Established by Congress through the Disaster Recovery Reform Act of 2018, the BRIC program has allocated more than $5 billion for investment in mitigation projects to reduce economic losses from floods, wildfires, and other disasters for hundreds of communities. Ending BRIC will cancel all applications from 2020-2023 and rescind more than $185 million in grants intended for Louisiana, leaving the 34 submitted and accepted projects funded by those grants in limbo.

Whereas the FEMA press release described BRIC as “wasteful and ineffective,” Cassidy identified “not doing the program and then having to rescue communities when the inevitable flood occurs – that is waste, because we could have prevented that from happening in the first place.”

A 2024 study backed by the U.S. Chamber of Commerce supports this claim, which found that disaster mitigation investments save $13 in benefits for every dollar spent.

FEMA’s decision coincides with recovery efforts in Natchitoches, a small Louisiana city, after flash flooding inundated homes and downed power lines just weeks before. BRIC was set to fund improvements to the city’s backup generator system to pump out floodwater during severe weather.

Similarly, Lafourche Parish will lose $20 million to strengthen 16 miles of power lines, which Cassidy noted toppled “like dominos” during last year’s Hurricane Francine. Jefferson Parish residents displaced following Hurricane Ida in 2021 will lose the home elevation disaster grants they finally secured earlier this year.

“Louisiana was the third-largest recipient of BRIC’s most recent round of funding and is the largest recipient on a per capita basis,” Cassidy said. “Without BRIC, none of these projects would be possible.”

A national problem

Beyond Louisiana, Cassidy pointed to numerous states ravaged by severe storms so far this year, particularly inland communities where flooding is traditionally unexpected. At least 25 people died amid a severe weather outbreak across the southern and midwestern U.S. last month, underscoring a growing need for resiliency planning in non-coastal areas.

BRIC is one of many programs facing sudden termination under the Trump Administration. Twenty-two states and the District of Columbia have filed a lawsuit demanding the federal government unfreeze essential funding, including BRIC grants. Though the administration is reportedly complying with a federal judge’s order blocking the freeze, the states involved claim funding remains inaccessible.

Louisiana has not joined the lawsuit, but Cassidy emphasized the congressional appropriation of the program and requested the fulfillment of preexisting BRIC applications. He argued that “to do anything other than use that money to fund flood mitigation projects is to thwart the will of Congress.”

As President Trump weighs disbanding FEMA entirely – even as FEMA responds to record-breaking numbers of billion-dollar disasters – it is imperative to recognize the vast co-beneficiary benefits of disaster resilience, and develop our partnerships across these stakeholder groups.

The Institutes’ Pete Miller and Francis Bouchard of Marsh McLennan discuss how AI is transforming property/casualty insurance as the industry attacks theclimate crisis.

“Climate” is not a popular word in Washington, D.C., today, so it would take a certain audacity to hold an event whose title prominently includes it in the heart of the U.S. Capitol.

For two days, expert panels at the Ronald Reagan Building and International Trade Center discussed climate-related risks – from flood, wind, and wildfire to extreme heat and cold – and the role of technology in mitigating and building resilience against them. Given the human and financial costs associated with climate risks, it was appropriate to see the property/casualty insurance industry strongly represented.

Peter Miller, CEO of The Institutes, was on hand to talk about the transformative power of AI for insurers, and Triple-I President and CEO Sean Kevelighan discussed – among other things – the collaborative work his organization and its insurance industry members are doing in partnership with governments, non-profits, and others to promote investment in climate resilience. Triple-I is an affiliate of the Institutes.

Sean Kevelighan of Triple-I and Denise Garth, Majesco’s chief strategy officer, discuss how to ensure equitable coverage against climate events.

You can get an idea of the scope and depth of these panels by looking at the agenda, which included titles like:

Building Climate-Resilient Futures: Innovations in Insurance, Finance, and Real Estate;

Fire, Flood, and Wind: Harnessing the Power of Advanced Data-Driven Technology for Climate Resilience;

The Role of Technology and Innovation to Advance Climate Resilience Across our Cities, States and Communities;

Pioneers of Parametric: Navigating Risks with Parametric Insurance Innovations;

Climate in the Crosshairs: How Reinsurers and Investors are Redefining Risk; and

Safeguarding Tomorrow: The Regulator’s Role in Climate Resilience.

