Technology trends – particularly the rise of artificial intelligence – have become the top priority for global insurance executives in 2025, according to the International Insurance Society (IIS) Global Priorities Survey.

IIS – like Triple-I, an affiliate of The Institutes – found that AI has overtaken inflation as the top priority of respondents, with two-thirds now ranking AI as their leading focus for technology and innovation. Executives cite AI’s potential to streamline operations, enhance analytics, and drive new product innovation, while inflation and climate risk remain significant concerns. Operational efficiency and cybersecurity remain high on the priority list, but the narrowing gap between climate risk and technological advancement highlights the growing influence of digital priorities.

Nearly 20,000 insurance executives worldwide participated in the 2025 survey.

“These tools enhance forecasting capabilities by allowing for deeper insights into trends and potential future risks,” on executive said, characterizing the bottom-line impact of AI. “By empowering themselves with robust analytics, organizations can improve their strategic planning and risk management efforts, ultimately driving better business outcomes.”

Beyond AI, insurance executives’ emphasis on technology generally has continued to grow. Forty-one percent of respondents now view technological advancement as a top social and environmental priority, continuing its rise from only 12 percent in 2021. This increased focus reflects a desire to harness innovations ranging from machine learning tools to sophisticated cybersecurity solutions.

Other challenges also remain top-of-mind. Inflation is the highest economic priority for the fourth consecutive year, with 63 percent of respondents citing it among their top three issues. Climate risk also continues to top the social and environmental category. Concerns over an aging workforce have almost doubled year-over-year but, generally speaking, employment issues – such as workforce readiness, workforce structure, DEI, and employee health and safety – remain lower priority issues, according to the survey.

Tying a fire-prevention IoT device to the distribution networks of major insurers may have cracked the code for modifying human behavior toward risk prediction and prevention, says the CEO of Whisker Labs, the producer of Ting.

Ting helps protect homes from electrical fires by using AI to detect arcing – the precursor to most electrical fires. Once connected to an outlet, Ting analyzes 30 million measurements per second to detect tiny electrical anomalies and power-quality problems. On average, Ting detects and mitigates fire hazards in 1 out of every 60 homes it protects.

Whisker Labs works with a growing community of insurers who provide Ting to their customers for free. More than one million Tings are deployed in the United States, and approximately 50,000 are installed each month. In his second appearance on Triple-I’s Executive Exchange video series in two years, Whisker Labs founder and CEO Bob Marshall reported to Triple-I CEO Sean Kevelighan on the product’s results to date.

“One of the cool things we’ve learned over the last couple of years is that insurers have found that Ting is like the gateway drug,” Marshall said. “I mean, if you actually get Ting into your customer’s home and we deliver a great experience to them, they’re much more willing to engage in water-loss prevention after that. So, it’s really critical that the homeowners engage.”

Ease of use has been critical to Ting’s success, Marshall said, pointing out that earlier attempts at similar products were “too complicated for the customer, too complicated for the carrier, and that’s why they didn’t work. With Ting, you just plug it in and it does its thing.”

Recent research demonstrated the efficacy and value provided by Ting. In partnership with Triple-I and Octagram Analytics, Whisker Labs found that Ting resulted in 0.39 fewer electrical fire claims per 1,000 home years of experience, translating to a fire claims reduction benefit of $81 per customer per year by the third year after installation. As Whisker Labs works with its growing community of insurers to extend Ting’s reach, Marshall believes these figures could improve even further.

“What we see in that study is that the claims frequency drops dramatically in the days, weeks, and months after you plug in Ting,” Marshall said, noting that the source for this finding “is not our data – it’s data from all the carriers that we work with.”

Kevelighan agreed that “from a carrier perspective, getting more of these into the community will make the community more resilient and more insurable,” particularly within dense neighborhoods and cities where fires can spread quickly. Such settings highlight the collective responsibility of risk mitigation on consumers as well as insurers, who play a key role in disseminating prevention solutions, Kevelighan stressed.

