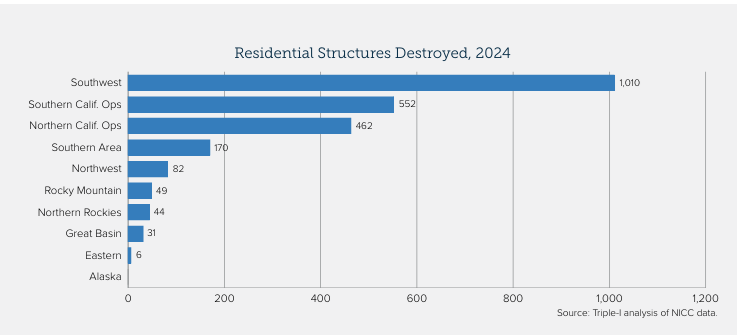

The 2024 wildfire season in the South and Southwest was particularly severe, marked by such events as the Texas and Oklahoma Panhandle fires in February and March and significant blazes in Arizona and New Mexico. The Southwest accounted for the largest number of residential structures destroyed by wildfire, and three of the top five areas for homes destroyed were in the South.

California accounted for the largest number of homes at risk for extreme wildfires. In the first half, the state experienced an above-average number of fires, though most were contained before growing to “major incident” size. Subsequent rains suppressed subsequent wildfire conditions – and caused substantial flooding.

But this rain contributed to an accumulation of fuels so that, when hurricane-force Santa Ana winds whipped through Los Angeles County in early January 2025, the conditions were right for fast-moving blazes to tear through Pacific Palisades and Eaton Canyon.

Temperature, humidity, wind, and topography vary too widely for a single “one size fits all” mitigation approach. This underscores the importance of granular data gathering and scrupulous analysis when underwriting and pricing insurance. It is also important that insurers proactively engage with diverse stakeholder groups to promote investment in mitigation and resilience.

A recent paper by Triple-I and Guidewire – a provider of software solutions to the insurance industry – uses case studies from three California areas with very different geographic and demographic characteristics to go deeper into how such tools can be used to identify properties with attractive risk properties, despite their location in wildfire-prone areas.

As high-severity natural catastrophes – wildfires, floods, hurricanes, and others – become more frequent and more people move into riskier locales, insurance affordability and availability have become a challenge in many states.

Insurers underwrite and price coverage based on the risks they’re assuming, and rising premiums in these states have pushed more homeowners into residual market mechanisms, such as state-backed insurance pools or agencies. Reliance on these funds – which often provide more limited coverage at higher costs – is not sustainable in the long term.

To ensure market stability and continued insurance availability and affordability, insurers must leverage more granular and dynamic risk models that account for real-time environmental conditions, mitigation measures, and property-specific characteristics. A new paper by Triple-I and Guidewire – a provider of software solutions to the insurance industry – uses case studies from three California areas with very different geographic and demographic characteristics to show how such tools can be used to identify properties with attractive risk properties, despite their location in wildfire-prone areas.

California’s risk profile

In addition to its particular risk characteristics, California’s insurance challenge is exacerbated by a 1988 measure – Proposition 103 – that has constrained insurers’ ability to profitably insure property in the state. In a dynamically evolving risk environment that includes earthquakes, drought, wildfire, landslides, and damaging floods, regulatory interpretation of Proposition 103 has made it hard for some insurers to offer coverage in the state.

In some cases, this has led to insurers limiting or reducing their business in the state. With fewer private insurance options available, more Californians are resorting to the state’s FAIR Plan, which offers less coverage for a higher premium. For many, this “insurer of last resort” has become the insurer of first resort. This isn’t a tenable situation for the state or its policyholders. California’s insurance availability/affordability challenges will require a multi-pronged approach, and underlying every component is the need for granular, high-quality, reliable data.

Modeling based on granular data

Guidewire’s analysis, based on its HazardHub Wildfire Score, has shown that wildfire mitigation and home hardening can reduce wildfire damage by as much as 70 percent. But identifying less risky lots in such areas is no easy task.

“Every property being assessed for wildfire risk is unique,” the report says. “Therefore, it’s important to subject as many relevant variables as possible to analysis. For example, proximity of structures to fuel is important – but, to be more predictive, it helps to know more: What kind of fuel? Is there potential for a wind-driven event? Is the property on a hill? If so, is it north-facing?”

Guidewire’s model includes standard variables, such as slope, aspect, wildfire history, wind, and the amount of nearby vegetation. It also includes differentiators like vegetation type and fire-suppression success rate.