As expected, the panels and “fireside chats” went deep into the role of technology; but the importance of partnership, collaboration, and investment across stakeholder groups was a dominant theme for all participants. Coming as the Trump Administration takes such steps as eliminating FEMA’s Building Resilient Infrastructure and Communities (BRIC) program; slashing budgets of federal entities like the National Oceanographic and Atmospheric Administration (NOAA) and the National Weather Service (NWS); and revoking FEMA funding for communities still recovering from last year’s devastation from Hurricane Helene, these discussions were, to say the least, timely.

Helge Joergensen, co-founder and CEO of 7Analytics, talks about using granular data to assess and address flood risk.

In addition to the panels, the event featured a series of “Shark Tank”-style presentations by Insurtechs that got to pitch their products and services to the audience of approximately 500 attendees. A Triple-I member – Norway-based 7Analytics, a provider of granular flood and landslide data – won the competition.

Earth Day 2025 is a good time to recognize organizations that are working hard and investing in climate-risk mitigation and resilience – and to recommit to these efforts for the coming years. What better place to do so than walking distance from both the White House and the Capitol?

The Trump Administration’s unwinding of the Building Resilient Infrastructure and Communities (BRIC) program and cancellation of all BRIC applications from fiscal years 2020-2023 reinforce the need for collaboration among state and local government and private-sector stakeholders in climate resilience investment.

Congress established BRIC through the Disaster Recovery Reform Act of 2018 to ensure a stable funding source to support mitigation projects annually. The program has allocated more than $5 billion for investment in mitigation projects to alleviate human suffering and avoid economic losses from floods, wildfires, and other disasters. FEMA announced on April 4 that it is ending BRIC .

Chad Berginnis, executive director of the Association of State Floodplain Managers (ASFPM), called the decision “beyond reckless.”

“Although ASFPM has had some qualms about how FEMA’s BRIC program was implemented, it was still a cornerstone of our nation’s hazard mitigation strategy, and the agency has worked to make improvements each year,” Berginnis said. “Eliminating it entirely — mid-award cycle, no less — defies common sense.”

While the FEMA press release called BRIC a “wasteful, politicized grant program,” Berginnis said investments in hazard mitigation programs “are the opposite of ‘wasteful.’ “ He pointed to a study by the National Institute of Building Sciences (NIBS) that showed flood hazard mitigation investments return up to $8 in benefits for every $1 spent.

“At this very moment, when states like Arkansas, Kentucky, and Tennessee are grappling with major flooding, the Administration’s decision to walk away from BRIC is hard to understand,” Berginnis said.

Heading into hurricane season

Especially hard hit will be catastrophe-prone Florida. Nearly $300 million in federal aid meant to help protect communities from flooding, hurricanes, and other natural disasters has been frozen since President Trump took office in January, according to an article in Government Technology.

The loss of BRIC funding leaves dozens of Florida projects in limbo, from a plan to raise roads in St. Augustine to a $150 million effort to strengthen canals in South Florida. According to Government Technology, the agency most impacted is the South Florida Water Management District, responsible for maintaining water quality, controlling the water supply, ecosystem restoration and flood control in a 16-county area that runs from Orlando south to the Keys.

“The district received only $6 million of its $150 million grant before the program was canceled,” the article said. “The money was intended to help build three structures on canals and basins in North Miami -Dade and Broward counties to improve flood mitigation.”

Florida’s Division of Emergency Management must return $36.9 million in BRIC money that was earmarked for management costs and technical assistance. Jacksonville will lose $24.9 million targeted to raise roads and make improvements to a water reclamation facility.

FEMA announced the decision to end BRIC the day after Colorado State University’s (CSU) Department of Atmospheric Science released a forecast projecting an above-average Atlantic hurricane season for 2025. Led by CSU senior research scientist and Triple-I non-resident scholar Phil Klotzbach CSU research team forecasts 17 named storms, nine hurricanes – four of them “major” (Category 3, 4, or 5). A typical season has 14 named storms, seven hurricanes – three of them major.

Nationwide impacts

More than $280 million in federal funding for flood protection and climate resilience projects across New York City — “including critical upgrades in Central Harlem, East Elmhurst, and the South Street Seaport” – is now at risk, according to an article in AMNY. The cuts affect over $325 million in pending projects statewide and another $56 million of projects where work has already begun.

Senate Majority Leader Chuck Schumer and Gov. Kathy Hochul warned that the move jeopardizes public safety as climate-driven disasters become more frequent and severe.

“In the last few years, New Yorkers have faced hurricanes, tornadoes, blizzards, wildfires, and even an earthquake – and FEMA assistance has been critical to help us rebuild,” Hochul said. “Cutting funding for communities across New York is short-sighted and a massive risk to public safety.”