Though more public education surrounding IoT is needed, Marshall noted that homeowners familiar with Ting’s success are often receptive to additional IoT solutions for other risks, potentially sending ripple effects of risk mitigation throughout the industry. His firm and their research collaborators aim for similar versatility with the Ting study, whose methodology has broad applicability for many types of prevention solutions.

“‘Predict and prevent’ – that’s a vision that, I think, rings true for everybody,” Marshall concluded, because “the best claim is the one that never happens. We just want to be a key part of it and help drive it.”

Economic shifts, geopolitical uncertainties, cybersecurity trends, and mounting climate perils have created an increasingly severe and interconnected risk crisis, according to participants in a members-only Triple-I webinar.

In an environment constrained, for instance, by frequent natural disasters and rising replacement costs, risks no longer develop in isolation. They collide with and compound each other. Their combined impact exceeds the sum of individual risks’ effects. Such interdependence complicates identifying, let alone mitigating, the forces underpinning a specific risk.

“Under this new system that’s emerging, risk can propagate very rapidly through a host of otherwise disconnected networks,” TradeSecure president and cofounder Scott Jones told webinar host Michel Léonard, Triple-I’s Chief Economist and Data Scientist. “This new reality fundamentally challenges the core principles that insurance has relied on for centuries.”

Jones emphasized the growing unpredictability of risk on a global scale, particularly as nations impose export controls, sanctions, investment restrictions, and tariffs for purposes like economic competition. Companies with global footprints may struggle to ascertain these interwoven, sometimes competing regulations, creating compliance concerns and potentially exacerbating supply-chain disruptions.

With the frequency and severity of U.S. cyber claims on the rise, cyberattacks also carry substantial transnational implications. Sophisticated ransomware encounters can exploit businesses of all sizes, propelling privacy liability claims and related third-party litigation.

TradeSecure vice president and cofounder Michael Beck explained how the almost universal accessibility of malware – harnessed by criminal syndicates, activist groups, or even lone hackers – presents “a new class of systemic non-physical disruption” that could undermine “the entire system’s liquidity and stability.”

“A coordinated non-state cyberattack wouldn’t just steal money – it could stop the flow of money, causing many transaction failures and possibly triggering a wave of claims far beyond what traditional cyber policies are designed to handle,” Beck said.

Though insurers as well as business owners and consumers consider cyber incidents a chief risk concern, personal cyber take-up rates remain low, with the broader cyber insurance market facing its third consecutive year of declining rates. Misunderstandings surrounding cyber risk and benefits of coverage fuel this discrepancy, revealing a gap between agent perceptions of product value and that of their customers.

With home repair and remodeling costs rising 61 percent over the past decade, many homeowners are delaying or forgoing routine maintenance for older homes. In a recent Executive Exchange discussion with Triple-I CEO Sean Kevelighan, PreFix founder and CEO James Bilodeau discussed how his Texas-based company can help insurers promote such maintenance to mitigate more expensive losses down the line.

PreFix pairs clients with individual repair technicians to deliver personalized, year-round home repair, including two annual maintenance visits for filter replacements and comprehensive home inspections, Bilodeau said.

For maintenance visits, Bilodeau explained, PreFix will “clean your AC condenser and condensate line; change your air and water filters; flush the sediment out of your water heater; clean the lint out of your dryer outtake; sanitize your washer and dishwasher with a natural cleansing agent; and change all the batteries in your smoke alarms,” among other tasks.

The firm also modifies its services based on insurer preferences and the specific risk profile of homes in a given area.

“We’re able to offer highly granular customized data collection on all of the homes that we service through direct observation of issues that can correlate to non-cat losses,” Bilodeau said, noting identification of corroded water valves, overhanging tree branches, and unsecured exterior doors can facilitate “resolution quickly, before extensive damage happens.”