“The traditional approach to wildfire risk assessment has left many Californians without access to affordable property insurance coverage,” said Triple-I Chief Insurance Officer Dale Porfilio. “Our research shows that with more detailed, property-level analysis, insurers can confidently offer coverage in areas previously deemed too risky.”

Important moves by California

California has taken steps to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing – most notably, the state’s Sustainable Insurance Strategy, an ambitious plan released by Insurance Commissioner Ricardo Lara in 2023 plan aimed at safeguarding the health of the insurance market while ensuring long-term sustainability. A key component of the plan is a requirement that insurers writing homeowners coverage in the state write no less than 85 percent of their statewide market share in areas identified by the commissioner as “under-marketed.”

Tightly focused, data-driven analysis using tools like the HazardHub Wildfire Score, can go a long way toward helping insurers meet those requirements by identifying less risky parcels in undermarketed areas.

“The Triple-I analysis highlights how next-generation tools and data can uncover lower-risk properties – even in high-risk areas – empowering insurers to expand coverage confidently and responsibly,” said Leo Tenenblat, Senior Vice President and General Manager, Data and Analytics at Guidewire.

Established by Congress through the Disaster Recovery Reform Act of 2018, the BRIC program has allocated more than $5 billion for investment in mitigation projects to reduce economic losses from floods, wildfires, and other disasters for hundreds of communities. Ending BRIC will cancel all applications from 2020-2023 and rescind more than $185 million in grants intended for Louisiana, leaving the 34 submitted and accepted projects funded by those grants in limbo.

Whereas the FEMA press release described BRIC as “wasteful and ineffective,” Cassidy identified “not doing the program and then having to rescue communities when the inevitable flood occurs – that is waste, because we could have prevented that from happening in the first place.”

A 2024 study backed by the U.S. Chamber of Commerce supports this claim, which found that disaster mitigation investments save $13 in benefits for every dollar spent.

FEMA’s decision coincides with recovery efforts in Natchitoches, a small Louisiana city, after flash flooding inundated homes and downed power lines just weeks before. BRIC was set to fund improvements to the city’s backup generator system to pump out floodwater during severe weather.

Similarly, Lafourche Parish will lose $20 million to strengthen 16 miles of power lines, which Cassidy noted toppled “like dominos” during last year’s Hurricane Francine. Jefferson Parish residents displaced following Hurricane Ida in 2021 will lose the home elevation disaster grants they finally secured earlier this year.

“Louisiana was the third-largest recipient of BRIC’s most recent round of funding and is the largest recipient on a per capita basis,” Cassidy said. “Without BRIC, none of these projects would be possible.”

A national problem

Beyond Louisiana, Cassidy pointed to numerous states ravaged by severe storms so far this year, particularly inland communities where flooding is traditionally unexpected. At least 25 people died amid a severe weather outbreak across the southern and midwestern U.S. last month, underscoring a growing need for resiliency planning in non-coastal areas.

BRIC is one of many programs facing sudden termination under the Trump Administration. Twenty-two states and the District of Columbia have filed a lawsuit demanding the federal government unfreeze essential funding, including BRIC grants. Though the administration is reportedly complying with a federal judge’s order blocking the freeze, the states involved claim funding remains inaccessible.

Louisiana has not joined the lawsuit, but Cassidy emphasized the congressional appropriation of the program and requested the fulfillment of preexisting BRIC applications. He argued that “to do anything other than use that money to fund flood mitigation projects is to thwart the will of Congress.”

As President Trump weighs disbanding FEMA entirely – even as FEMA responds to record-breaking numbers of billion-dollar disasters – it is imperative to recognize the vast co-beneficiary benefits of disaster resilience, and develop our partnerships across these stakeholder groups.

New, alarming financial risks for homebuyers who are unaware of property flood histories has driven several states to implement new disclosure laws, helping protect consumers from unexpected costs after purchasing flood-prone homes, according to new research from Milliman.

Atmospheric conditions are intensifying flood risks across the U.S., with severe storms and rain events becoming more devastating and frequent. Despite this escalating threat, a significant regulatory gap has persisted: many states haven’t required home sellers to disclose previous flooding to potential buyers.

This omission creates a dangerous scenario where unsuspecting homebuyers invest their savings in properties with undisclosed flood histories.