According to the National Association of Counties, cancellation of BRIC funding has several implications for counties, including paused or canceled projects, budget and planning adjustments, and reduced capacity for long-term risk reduction.

North Dakota, for example, has 10 projects that were authorized for federal funding. Those dollars will now be rescinded. Impacted projects include $7.1 million for a water intake project in Washburn; $7.8 million for a regional wastewater treatment project in Lincoln; and $1.9 million for a wastewater lagoon project in Fessenden.

“This is devastating for our community,” said Tammy Roehrich, emergency manager for Wells County. “Two million dollars to a little community of 450 people is huge.”

The cancellation of BRIC roughly coincides with FEMA’s decision to deny North Carolina’s request to continue matching 100 percent of the state’s spending on Hurricane Helene recovery.

“The need in western North Carolina remains immense — people need debris removed, homes rebuilt, and roads restored,” said Gov. Josh Stein. “Six months later, the people of western North Carolina are working hard to get back on their feet; they need FEMA to help them get the job done.”

Resilience key to insurance availability

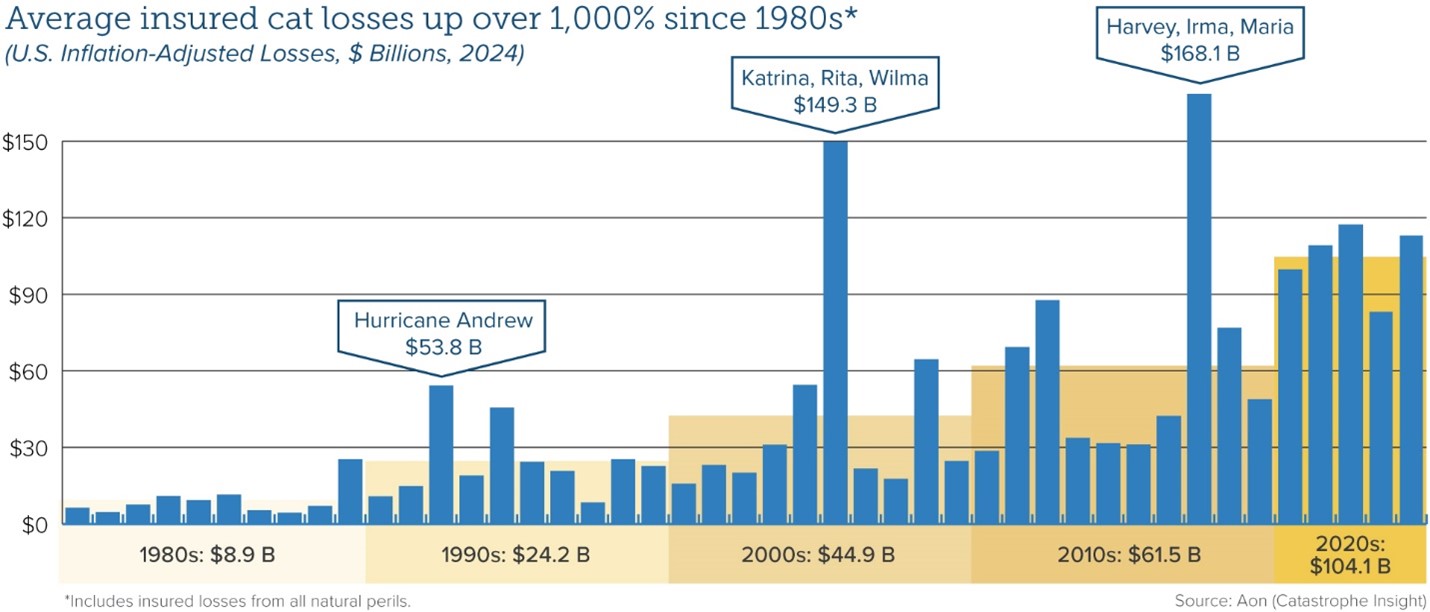

Average insured catastrophe losses have been on the rise for decades, reflecting a combination of climate-related factors and demographic trends as more people have moved into harm’s way.

“Investing in the resilience of homes, businesses, and communities is the most proactive strategy to reducing the damage caused by climate,” said Triple-I Chief Insurance Officer Dale Porfilio. “Defunding federal resilience grants will slow the essential investments being made by communities across the U.S.”