By continuously monitoring and mitigating these risks, Bilodeau believes his firm can help lower underwriting costs and premiums, as well as support smart home telematics adoption and catastrophe risk modeling.

“While aggregation is useful – which is what many providers do – many of the component inputs like home inspection data degrade quickly over two to five years,” Bilodeau said. “Inaccuracy can then be exacerbated when the data is extrapolated to other homes using inference.”

Kevelighan added that initial inspections as part of the home buying process often overlook or fail to communicate the true risks a property faces, leaving homeowners unaware of risks until catastrophe strikes.

“If you can enter risk management into the process of home purchasing much sooner and help the customer understand what they are purchasing beyond the four walls of their house and the community that it’s in, that could very much create a win-win for the insurer and the customer,” Kevelighan said.

Kevelighan and Bilodeau agreed that removing friction from home maintenance is imperative not only to better accommodate consumers, but to facilitate the insurance industry’s shift beyond repairing and replacing damaged property to predicting and preventing damage to begin with. Solutions like PreFix highlight how proactive loss mitigation necessarily involves engages all affected parties that have a stake in mitigation and resilience.

Among homeowners surveyed by the Insurance Research Council (IRC), 88 percent recognize that aerial imagery is a beneficial tool for insurers.

Nearly all respondents said they recognize the value of using satellite, drone, and aircraft images for early problem detection, claims processing, and hazard identification before costly damage occurs. Most also said they believe aerial imaging can lead to fairer pricing.

Key findings:

Nine out of 10 respondents said they see at least one benefit from aerial imagery’s use in insurance. More than half said it leads to fairer insurance pricing.

While 60 percent have some awareness that insurers use aerial imagery, 40 percent know little or nothing about it.

When homeowners are familiar with the use of aerial imagery for underwriting, they are nearly twice as likely to think it makes insurance pricing fairer.

Homeowners worry more about accuracy than privacy in the context of aerial imagery. Accuracy emerges as the top individual concern, with 31 percent citing it as their biggest worry, compared to 24 percent who cite privacy as their primary concern.

Education and transparency are key to acceptance of this technology, the survey found. Homeowners who were already familiar with aerial imagery applications were found to show consistently higher confidence levels, greater benefit recognition, and more positive sentiment across all insurance uses. Younger homeowners also demonstrated greater acceptance and higher confidence in the technology’s accuracy.

“Consumers see value in aerial imagery when they understand how it’s used in insurance,” said IRC President Pat Schmid. “Efforts to increase transparency and consumer knowledge can bridge the confidence gap, improve customer trust, and help homeowners realize the benefits of faster claims, fairer pricing, and better risk prevention.”

The IRC, like Triple-I, is an affiliate of The Institutes.

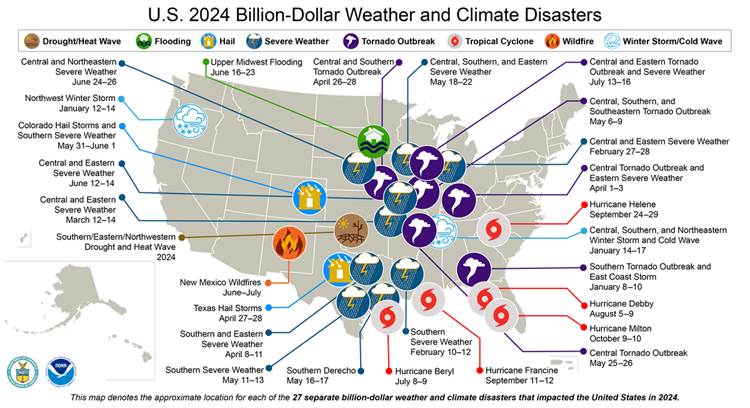

A climate nonprofit plans to revive a key federal database tracking billion-dollar weather and climate disasters that the Trump Administration stopped updating in May, Bloomberg reported.