As Joel Scata, senior attorney in the climate adaptation division at the Natural Resources Defense Council (NRDC), explains, “If a buyer doesn’t know the house is flood-prone, they don’t know they need to buy flood insurance. They don’t know they need to mitigate that risk, and that they could be in a really bad situation when the next flood happens.”

The issue became impossible to ignore in 2018 when Hurricane Florence inundated more than 74,000 buildings in North Carolina. At that time, sellers weren’t required to inform buyers about previous flooding, meaning hurricane-damaged homes could be cleaned up and sold without disclosure of this critical history. Since properties that have flooded once are likely to flood again, this lack of transparency created significant financial vulnerability for new homeowners, according to Milliman.

Quantifying the Financial Impact

To drive policy change, NRDC needed hard data quantifying the financial risks to homebuyers. They partnered with Milliman, where Larry Baeder, a senior data scientist, co-authored a study titled, “Estimating undisclosed flood risk in real estate transactions.”

Using catastrophe models, proprietary datasets, real estate transaction data, historical flood events and demographic patterns, Baeder analyzed the impact in three states with low marks on NRDC’s Flood Risk Disclosure Laws Scorecard: North Carolina, New York and New Jersey.

The findings revealed staggering financial disparities. In North Carolina, a home without flood history might face an average annual loss (AAL) of about $60. In contrast, a flood-prone property’s AAL jumped to approximately $1,200 — 20 times higher — and could exceed $2,000 based on future flood projections. Over 15 years, previously flooded North Carolina properties might require more than $18,000 in repairs.

The numbers were even more concerning in the Northeast. In New York, flood history could increase a property’s AAL from about $100 to $3,000. A previously flooded New Jersey home might incur $25,000 in damages over a 15-year period.

“These are big numbers, and they’re a scary reality that people are going to have to deal with,” Baeder noted. “If a homebuyer is taking on this risk, they should be aware of the risk.” Milliman’s research also found that more than 6% of all homes sold across these three states in 2021 had a record of flooding—with no requirement to warn new owners about this history.

Data-Driven Legislative Change

Armed with Milliman’s analysis, NRDC approached lawmakers with compelling evidence of the problem’s scale and impact.

“Before the report, I think legislators knew that people struggled to rebuild after a flood,” Scata said, “but I don’t think they realized just how much it costs a homeowner. These numbers helped lawmakers see this was a big problem, that their constituents were suffering, and that they should do something about it.”

The data-driven approach proved effective. In 2023, New Jersey began legally requiring sellers to disclose a property’s flood history. North Carolina and New York soon followed, with New York enacting disclosure requirements at the end of 2023 and North Carolina amending mandatory forms in 2024.

The impact extended beyond these three states. Four additional states — Florida, Maine, New Hampshire and Vermont — independently adopted disclosure requirements in 2024 after recognizing the need demonstrated elsewhere.

“The laws show the power of data,” Scata noted. “Having Milliman do this work was really important for showing the actual impacts of flood damage on homeowners and effecting change through the legislatures.”

The momentum continues as Baeder now leads a follow-up study for NRDC expanding the research to 25 additional states with insufficient disclosure laws. Scata hopes to eventually see strong disclosure requirements nationwide, providing all homebuyers and renters with insight into their flood risk.

“If we’re going to tell people about lead-based paint,” Scata concludes, referring to other widespread real estate disclosures, “if we’re going to tell people about asbestos, we should probably tell people about flooding, because flooding has such an impact on someone’s finances and health.”

The Institutes’ Pete Miller and Francis Bouchard of Marsh McLennan discuss how AI is transforming property/casualty insurance as the industry attacks theclimate crisis.

“Climate” is not a popular word in Washington, D.C., today, so it would take a certain audacity to hold an event whose title prominently includes it in the heart of the U.S. Capitol.

For two days, expert panels at the Ronald Reagan Building and International Trade Center discussed climate-related risks – from flood, wind, and wildfire to extreme heat and cold – and the role of technology in mitigating and building resilience against them. Given the human and financial costs associated with climate risks, it was appropriate to see the property/casualty insurance industry strongly represented.

Peter Miller, CEO of The Institutes, was on hand to talk about the transformative power of AI for insurers, and Triple-I President and CEO Sean Kevelighan discussed – among other things – the collaborative work his organization and its insurance industry members are doing in partnership with governments, non-profits, and others to promote investment in climate resilience. Triple-I is an affiliate of the Institutes.

Sean Kevelighan of Triple-I and Denise Garth, Majesco’s chief strategy officer, discuss how to ensure equitable coverage against climate events.