Flood is a particularly pressing problem, as 90 percent of natural disasters involve flooding, according to the National Flood Insurance Program (NFIP). The devastation wrought by Hurricane Helene in 2024 across a 500-mile swath of the U.S. Southeast – including Florida, Georgia, the Carolinas, Virginia, and Tennessee – highlighted the growing vulnerability of inland areas to flooding from both tropical and severe convective storms, as well as the scale of the flood-protection gap in non-coastal areas.

Coastal flooding in the U.S. now occurs three times more frequently than 30 years ago, and this acceleration shows no signs of slowing, according to recent research. By 2050, flood frequency is projected to increase tenfold compared to current levels, driven by rising sea levels that push tides and storm surges higher and further inland.

In addition to the movement of more people and property into harm’s way, climate-related risks are exacerbated by inflation (which drives up the cost of repairing and replacing damaged property); legal system abuse, (which delays claim settlements and drives up insurance premium rates); and antiquated regulations (like California’s Proposition 103) that discourage insurers from writing business in the states subject to them.

Thanks to the engagement and collaboration of a range of stakeholders, some of these factors in some states are being addressed. Others – for example, improved building and zoning codes that could help reduce losses and improve insurance affordability – have met persistent local resistance.

As frequently reported on this blog, the property/casualty insurance industry has been working hard with governments, communities, businesses, and others to address the causes of high costs and the insurance affordability and availability challenges that flow from them. Triple-I, its members, and partners are involved in several of these efforts, which we’ll be reporting on here as they progress.

Approximately 2.5 million Americans in 1.4 million homes will be at risk from severe coastal flooding by 2050, with Florida, New York, and New Jersey facing the highest exposure, according to a new report from Climate Central’s Coastal Risk Finder.

Coastal flooding in the U.S. now occurs three times more frequently than 30 years ago, and this acceleration shows no signs of slowing. By 2050, flood frequency is projected to increase tenfold compared to current levels, driven by rising sea levels that push tides and storm surges higher and further inland, according to the report.

The report defines a “severe flood” as one with a 1% chance of occurring in any given year. Such events, while statistically rare, can cause catastrophic damage to communities and infrastructure. The analysis incorporates the latest elevation data, levee information, sea level rise projections, and U.S. Census statistics to create comprehensive risk assessments.

Regional differences in risk exposure are significant. While the densely populated Northeast shows higher numbers of at-risk residents, the Gulf region faces greater land area vulnerability due to higher rates of sea level rise and naturally low-lying coasts.

Vulnerable Communities and Populations

Florida leads the nation with 505,000 residents projected to face risk from a severe coastal flood by 2050, followed by New York and New Jersey. At the municipal level, New York City tops the list with an estimated 271,000 people living in “high” at-risk areas. Among the cities with the highest exposure, six are located in the Northeast.

The report also highlighted a troubling demographic pattern: older adults face disproportionate exposure to coastal flood risks. Nearly 540,000 people aged 65 or older live in areas at risk of severe coastal flooding by 2050, representing 22% of the total at-risk population despite comprising only 16% of residents in coastal states. Florida has the highest number of vulnerable seniors with more than 143,000 at risk, while Maine, Oregon, and Delaware show the highest proportions of seniors living in flood-prone areas.

Social vulnerability—the combination of socioeconomic factors that worsen disaster impacts—further complicates the risk landscape. The report utilizes the U.S. Census Bureau’s Community Resilience Estimates to identify individuals with various risk components. Of the 2.5 million Americans in flood-risk zones, approximately 1.85 million (74%) have at least one component of risk, and 617,000 (25%) have three or more risk factors.

“Older adults, especially those living in care facilities, are among the most vulnerable to death and health setbacks due to hurricanes, storm surges, and other floods,” the report noted, emphasizing that age is just one of many factors contributing to vulnerability.

Tools and Adaptation Imperatives

The Coastal Risk Finder tool, which informed this report, offers detailed flood projections and risk assessments for any coastal state, county, city, town or district in the contiguous U.S. Developed following interviews with over 100 government officials, community leaders and researchers, the tool addresses the specific information needs of coastal communities.

Users can access customized maps, graphics and data to understand flood risks under different climate scenarios. The tool includes specific resources for media professionals, government officials and community leaders to help communicate and plan for worsening coastal flood risks.

The full range of demographic data, including social vulnerability metrics, is available for states, counties and cities through the Coastal Risk Finder, enabling communities to develop more targeted and equitable resilience plans.

Florida’s legislative reforms to address claim fraud and legal system abuse are stabilizing the state’s property/casualty insurance market, according to the latest Triple-I Issues Brief.