The database captures the financial toll of increasingly intense weather events and was used by insurers and others to understand, model, and predict weather perils across the United States. Dr. Adam B. Smith, the former NOAA climatologist who spearheaded the database for more than a decade, has been hired to manage it for the nonprofit, Climate Central.

NOAA in May announced it would stop tracking the cost of the country’s most expensive disasters, those which cause at least $1 billion in damage – a move that would leave insurers, researchers, and government policymakers with less reliable information to help understand the patterns of major disasters like hurricanes, drought or wildfires, and their economic consequences.

Climate Central plans to expand beyond the database’s original scope by tracking disasters as small as $100 million and calculating losses from individual wildfires, rather than simply reporting seasonal regional totals.

A record 28 billion-dollar disasters hit the United States in 2023, including a drought that caused $14.8 billion in damages. In 2024, 27 incidents of that scale occurred. Since 1980, an average of nine such events have struck in the United States annually.

This summer – amid deadly wildfires and floods – the Trump Administration has appeared to be rolling back some of its DOGE-driven NOAA funding cuts. NOAA recently announced that it would be hiring 450 meteorologists, hydrologists, and radar technicians for the National Weather Service (NWS), after having terminated over 550 such positions in the already-understaffed agency in the spring.

In addition, the administration’s announced termination of the Building Resilient Infrastructure and Communities (BRIC) program — run by the Federal Emergency Management Agency (FEMA) — has been held up by a court injunction while legislators debate its future. Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters.

Regarding the rescue of the NOAA dataset, Colorado State University researcher and Triple-I non-resident scholar Dr. Phil Klotzbach said, “The billion-dollar disaster dataset is important for those of us working to better understand the impacts of tropical cyclones. It uses a consistent methodology to estimate damage caused by natural disasters from 1980 to the present and was a critical input to our papers investigating the relationship between landfalling wind, pressure and damage. I’m very happy to hear that this dataset will continue!”

Parents are increasingly open to using technology to keep their teen drivers safe on the road, a recent survey from Nationwide finds.

The survey found 4 out of 5 parents would enroll their teens in telematics programs that reward safe driving. This enthusiasm for tech-based solutions comes despite mixed parental assessments of their teens’ driving abilities: While 42 percent rate their teen’s driving as “good” or “excellent”, similar percentages express concerns about distracted driving and reckless behavior.

“Parents want to feel confident that their teens are making smart choices behind the wheel,” says Casey Kempton, Nationwide president of P&C personal lines. “These tools help make that possible—not just by monitoring behavior, but by encouraging better habits through positive reinforcement.”

Despite recognizing the value of safety technology, adoption remains limited. While 96 percent of parents said they believe dashcams provide valuable evidence after accidents, only 26 percent of teen drivers actually have them installed.

The survey reveals a broader trend in which consumers are drawn to telematics and monitoring technologies, though motivations vary. While parents prioritize safety benefits, many consumers are equally interested in the insurance premium discounts these programs can provide.

“This isn’t just about technology,” Kempton says. “It’s about creating a culture of accountability and shared responsibility on the road.”

As comfort with AI-enabled monitoring grows, it appears that families are embracing a future in which technology supports — but does not replace — good judgment.

As property/casualty insurers increase their focus on predicting and preventing costly damage that drives up claims and premiums, telematics technology has come to play an increasing role. From video doorbells that reduce theft and vandalism to “smart plumbing” solutions that detect leaks and shut off water before in-home flooding can occur, these technologies clearly offer value to homeowners and insurers.

But how much value?