You can get an idea of the scope and depth of these panels by looking at the agenda, which included titles like:

Building Climate-Resilient Futures: Innovations in Insurance, Finance, and Real Estate;

Fire, Flood, and Wind: Harnessing the Power of Advanced Data-Driven Technology for Climate Resilience;

The Role of Technology and Innovation to Advance Climate Resilience Across our Cities, States and Communities;

Pioneers of Parametric: Navigating Risks with Parametric Insurance Innovations;

Climate in the Crosshairs: How Reinsurers and Investors are Redefining Risk; and

Safeguarding Tomorrow: The Regulator’s Role in Climate Resilience.

As expected, the panels and “fireside chats” went deep into the role of technology; but the importance of partnership, collaboration, and investment across stakeholder groups was a dominant theme for all participants. Coming as the Trump Administration takes such steps as eliminating FEMA’s Building Resilient Infrastructure and Communities (BRIC) program; slashing budgets of federal entities like the National Oceanographic and Atmospheric Administration (NOAA) and the National Weather Service (NWS); and revoking FEMA funding for communities still recovering from last year’s devastation from Hurricane Helene, these discussions were, to say the least, timely.

Helge Joergensen, co-founder and CEO of 7Analytics, talks about using granular data to assess and address flood risk.

In addition to the panels, the event featured a series of “Shark Tank”-style presentations by Insurtechs that got to pitch their products and services to the audience of approximately 500 attendees. A Triple-I member – Norway-based 7Analytics, a provider of granular flood and landslide data – won the competition.

Earth Day 2025 is a good time to recognize organizations that are working hard and investing in climate-risk mitigation and resilience – and to recommit to these efforts for the coming years. What better place to do so than walking distance from both the White House and the Capitol?

The Trump Administration’s unwinding of the Building Resilient Infrastructure and Communities (BRIC) program and cancellation of all BRIC applications from fiscal years 2020-2023 reinforce the need for collaboration among state and local government and private-sector stakeholders in climate resilience investment.

Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters. FEMA announced on April 4 that it is ending BRIC .

Chad Berginnis, executive director of the Association of State Floodplain Managers (ASFPM), called the decision “beyond reckless.”

“Although ASFPM has had some qualms about how FEMA’s BRIC program was implemented, it was still a cornerstone of our nation’s hazard mitigation strategy, and the agency has worked to make improvements each year,” Berginnis said. “Eliminating it entirely — mid-award cycle, no less — defies common sense.”

While the FEMA press release called BRIC a “wasteful, politicized grant program,” Berginnis said investments in hazard mitigation programs “are the opposite of ‘wasteful.’ “ He pointed to a study by the National Institute of Building Sciences (NIBS) that showed flood hazard mitigation investments return up to $8 in benefits for every $1 spent.

“At this very moment, when states like Arkansas, Kentucky, and Tennessee are grappling with major flooding, the Administration’s decision to walk away from BRIC is hard to understand,” Berginnis said.

Heading into hurricane season

Especially hard hit will be catastrophe-prone Florida. Nearly $300 million in federal aid meant to help protect communities from flooding, hurricanes, and other natural disasters has been frozen since President Trump took office in January, according to an article in Government Technology.

The loss of BRIC funding leaves dozens of Florida projects in limbo, from a plan to raise roads in St. Augustine to a $150 million effort to strengthen canals in South Florida. According to Government Technology, the agency most impacted is the South Florida Water Management District, responsible for maintaining water quality, controlling the water supply, ecosystem restoration and flood control in a 16-county area that runs from Orlando south to the Keys.

“The district received only $6 million of its $150 million grant before the program was canceled,” the article said. “The money was intended to help build three structures on canals and basins in North Miami -Dade and Broward counties to improve flood mitigation.”

Florida’s Division of Emergency Management must return $36.9 million in BRIC money that was earmarked for management costs and technical assistance. Jacksonville will lose $24.9 million targeted to raise roads and make improvements to a water reclamation facility.

FEMA announced the decision to end BRIC the day after Colorado State University’s (CSU) Department of Atmospheric Science released a forecast projecting an above-average Atlantic hurricane season for 2025. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach CSU research team forecasts 17 named storms, nine hurricanes – four of them “major” (Category 3, 4, or 5). A typical season has 14 named storms, seven hurricanes – three of them major.

