By Lewis Nibbelin, Research Writer, Triple-I

With last week’s end of the longest U.S. government shutdown in history, Congress reauthorized FEMA’s National Flood Insurance Program (NFIP).

During the shutdown, the NFIP continued to pay claims using available funds, but it could not sell or renew policies until reauthorized. These restrictions affected an estimated 1,300 property sales each day, as prospective property owners must purchase flood coverage in Special Flood Hazard Areas (SFHA), where private flood options – despite gaining traction – are still limited.

With millions of homeowners and countless communities relying on the NFIP, many organizations across the risk and insurance industry sent a letter urging congressional leaders to reauthorize NFIP ahead of its expiration, writing that a lapse “could further impact affordable housing, create additional challenges for small businesses, unnecessarily further increase the cost of homeownership, and must be avoided.”

While reauthorization allows NFIP insurers to retroactively issue policies for applications received during the shutdown, the measure extends their authority only through Jan. 30, 2026, leaving the program’s fate an open question. Absent a long-term NFIP authorization bill, Congress has now reauthorized the program 34 times since fiscal year 2017.

Incentivizing risk reduction

Flood risk was long considered untouchable by private insurers, which is a large part of the reason NFIP exists. While private participation in the flood market has grown in recent years, NFIP remains a critical source of protection for this growing and underinsured peril.

Beyond providing economic protection for policyholders, the NFIP also plays a critical role in promoting climate resilience, particularly through its Community Rating System (CRS). A voluntary program, the CRS rewards homeowners with premium discounts when their communities invest in floodplain management practices that exceed the NFIP’s minimum standards, with the program’s highest rating qualifying residents for a 45 percent premium reduction.

After the cancellation of other FEMA-managed initiatives like BRIC, the CRS can help provide relief where still needed. For instance, Jefferson Parish homeowners displaced following Hurricane Ida in 2021 had secured BRIC grants to elevate and reconstruct their homes shortly before the program ended, leaving these projects in limbo. But the CRS now offers residents and businesses more than $12 million in flood insurance savings annually after the parish secured a Class 3 rating – the first of its kind in Louisiana.

By incentivizing improved building codes, citizen awareness campaigns, and other resilience solutions, the CRS can ensure that vulnerable communities “will continue to benefit from a comprehensive floodplain management and mitigation plan that helps make us more resilient in the face of disasters,” said Jefferson Parish President Cynthia Lee Sheng in a statement. Notably, however, the parish earned its rating mere weeks ahead of the NFIP lapse, which delayed the discounts from appearing in new and renewed policies.

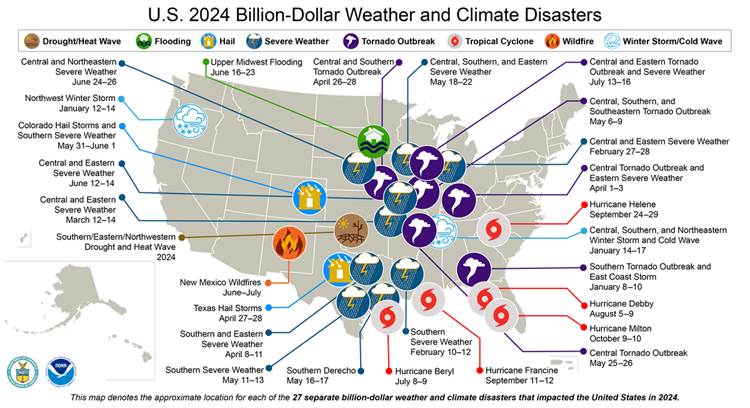

As climate and weather-related events become increasingly frequent and severe, the success of these investments will depend on proactive strategies informed by timely, granular data. Though NOAA announced it would cease tracking the country’s costliest disasters earlier this year, nonprofit Climate Central aims to fill the gap by rebuilding NOAA’s database and expanding it to track smaller catastrophes, providing insurers and other stakeholders more reliable information to understand individual disasters.

Taken together, such efforts can help insurers accurately reflect rising risks in insurance pricing while engaging with communities and businesses in solutions to keep coverage accessible. Sustaining this balance involves continuous collaboration between public and private sectors.

Learn More:

JIF 2025: Federal Cuts Imperil Resilience Efforts

Some Weather Service Jobs Being Restored; BRIC Still Being Litigated

Louisiana Senator Seeks Resumption of Resilience Investment Program

Nonprofit to Rescue NOAA Billion-Dollar Dataset

BRIC Funding Loss Underscores Need for Collective Action on Climate Resilience

Hurricane Helene Highlights Inland Flood Protection Gap

Executive Exchange: Using Advanced Tools to Drill Into Flood Risk

Accurately Writing Flood Coverage Hinges on Diverse Data Sources

Lee County, Fla., Towns Could Lose NFIP Flood Insurance Discounts