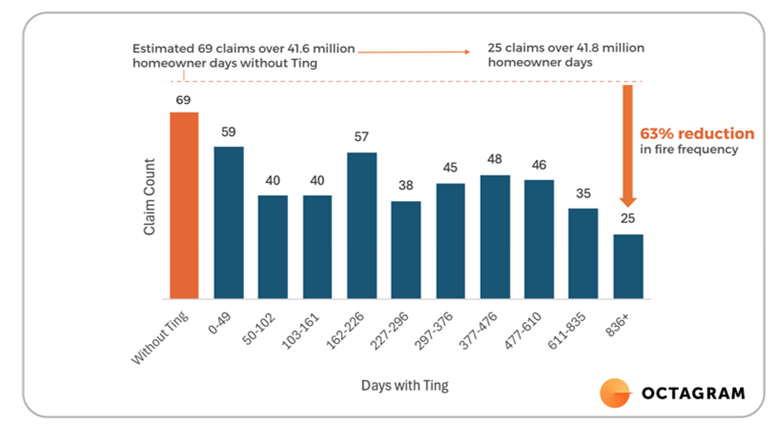

Whisker Labs – maker of the Ting home fire prevention solution – has taken on the challenge of quantifying its product’s efficacy and return on investment. In a research partnership with Octagram Analytics for independent data analysis and modeling and Triple-I for its insurance industry expertise and insight, Whisker Labs found that Ting reduced fire claims within the study sample by an estimated 63 percent, resulting in 0.39 fewer electrical fire claims per 1,000 home years of experience, in the third year after installation. This translates into a fire claims reduction benefit of $81 per customer.

“This study provides concrete evidence of the value that telematics technology can deliver,” said Patrick Schmid, chief insurance officer at Triple-I. “While IoT solutions are gaining traction with many success stories, rigorous analysis of claims reduction has been harder to find until now. This analysis clearly shows Ting reduces claims and provides a positive return on investment for insurers.”

Ting helps protect homes from electrical fires by using advanced AI to detect arcing, the precursor to most electrical fires. Once connected to a single outlet, Ting analyzes 30 million measurements per second, analyzing voltage at high frequencies to detect tiny electrical anomalies and power quality problems. These hazards can originate from wiring in the home, connected devices and appliances, or even the power coming in from the utility. On average, Ting detects and mitigates fire hazards in 1 out of every 60 homes it protects.

“Ting is about saving lives and homes – that’s always been our mission,” said Bob Marshall, CEO and cofounder of Whisker Labs. “By analyzing verified claims data over time, this analysis shows that what’s best for families also delivers a strong financial return for insurers. Prevention is better for everyone.”

Whisker Labs works with a growing community of 30 insurers who provide Ting to their customers for free. More than one million Tings are deployed in the United States, and approximately 50,000 new Tings are installed each month.

In addition to monitoring voltage and features of voltage at high frequencies to detect arcing that is indicative of fire hazards, Ting has a temperature sensor that monitors the temperature within the home.

“When the temperature drops below 42 degrees, an alert is issued,” Marshall said. “Thus, Ting detects and warns about conditions that can result in frozen and burst pipes and alerts the homeowner to correct the situation before damage occurs. Over the past three years, we have issued low-temperature warnings to about 1 in 560 customers per year.”

Measuring the value

Like Ting, other peril-based IoT solutions issue alerts and warnings when a hazard is detected. Thousands of hazards are detected and alerts sent, but how do you know that this reduces claims? How do you estimate the return on investment for these devices? How can you prove that the bad thing, a loss and a claim, didn’t occur?

“We developed a methodology to do this in the real world with existing customers and experience data,” said Whisker Labs Chief Scientist Stan Heckman.

Whisker Labs and Octagram had to overcome challenges related to limited data and sampling bias. To address these, a self-controlled study was developed that assesses claims over time in homes with Ting in place. (See paper for a fuller explanation of the methodology).

The chart below shows how the number of fire claims in Ting-equipped homes declines over time. The claims frequencies observed and associated percent reduction in claims are highly dependent on the definition of the sample of non-cat fire claims provided by carriers that participated in the analysis. However, this does not affect the observed absolute reduction.