Claims-related litigation has significantly declined over the past two years, and premium averages are nearly flat, with several insurers requesting rate decreases from the state’s insurance regulator. In addition, the brief says, the number of insurers writing business in the state has rebounded after a multi-year exodus. This competition from the private market has allowed policyholders to leave Citizens Property Insurance Corp. – the state-run insurer of last resort – to obtain coverage at previously unavailable rates from a much healthier private market.

According to the state’s Office of Insurance Regulation (OIR), Florida in 2022 accounted for nearly 71 percent of the nation’s homeowners claim-related litigation, despite representing only 15 percent of homeowners insurance claims. The same year – before Hurricane Ian made landfall in Florida – six insurers in the state declared insolvency, primarily due to economic pressures from legal system abuse. Based on insured losses, Ian became the second-most costly U.S. hurricane on record, due in large part to extraordinary litigation costs for disputed claims.

The Legislature responded to the growing crisis by passing several pieces of insurance reform that, among other things, eliminated one-way attorney fees and assignment of benefits (AOB) for property insurance claims and prohibited misleading legal service ads and the misuse of consumer health information for legal services.

Premium rate growth slowing

The impact of the 2022 and 2023 reforms can be seen in premium rate changes, particularly with respect to homeowners insurance. Homeowners rates in Florida grew at a much slower rate in 2024, even as rate growth remained strong nationally. Growth in personal auto insurance premium rates in Florida has slowed since the repeal of AOB and one-way attorney fees, but the trend also is consistent with nationwide experience.

“There are a lot of factors involved in insurance rates, and Florida’s property and auto markets are challenging,” Florida Governor Ron DeSantis said in February, “but…data suggests that, in 2024, Florida had the lowest average homeowners’ premium increases in the nation, and the overall market has stabilized, with 11 new companies having entered the market over the past two years.”

Among the top 10 national insurers writing homeowners insurance in Florida, 60 percent have expanded their business over the past year, and 40 percent of all insurers operating in the state filed for rate decreases in 2024, according to Florida Insurance Commissioner Michael Yaworksy.

The cost of reinsurance also continues to decrease for Florida carriers.

“In 2024, most companies paid less for reinsurance than they did in 2023,” according to the OIR website. “The average risk-adjusted cost for 2024 was -0.7 percent, a large reduction from last year’s change of 27 percent increase from the prior year.”

Reinsurance costs are factored into premium rates, so this is another reason Florida now has the lowest average rate filings in the United States in 2024, according to S&P Global Marketplace.

Heading into 2025, countless communities are still grappling with the $27 billion natural disasters that impacted the United States last year – a total driven by costly storms and severe inland flooding. Many affected residents lacked flood coverage and will rely almost exclusively on federal relief funding to recover, underscoring a widespread protection gap.

Aiming to expedite disaster recovery for riverine communities in the Mississippi River Basin, the Mississippi River Cities and Towns Initiative (MRCTI) recently announced a flood insurance pilot currently in development with Munich Re that will use parametric insurance.

Unlike traditional indemnity insurance, parametric structures cover risks without sending adjusters to evaluate post-catastrophe damages. Rather than paying for specific damages incurred, parametric policies issue agreed-upon payouts if certain conditions are met – for example, if wind speeds or rainfall measurements meet an established threshold. Speed of payment and reduced administration costs can ease the burden on both insurers and policyholders, especially as weather and climate risks become more severe and unpredictable.

Several insurers demonstrated this efficiency in the wake of last year’s hurricanes – among them climate risk-management firm Arbol, which paid out $20 million in parametric reinsurance claims within 30 days after Milton made landfall.

Coast-to-coast trends

Though the MRCTI pilot presents a novel approach to inland flooding, similar pilots are already underway along the coast. New York City developed its own parametric flood program following Superstorm Sandy to bolster the resilience of low- and moderate-income neighborhoods struggling to recover. The program received enough funding last year not only for renewal but expansion, bringing needed protection to even more vulnerable communities.

For flood-prone Isleton, Calif. – a small Sacramento County town that lacks the resources to support a police department – risk mitigation has long taken a backseat to more immediate concerns. But the city’s location in a floodplain made it the perfect candidate for California’s parametric flood pilot, backed by a two-year, $200,000 grant going into effect this year.

The emergence of these community flood solutions reflects a growing interest in parametric insurance throughout the U.S., which propelled the $18 billion value of the global parametric insurance market in 2023. From Lloyd’s first dedicated parametric syndicate to Amwins’ parametric program for golf courses, more parametric coverage options are available than ever before, particularly after numerous private carriers – emboldened by improved data analytics and modeling – expanded their parametric flood insurance business in the U.S. last year.