Nationwide impacts

More than $280 million in federal funding for flood protection and climate resilience projects across New York City — “including critical upgrades in Central Harlem, East Elmhurst, and the South Street Seaport” – is now at risk, according to an article in AMNY. The cuts affect over $325 million in pending projects statewide and another $56 million of projects where work has already begun.

Senate Majority Leader Chuck Schumer and Gov. Kathy Hochul warned that the move jeopardizes public safety as climate-driven disasters become more frequent and severe.

“In the last few years, New Yorkers have faced hurricanes, tornadoes, blizzards, wildfires, and even an earthquake – and FEMA assistance has been critical to help us rebuild,” Hochul said. “Cutting funding for communities across New York is short-sighted and a massive risk to public safety.”

According to the National Association of Counties, cancellation of BRIC funding has several implications for counties, including paused or canceled projects, budget and planning adjustments, and reduced capacity for long-term risk reduction.

North Dakota, for example, has 10 projects that were authorized for federal funding. Those dollars will now be rescinded. Impacted projects include $7.1 million for a water intake project in Washburn; $7.8 million for a regional wastewater treatment project in Lincoln; and $1.9 million for a wastewater lagoon project in Fessenden.

“This is devastating for our community,” said Tammy Roehrich, emergency manager for Wells County. “Two million dollars to a little community of 450 people is huge.”

The cancellation of BRIC roughly coincides with FEMA’s decision to deny North Carolina’s request to continue matching 100 percent of the state’s spending on Hurricane Helene recovery.

“The need in western North Carolina remains immense — people need debris removed, homes rebuilt, and roads restored,” said Gov. Josh Stein. “Six months later, the people of western North Carolina are working hard to get back on their feet; they need FEMA to help them get the job done.”

Resilience key to insurance availability

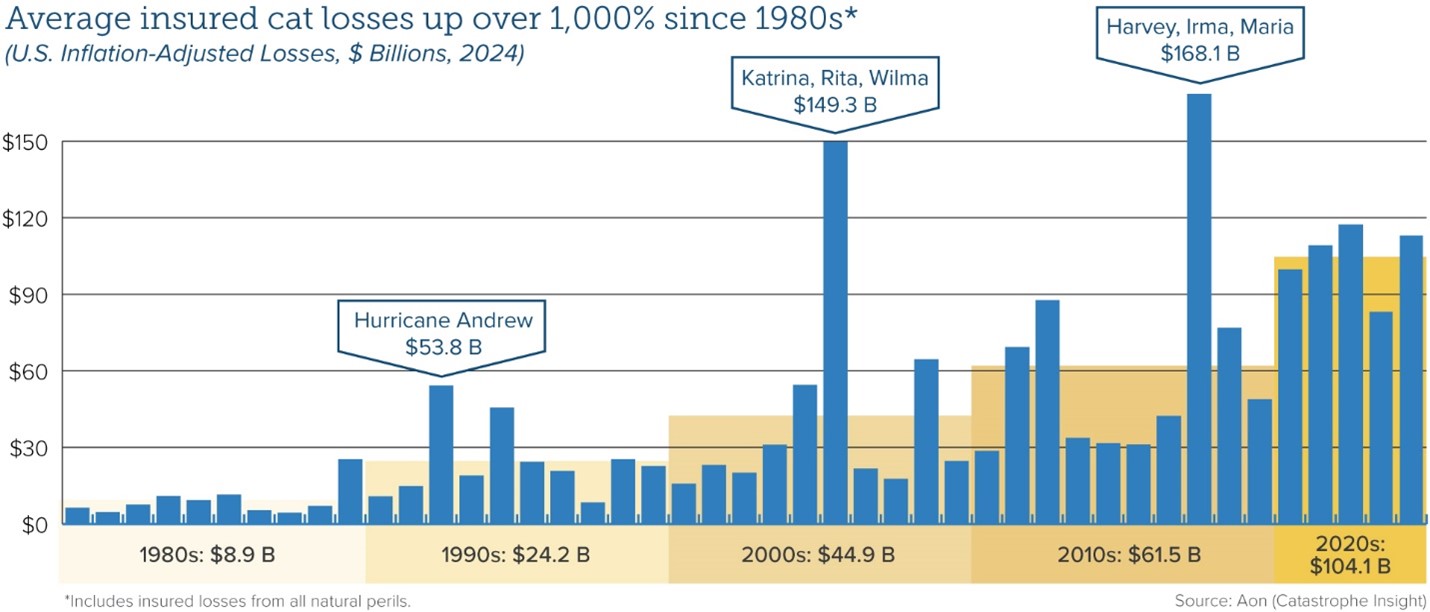

Average insured catastrophe losses have been on the rise for decades, reflecting a combination of climate-related factors and demographic trends as more people have moved into harm’s way.