Using data from Triple-I and Verisk, Whisker Labs determined that Ting provides a loss-prevention benefit of $81 per home per year. (See paper for details).

“Add in benefits associated with reduction in water-related losses from frozen pipes and failing sump pumps and water heaters,” and the benefits are likely substantially higher, Marshall said. Insurers who provide Ting to their policyholders also may enjoy improvements in customer retention.

Analysis based on granular, cutting-edge data is essential to staying ahead in our rapidly shifting risk landscape. During Triple-I’s Joint Industry Forum in Chicago, two “Risk Take” presenters dove deep into the innovative data initiatives they engaged in to help turn these challenges into new opportunities for insurers.

Balancing consumer needs

With natural catastrophe frequency and supply chain uncertainty on the rise, so are home maintenance costs. Estimated to exceed $10,000 annually in 2024 – at a 5.9 percent year-over-year increase – home maintenance further weighs against the mounting costs of premium rates and property taxes across the U.S., leading many homeowners to forgo investing in at-home risk mitigation like smart home telematics.

“Across the providers we’ve talked to, adoption of telematics falls somewhere between the single digits,” said presenter James Bilodeau, CEO and founder of PreFix Inc. “The reason is simple: the value proposition of what we would like homeowners to do isn’t important enough compared to what homeowners actually need.”

For Bilodeau, the solution is also simple: combine advanced technology with routine preventative maintenance. By providing personalized, year-round home repair, Bilodeau’s Texas-based firm aims to mitigate losses while gathering unique primary data on the properties they service. Insurers can use this data to develop telematics technology and more accurately price the associated risks.

Such data collection “creates a flywheel in which we help our partners delight their customers with exceptional service and hit directly at affordability issues, both with home maintenance and in premium reduction,” Bilodeau said.

After a successful pilot program, USAA expanded its partnership with the company to offer discounted maintenance services to members who sign up for PreFix. Noting that the company is pursuing partnerships with other major insurers, Bilodeau highlighted that industry collaboration is crucial to not only facilitate more refined coverage but to lower the cost of entry to enhancing resilience.

Emerging public safety risks

An eightfold increase in New York City fire incidents between 2019 and 2023 correlates strongly with the growing popularity of e-mobility devices, according to a joint report by UL Standards & Engagement (ULSE) and Oxford Economics that is based in part on Triple-I data.

Presenting on the report, ULSE Director of Insights Sayon Deb explained how lithium-ion battery fires linked to e-bikes and scooters became a mainstream risk for COVID-era urban environments, due in part to the booming online food and grocery delivery market.

“Nearly $519 million worth of damages were caused in just four years from structural property damage, injuries, and loss of life,” Deb said, pointing out that this figure does not account for “the additional cost of communal fear, in terms of fires happening across the hallway from you, and also the loss in economic opportunities and the community toll that it takes as we respond to these fires.”

Inadequate public safety awareness, paired with the easy availability of uncertified devices, helped fuel the crisis. Beyond overusing or incorrectly charging the devices, e-mobility users often left them in dangerous locations, with “66 percent of those who charge at home charging their devices near their exit,” Deb explained – effectively “blocking your exit from your home in the event of a fire.”

E-mobility regulations vary wildly by state. Though New York City regulations passed in 2023 show progress, ULSE recommends more proactive public outreach, safety standard enforcement, and incident reporting to better track e-mobility risk data.

“The better the data we collect, the better we can understand where, how, and why these battery fires occur, so that we can prevent future fires from happening,” Deb concluded.

Global economic uncertainty emerging from recent U.S. policy actions was a major concern for thought leaders on the “Economics, Underwriting, and Geopolitics” panel at Triple-I’s Joint Industry Forum in Chicago.

Despite recently posting its most favorable underwriting performance since 2013, the property/casualty insurance industry faces several obstacles to continued progress, particularly from tariffs issued by the Trump Administration.