Take FloodFlash, a leading parametric flood insurance provider based in London. Initially limited to five states, FloodFlash became known for offering coverage beyond the National Flood Insurance Program’s (NFIP) limits and in areas traditionally unsupported by private markets. Increased broker demand motivated the company, in partnership with Munich Re, to gradually roll out coverage to all mainland states last year, ahead of active hurricane season forecasts.

New insurance startups like Ric are also lowering the cost of entry into innovative parametric-based resilience. A winner of the RISE Flood Insurance of the Future Challenge, Ric will launch later this year on the coasts with micro-policies ranging from $14 to $50 per month. The company plans to collaborate with employers to extend their policies as employee benefits, which could help raise awareness of and reduce coverage gaps.

Regulatory momentum

As parametric risk transfer continues to gain traction, regulatory uncertainty in the absence of corresponding insurance laws persists. Given that many jurisdictions have structured their legal insurance framework around traditional indemnity principles, it’s unclear how restrained insurers in some areas are to issuing payouts only for actual losses.

Determining appropriate thresholds for coverage poses another challenge. For example, following extensive devastation from Hurricane Beryl last year, a $150 million parametric catastrophe bond did not yield a payout because air pressure levels narrowly missed the predefined minimum. The ensuing backlash included an intergovernmental “examination” into insurance-linked securities broadly and sparked industry-wide debate surrounding the equity of parametric structures.

To date, only a handful of states have enacted parametric insurance legislation, though substantial movement last year suggests more regulations are on the horizon. Notably, Vermont updated its previous 2022 law permitting captive insurance companies to enter parametric contracts. Based on evidence of their utility as insurance contracts, parametric contracts are now less restricted.

New York also unanimously passed its first parametric insurance law, recognizing parametric coverage as an authorized form of personal line insurance within the state. The law further stipulates mandatory disclosures on all parametric applications that distinguish parametric insurance as less comprehensive, and therefore not a substitute for, traditional property and flood insurance.

Such regulations are a promising step forward towards refining parametric coverage and facilitating its adoption across the country, but tensions between parametric and indemnity risk structures remain largely unresolved. Navigating how parametric insurance functions alone or as part of a package including indemnity coverage will require more collective input from all industry stakeholders.

One thing is for certain: traditional risk-transfer mechanisms are no longer sufficient to address the risk crisis presented by our evolving climate. Tools like parametric insurance – paired with hazard mitigation and community resilience planning – are guiding the way forward.

Babcock Ranch – a small community in southwestern Florida dubbed “The Hometown of Tomorrow” – made headlines for sheltering thousands of evacuees and never losing power during Hurricane Milton, which devastated numerous neighboring cities and left more than three million people without power.

Hunters Point, a subdivision on Florida’s Gulf Coast, remained similarly unscathed during both Hurricanes Helene and Milton. Though the development is only two years old, it’s already been through four major hurricanes. Its homes were designed with an elevation high enough to avoid severe flooding and materials that make them as sturdy as possible in high winds. When the power goes out, each home turns to its own solar panels and battery system.

For residents of both communities, this news comes as no surprise; their flood-resistant infrastructure and solar panel power systems have helped them survive several storms and hurricanes with only minor damages, demonstrating the utility of disaster resilience planning.

Such planning is expensive to implement. Homes in either community can run for over a million dollars. But, as the combined costs of Hurricanes Helene and Milton rise to the tens of billions, it’s hard to overstate the long-term benefits. Every dollar invested in disaster resilience could save 13 in property damage, remediation, and economic impact costs, suggesting risk mitigation and recovery strategies will become even more essential as natural catastrophe severity increases.

Incentivizing investment

The National Flood Insurance Program (NFIP) Community Rating System (CRS) – a voluntary program that rewards homeowners with reduced premiums when their communities invest in floodplain management practices that exceed NFIP minimum standards – aims to encourage resilience. Class 1 is the program’s highest rating, qualifying residents for a 45 percent reduction in their premiums. Of the nearly 23,000 participating NFIP communities, only 1,500 participate in the CRS. Of those 1,500, only two – Tulsa, Okla., and Roseville, Calif. – have achieved the highest rating.

High ratings are difficult to secure and maintain. Homeowners in Lee County, which borders Babcock Ranch, nearly lost their discounts earlier this year due to improper post-Hurricane Ian monitoring and documentation within flood hazard areas.

