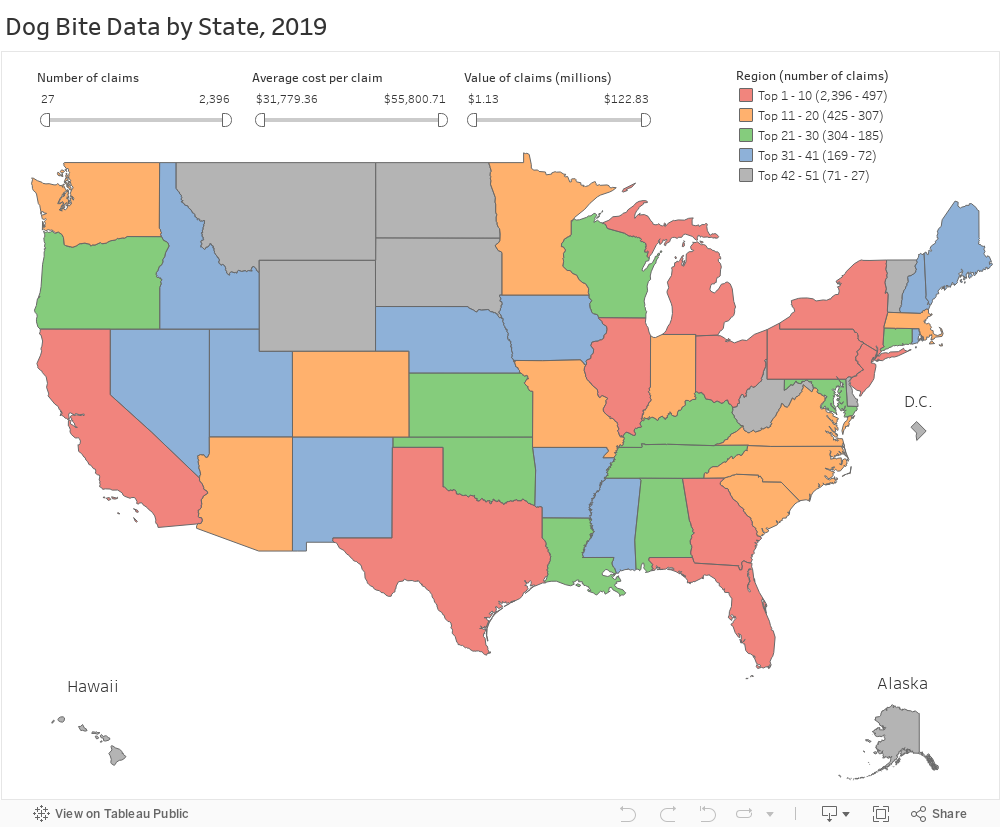

Our previous post discussed homeowners liability claims stemming from dog bites. Today, Janet Ruiz, I.I.I.’s Director of Strategic Communications, has these valuable safety tips from National Dog Bite Prevention

Week ® Coalition partners.

The American Veterinary Medical Association (AVMA) estimates there are approximately 78 million dogs in U.S. homes and each year 4.5 million people are bitten or injured. “Even the gentlest dog can bite if they are in pain, feel threatened, or are competing for resources such as food or space,” said Dr. John de Jong, AVMA President. “Not only is it important to understand how dogs behave, it is important to understand how a dog may interpret our behavior.” AVMA’s ‘Jimmy the Dog’ video series lets preschoolers look at how a dog might interpret different scenarios.

“We’ve seen firsthand over the years the tragic consequences surrounding dog bites and their effect on those involved – the people who are injured, the animals who may be relinquished or even destroyed, and the dog’s owners who have to cope with the loss of a beloved family member,” said Lesa Staubus, DVM, American Humane Rescue veterinarian, “Once your dog has bitten someone – or you or a family member fall victim to a dog bite – it will be already be too late. Let’s practice good prevention instead.”

Because of the high-risk involving dogs, babies, and children, American Humane offers a free online booklet called Pet Meets Baby that provides families with valuable information on introducing a new child to a home with a dog.

Additional safety tips from American Humane include:

- NEVER leave a baby or small child alone with a dog, even if it is a family pet. Children are often bitten by dogs in their own household.

- Make sure your pet is socialized so it feels at ease around people and other animals.

- Walk and exercise your dog on a leash to keep it healthy and provide mental stimulation.

- Regular veterinary visits are essential to regulating the health of your dog. A sick or injured dog is more likely to bite.

- Be alert. If someone approaches you and your dog, caution them to wait before petting the dog. Give your pet time to be comfortable with the stranger.

- Understand and respond to changes in your dogs’ body language. Look at the eyes, ears, tail, and posture to know when your dog may be happy, fearful, or angry.