Short-term economic impacts

“Tariffs aren’t inherently good or bad,” said Triple-I Chief Economist and Data Scientist Dr. Michel Léonard, who co-moderated the discussion. “Where there is consensus among economists is that, in the short term, tariffs do lead to inflation and disruption.”

Put simply, tariffs can raise revenue for the issuing government while costing the domestic businesses that rely on imported goods. In advance of pending tariffs, companies up and down the supply chain are purchasing such goods at a record pace, which boosts the demand and prices of these materials. Consumers will inevitably shoulder some or all of the added cost.

Many proposed or enacted tariffs involve materials essential to construction and auto manufacturing. Earlier this month, for instance, the administration doubled its new steel and aluminum tariff to 50 percent – including on Canada, the largest steel supplier to the United States. P/C replacement costs will likely rise throughout the industry, leading to higher claim payouts and, consequently, premium rates.

Amid various tariff reductions, increases, impositions, and pauses, President Trump’s trade policies remain difficult to determine or predict. This lingering ambiguity – paired with impending replacement cost increases – creates a “double whammy” for insurers, said Aaron Klein, Miriam K. Carliner Chair and senior fellow in Economic Studies at the Brookings Institution.

“Other markets can adapt to that more quickly,” Klein said. “When I renew my auto policy in February, the insurer on the other side has to guess what the costs are going to be over six months.”

While in a period of extraordinary performance, the workers compensation line also faces potential risks from oncoming tariffs, noted Donna Glenn, chief actuary at the National Council on Compensation Insurance (NCCI). Mitigated by investments in technology and safety, workplace incidents could rise, she explained, as “a lot of the uncertainty puts businesses back in a defensive mode and asking, ‘how should I spend my money?’”

“I caution and say there will be some temporary lack of investment in safety,” Glenn continued.

Talent and technology

An evolving workforce poses additional risks.

“Workers comp has benefited from a very strong labor market,” Glenn said, pointing to consistently low U.S. unemployment rates, but current mass deportation efforts could undermine this trend. “We are accustomed to having a significant influx of foreign-born workers,” Glenn explained. “When we don’t – and when we shift to not having them – the labor market could stifle to some degree.”

Bridging the talent gap lends further urgency to this issue, as roughly 400,000 workers are projected to leave the insurance industry through attrition by 2026 in the U.S. alone, according to the U.S. Bureau of Labor Statistics. And with generative AI automating more processes across the insurance value chain, cultivating a workforce possessing the necessary skillset to oversee them compounds the problem.

“AI can certainly help improve productivity,” said Triple-I Chief Insurance Officer and co-moderator Dale Porfilio, “but we’re going to need people to do an awful lot of those jobs. We’re still going to have that talent gap.”

Embracing advanced technology, then, gives insurers an opportunity to both develop that expertise and rebuild the workforce by attracting younger tech professionals who might otherwise overlook the industry. Innovative companies like Argo Group are already paving the way for this collaboration.

Patrick Schmid, president of The Institutes’ RiskStream Collaborative, acknowledged that “getting clarity about how significantly you can leverage AI is very important.”

Concern about using AI in underwriting, Schmid said, given an absence of AI regulatory guidance, which does not exist federally and is set to be blocked on a state level.

To provide insight into these efficiencies, Schmid described how RiskStream – a consortium of insurers, brokers, reinsurers, and other industry leaders – applies AI to streamline data processing, lower operating costs, and enhance customer experiences. Beyond expediting business operations, AI offers potential solutions to a range of challenges plaguing insurers, Schmid said – including one application that might help mitigate legal system abuse by facilitating earlier claims intervention, preventing excessive attorney involvement.

The panelists agreed that insurers will continue to adapt their underwriting and pricing to reflect this dynamic environment and emphasized the economy’s strong, steady recovery post-COVID.

“There’s not been a single case of an economic expansion in recorded history dying of old age,” Klein said. “Are we near the tipping point? I don’t think so.”