“Investing in the resilience of homes, businesses, and communities is the most proactive strategy to reducing the damage caused by climate,” said Triple-I Chief Insurance Officer Dale Porfilio. “Defunding federal resilience grants will slow the essential investments being made by communities across the U.S.”

Flood is a particularly pressing problem, as 90 percent of natural disasters involve flooding, according to the National Flood Insurance Program (NFIP). The devastation wrought by Hurricane Helene in 2024 across a 500-mile swath of the U.S. Southeast – including Florida, Georgia, the Carolinas, Virginia, and Tennessee – highlighted the growing vulnerability of inland areas to flooding from both tropical and severe convective storms, as well as the scale of the flood-protection gap in non-coastal areas.

Coastal flooding in the U.S. now occurs three times more frequently than 30 years ago, and this acceleration shows no signs of slowing, according to recent research. By 2050, flood frequency is projected to increase tenfold compared to current levels, driven by rising sea levels that push tides and storm surges higher and further inland.

In addition to the movement of more people and property into harm’s way, climate-related risks are exacerbated by inflation (which drives up the cost of repairing and replacing damaged property); legal system abuse, (which delays claim settlements and drives up insurance premium rates); and antiquated regulations (like California’s Proposition 103) that discourage insurers from writing business in the states subject to them.

Thanks to the engagement and collaboration of a range of stakeholders, some of these factors in some states are being addressed. Others – for example, improved building and zoning codes that could help reduce losses and improve insurance affordability – have met persistent local resistance.

As frequently reported on this blog, the property/casualty insurance industry has been working hard with governments, communities, businesses, and others to address the causes of high costs and the insurance affordability and availability challenges that flow from them. Triple-I, its members, and partners are involved in several of these efforts, which we’ll be reporting on here as they progress.

Even as California moves to address regulatory obstacles to fair, actuarially sound insurance underwriting and pricing, the state’s risk profile continues to evolve in ways that impede progress, according to the most recent Triple-I Issues Brief.

Like many states, California has suffered greatly from climate-related natural catastrophe losses. Like some disaster-prone states, it also has experienced a decline in insurers’ appetite for covering its property/casualty risks.

But much of California’s problem is driven by regulators’ application of Proposition 103 – a decades-old measure that constrains insurers’ ability to profitably write business in the state. As applied, Proposition 103 has:

Kept insurers from pricing catastrophe risk prospectively using models, requiring them to price based on historical data alone;

Barred insurers from incorporating reinsurance costs into pricing; and

Allowed consumer advocacy groups to intervene in the rate-approval process, making it hard for insurers to respond quickly to changing market conditions and driving up administration costs.

As insurers have adjusted their risk appetite to reflect these constraints, more property owners have been pushed into the California FAIR plan – the state’s property insurer of last resort. As of December 2024, the FAIR plan’s exposure was $529 billion – a 15 percent increase since September 2024 (the prior fiscal year end) and a 217 percent increase since fiscal year end 2021. In 2025, that exposure will increase further as FAIR begins offering higher commercial coverage for larger homeowners, condominium associations, homebuilders and other businesses.

Insurance Commissioner Ricardo Lara has implemented a Sustainable Insurance Strategy to alleviate these pressures. The strategy has generated positive impacts, but it continues to meet resistance from legislators and consumer groups. And, regardless of what regulators or legislators do, California homeowners’ insurance premiums will need to rise.

The Triple-I brief points out that – despite the Golden State’s many challenges – its homeowners actually enjoy below-average home and auto insurance rates as a percentage of median income. Insurance availability ultimately depends on insurers being able to charge rates that adequately reflect the full impact of increasing climate risk in the state. In a disaster-prone state like California, these artificially low premium rates are not sustainable.

“Higher rates and reduced regulatory restrictions will allow more carriers to expand their underwriting appetite, relieving the availability crisis and reliance on the FAIR plan,” said Triple-I Chief Insurance Officer Dale Porfilio.

With events like January’s devastating fires, frequent “atmospheric rivers” that bring floods and mudslides, and the ever-present threat of earthquakes – alongside the many more mundane perils California shares with its 49 sister states – premium rates that adequately reflect the full impact of these risks are essential to continued availability of private insurance.