Discounts in lower-rated jurisdictions, however, still equate to large premium reductions. Miami-Dade County, Fla., for instance, earned a Class 3 rating after extensive stormwater infrastructure upgrades, saving the community an estimated $12 million annually. Residents sustained minimized flooding from Hurricane Milton under these improvements, further justifying their cost.

Local mitigation efforts offer targeted resilience solutions and resources to alleviate community risks. The insurance industry-funded Strengthen Alabama Homes provides homeowners grants to retrofit their houses along voluntary standards for constructing buildings resistant to severe weather. Completed retrofits reduce post-disaster claims and qualify grantees for substantial insurance premium discounts, prompting flood-prone Louisiana to replicate the program.

Other nature-based planning exploits local flora as a source of natural hazard protection. Previous studies support conserving natural wetlands and mangroves to impede the rate and flow of flooding, leading many communities – including Babcock Ranch, which is 90 percent wetlands – to invest in green infrastructure. Reforestation and wetland restoration projects undertaken by the Milwaukee Metropolitan Sewerage District (MMSD) also promise to store or capture millions of gallons of storm and flood water, enabling risk management alongside improved quality of life for citizens.

Most resilience projects are impossible to fund or operate without stakeholder partnerships and advanced data and analytics. Insurers, who have long assessed and measured catastrophe risk utilizing cutting-edge data tools, are uniquely positioned to confront these evolving risks and present a framework for successful preemptive mitigation.

Despite warnings from two leading insurance rating agencies that Hurricane Milton weakened or threatened Florida’s recovering home insurance market, the market “can manage losses” from the Category 4 storm “and are ready to cover yet another hurricane,” if one should come this season, according to industry experts who spoke with the South Florida Sun Sentinel.

AM Best and Fitch Ratings each issued reports last week warning that Milton could stretch liquidity of Florida-based residential insurers that are primarily focused on protecting in-state homeowners. But experts closer to Florida’s insurance industry cast doubt on those assertions. One reason is the two companies don’t rate most of the domestic Florida insurers whose financial strength they question, the Sun Sentinel reported.

While cautioning that loss estimates haven’t been released yet from catastrophe modelers, Florida market experts said the state’s insurers have sufficient reinsurance capital to weather not only hurricanes Debby, Helene, and Milton but another Milton-sized storm if one emerges during the latter portion of the 2024 Atlantic season.

Karen Clark, president of catastrophe modeler Karen Clark & Co., told the Sun Sentinel, “Florida insurers and the reinsurers that protect them use sophisticated tools to understand the probabilities of hurricane losses of different sizes.”

Joe Petrelli, president of Demotech – the only rating firm that reviews the financial health of most Florida-based property insurers – said insurers can purchase additional reinsurance capacity if they use up what they purchased to get them through the year.

“Carriers will have catastrophe reinsurance in place for another event, so it should not be an issue,” Petrelli told the Sun Sentinel.

“While we expect Milton to be a larger wind loss event compared to hurricanes Debby and Helene, we do not anticipate it to be near the level of insured losses caused by Hurricane Ian,” Mark Friedlander, Triple-I’s director of corporate communications said.

Ian was a Category 4 major hurricane that made landfall in Southwest Florida in September 2022 and caused an estimated $50 billion to $60 billion in private insured losses. The estimate accounted for up to $10 billion in litigated claims due to one-way attorney fees that were in effect at the time of the storm.

“The market is in its best financial condition in many years due to state legislative reforms in 2022 and 2023 that addressed the man-made factors which caused the Florida risk crisis – legal system abuse and claim fraud,” Friedlander said. “Florida residential insurers also have adequate levels of reinsurance to cover catastrophic loss events like Milton.”

Withdrawing federal subsidies in climate-vulnerable areas can deter development and promote disaster resilience, according to a recent Nature Climate Change study. The study found that these benefits extend beyond the targeted areas.

These findings underscore the utility of land conservation as hazard protection, as well as the critical role financial incentives play in driving – or obstructing – resilience.

A natural experiment

“Empirical research into this question is limited because few policy experiments exist where a clear comparison can be made of ‘treatment’ settings, where incentives for development have been removed, and ‘control’ settings, similar areas where such incentives remain,” the study states. “One such experiment does exist, however.”

The 1982 Coastal Barrier Resources Act (CBRA) rendered more than one million acres along U.S. coasts ineligible for various incentives, including access to flood insurance through the National Flood Insurance Program (NFIP). Though development in these high-risk areas remains legal, the CBRA shifts total responsibility onto property owners to manage that risk.

