By Lewis Nibbelin, Contributing Writer, Triple-I

The Georgia Senate recently approved legislation aimed at curbing the state’s soaring litigation. Backed by Georgia Gov. Brian Kemp, Senate Bill 68 is designed to facilitate more equitable courtroom outcomes and stabilize insurance rates.

Among other provisions, the bill includes a cap on pain and suffering evidence that would reduce premises liability lawsuits, or those against owners for injuries and/or criminal conduct that occurred on their property. It also would restrict “phantom damages,” meaning plaintiffs could seek damages only in the amount actually paid for medical bills, rather than an inflated amount determined by a healthcare provider’s list prices.

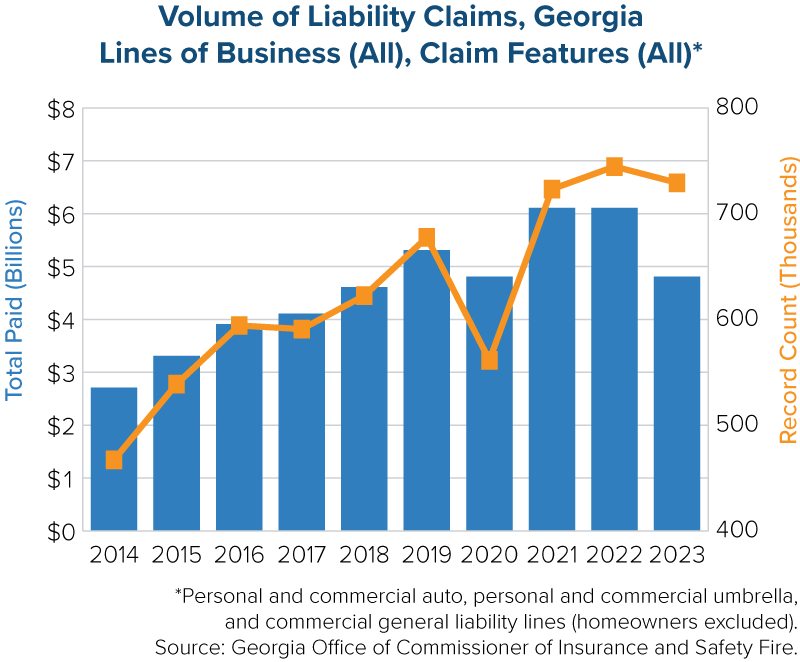

Both practices have generated nuclear verdicts (awards of $10 million or more) in Georgia, contributing to the fourth-most nuclear verdicts in personal injury litigation per capita of any state from 2013 to 2022.

Another bill – SB 69 – targets third-party litigation funding, in which investors anonymously finance litigation and often delay prompt settlement in exchange for a share of larger damage awards, thereby driving up claims costs. If enacted, the bill would limit their influence over legal decisions and require third parties to register with the Department of Banking and Finance, effectively banning foreign adversaries from funding litigation.

Much of the legislation is based on a report from the office of Georgia Insurance and Safety Fire Commissioner John F. King, which revealed a steady increase in liability claims frequency and identified growing legal involvement in claims as a key driver of insurance rates.

“Georgia’s legal climate amounts to a hidden tax on families and small businesses, driving up costs and threatening our long-term future,” King said in a recent press conference, explaining that tort reform can “level the playing field in our courtrooms and help ensure Georgia’s long-term prosperity and security.”

Economic impact on Georgia

Georgia loses over 137,000 jobs annually due to excessive litigation, which further imposes an estimated $1,415 “tort tax” on each resident per year, earning the state a recurring spot on the American Tort Reform Foundation’s annual list of “judicial hellholes.” With litigation for personal auto claims at a rate more than twice that of the median state, Georgia also ranks among the least affordable states for personal auto insurance, according to research by the Insurance Research Council (IRC) – an affiliate of The Institutes, like Triple-I.

To bolster stakeholder education on the economic impacts of legal system abuse, Triple-I recently expanded its comprehensive awareness campaign in Georgia. The campaign now encompasses multiple brick-and-mortar interstate billboards in Downtown Atlanta, along with digital bus shelter billboards across the Metro Atlanta area. All billboards promote Triple-I’s microsite encouraging consumer support for reform in the state.

Though hundreds – including doctors and business owners – have galvanized behind the reforms, neither bill is without controversy. Opponents argue such legislation may not improve insurance rates and could overcorrect to favor insurance companies at the expense of policyholders.

Following reforms in 2022 and 2023, however, Florida welcomed flat or decreased insurance rates last year, as the state’s insurance market began to recover from its former status as the “poster child” for legal system abuse. Substantial rate reductions have continued into 2025, particularly for three major auto insurance carriers, according to Florida Gov. Ron Desantis’ announcement earlier this month.

While the specific policy levers may differ, Florida’s success models the potential benefits of similar legislation in other areas. Certainly, understanding and mitigating these trends is crucial to restoring Georgia’s economy.

Learn More:

New Triple-I Issue Brief Puts the Spotlight on Georgia’s Insurance Affordability Crisis

How Georgia Might Learn From Florida Reforms

Triple-I launches Campaign to Highlight Challenges to Insurance Affordability in Georgia

Georgia Is Among the Least Affordable States for Auto Insurance

{kind=link}