Decades later, areas under the CBRA have 83 percent fewer buildings per acre than similar non-designated areas, leading to higher development densities in less risky neighboring areas. Subsequent reductions in flood damages have generated hundreds of millions in NFIP savings per year – due not only to NFIP ineligibility in CBRA areas, but also to fewer and less costly flood claims filed in neighboring areas.

Neighboring areas benefit from the natural infrastructure provided by undeveloped wetlands, which can ease flood risk severity by impeding the rate and flow of flooding.

Housing demand a challenge

Despite the evident value of limiting development in high-risk areas, such limitations are challenging to implement during a nationwide affordable housing shortage. Navigating housing demands in tandem with a rise in natural disasters will require a coordinated effort on local, state, and federal levels.

One approach is FEMA’s Community Rating System (CRS), a voluntary program that incentivizes local floodplain management practices exceeding the NFIP’s minimum standards. Class 1 is the highest rating, qualifying residents for a 45 percent reduction in their premiums. Of the nearly 23,000 participating NFIP communities, only 1,500 participate in the CRS. Of those 1,500, only two have achieved the highest rating: Tulsa, Okla., and Roseville, Calif.

While high ratings are difficult to secure, investments in flood planning yield long-term gains via safer infrastructure and more affordable premiums, with discounts in lower-rated jurisdictions still equating to millions in savings.

CRS discounts are especially advantageous following NFIP’s Risk Rating 2.0 reforms and increased private-sector interest in flood risk. Both have contributed to a more representative and actuarially sound flood insurance market that sets rates based on property-specific risks, thereby raising the premiums of riskier property owners.

Concerns about effective climate risk mitigation strategies persist, however – especially in the wake of unprecedented destruction wrought by Hurricane Helene.

While NFIP reforms are making flood insurance more equitable, many homeowners – including many of those most impacted by Hurricane Helene – are unaware that flood coverage is not offered by a standard homeowners policy. Likewise, many believe that flood insurance is necessary only if required by their lenders, leaving inland residents more susceptible to costly flood damages.

This lack of common knowledge about insurance is not a failure of consumers – rather, it represents the insurance industry’s urgent need to provide greater outreach, public education, and stakeholder collaboration.

Incentivizing public-private collaboration has demonstrated success, so removing federal incentives from additional high-risk areas would require extensive multidisciplinary coordination to prevent inadvertently widening the insurance protection gap. Emerging approaches to risk mitigation and resilience – such as community-based catastrophe insurance, New York City’s recent parametric insurance flood pilot, and the nation’s first public wildfire catastrophe model in California – offer opportunities for fairer rates and targeted local resilience.

If paired with policies based on the CBRA, such innovations could help ensure that appropriate risk transfer occurs alongside substantial risk reduction.

As work continues to address the harm inflicted by Hurricane Helene, researchers at Colorado State University (CSU) warn that the next two weeks “will be characterized by [tropical storm] activity at above normal levels.”

The CSU researchers define “above normal” by accumulated cyclone energy (ACE) of more than 10. This level of hurricane intensity has been reached in less than one-third of two-week periods in early October since records have been kept.

Hurricane Kirk, they wrote, is “extremely likely” to generate more than 10 ACE during its lifetime in the eastern/central Atlantic. Tropical Depression 13 has just formed and is likely to generate considerable ACE in its lifetime across the Atlantic. The National Hurricane Center is monitoring an additional area for formation in the Gulf of Mexico that should be monitored for potential U.S. impacts.

“Hurricane Kirk is forecast to track northwestward across the open Atlantic over the next few days, likely becoming a powerful major hurricane in the process,” said CSU research scientist and Triple-I Non-resident Scholar Phil Klotzbach. “The system looks to generate approximately an additional 20 ACE before dissipation, effectively guaranteeing the above-normal category for the two-week period.”

With more than 160 people confirmed dead in Florida, Georgia, South Carolina, North Carolina, Virginia, and Tennessee, Helene is now the second-deadliest hurricane to strike the mainland United States in the past 55 years, topped only by Hurricane Katrina in 2005.

Reinsurance broker Gallagher Re predicts that private insurance market losses from Helene will rise to the mid-to-high single-digit billion dollar level, higher than its pre-landfall forecast of $3 billion to $6 billion, according to Chief Science Officer and Meteorologist Steve Bowen.

As always – and with particular urgency in the wake of Helene’s devastation – Triple-I urges everyone in hurricane-prone areas to stay informed, be prepared, and follow the instructions of local authorities. We also ask that people be mindful of the potential for flood danger far inland, as reflected in the experiences of many non-coastal communities during Hurricane Ida and Helene.